2

FORWARD-

LOOKING

STATEMENT

This presentation isnot intended to provide investment or medical advice. It should be noted that some products under development described

herein have not been found safe or effective by any regulatory agency and are not approved for any use outside of clinical trials.

This presentation contains forward-looking statements, which express the current beliefs and expectations of Kamada’s management. Such

statements include 2025 financial guidance; growth strategy and plans for double digit growth; growth prospects related to CYTOGAM®,

GLASSIA®, and the Israeli distribution business segment; success in identifying and integrating M&A targets for growth; advancement and future

expected revenues driven by our plasma collection operation; and continued progression of the inhaled AAT clinical study, its benefits and

advantages, potential market size, reduction of the study sample to approximately 180 patients, and the plan to conduct an interim futility

analysis by the end of 2025. These statements involve a number of known and unknown risks and uncertainties that could cause Kamada's

future results, performance or achievements to differ significantly from the projected results, performances or achievements expressed or

implied by such forward-looking statements. Important factors that could cause or contribute to such differences include, but are not limited to,

risks relating to Kamada's ability to successfully develop and commercialize its products and product candidates, progress and results of any

clinical trials, introduction of competing products, continued market acceptance of Kamada’s commercial products portfolio, impact of geo-

political environment in the middle east, impact of any changes in regulation and legislation that could affect the pharmaceutical industry,

difficulty in predicting, obtaining or maintaining U.S. Food and Drug Administration, European Medicines Agency and other regulatory authority

approvals, restrains related to third parties’ IP rights and changes in the health policies and structures of various countries, success of M&A

strategies, environmental risks, changes in the worldwide pharmaceutical industry and other factors that are discussed under the heading “Risk

Factors” of Kamada’s 2024 Annual Report on Form 20-F (filed on March 5, 2025), as well as in Kamada’s recent Forms 6-K filed with the U.S.

Securities and Exchange Commission.

This presentation includes certain non-IFRS financial information, which is not intended to be considered in isolation or as a substitute for, or

superior to, the financial information prepared and presented in accordance with IFRS. The non-IFRS financial measures may be calculated

differently from, and therefore may not be comparable to, similarly titled measures used by other companies. In accordance with the

requirement of the SEC regulations a reconciliation of these non-IFRS financial measures to the comparable IFRS measures is included in an

appendix to this presentation. Management uses these non-IFRS financial measures for financial and operational decision-making and as a

means to evaluate period-to-period comparisons. Management believes that these non-IFRS financial measures provide meaningful

supplemental information regarding Kamada’s performance and liquidity.

Forward-looking statements speak only as of the date they are made, and Kamada undertakes no obligation to update any forward-looking

statement to reflect the impact of circumstances or events that arise after the date the forward-looking statement was made, except as required

by applicable law.

3.

