A G EN D A

• Digital identification

• Customer digital onboarding

• Digital signatures

• Challenges

• Arab Country survey insights

3.

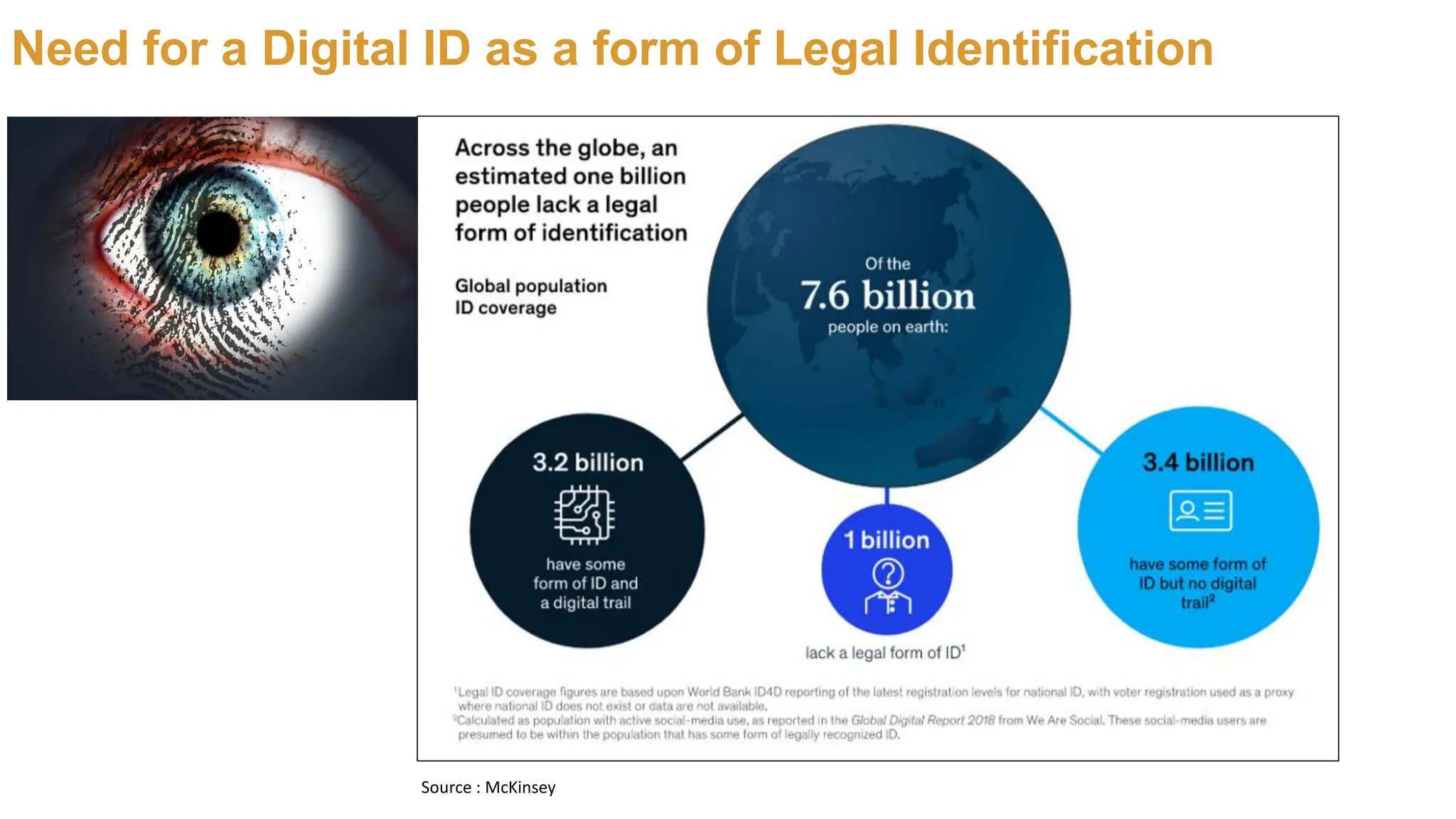

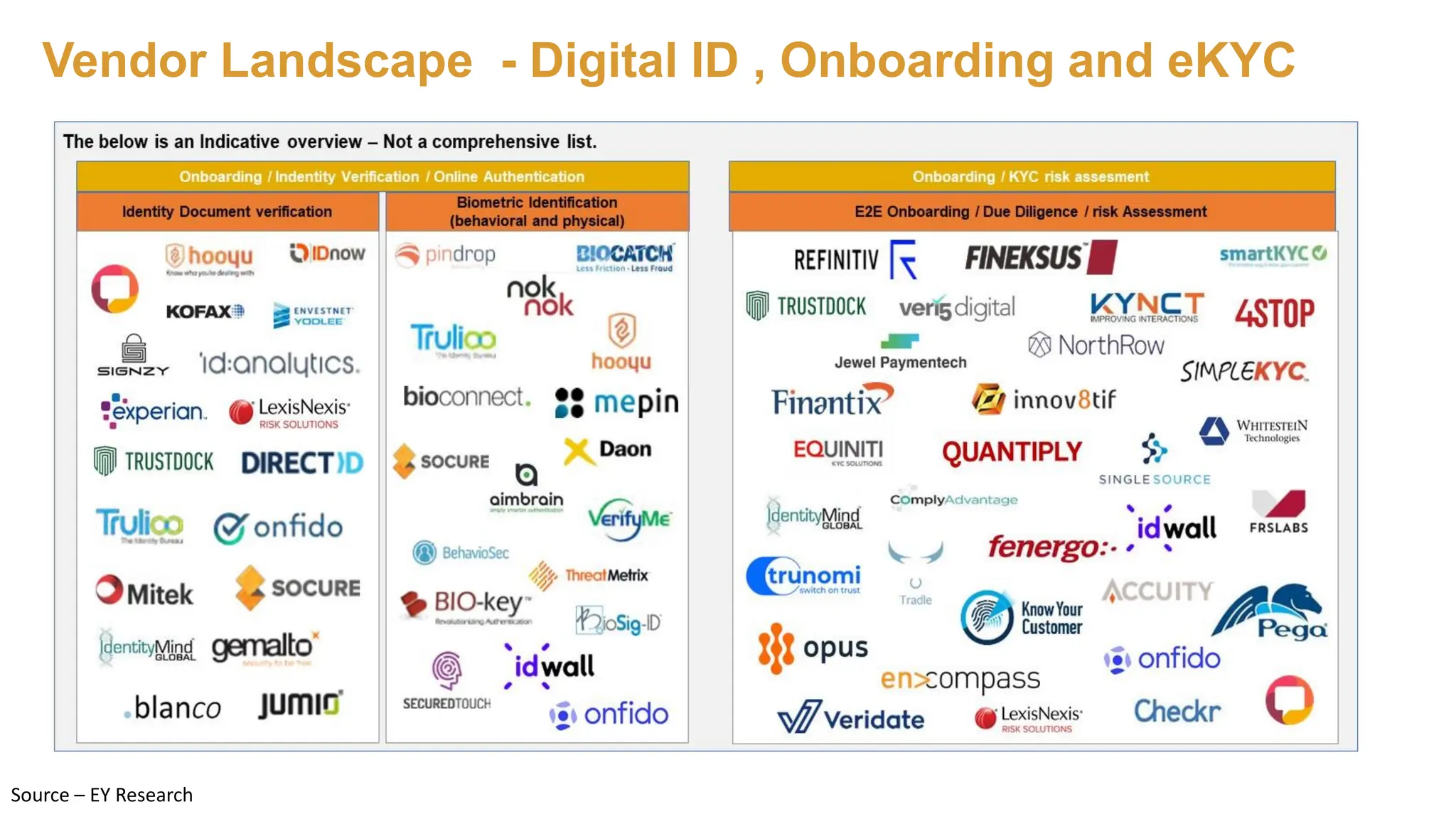

Need for aDigital ID as a form of Legal Identification

Source : McKinsey

4.

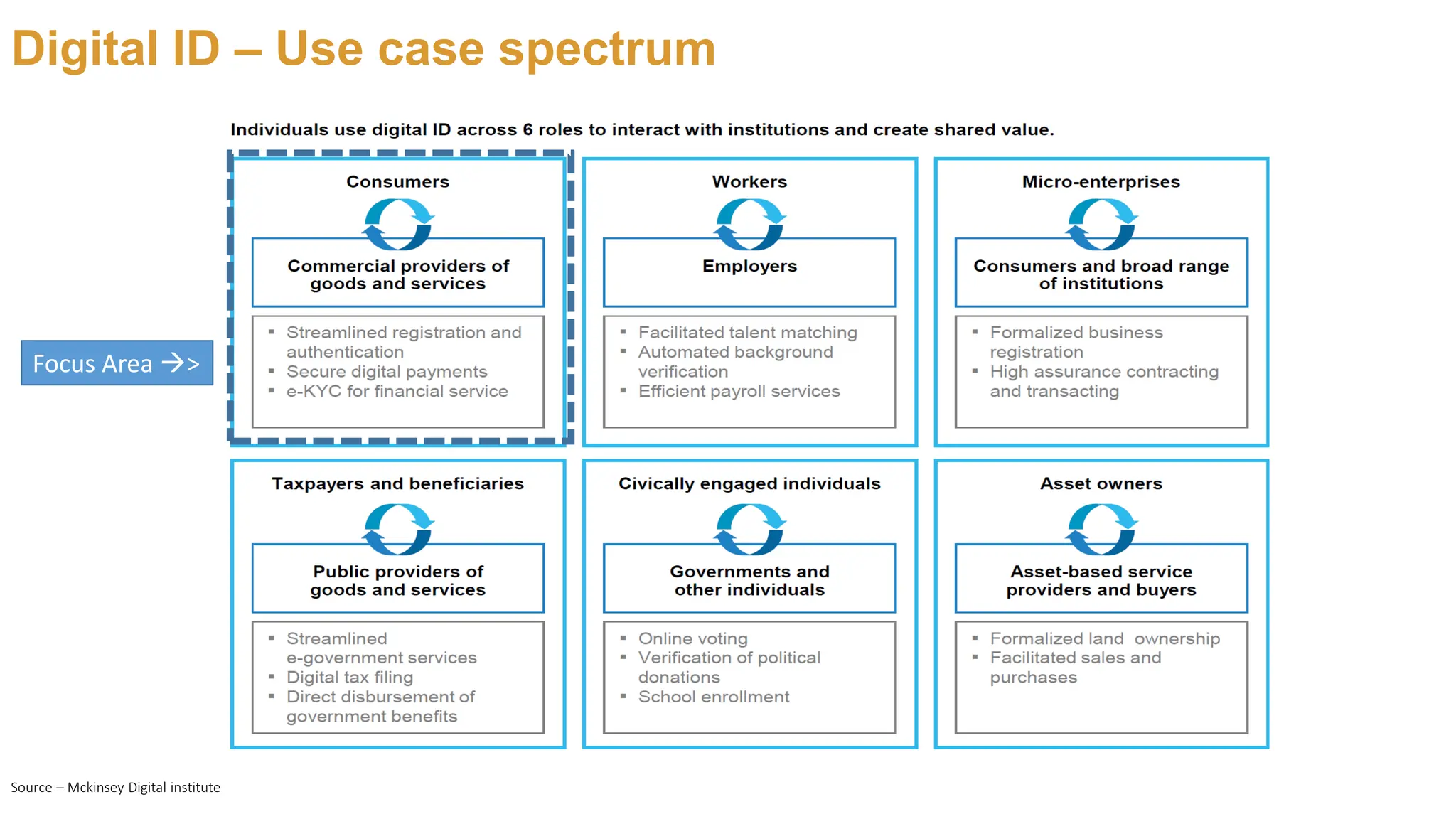

Digital ID –Use case spectrum

Source – Mckinsey Digital institute

Focus Area →>

5.

