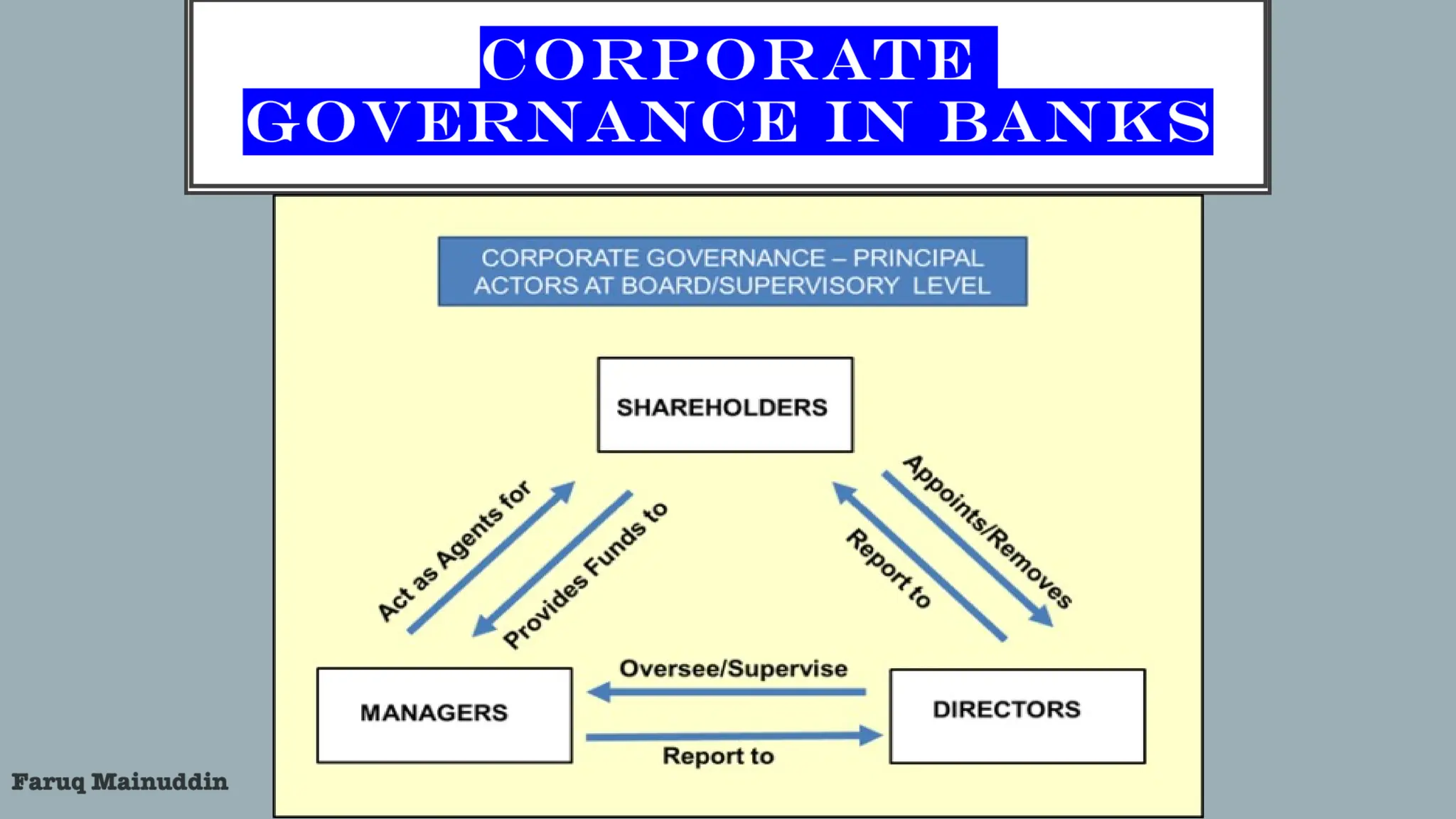

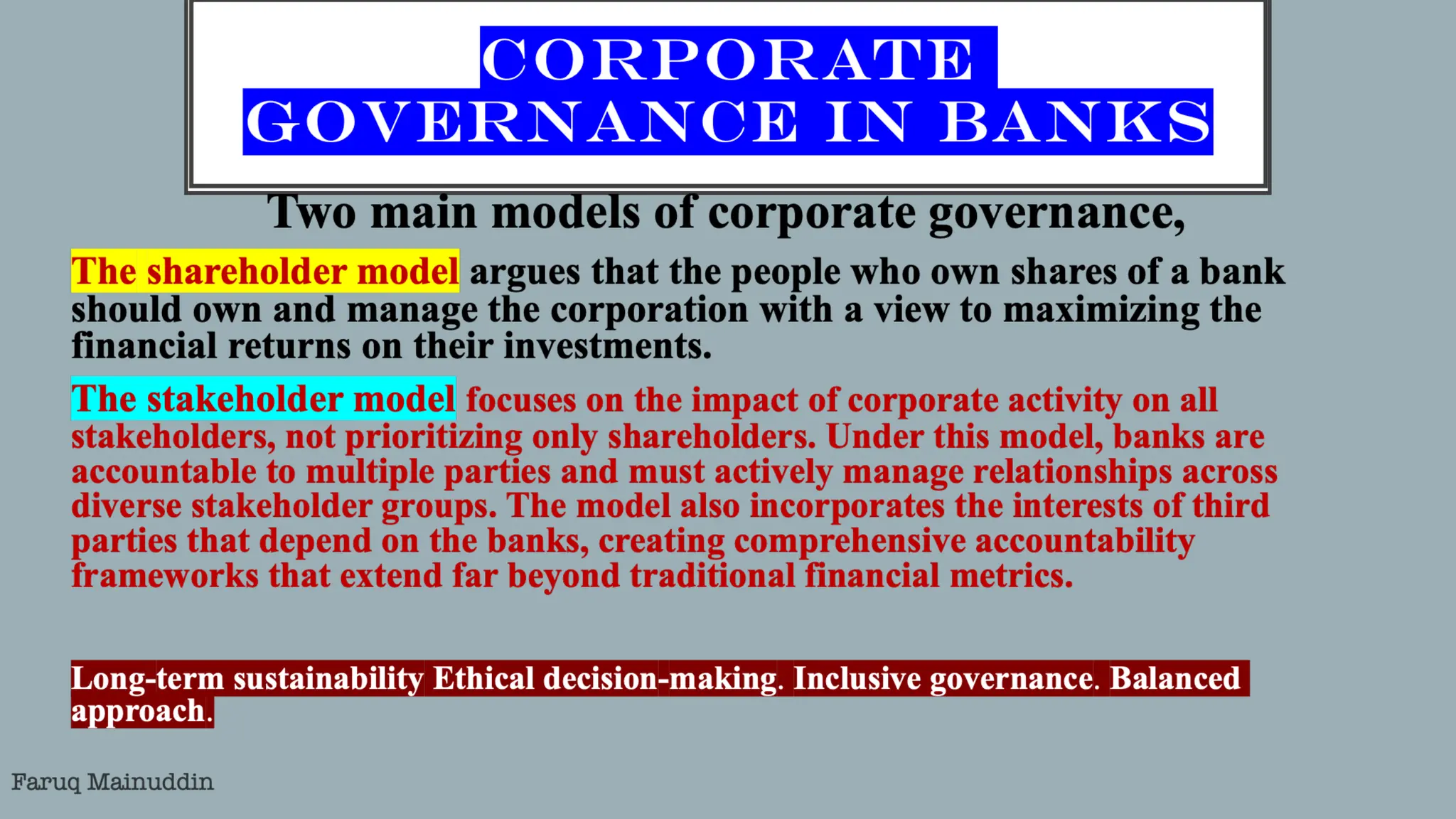

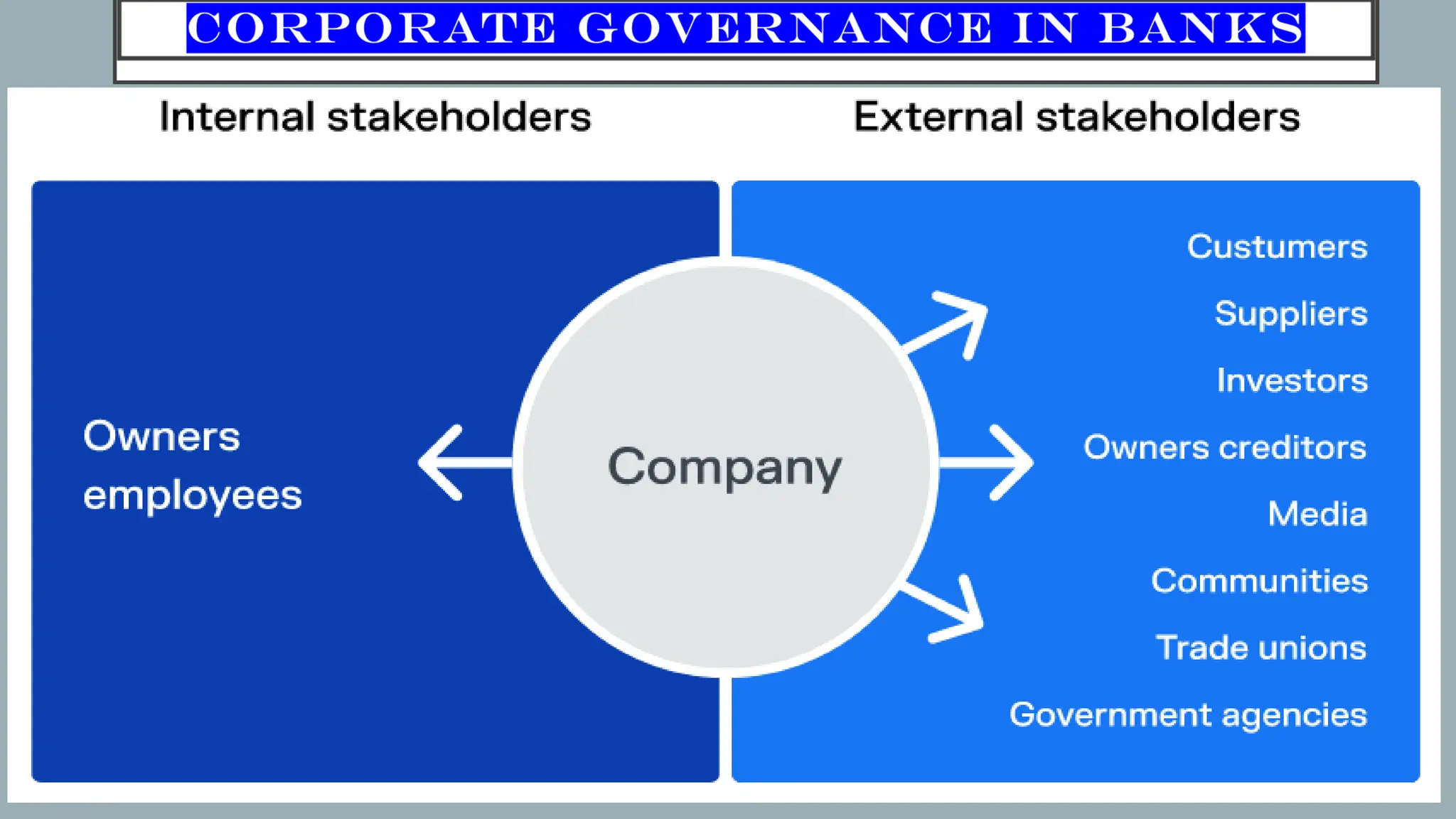

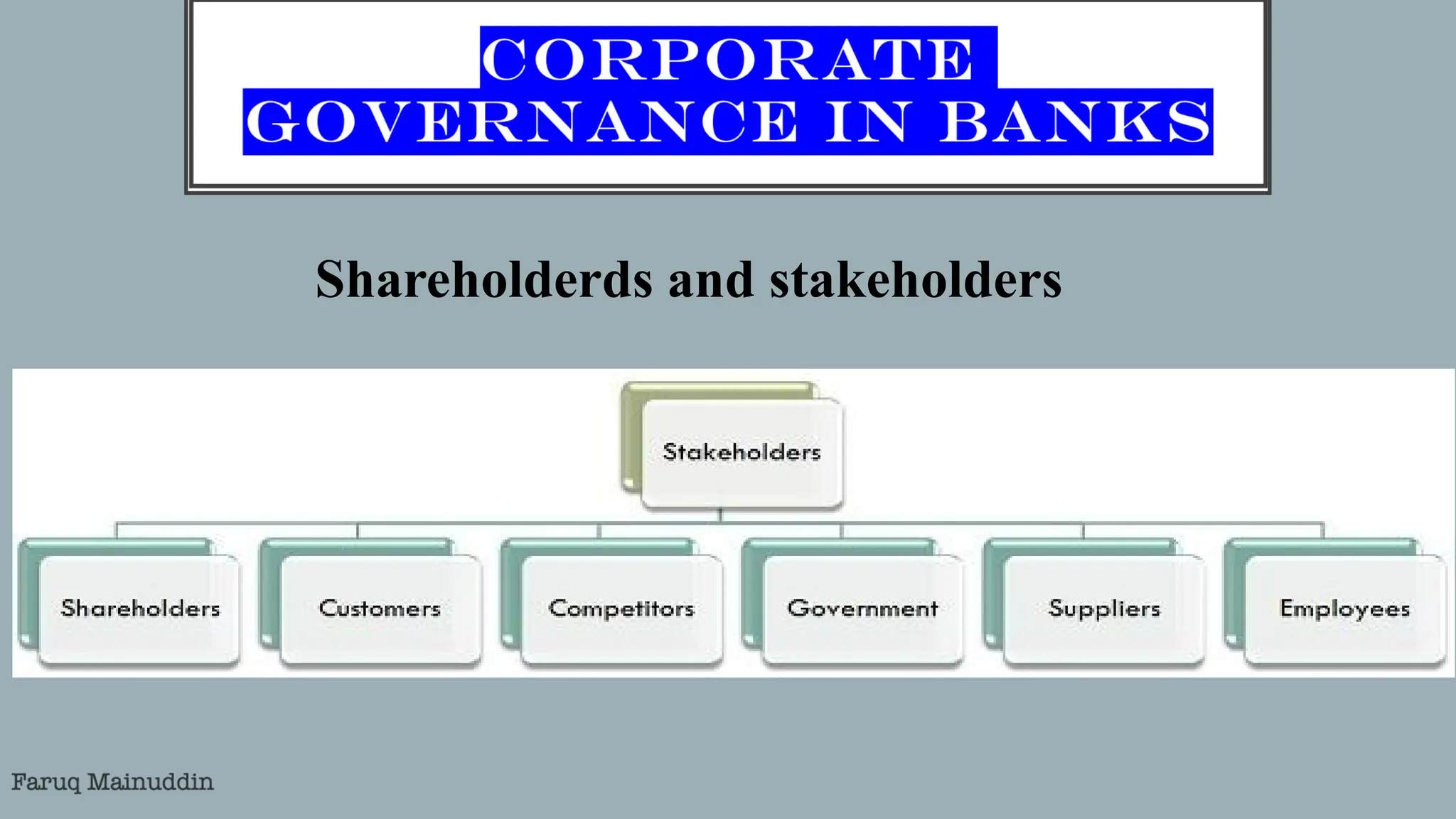

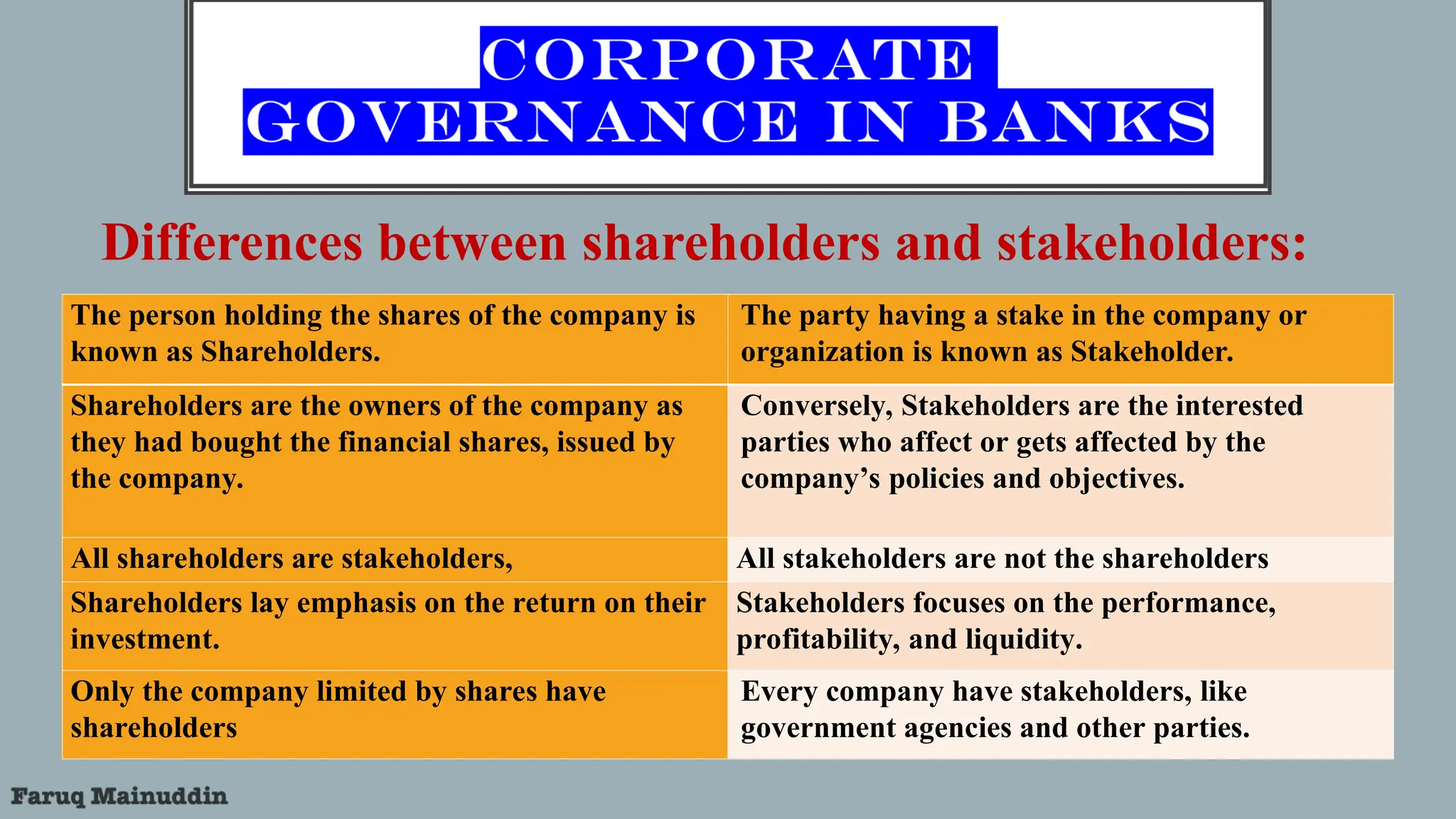

Differences between shareholdersand stakeholders:

The person holding the shares of the company is

known as Shareholders.

The party having a stake in the company or

organization is known as Stakeholder.

Shareholders are the owners of the company as

they had bought the financial shares, issued by

the company.

Conversely, Stakeholders are the interested

parties who affect or gets affected by the

company’s policies and objectives.

All shareholders are stakeholders, All stakeholders are not the shareholders

Shareholders lay emphasis on the return on their

investment.

Stakeholders focuses on the performance,

profitability, and liquidity.

Only the company limited by shares have

shareholders

Every company have stakeholders, like

government agencies and other parties.