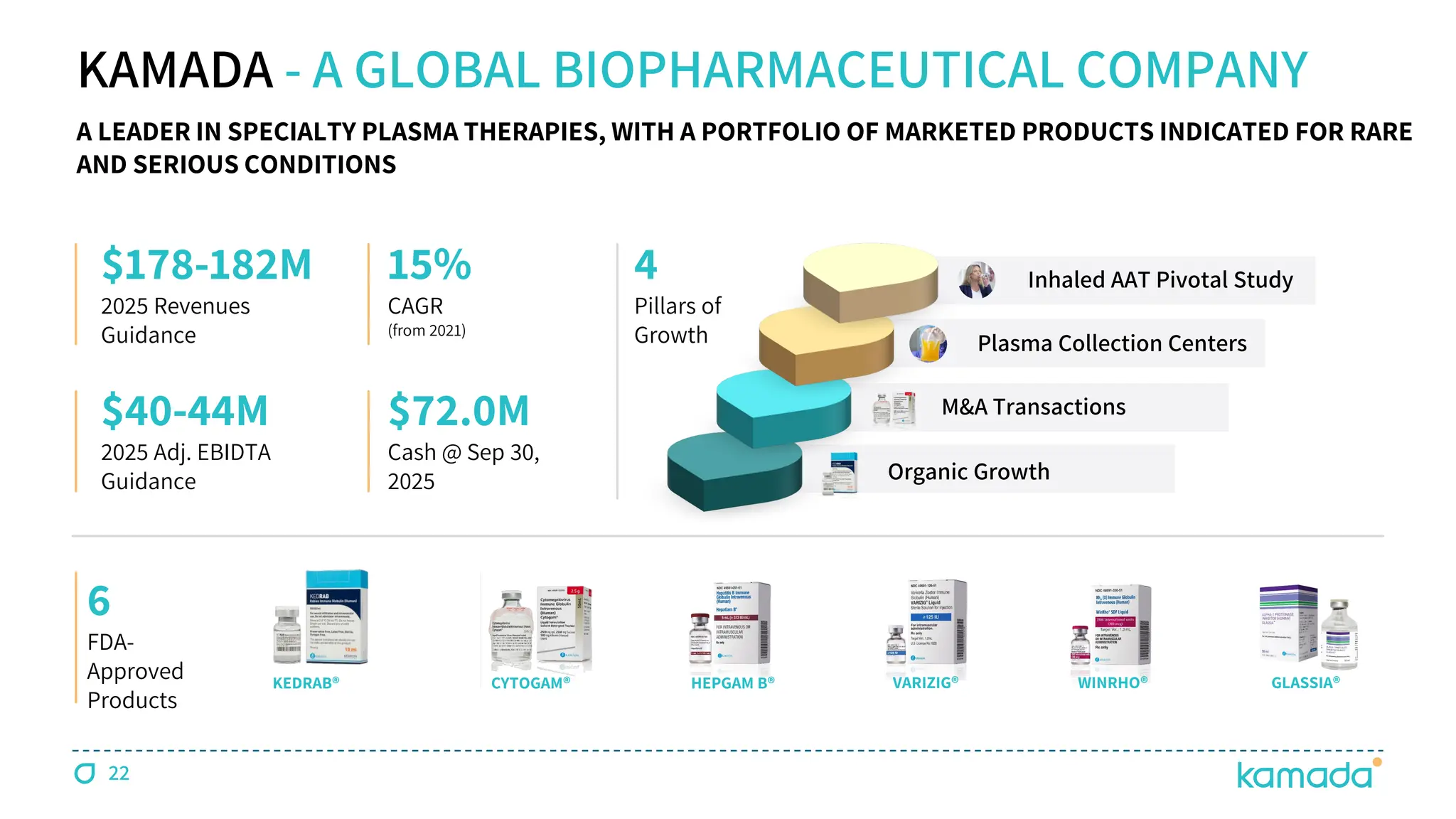

KEDRAB® CYTOGAM® HEPGAMB® VARIZIG® WINRHO® GLASSIA®

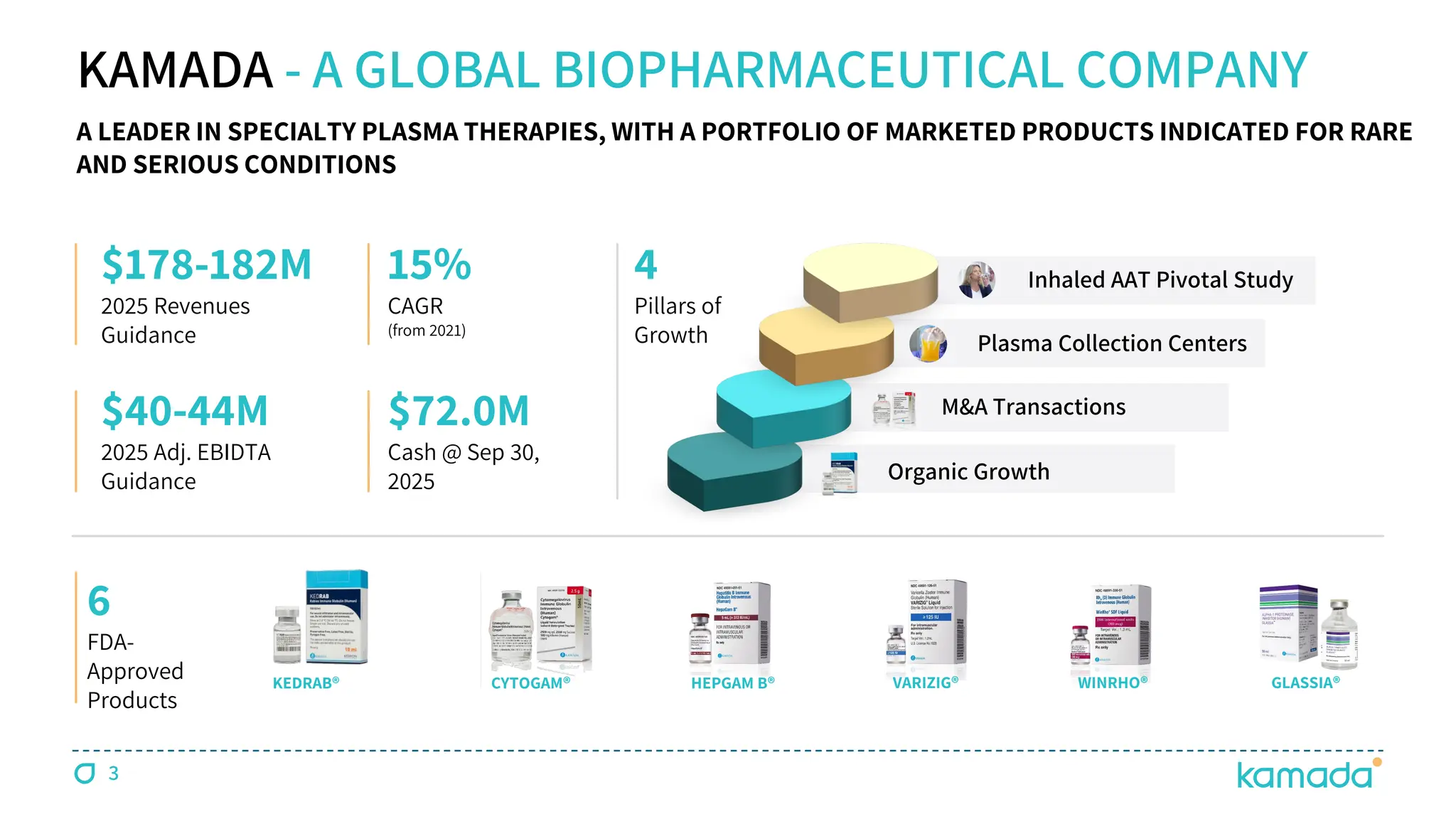

KAMADA - A GLOBAL BIOPHARMACEUTICAL COMPANY

6

FDA-

Approved

Products

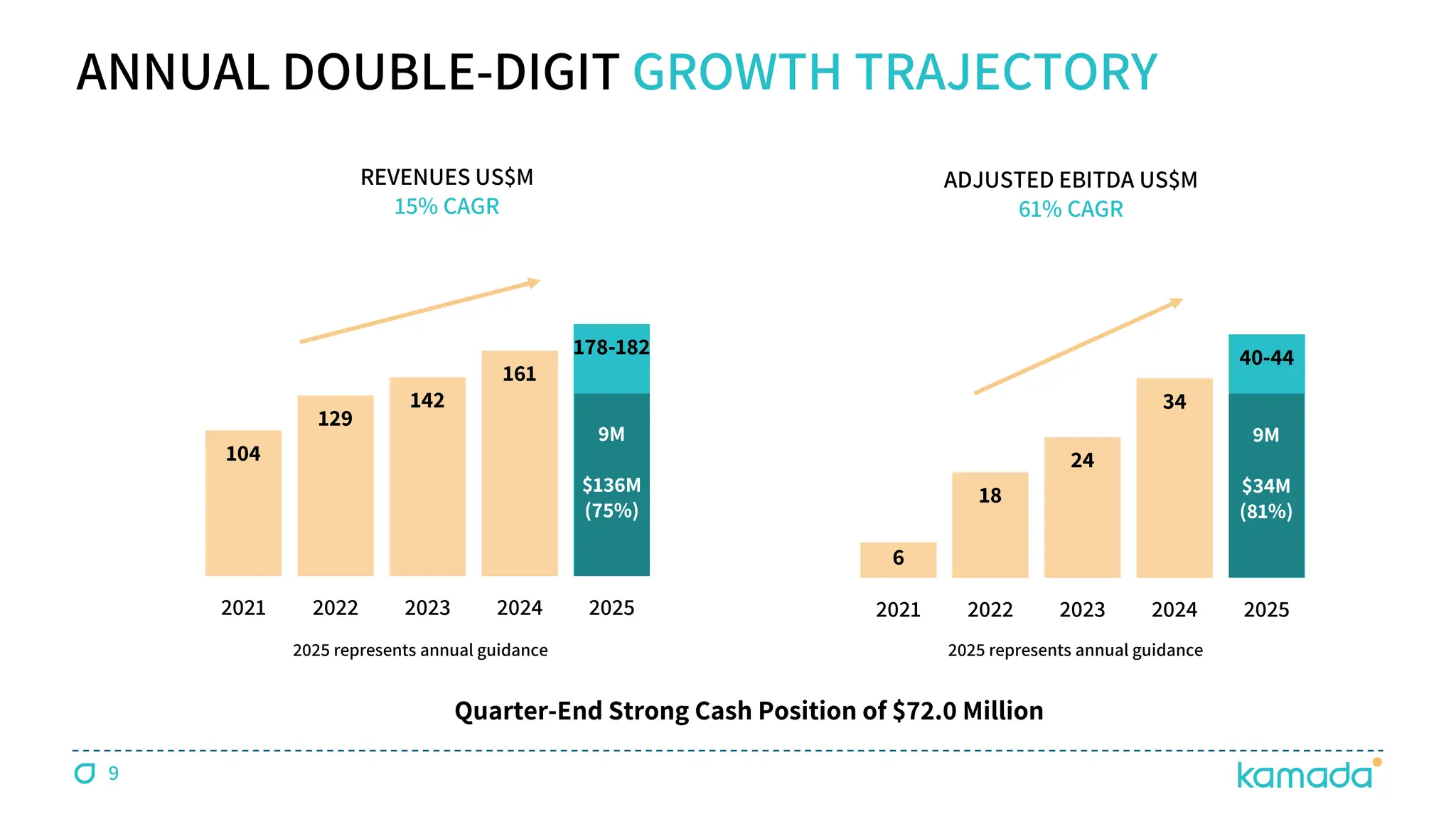

15%

CAGR

(from 2021)

$178-182M

2025 Revenues

Guidance

$40-44M

2025 Adj. EBIDTA

Guidance

4

Pillars of

Growth

A LEADER IN SPECIALTY PLASMA THERAPIES, WITH A PORTFOLIO OF MARKETED PRODUCTS INDICATED FOR RARE

AND SERIOUS CONDITIONS

$72.0M

Cash @ Sep 30,

2025

3

Organic Growth

M&A Transactions

Inhaled AAT Pivotal Study

Plasma Collection Centers

4.

4

6 FDA-APPROVED SPECIALTYPLASMA PRODUCTS

KEDRAB®

[Rabies Immune

Globulin (Human)]

Post exposure prophylaxis

of rabies infection

CYTOGAM®

[Cytomegalovirus

Immune Globulin (Human)]

Prophylaxis of CMV

disease associated

with transplants

HEPGAM B®

[Hepatitis B Immune

Globulin (Human)]

Prevention of HBV

recurrence following

liver transplants

VARIZIG®

[Varicella Zoster Immune

Globulin (Human)]

Post-exposure prophylaxis

of varicella

in high- risk patients

WINRHO®

[Rho(D) Immune

Globulin (Human)]

Treatment of ITP &

suppression of Rh

isoimmunization (HDN)

KEY FOCUS ON TRANSPLANTS & RARE CONDITIONS

For Important Safety Information, visit www.Kamada.com

GLASSIA®

[Alpha1-Proteinase

Inhibitor (Human)]

Augmentation therapy

for Alpha-1 Antitrypsin

Deficiency (AATD)

5.

5

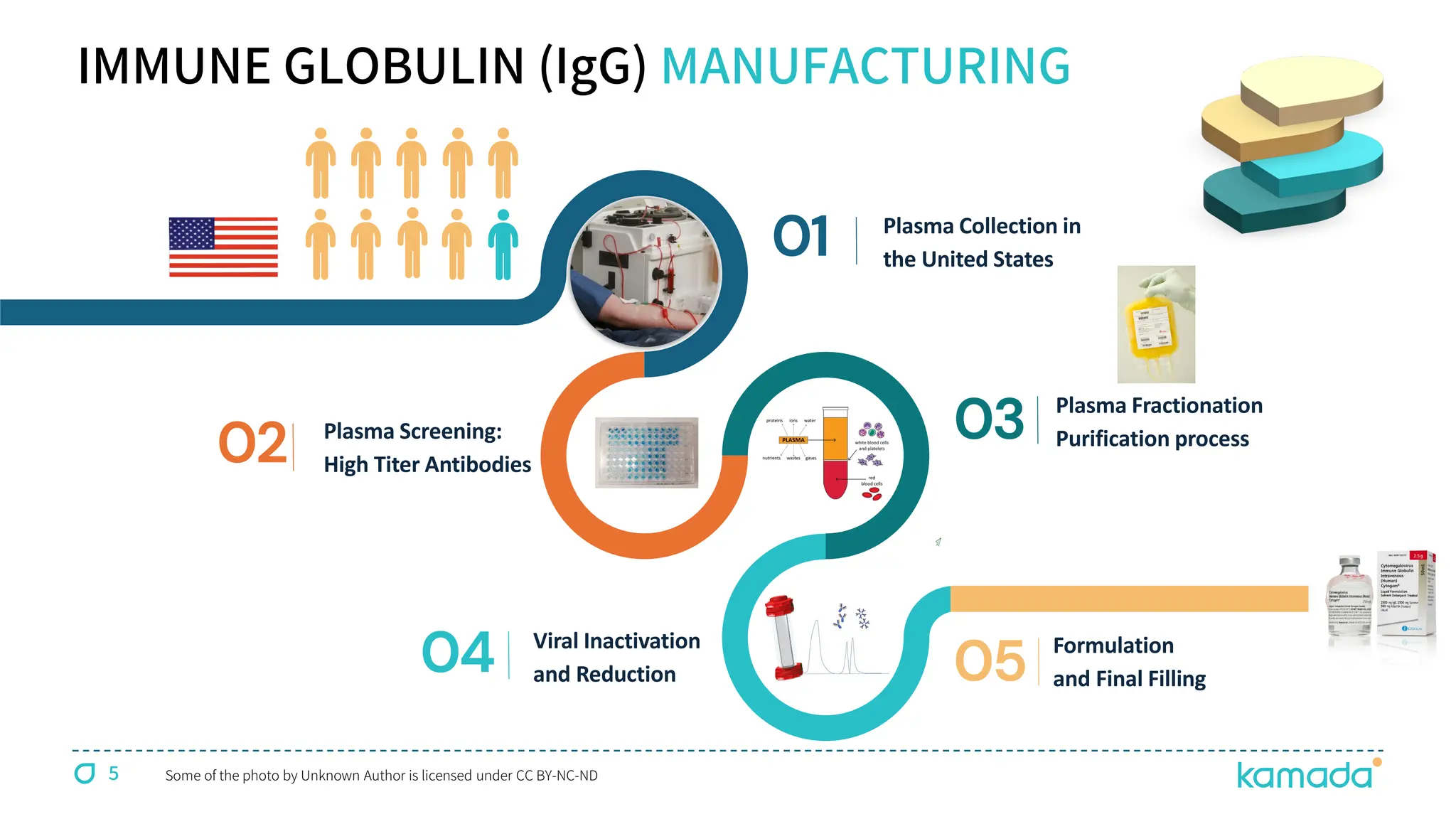

IMMUNE GLOBULIN (IgG)MANUFACTURING

Some of the photo by Unknown Author is licensed under CC BY-NC-ND

02 Plasma Screening:

High Titer Antibodies

03 Plasma Fractionation

Purification process

01 Plasma Collection in

the United States

04 Viral Inactivation

and Reduction 05 Formulation

and Final Filling

6.