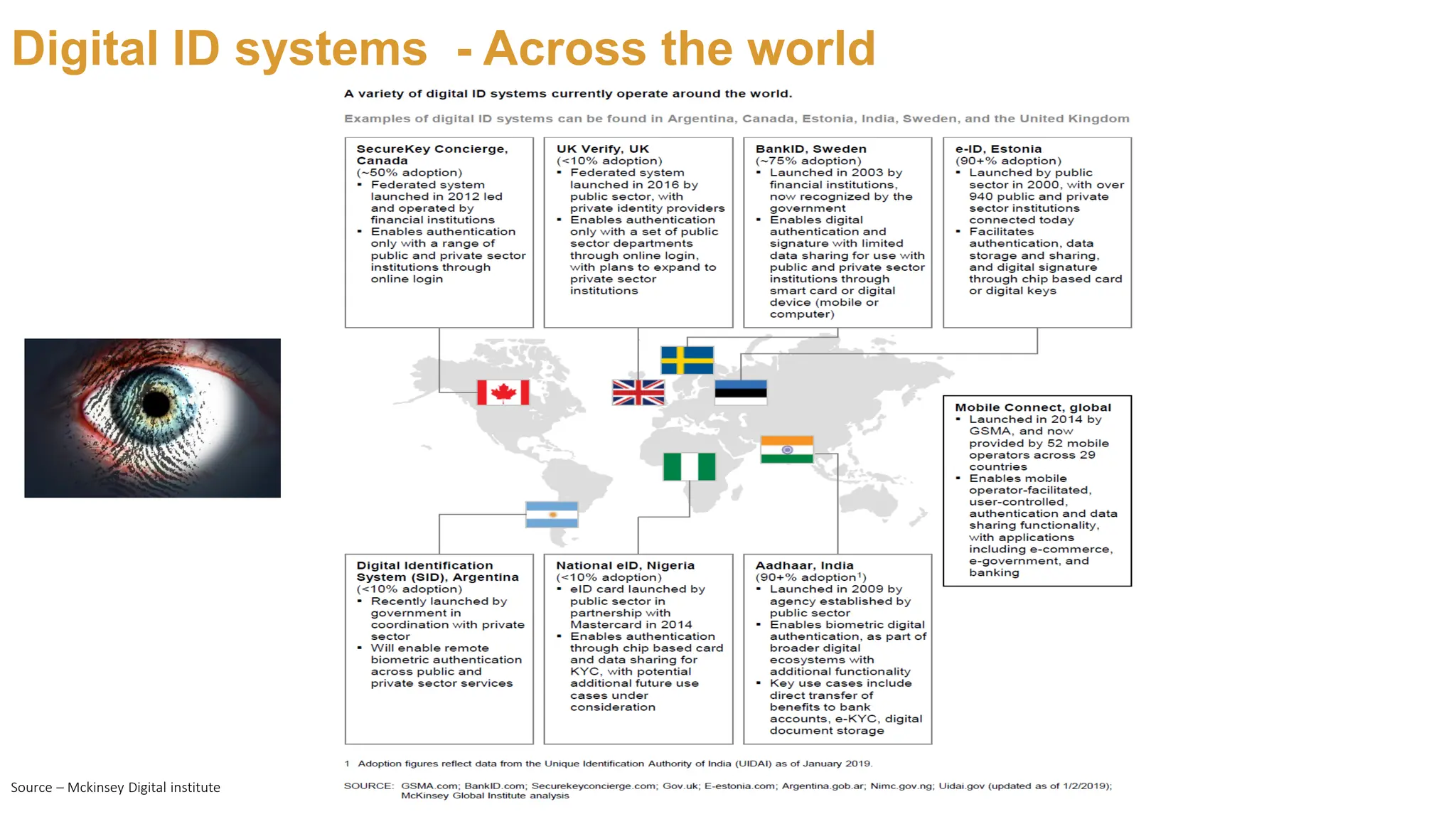

Digital ID systems- Across the world

Source – Mckinsey Digital institute

6.

Digital ID –Recipe for a good Digital ID

Source – Mckinsey Digital institute

• Verification over digital channels

• Verified to a high degree of assurance

• Unique- And linked with a biometric element

• Established with individual consent

7.

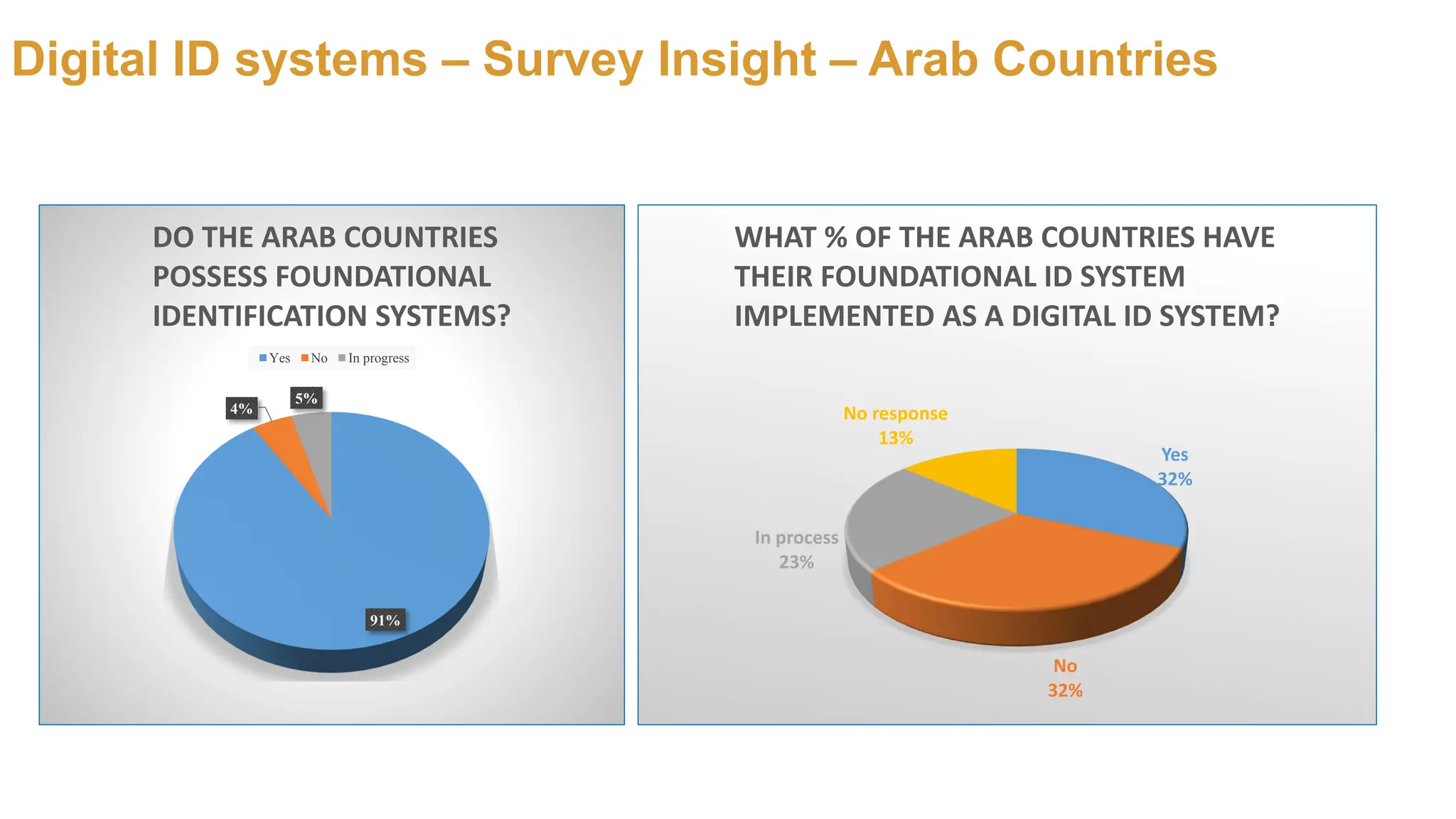

Digital ID systems– Survey Insight – Arab Countries

91%

4%

5%

DO THE ARAB COUNTRIES

POSSESS FOUNDATIONAL

IDENTIFICATION SYSTEMS?

Yes No In progress

Yes

32%

No

32%

In process

23%

No response

13%

WHAT % OF THE ARAB COUNTRIES HAVE

THEIR FOUNDATIONAL ID SYSTEM

IMPLEMENTED AS A DIGITAL ID SYSTEM?

8.