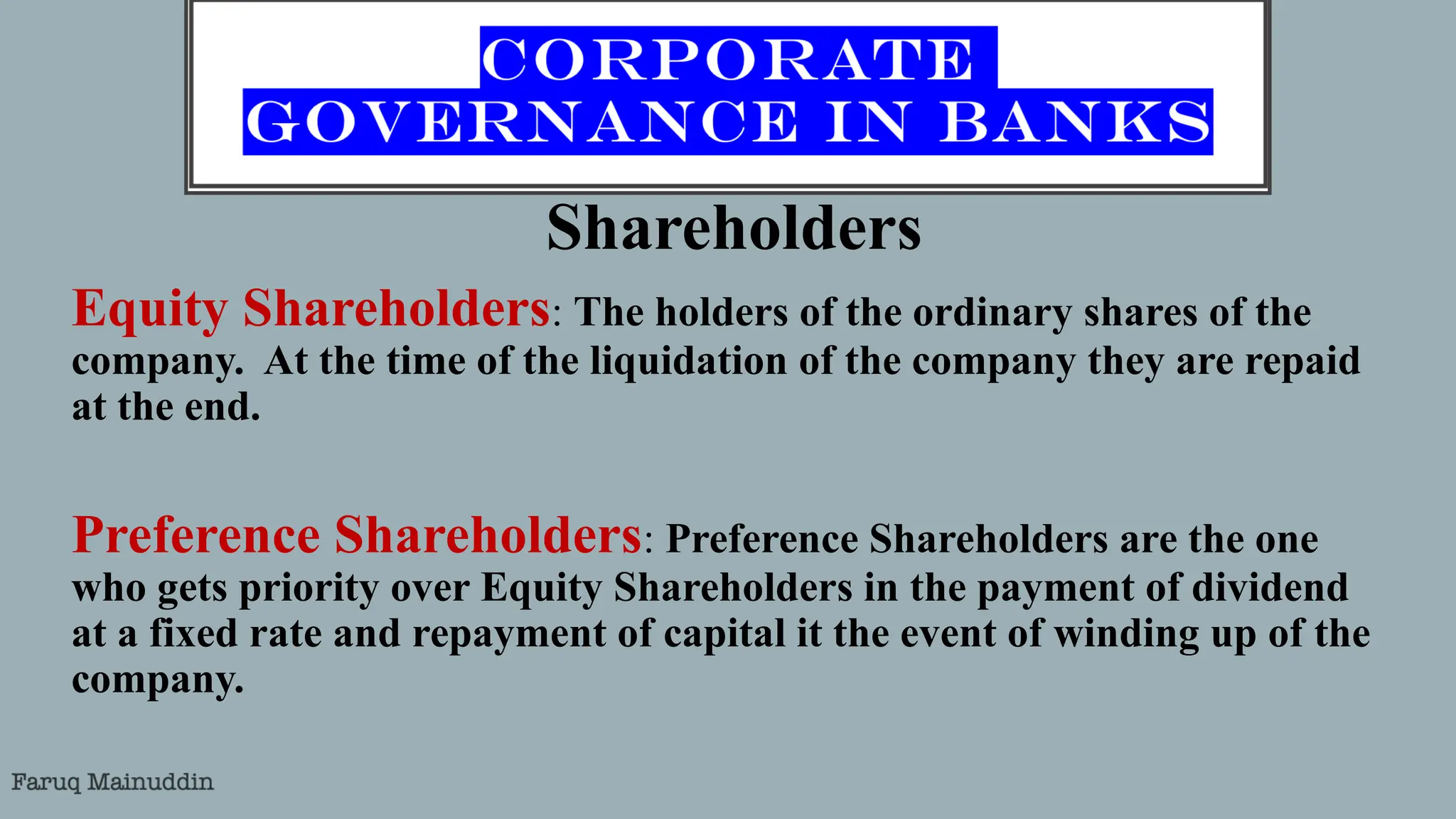

17.

Shareholders

Equity Shareholders: Theholders of the ordinary shares of the

company. At the time of the liquidation of the company they are repaid

at the end.