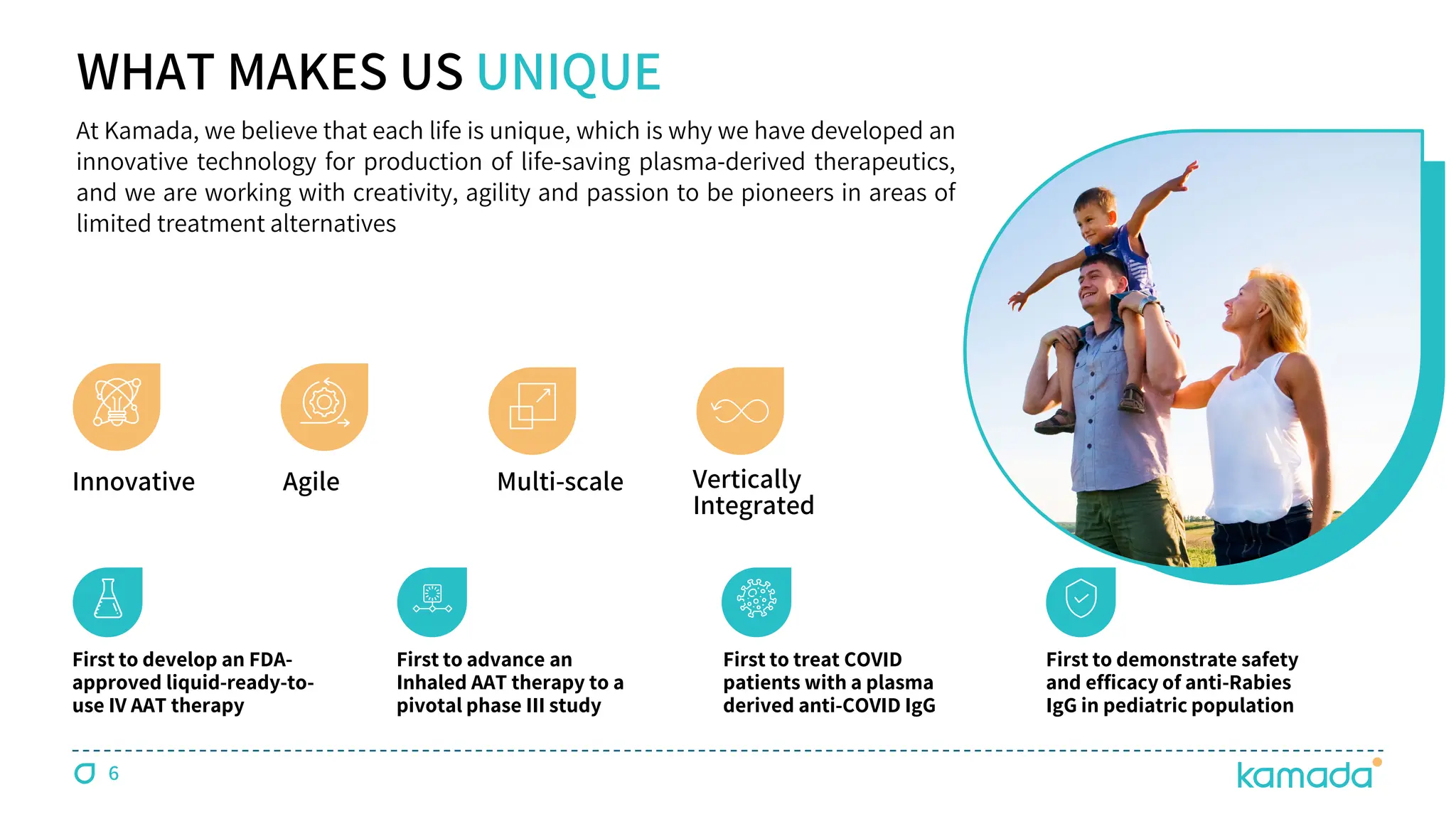

Multi-scale

Innovative Agile

WHAT MAKESUS UNIQUE

First to develop an FDA-

approved liquid-ready-to-

use IV AAT therapy

First to advance an

Inhaled AAT therapy to a

pivotal phase III study

First to demonstrate safety

and efficacy of anti-Rabies

IgG in pediatric population

First to treat COVID

patients with a plasma

derived anti-COVID IgG

Vertically

Integrated

At Kamada, we believe that each life is unique, which is why we have developed an

innovative technology for production of life-saving plasma-derived therapeutics,

and we are working with creativity, agility and passion to be pioneers in areas of

limited treatment alternatives

6

7.

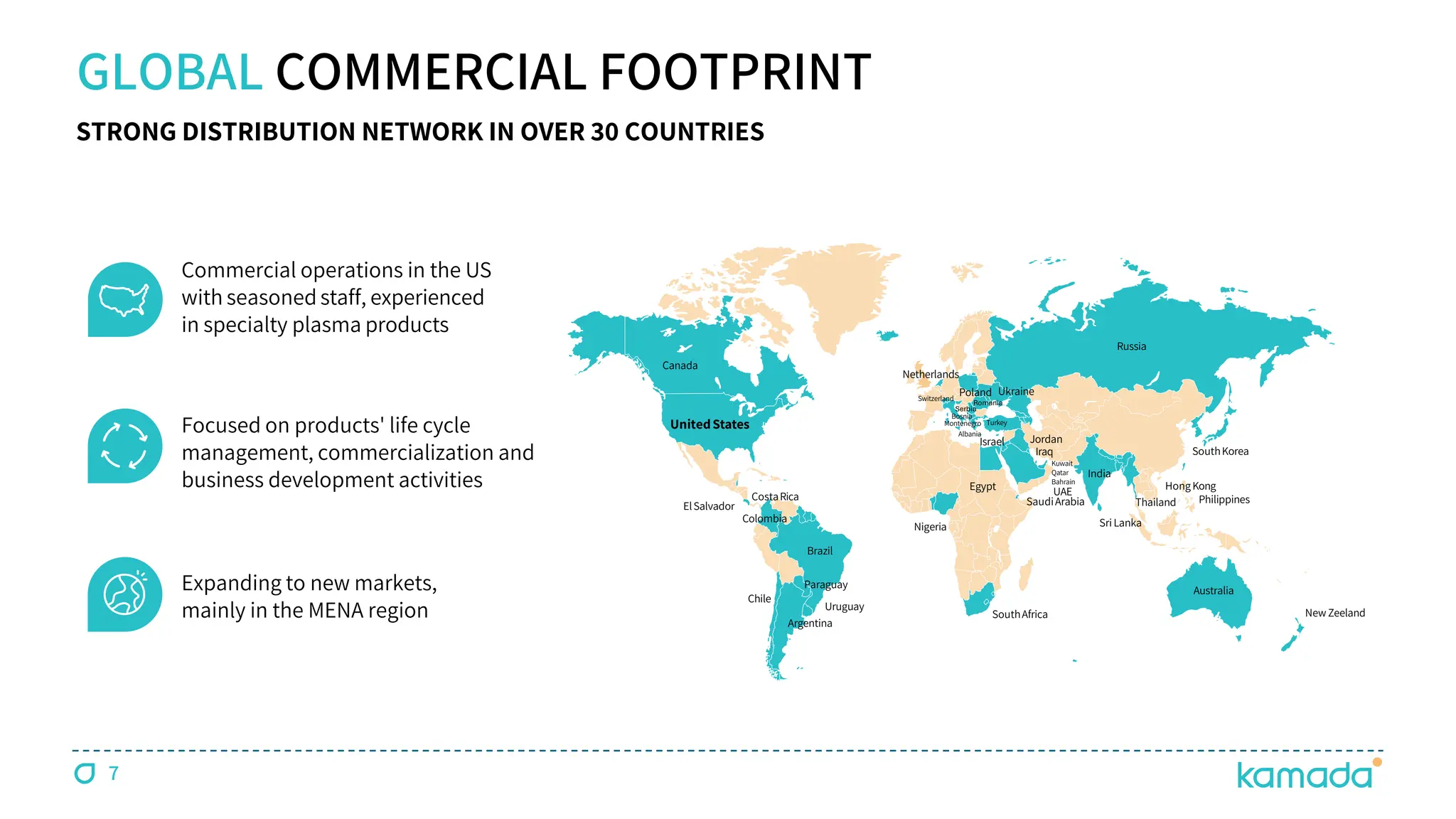

GLOBAL COMMERCIAL FOOTPRINT

UnitedStates

ElSalvador

Brazil

Nigeria

India

SouthKorea

Russia

Israel

Chile

Thailand

SriLanka

Australia

SouthAfrica

Uruguay

Argentina

Paraguay

Colombia

Canada

Hong Kong

SaudiArabia

Kuwait

Qatar

Bahrain

UAE

Egypt

Philippines

Jordan

Iraq

Netherlands

Montenegro

Albania

Turkey

CostaRica

NewZeeland

Ukraine

Poland

Bosnia

Expanding to new markets,

mainly in the MENA region

Commercial operations in the US

with seasoned staff, experienced

in specialty plasma products

Focused on products' life cycle

management, commercialization and

business development activities

STRONG DISTRIBUTION NETWORK IN OVER 30 COUNTRIES

7

Switzerland

Serbia

Romania

8.