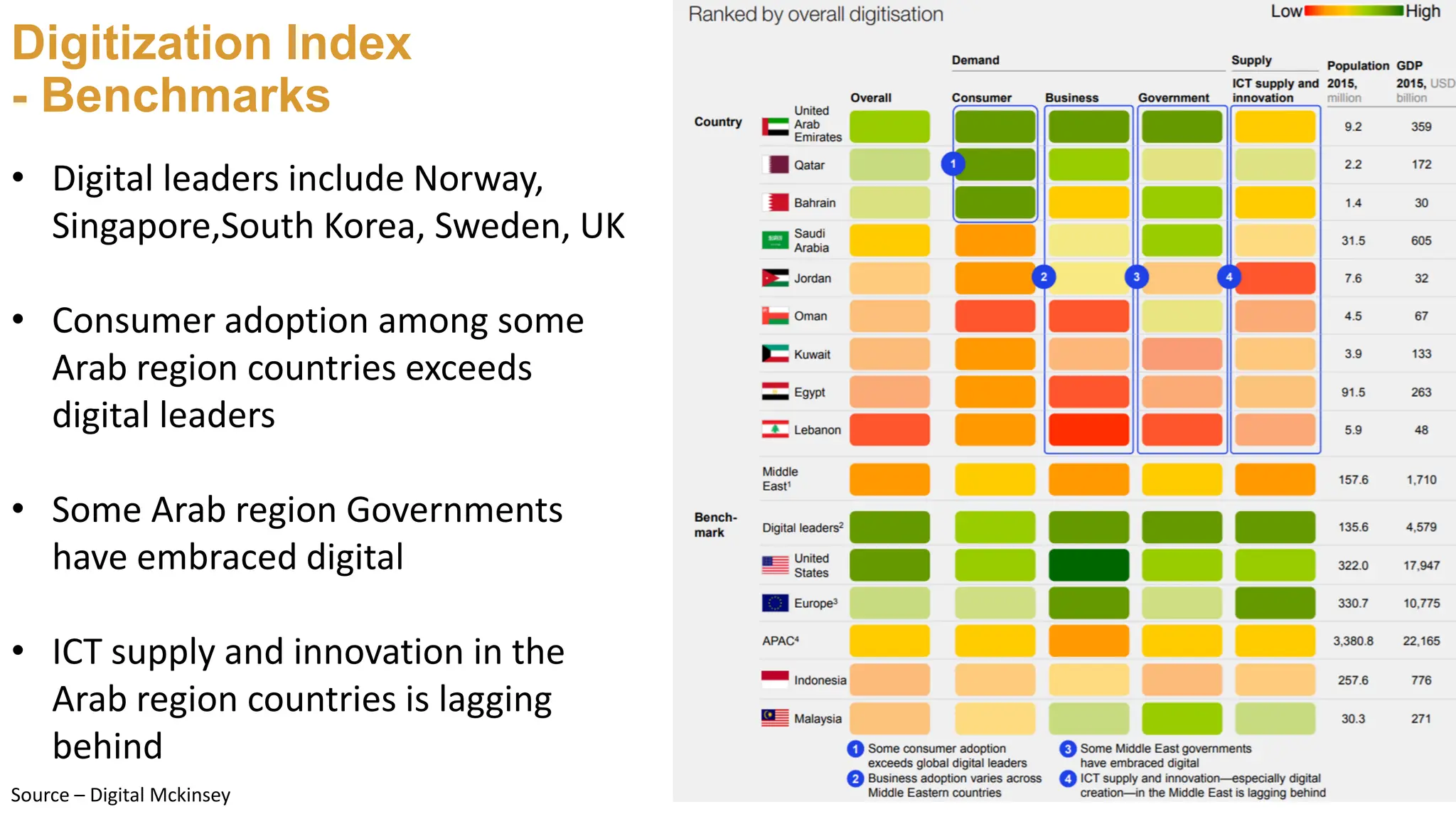

Digitization Index

- Benchmarks

•Digital leaders include Norway,

Singapore,South Korea, Sweden, UK

• Consumer adoption among some

Arab region countries exceeds

digital leaders

• Some Arab region Governments

have embraced digital

• ICT supply and innovation in the

Arab region countries is lagging

behind

Source – Digital Mckinsey

9.

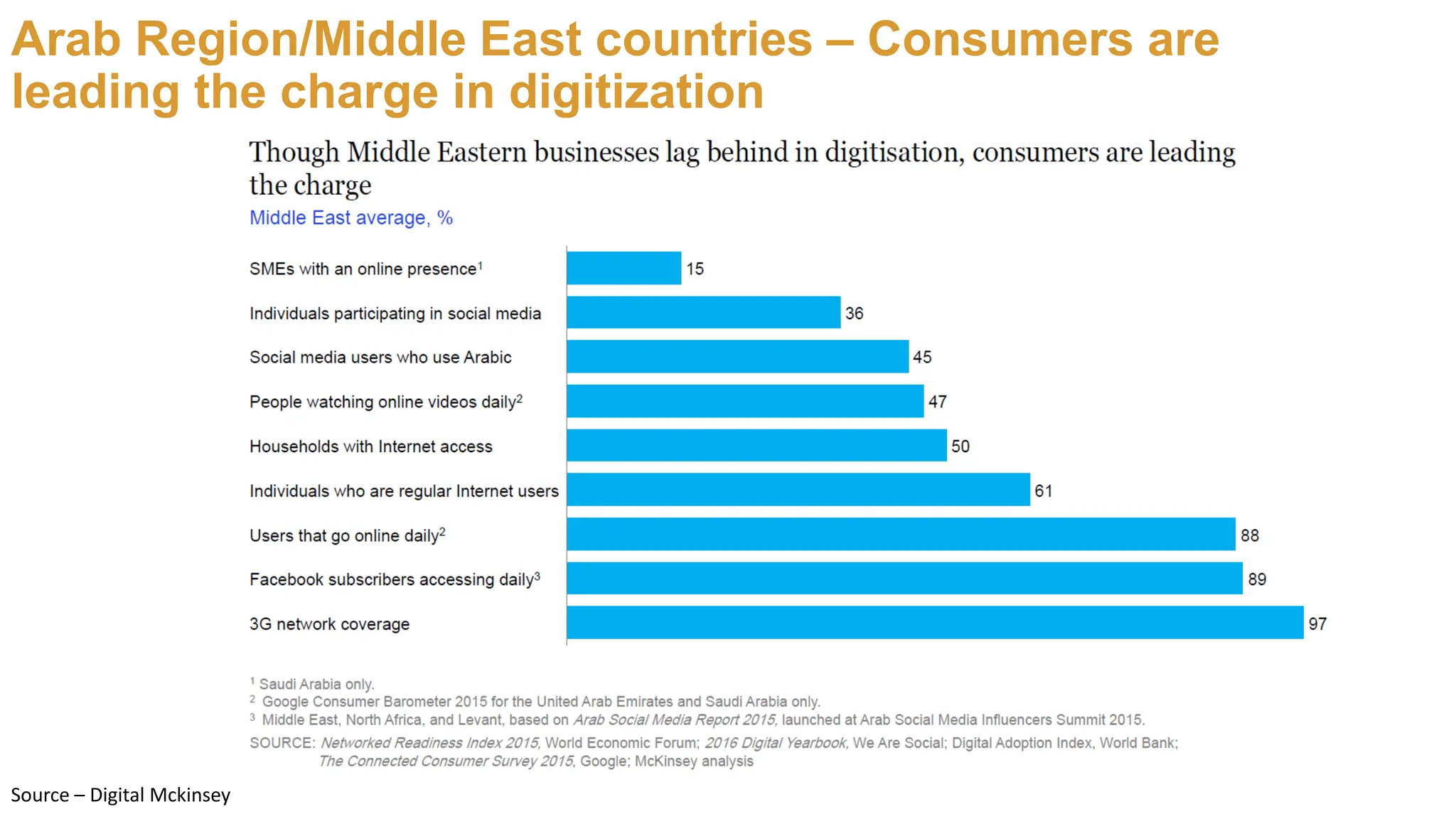

Arab Region/Middle Eastcountries – Consumers are

leading the charge in digitization

Source – Digital Mckinsey

10.

Customer Digital On-boarding

•Majority of financial institutions undertake

cumbersome and strenuously manual processes

for customer onboarding onto the banking

system.

• Involves collection of ID documents,

verification against national ID sources, AML

and sanction list checks, credit bureau checks

etc

• Today’s technology allows for onboarding

customers digitally and in minutes

Digital Onboarding enables a new and seamless

customer experience by simplifying the access to

financial services while reducing processing time and

cost for financial institutions due to optimized

processes

11.

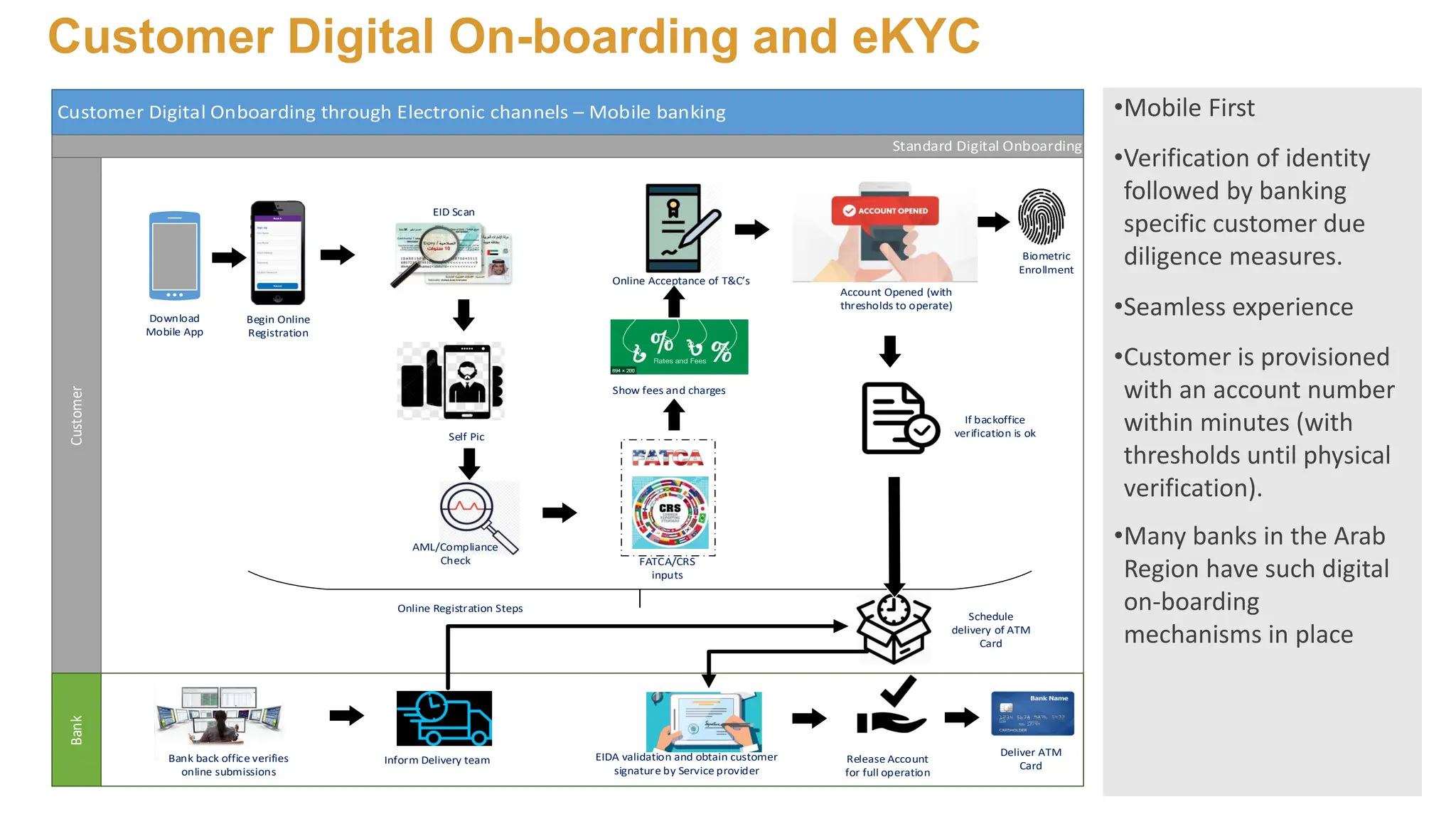

Customer Digital On-boardingand eKYC

Customer Digital Onboarding through Electronic channels – Mobile banking

Customer

Bank

Standard Digital Onboarding

Download

Mobile App

Begin Online

Registration

Online Registration Steps

EID Scan

Self Pic

AML/Compliance

Check FATCA/CRS

inputs

Show fees and charges

Online Acceptance of T&C’s

Biometric

Enrollment

Account Opened (with

thresholds to operate)

If backoffice

verification is ok

Schedule

delivery of ATM

Card

Bank back office verifies

online submissions

Release Account

for full operation

Inform Delivery team EIDA validation and obtain customer

signature by Service provider

Deliver ATM

Card

•Mobile First

•Verification of identity

followed by banking

specific customer due

diligence measures.

•Seamless experience

•Customer is provisioned

with an account number

within minutes (with

thresholds until physical

verification).

•Many banks in the Arab

Region have such digital

on-boarding

mechanisms in place

12.

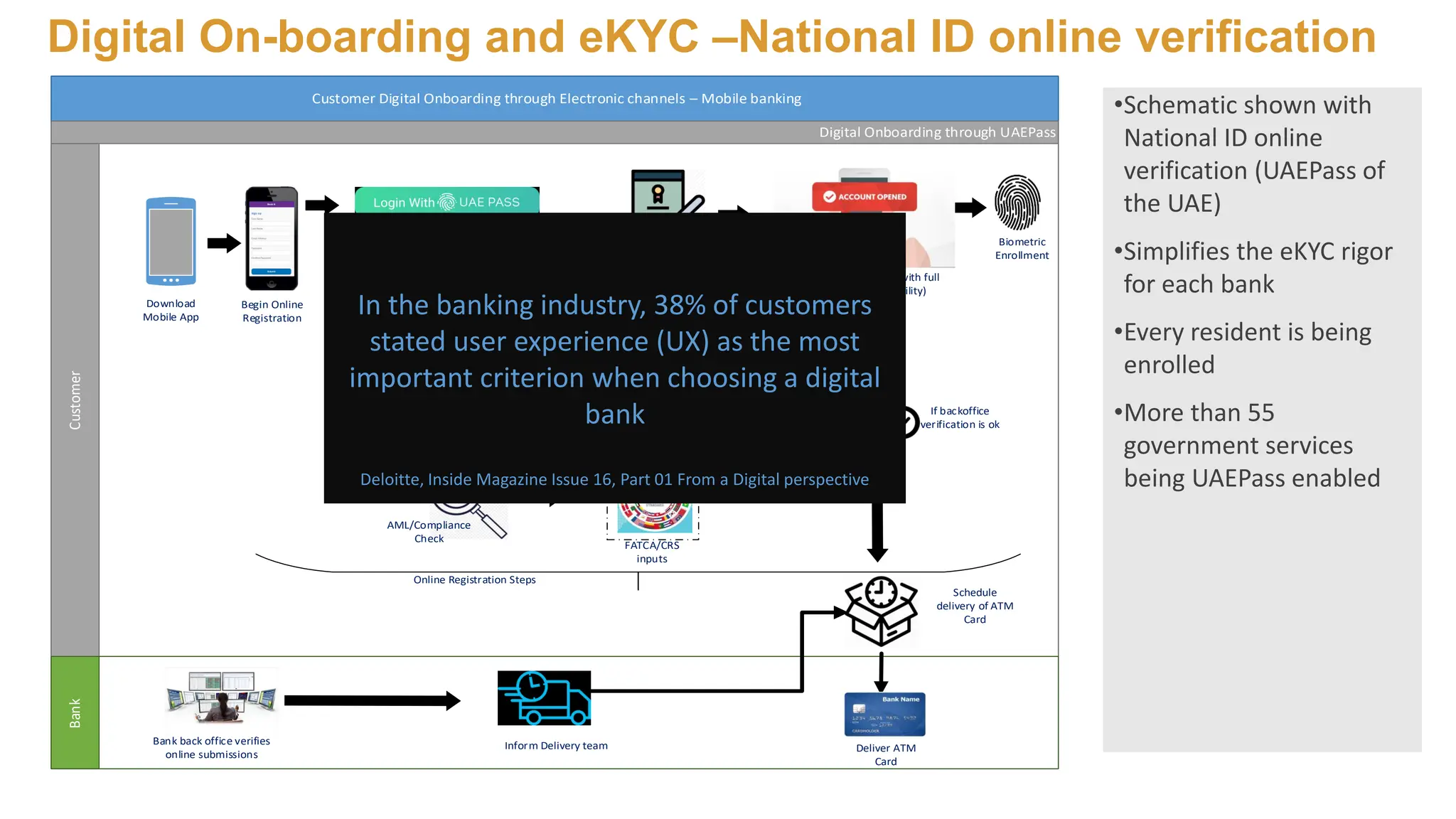

Digital On-boarding andeKYC –National ID online verification

•Schematic shown with

National ID online

verification (UAEPass of

the UAE)

•Simplifies the eKYC rigor

for each bank

•Every resident is being

enrolled

•More than 55

government services

being UAEPass enabled

Customer Digital Onboarding through Electronic channels – Mobile banking

Customer

Bank

Digital Onboarding through UAEPass

Download

Mobile App

Begin Online

Registration

Online Registration Steps

AML/Compliance

Check

FATCA/CRS

inputs

Show fees and charges

Online Acceptance of T&C’s

Biometric

Enrollment

Account Opened (with full

operation capability)

If backoffice

verification is ok

Schedule

delivery of ATM

Card

Bank back office verifies

online submissions

Inform Delivery team Deliver ATM

Card

UAEPass

Validation for

“Verified” ID

In the banking industry, 38% of customers

stated user experience (UX) as the most

important criterion when choosing a digital

bank

Deloitte, Inside Magazine Issue 16, Part 01 From a Digital perspective

13.

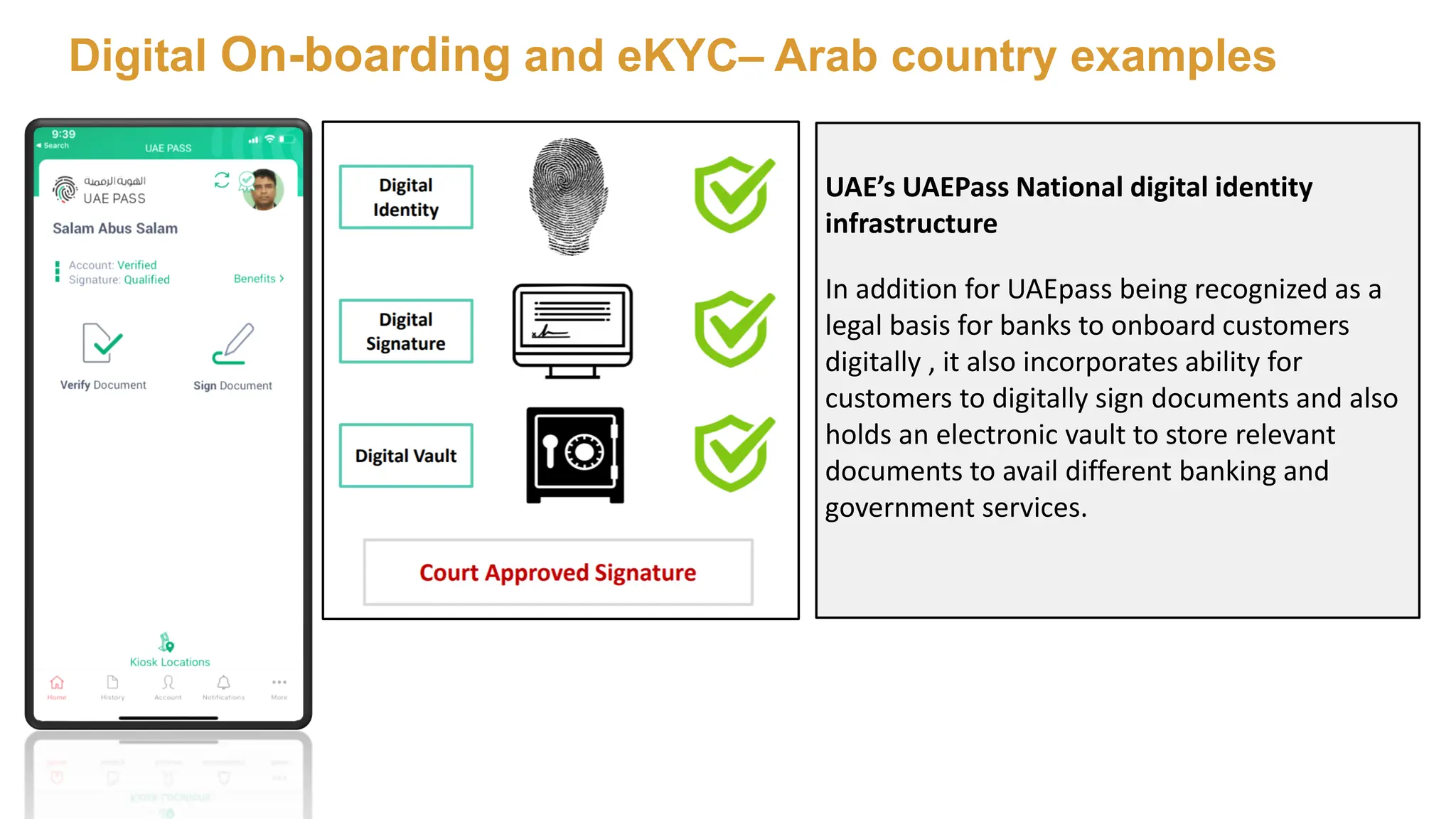

Digital On-boarding andeKYC– Arab country examples

UAE’s UAEPass National digital identity

infrastructure

In addition for UAEpass being recognized as a

legal basis for banks to onboard customers

digitally , it also incorporates ability for

customers to digitally sign documents and also

holds an electronic vault to store relevant

documents to avail different banking and

government services.

14.