8

EXPERIENCED LEADERSHIP

Amir London

CEO

HanniNeheman

VP Marketing

& Sales

Liron Reshef

VP Human Resources

Shavit Beladev

VP Kamada

Plasma

Chaime Orlev

CFO

Jon Knight

VP U.S Commercial

Yael Brenner

VP Quality

Boris Gorelik

VP Business Development

& Strategic Programs

Nir Livneh

VP Legal, General Counsel

& Corporate Secretary

Eran Nir

COO

Orit Pinchuk

VP Regulatory

Affairs & PVG

WITH PROVEN TRACK RECORD

10

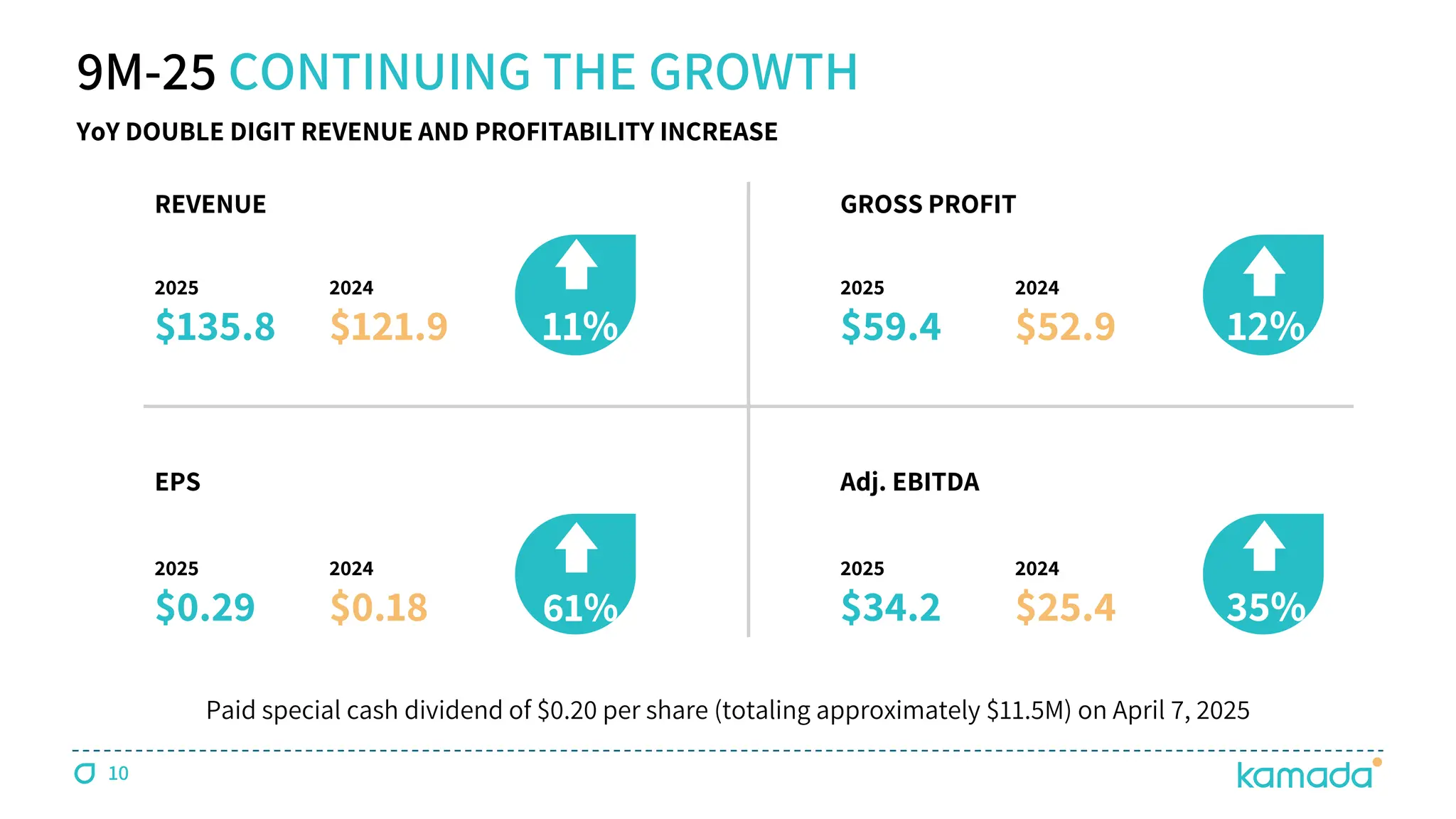

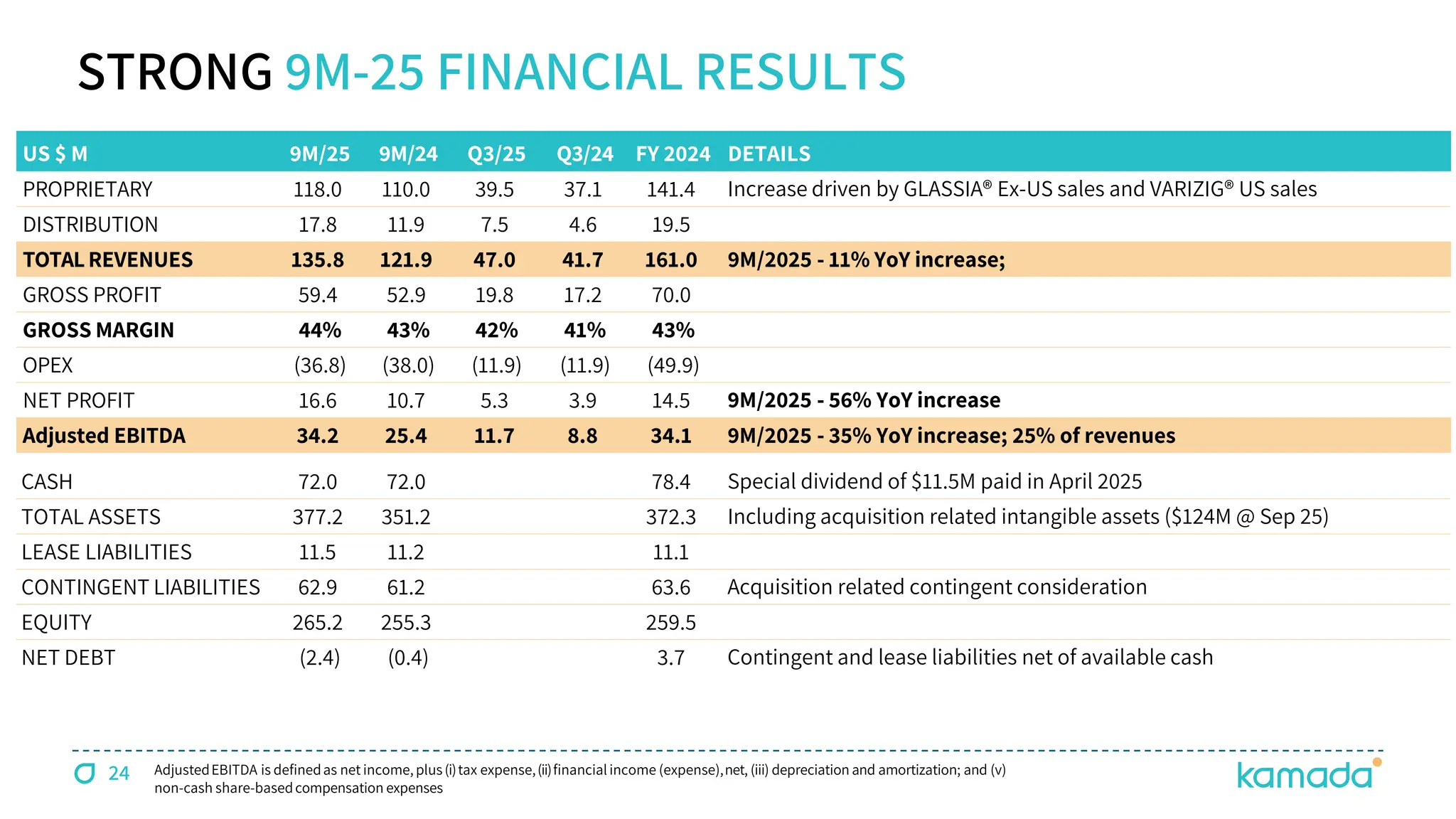

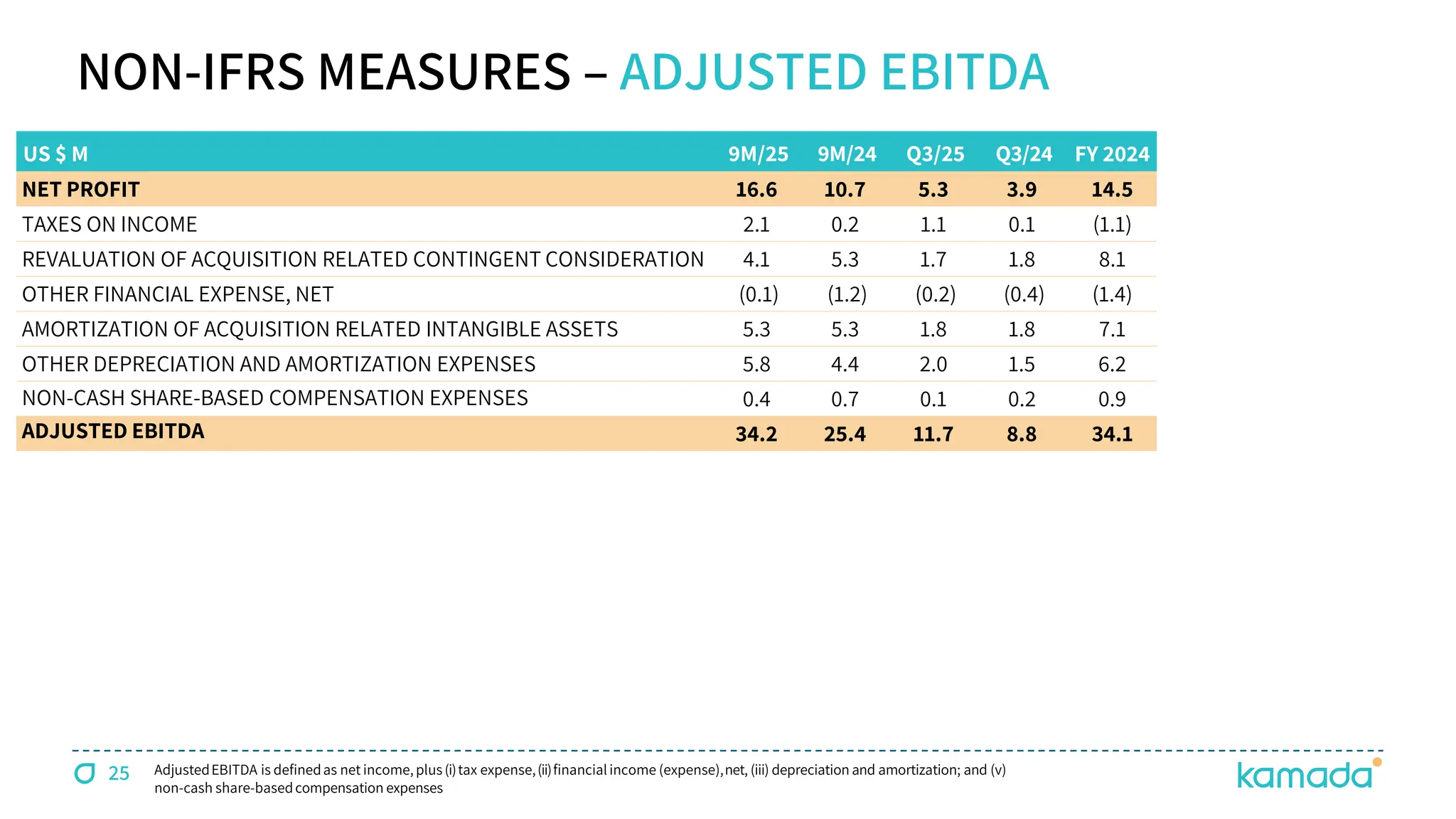

9M-25 CONTINUING THEGROWTH

YoY DOUBLE DIGIT REVENUE AND PROFITABILITY INCREASE

Paid special cash dividend of $0.20 per share (totaling approximately $11.5M) on April 7, 2025

REVENUE GROSS PROFIT

2025

$135.8

2024

$121.9 11%

2025

$59.4

2024

$52.9 12%

EPS Adj. EBITDA

2025

$0.29

2024

$0.18 61%

2025

$34.2

2024

$25.4 35%

11.