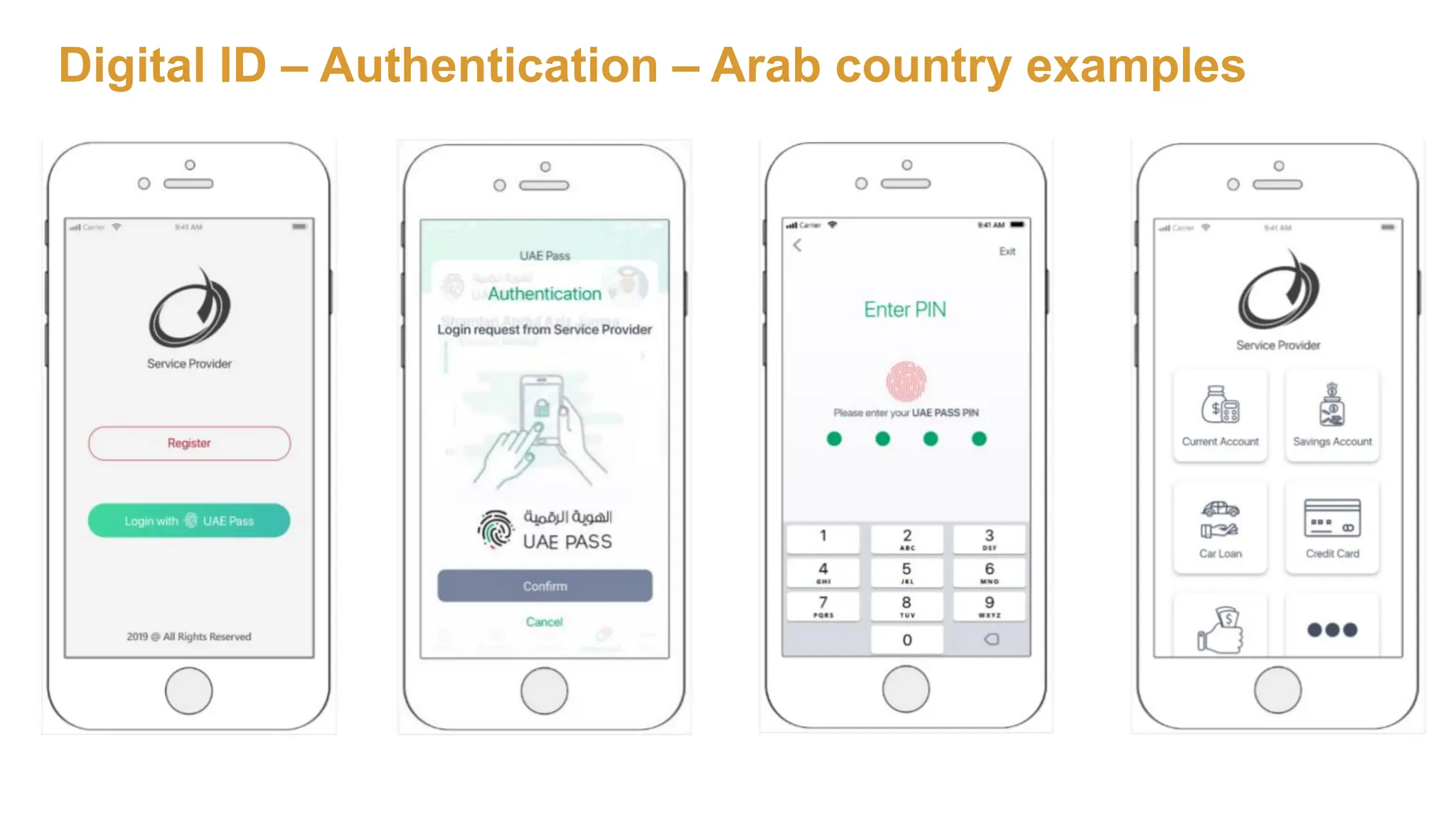

Digital ID –Authentication – Arab country examples

15.

Digital On-boarding andeKYC– Arab country examples

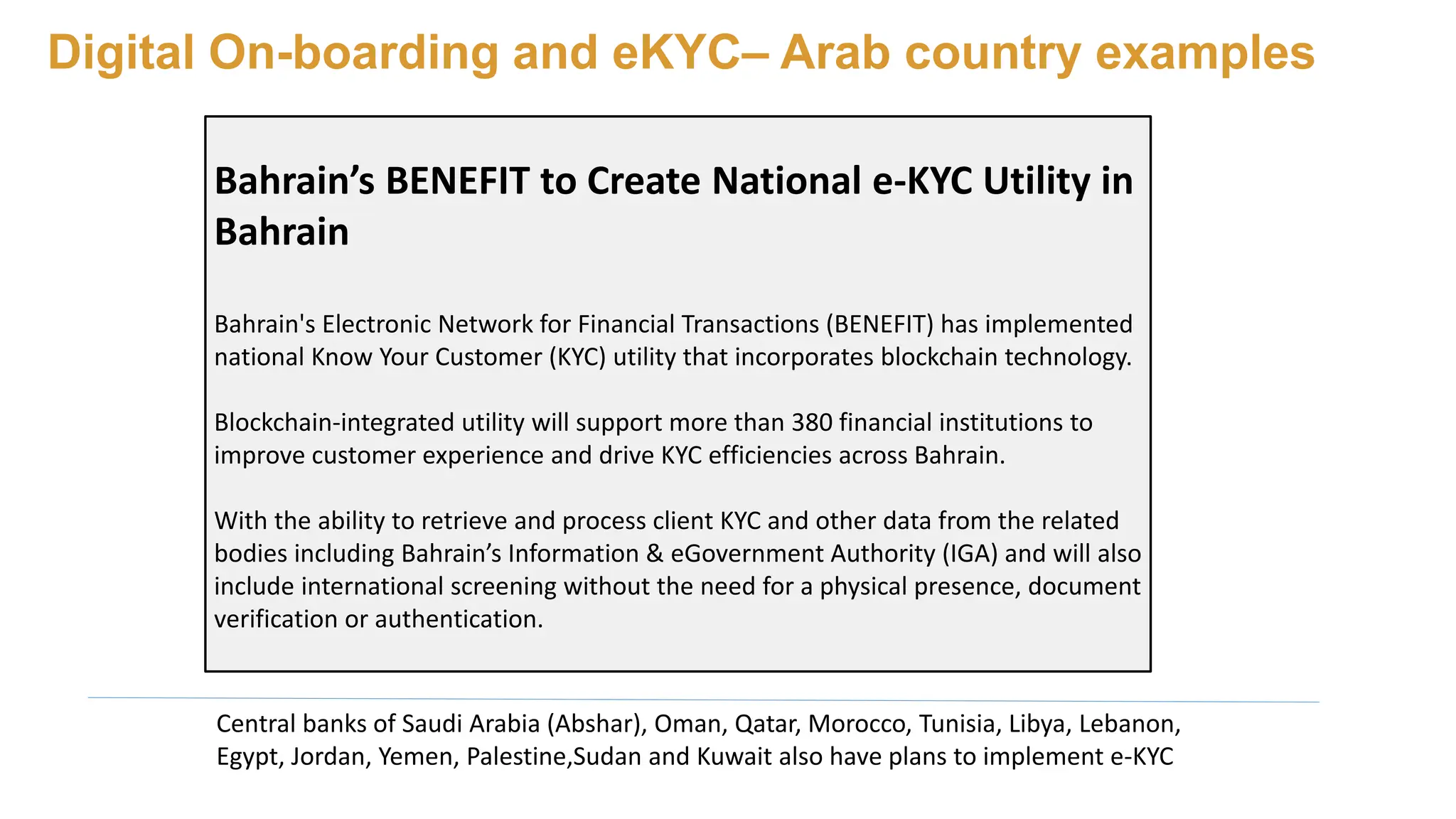

Central banks of Saudi Arabia (Abshar), Oman, Qatar, Morocco, Tunisia, Libya, Lebanon,

Egypt, Jordan, Yemen, Palestine,Sudan and Kuwait also have plans to implement e-KYC

Bahrain’s BENEFIT to Create National e-KYC Utility in

Bahrain

Bahrain's Electronic Network for Financial Transactions (BENEFIT) has implemented

national Know Your Customer (KYC) utility that incorporates blockchain technology.

Blockchain-integrated utility will support more than 380 financial institutions to

improve customer experience and drive KYC efficiencies across Bahrain.

With the ability to retrieve and process client KYC and other data from the related

bodies including Bahrain’s Information & eGovernment Authority (IGA) and will also

include international screening without the need for a physical presence, document

verification or authentication.

16.

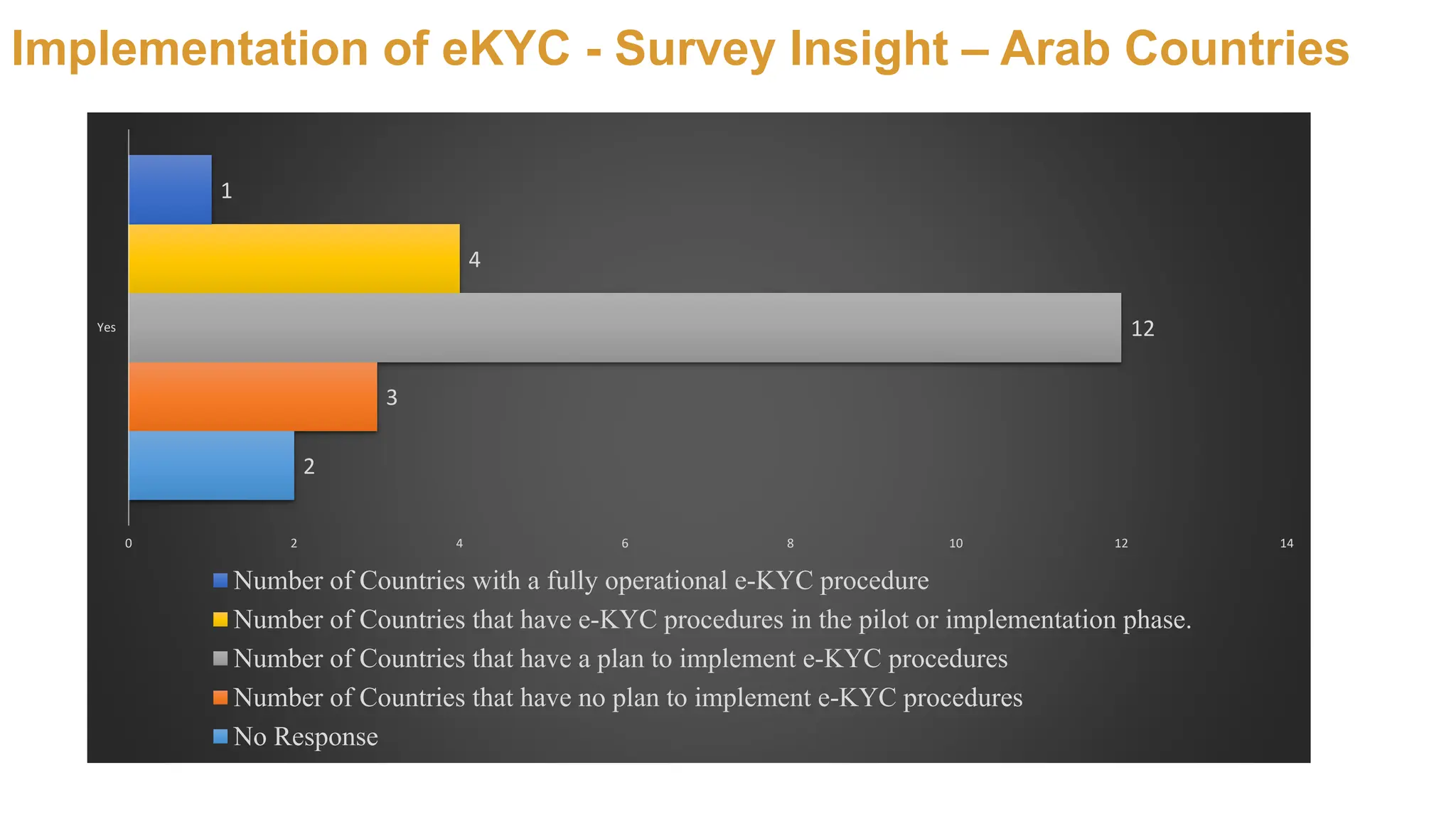

Implementation of eKYC- Survey Insight – Arab Countries

2

3

12

4

1

0 2 4 6 8 10 12 14

Yes

Number of Countries with a fully operational e-KYC procedure

Number of Countries that have e-KYC procedures in the pilot or implementation phase.

Number of Countries that have a plan to implement e-KYC procedures

Number of Countries that have no plan to implement e-KYC procedures

No Response

17.

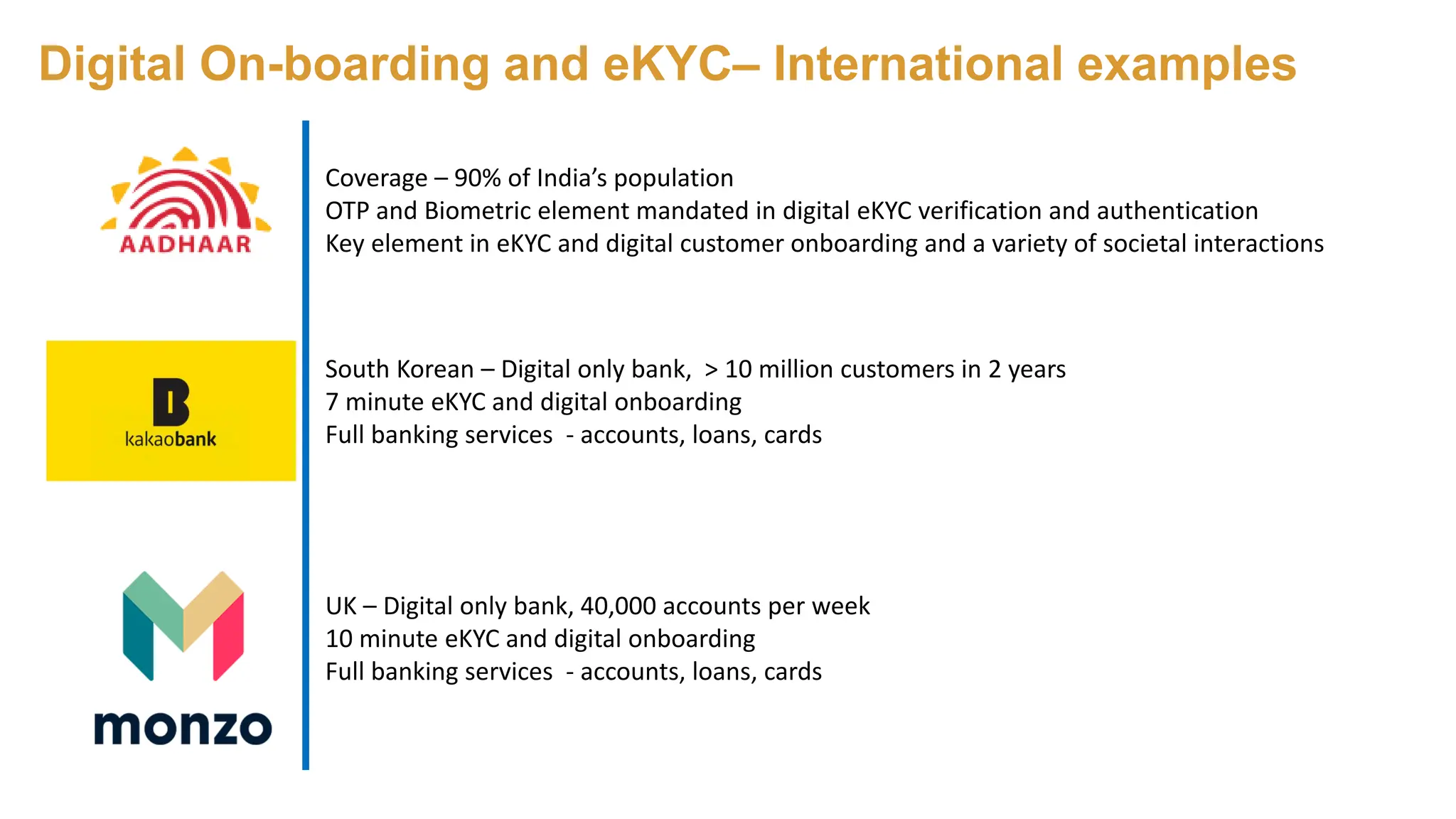

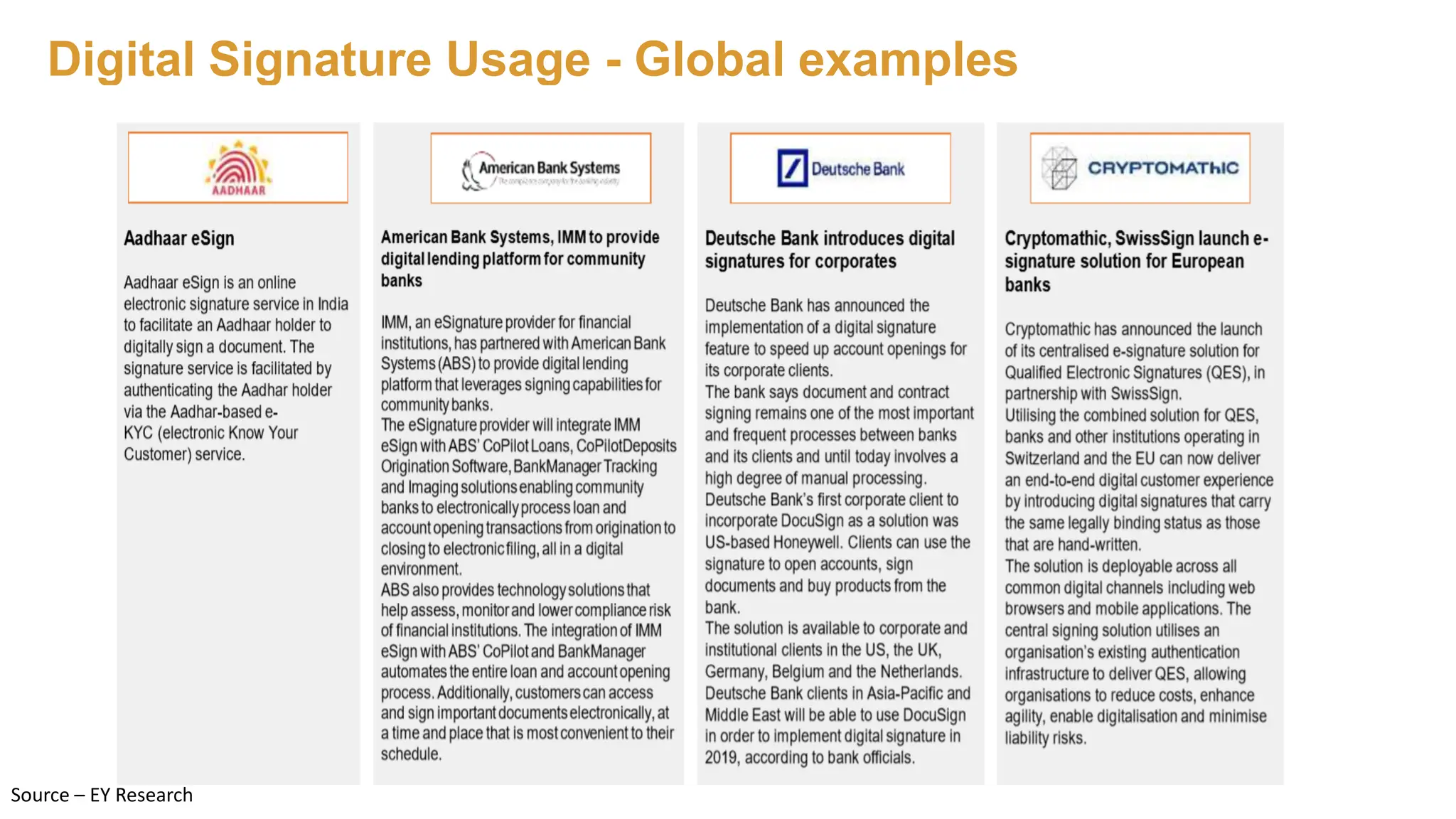

Digital On-boarding andeKYC– International examples

Coverage – 90% of India’s population

OTP and Biometric element mandated in digital eKYC verification and authentication

Key element in eKYC and digital customer onboarding and a variety of societal interactions

South Korean – Digital only bank, > 10 million customers in 2 years

7 minute eKYC and digital onboarding

Full banking services - accounts, loans, cards

UK – Digital only bank, 40,000 accounts per week

10 minute eKYC and digital onboarding

Full banking services - accounts, loans, cards

18.