11

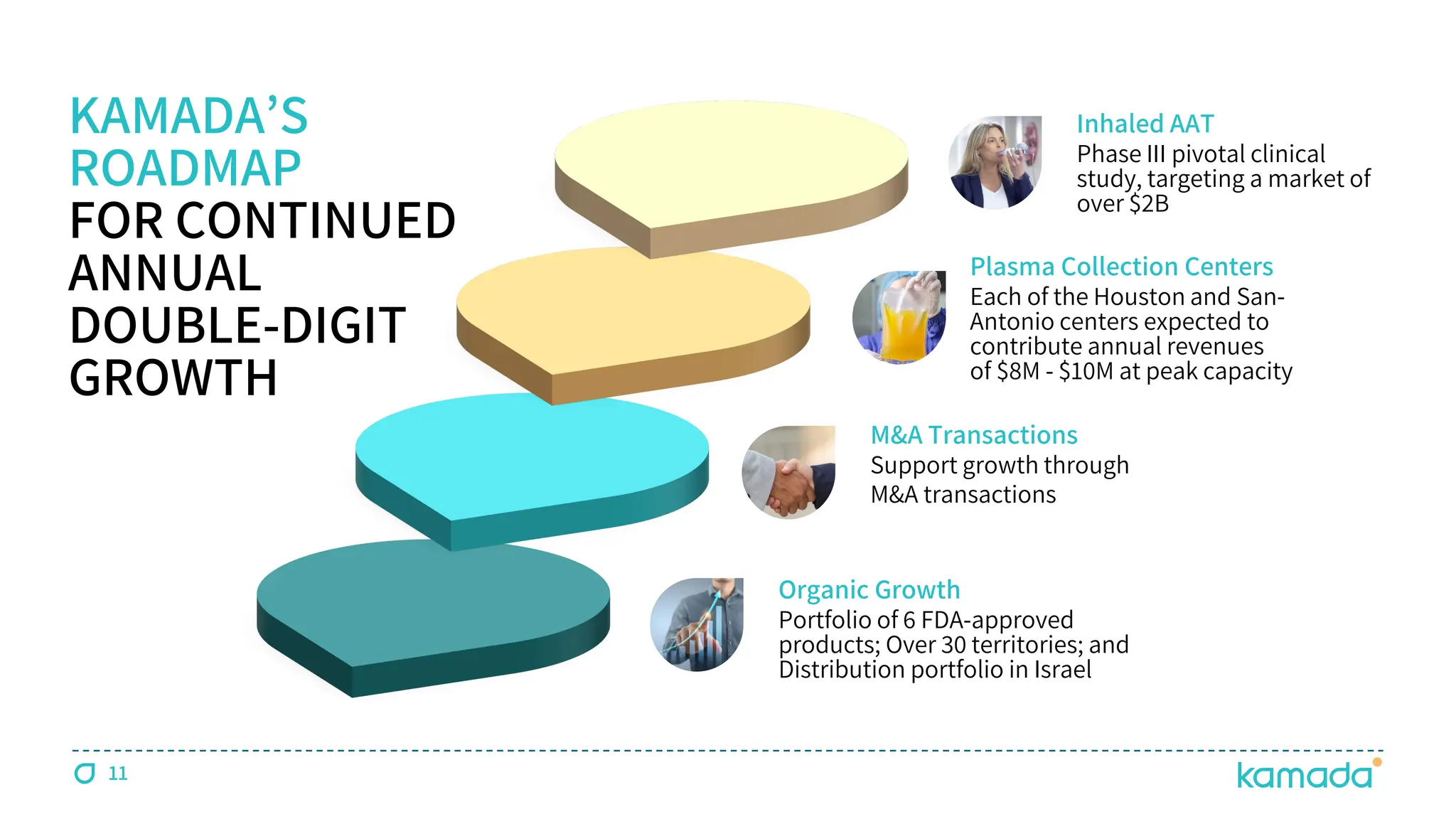

KAMADA’S

ROADMAP

FOR CONTINUED

ANNUAL

DOUBLE-DIGIT

GROWTH

Organic Growth

Portfolioof 6 FDA-approved

products; Over 30 territories; and

Distribution portfolio in Israel

M&A Transactions

Support growth through

M&A transactions

Plasma Collection Centers

Each of the Houston and San-

Antonio centers expected to

contribute annual revenues

of $8M - $10M at peak capacity

Inhaled AAT

Phase III pivotal clinical

study, targeting a market of

over $2B

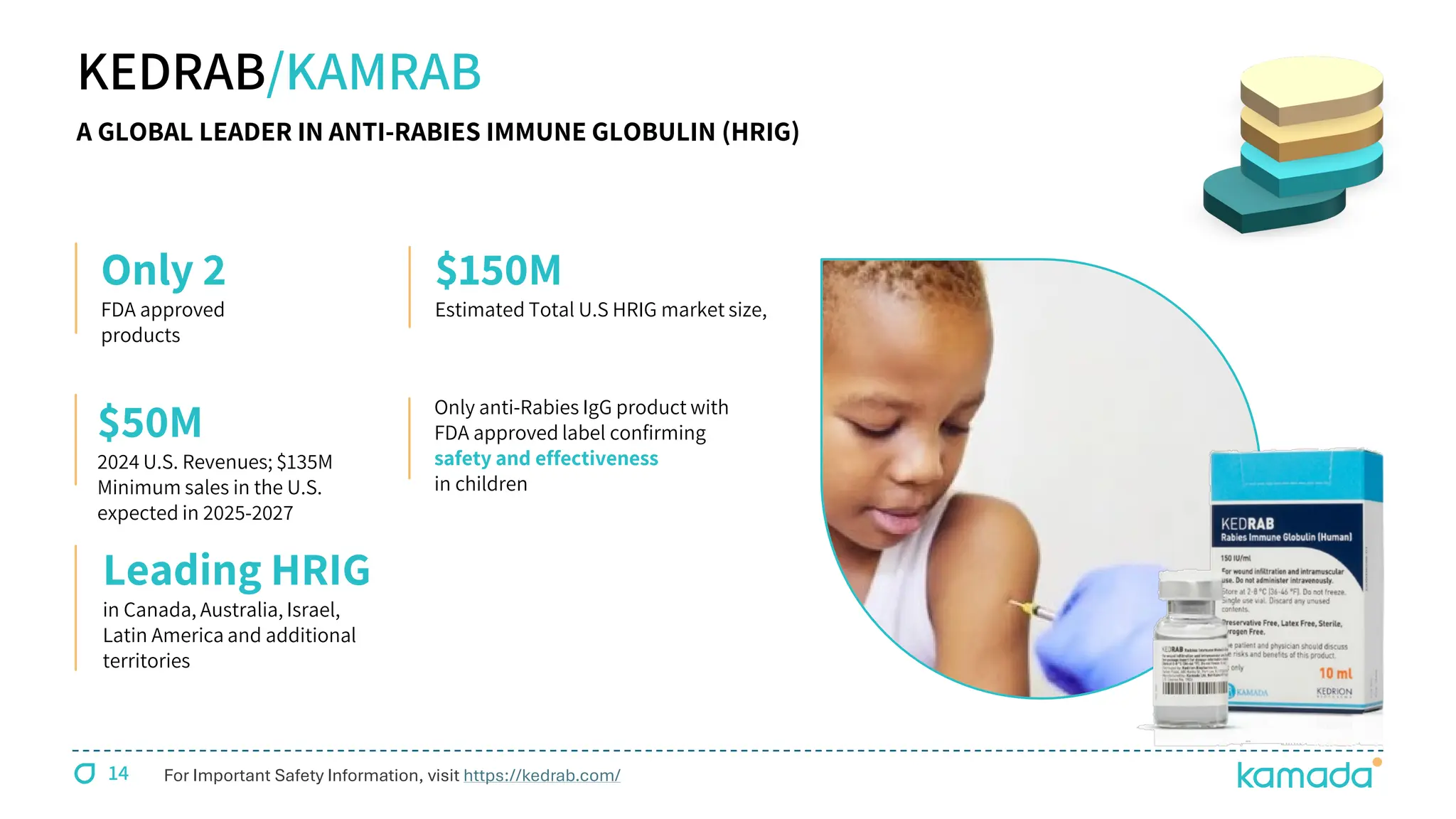

$150M

Estimated Total U.SHRIG market size,

Only anti-Rabies IgG product with

FDA approved label confirming

safety and effectiveness

in children

KEDRAB/KAMRAB

$50M

2024 U.S. Revenues; $135M

Minimum sales in the U.S.

expected in 2025-2027

Only 2

FDA approved

products

Leading HRIG

in Canada, Australia, Israel,

Latin America and additional

territories

A GLOBAL LEADER IN ANTI-RABIES IMMUNE GLOBULIN (HRIG)

For Important Safety Information, visit https://kedrab.com/

14

15.