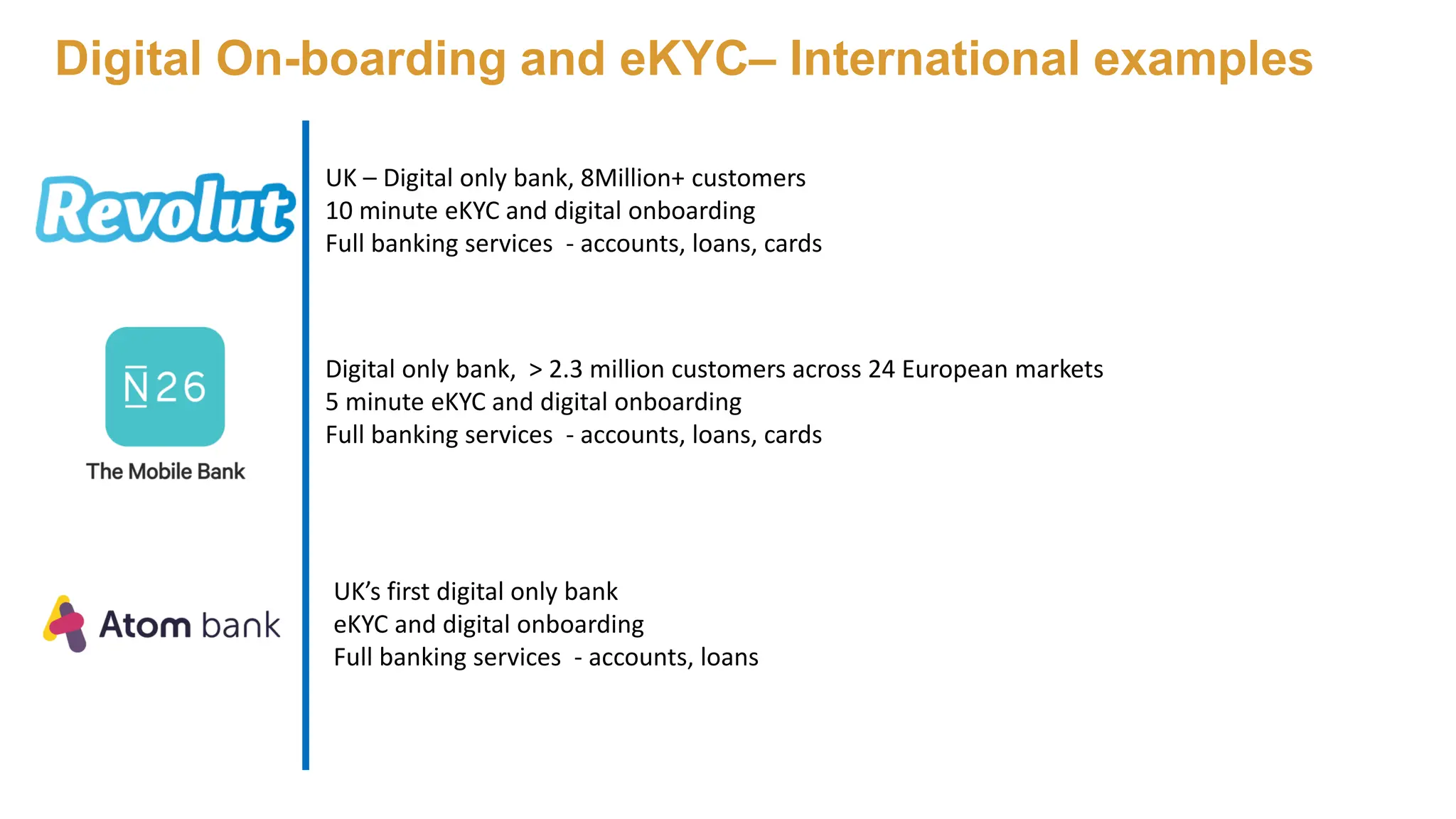

Digital On-boarding andeKYC– International examples

UK – Digital only bank, 8Million+ customers

10 minute eKYC and digital onboarding

Full banking services - accounts, loans, cards

Digital only bank, > 2.3 million customers across 24 European markets

5 minute eKYC and digital onboarding

Full banking services - accounts, loans, cards

UK’s first digital only bank

eKYC and digital onboarding

Full banking services - accounts, loans

Authentication

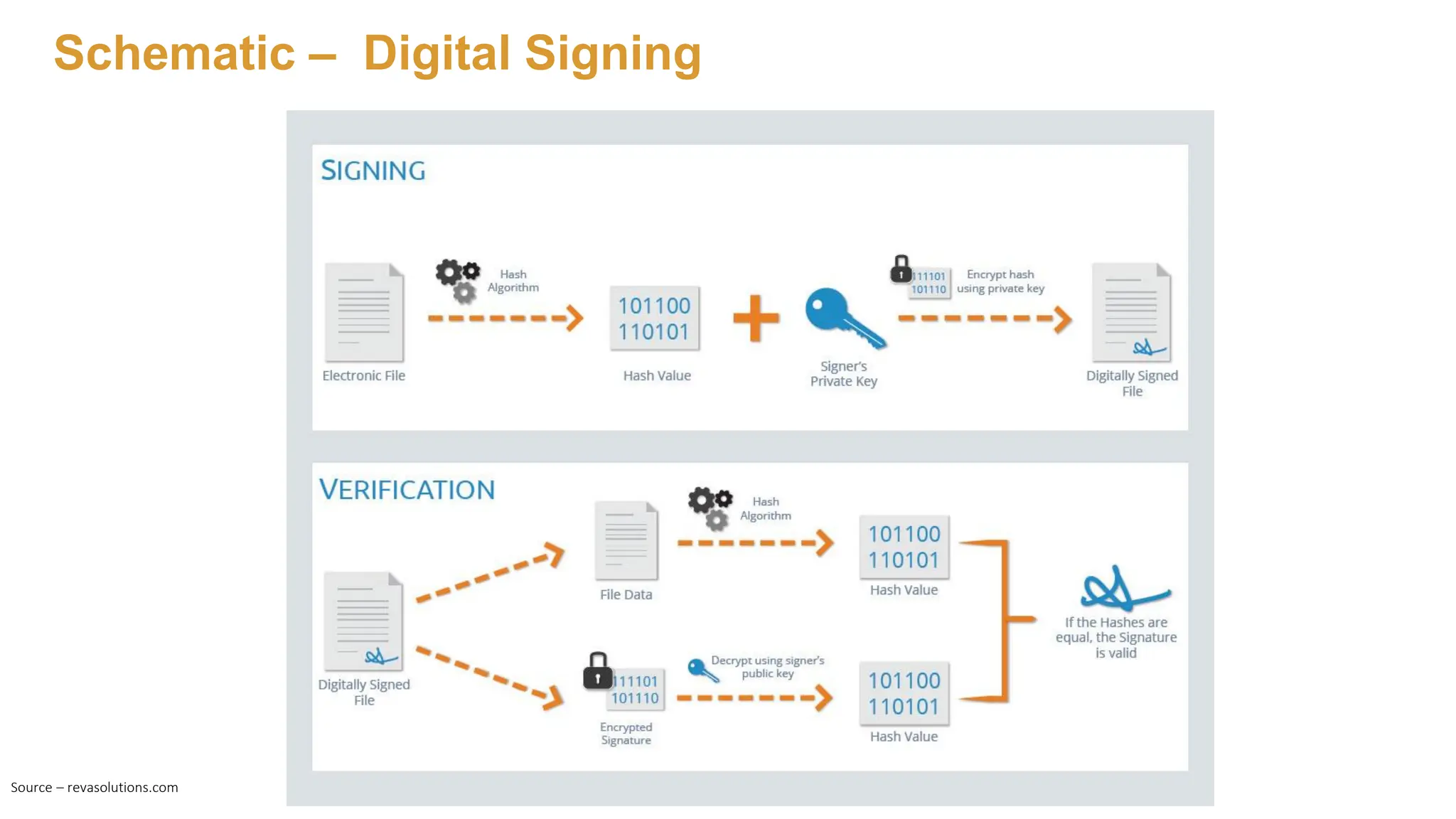

• Digital signaturesare used to authenticate the source of messages. The ownership of

a digital signature key is bound to a specific user, so a valid signature shows that the

message was sent by that user.

Integrity

• In many scenarios, the sender and receiver of a message need assurance that the

message has not been altered during transmission. Digital signatures provide this

feature by using cryptographic message digest functions.

Non-repudiation

• Digital signatures ensure that the sender who has signed the information cannot at a

later time deny having signed it.

Key elements of Digital signature

Cost Reduction anderror prevention.

• Reduce turnaround times by 80%, Significant ROI benefits, reduce document errors

• RBC saved 8 Million USD annually by shaving 82,000 staff hours and reduced

document errors by 75%

Enhanced Security

• Technologies using digital certificate signing have matured providing a very high

degree of assurance

Faster service delivery

• Much faster delivery and acceptance of digitally signed documents

User Convenience

• Customers are able to process signatures from any computer, tablet, or smartphone

Digital signatures provide the following key benefits

23.

• Product offeringsto customers

• Account opening

• Signature cards

• Standing orders

• Loan documents

• Investments

• Mortgage origination and closing

• Operational support materials, such as appraisals, disclosures, and employment

verification

• Vendor contracts

Key Banking processes for Digital signature adoption

24.

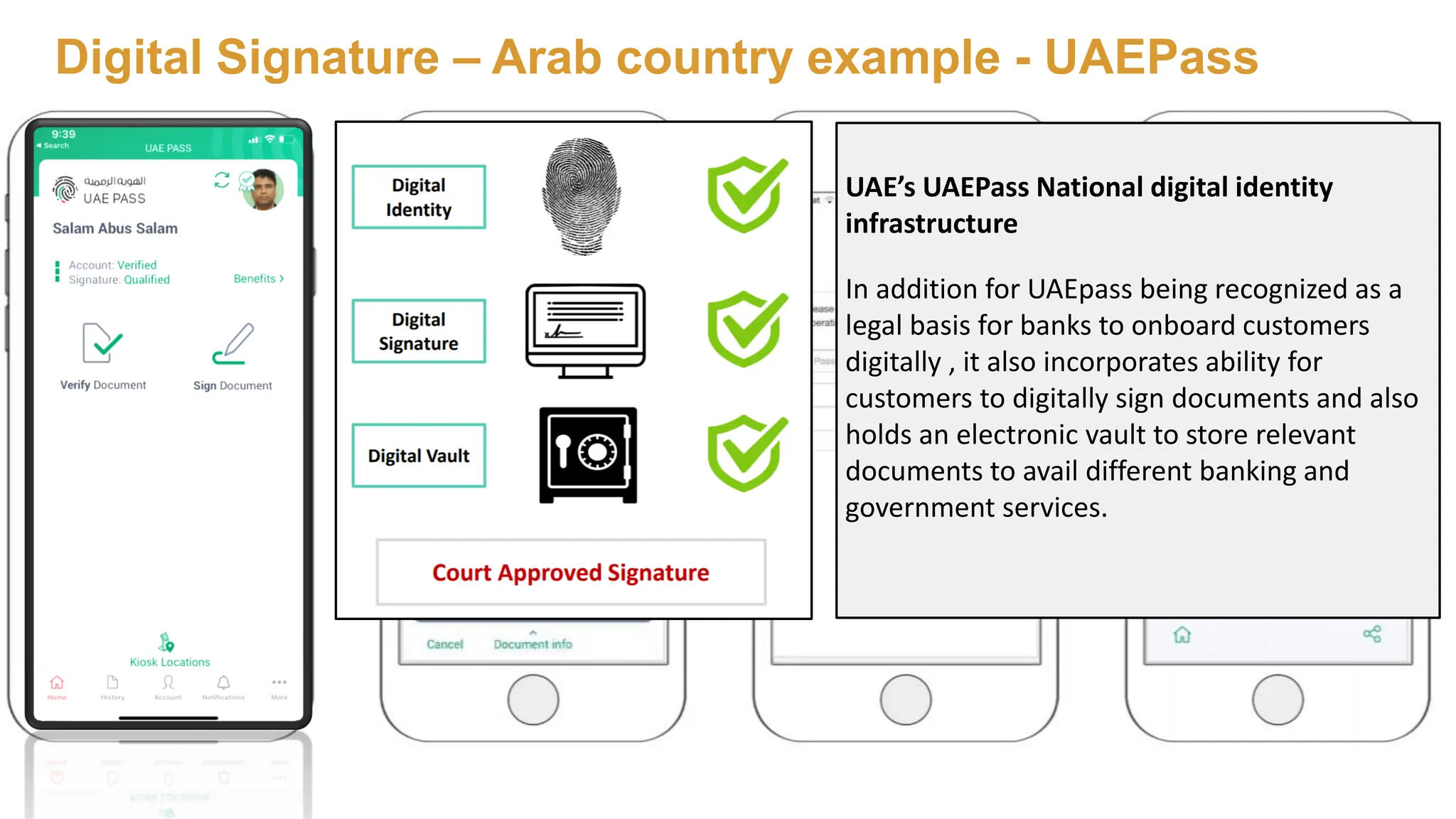

Digital Signature –Arab country example - UAEPass

UAE’s UAEPass National digital identity

infrastructure

In addition for UAEpass being recognized as a

legal basis for banks to onboard customers

digitally , it also incorporates ability for

customers to digitally sign documents and also

holds an electronic vault to store relevant

documents to avail different banking and

government services.