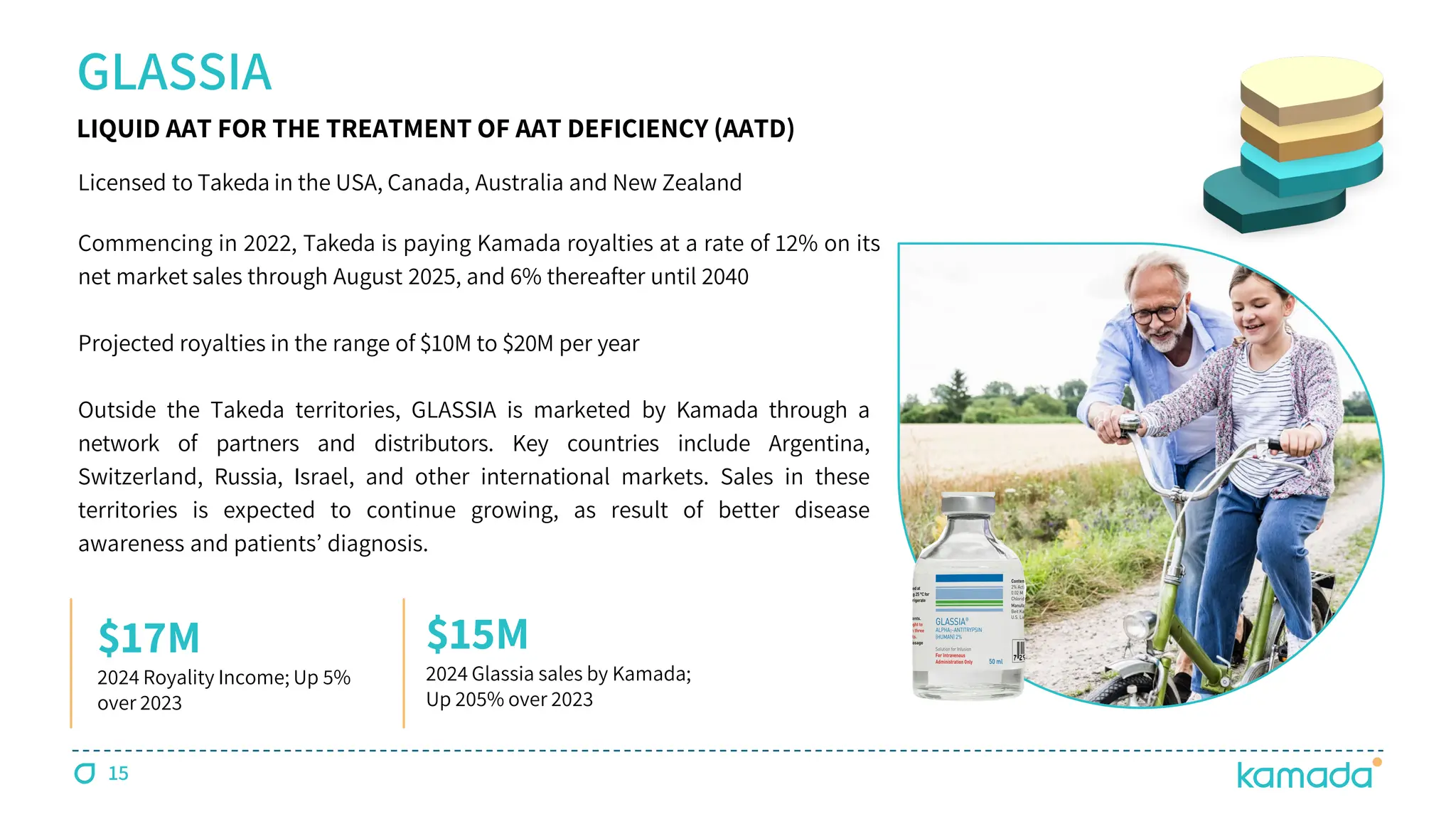

15

Licensed to Takedain the USA, Canada, Australia and New Zealand

Commencing in 2022, Takeda is paying Kamada royalties at a rate of 12% on its

net market sales through August 2025, and 6% thereafter until 2040

Projected royalties in the range of $10M to $20M per year

Outside the Takeda territories, GLASSIA is marketed by Kamada through a

network of partners and distributors. Key countries include Argentina,

Switzerland, Russia, Israel, and other international markets. Sales in these

territories is expected to continue growing, as result of better disease

awareness and patients’ diagnosis.

GLASSIA

$17M

2024 Royality Income; Up 5%

over 2023

LIQUID AAT FOR THE TREATMENT OF AAT DEFICIENCY (AATD)

$15M

2024 Glassia sales by Kamada;

Up 205% over 2023

16.

16

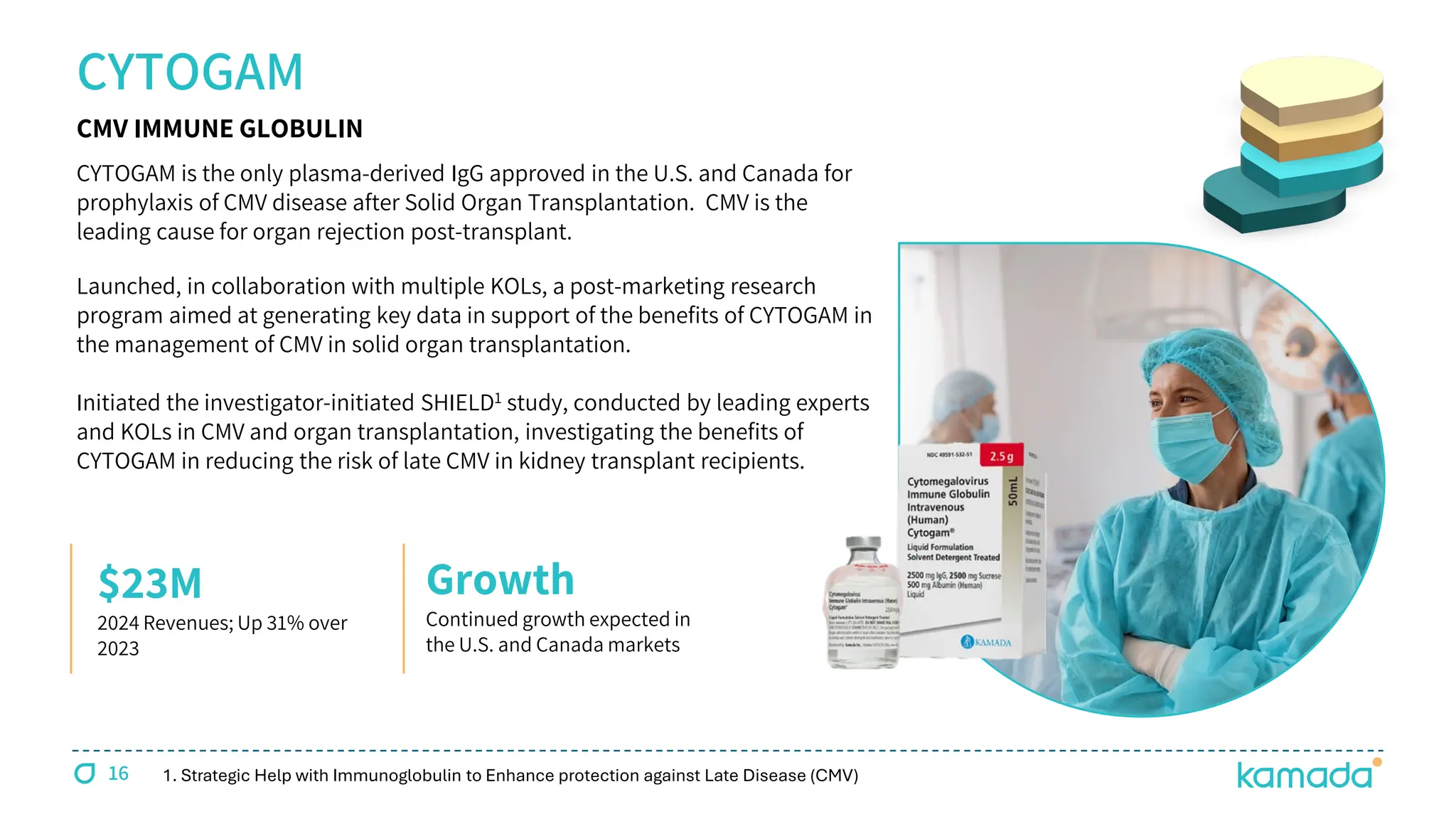

CYTOGAM is theonly plasma-derived IgG approved in the U.S. and Canada for

prophylaxis of CMV disease after Solid Organ Transplantation. CMV is the

leading cause for organ rejection post-transplant.

CYTOGAM

$23M

2024 Revenues; Up 31% over

2023

CMV IMMUNE GLOBULIN

Growth

Continued growth expected in

the U.S. and Canada markets

Launched, in collaboration with multiple KOLs, a post-marketing research

program aimed at generating key data in support of the benefits of CYTOGAM in

the management of CMV in solid organ transplantation.

Initiated the investigator-initiated SHIELD1 study, conducted by leading experts

and KOLs in CMV and organ transplantation, investigating the benefits of

CYTOGAM in reducing the risk of late CMV in kidney transplant recipients.

1. Strategic Help with Immunoglobulin to Enhance protection against Late Disease (CMV)

17.