25.

Digital On-boarding andeKYC– Arab country examples

DMCC has implemented E-signature

DMCC is the first Free Zone in the UAE to offer electronic

signatures

Enabling DMCC members to execute signature requirements

on a range of documents online, from any device in any

location in a safe a secure way.

DMCC has partnered with DocuSign.

Free Zone in the UAE

26.

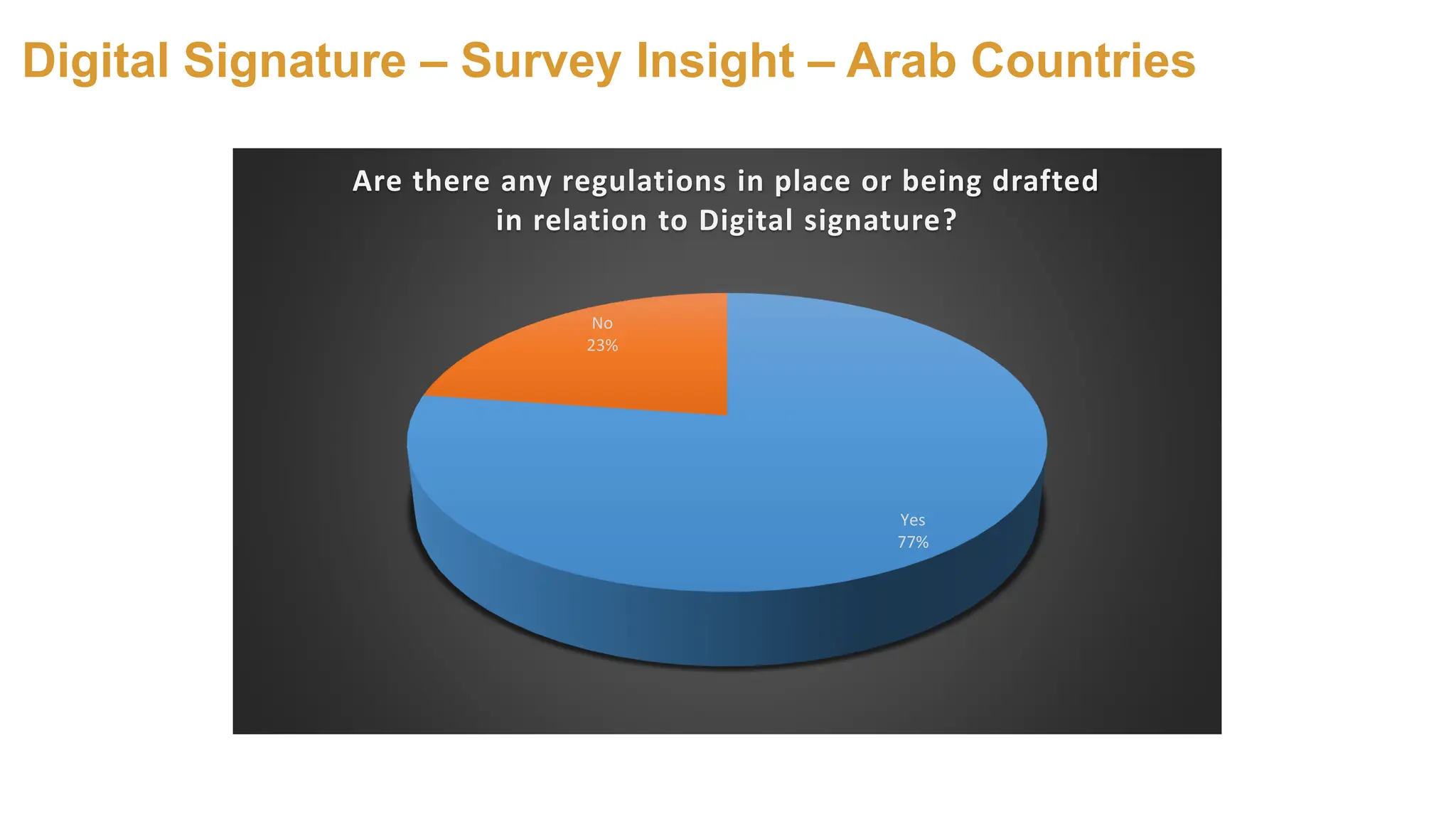

Digital Signature –Survey Insight – Arab Countries

Yes

77%

No

23%

Are there any regulations in place or being drafted

in relation to Digital signature?

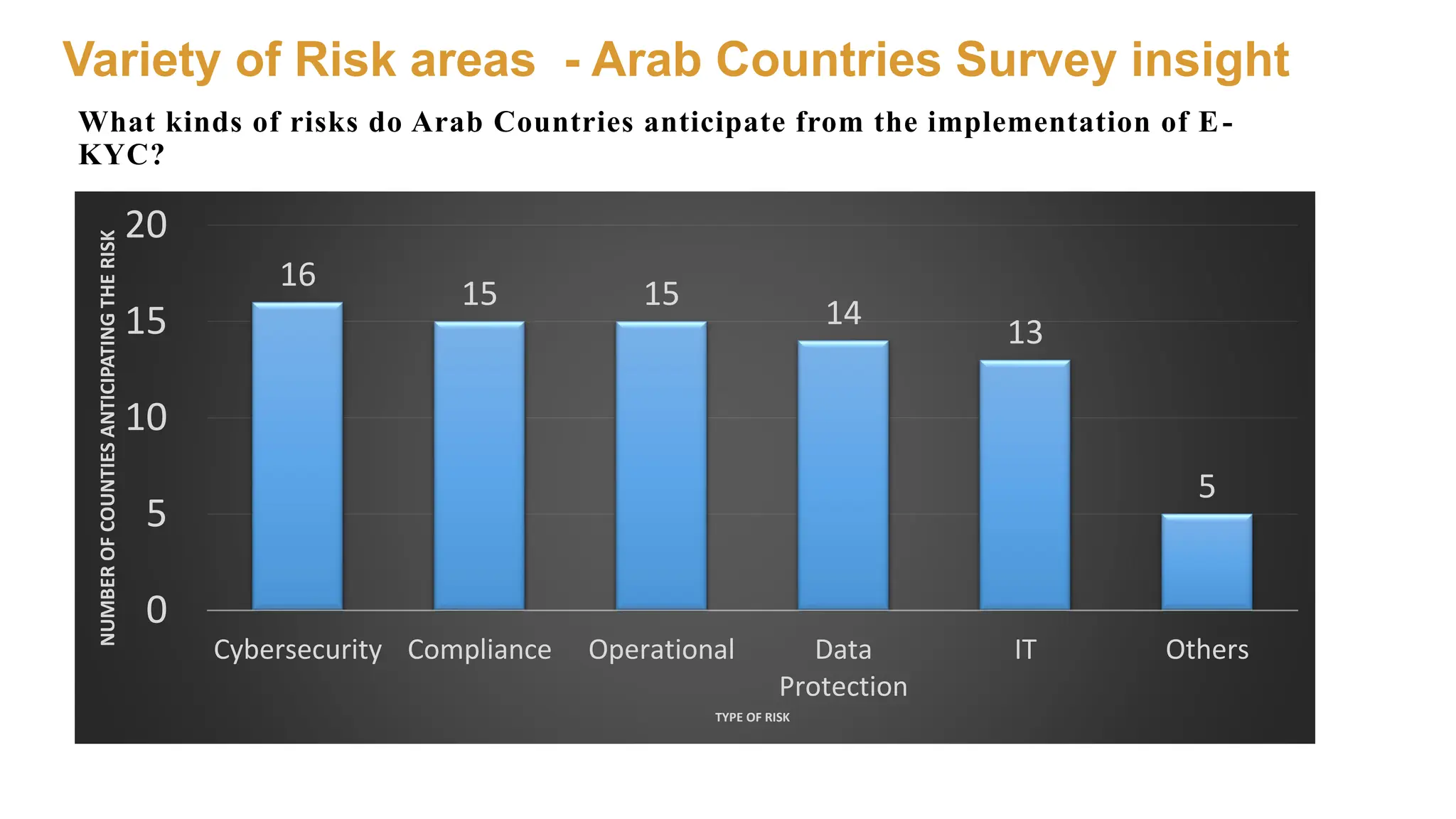

Variety of Riskareas - Arab Countries Survey insight

What kinds of risks do Arab Countries anticipate from the implementation of E-

KYC?

16

15 15

14

13

5

0

5

10

15

20

Cybersecurity Compliance Operational Data

Protection

IT Others

NUMBER

OF

COUNTIES

ANTICIPATING

THE

RISK

TYPE OF RISK

33.

Key Challenges inDigital onboarding, eKYC

- No common Global standards for eKYC

- Address Verification (Especially unbanked and underprivileged sections)

- Periodic updation of eKYC and Legal documentation status

- Disparities in eKYC compliance legislation and mandates (FATCA, GDPR, IFRS9 )

- Enhanced due diligence demands additional scrutiny and documentation

- Cybersecurity provisioning is demanding (to avoid phishing, ID misuse etc)

- Some regions present internet connectivity challenges prevent digital banking

outreach

• Digital identificationhas been established as a means to propel economies and create deep and lasting

value to the quality of life of the citizens and also to the efficient and cost effective functioning of the

Governments

• Almost all Arab countries embarking upon digital identification for their citizens as part of their vision

and digitization roadmap

• The technical architecture towards achieving true customer digital on-boarding with robust e-KYC and

compliance, AML, ATF deterrents is quite mature and several case studies are available to be adapted

• Survey feedback from the Central banks of the Arab countries reveal that the vision of the Arab

countries is to focus and lead in the domain of e-governance for betterment of the lives of their

citizens and residents

• The challenges are not unsurmountable and there are many enabling foundational technologies and

vendors who can provide solutions in this space.

Conclusion

Conclusion

www.amf.org

FintechWG@amf.org.ae

This presentation isa product of the AMF Regional Fintech Technical Working group for the Arab Monetary Fund

All product names, logos, brands, trademarks and registered trademarks referred in this document are property of their respective owners. All company, product and service names

used are for identification purposes only. Use of these names, trademarks and brands does not imply endorsement