17

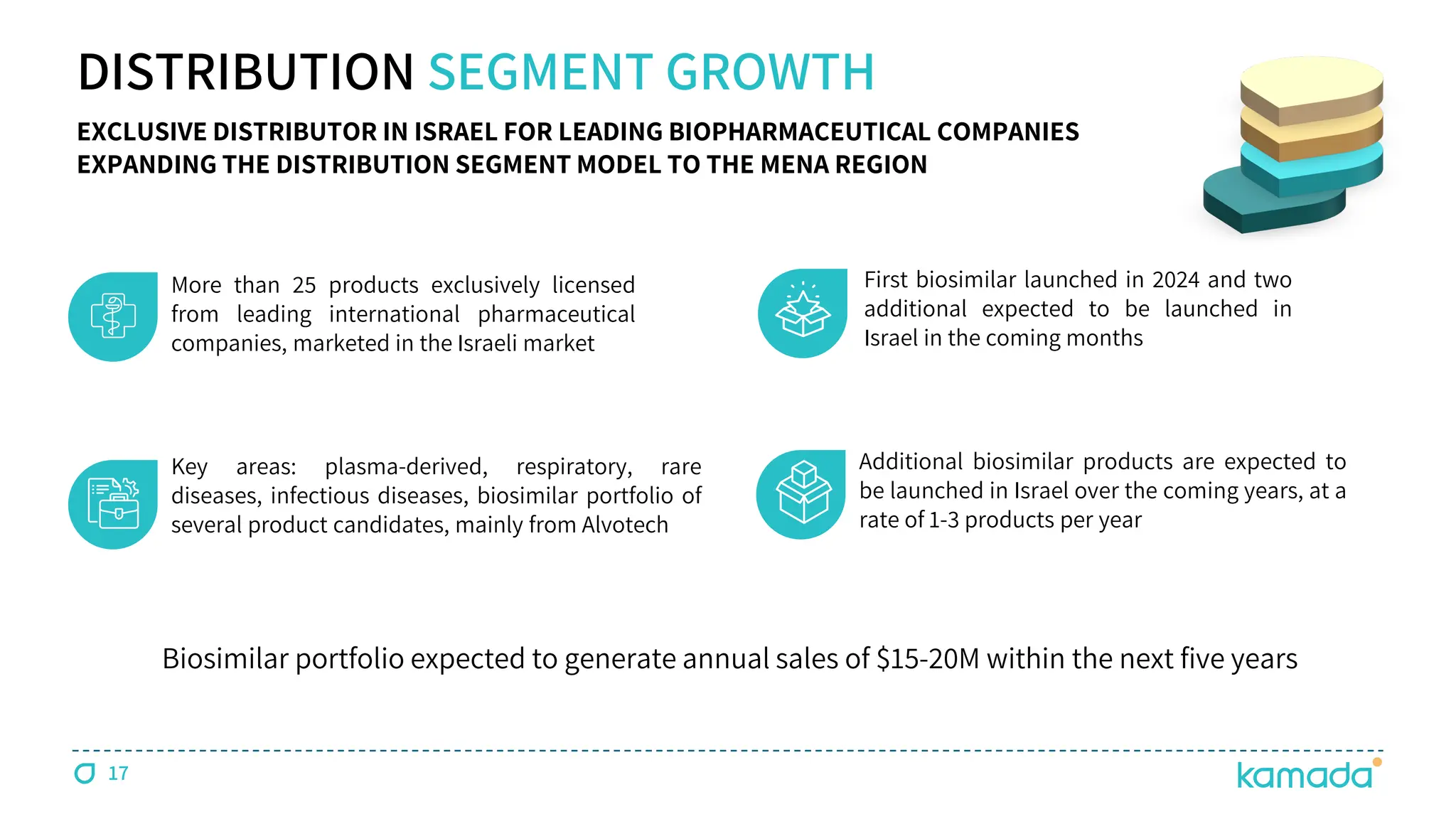

DISTRIBUTION SEGMENT GROWTH

Morethan 25 products exclusively licensed

from leading international pharmaceutical

companies, marketed in the Israeli market

EXCLUSIVE DISTRIBUTOR IN ISRAEL FOR LEADING BIOPHARMACEUTICAL COMPANIES

EXPANDING THE DISTRIBUTION SEGMENT MODEL TO THE MENA REGION

Key areas: plasma-derived, respiratory, rare

diseases, infectious diseases, biosimilar portfolio of

several product candidates, mainly from Alvotech

First biosimilar launched in 2024 and two

additional expected to be launched in

Israel in the coming months

Additional biosimilar products are expected to

be launched in Israel over the coming years, at a

rate of 1-3 products per year

Biosimilar portfolio expected to generate annual sales of $15-20M within the next five years

18.

18

M&A TRANSACTIONS

EXPECT TOSECURE NEW BIZ DEV AND M&A TRANSACTIONS IN THE COMING MONTHS;

LEVERAGING OVERALL FINANCIAL STRENGTH AND COMMERCIAL INFRASTRUCTURE

Screening strategic business development

opportunities to identify potential acquisition

or in-licensing to accelerate long-term growth

Focusing on products synergistic to our

existing commercial and/or production

activities as well as marketing infrastructure

Strong financial position, commercial

infrastructure and proven successful M&A

capabilities

19.

19

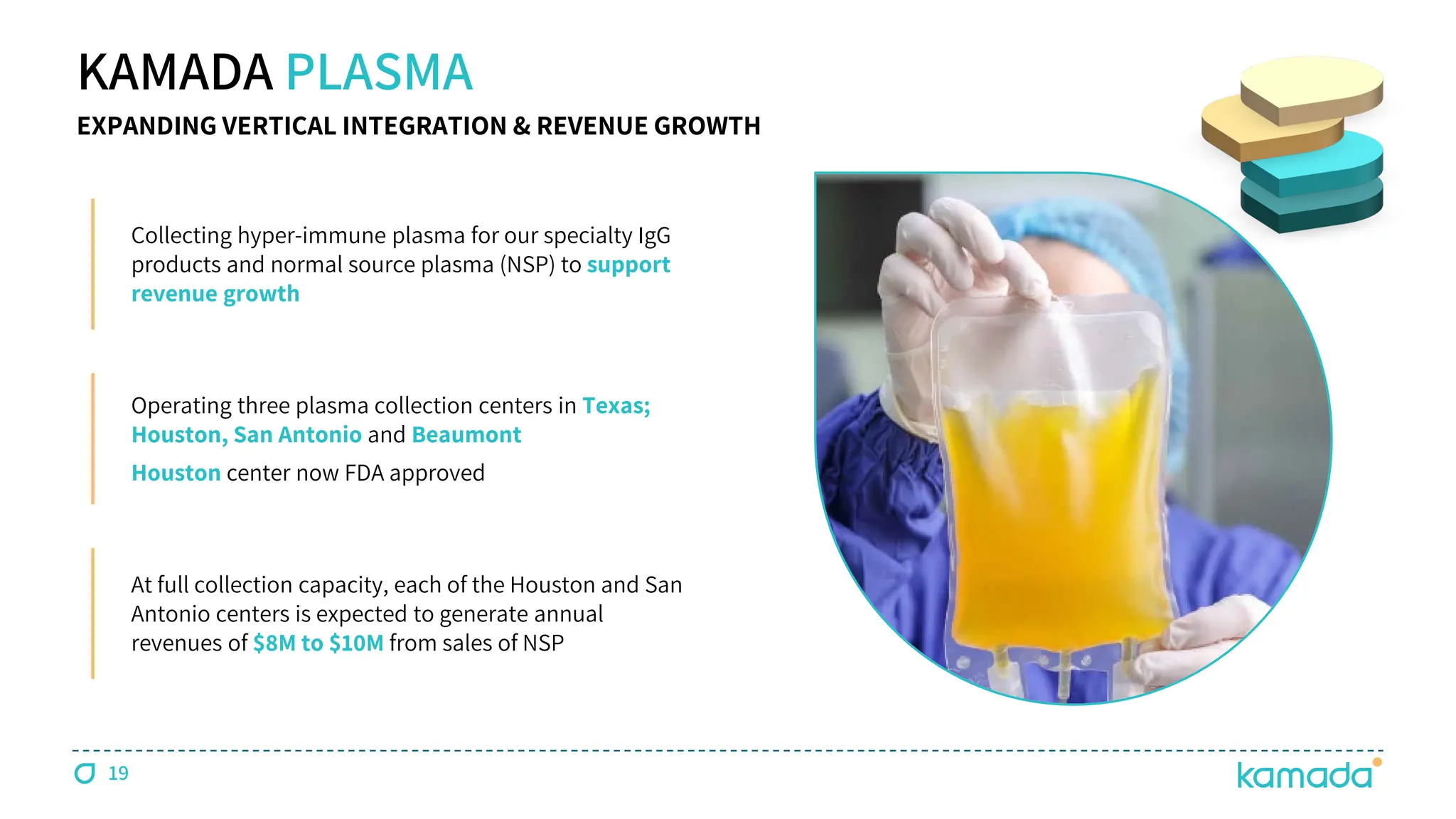

KAMADA PLASMA

EXPANDING VERTICALINTEGRATION & REVENUE GROWTH

Collecting hyper-immune plasma for our specialty IgG

products and normal source plasma (NSP) to support

revenue growth

Operating three plasma collection centers in Texas;

Houston, San Antonio and Beaumont

Houston center now FDA approved

At full collection capacity, each of the Houston and San

Antonio centers is expected to generate annual

revenues of $8M to $10M from sales of NSP

20.

20

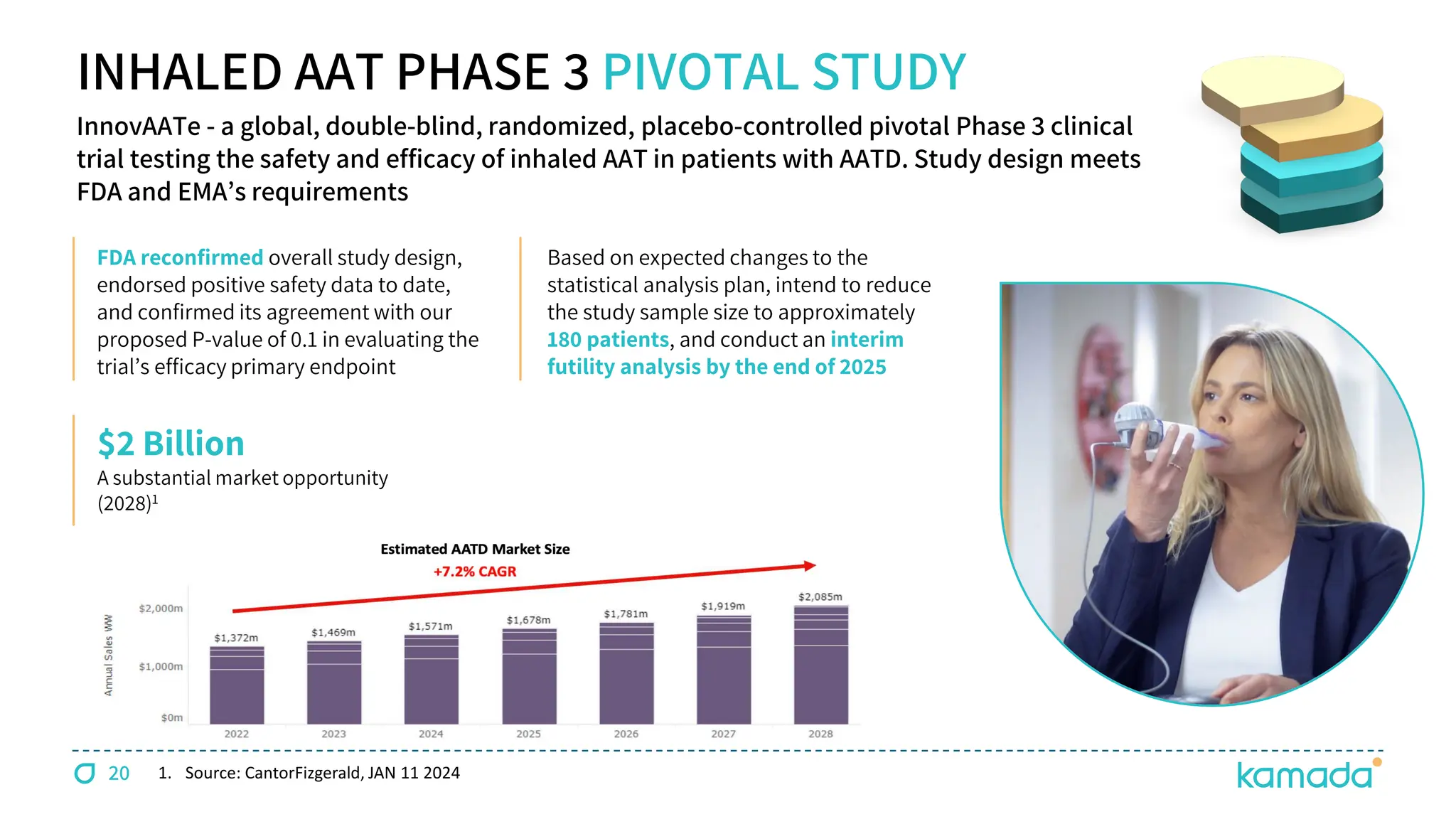

$2 Billion

A substantialmarket opportunity

(2028)1

Based on expected changes to the

statistical analysis plan, intend to reduce

the study sample size to approximately

180 patients, and conduct an interim

futility analysis by the end of 2025

FDA reconfirmed overall study design,

endorsed positive safety data to date,

and confirmed its agreement with our

proposed P-value of 0.1 in evaluating the

trial’s efficacy primary endpoint

INHALED AAT PHASE 3 PIVOTAL STUDY

InnovAATe - a global, double-blind, randomized, placebo-controlled pivotal Phase 3 clinical

trial testing the safety and efficacy of inhaled AAT in patients with AATD. Study design meets

FDA and EMA’s requirements

1. Source: CantorFizgerald, JAN 11 2024

21.

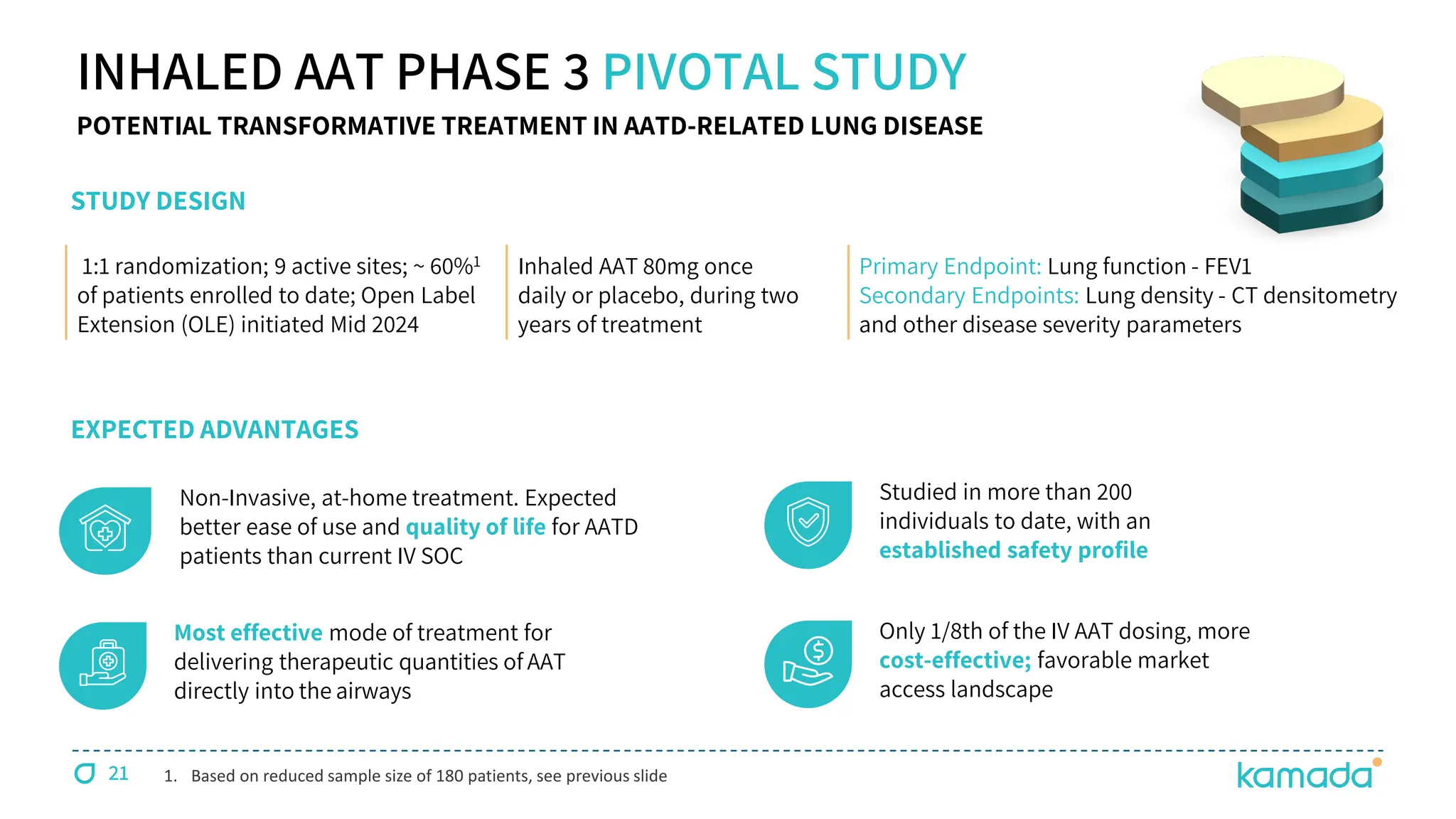

INHALED AAT PHASE3 PIVOTAL STUDY

Non-Invasive, at-home treatment. Expected

better ease of use and quality of life for AATD

patients than current IV SOC

Most effective mode of treatment for

delivering therapeutic quantities of AAT

directly into the airways

Studied in more than 200

individuals to date, with an

established safety profile

Only 1/8th of the IV AAT dosing, more

cost-effective; favorable market

access landscape

STUDY DESIGN

EXPECTED ADVANTAGES

1:1 randomization; 9 active sites; ~ 60%1

of patients enrolled to date; Open Label

Extension (OLE) initiated Mid 2024

Inhaled AAT 80mg once

daily or placebo, during two

years of treatment

Primary Endpoint: Lung function - FEV1

Secondary Endpoints: Lung density - CT densitometry

and other disease severity parameters

21

POTENTIAL TRANSFORMATIVE TREATMENT IN AATD-RELATED LUNG DISEASE

1. Based on reduced sample size of 180 patients, see previous slide

22.

KEDRAB® CYTOGAM® HEPGAMB® VARIZIG® WINRHO® GLASSIA®

KAMADA - A GLOBAL BIOPHARMACEUTICAL COMPANY

6

FDA-

Approved

Products

15%

CAGR

(from 2021)

$178-182M

2025 Revenues

Guidance

$40-44M

2025 Adj. EBIDTA

Guidance

4

Pillars of

Growth

A LEADER IN SPECIALTY PLASMA THERAPIES, WITH A PORTFOLIO OF MARKETED PRODUCTS INDICATED FOR RARE

AND SERIOUS CONDITIONS

$72.0M

Cash @ Sep 30,

2025

22

Organic Growth

M&A Transactions

Inhaled AAT Pivotal Study

Plasma Collection Centers

![4

6 FDA-APPROVED SPECIALTY PLASMA PRODUCTS

KEDRAB®

[Rabies Immune

Globulin (Human)]

Post exposure prophylaxis

of rabies infection

CYTOGAM®

[Cytomegalovirus

Immune Globulin (Human)]

Prophylaxis of CMV

disease associated

with transplants

HEPGAM B®

[Hepatitis B Immune

Globulin (Human)]

Prevention of HBV

recurrence following

liver transplants

VARIZIG®

[Varicella Zoster Immune

Globulin (Human)]

Post-exposure prophylaxis

of varicella

in high- risk patients

WINRHO®

[Rho(D) Immune

Globulin (Human)]

Treatment of ITP &

suppression of Rh

isoimmunization (HDN)

KEY FOCUS ON TRANSPLANTS & RARE CONDITIONS

For Important Safety Information, visit www.Kamada.com

GLASSIA®

[Alpha1-Proteinase

Inhibitor (Human)]

Augmentation therapy

for Alpha-1 Antitrypsin

Deficiency (AATD)](https://image.slidesharecdn.com/kamada-corporatepresentation-eachlifeisunique-november2025-final-251125130830-35dc6b9f/75/Kamada-Corporate-Presentation-Each-Life-is-Unique-November-2025-4-2048.jpg)