Preference Shareholders: Preference Shareholders are the one

who gets priority over Equity Shareholders in the payment of dividend

at a fixed rate and repayment of capital it the event of winding up of the

company.

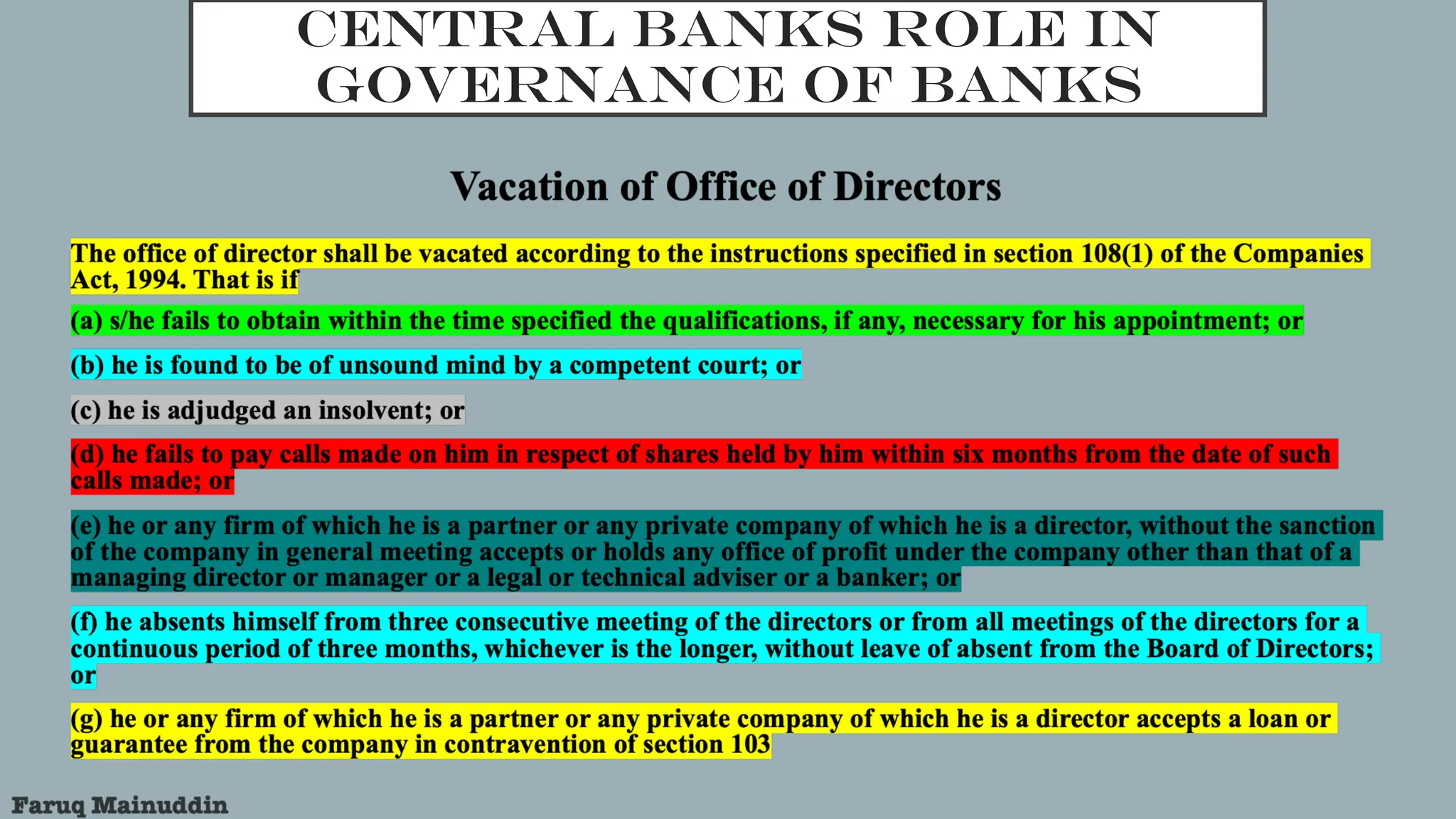

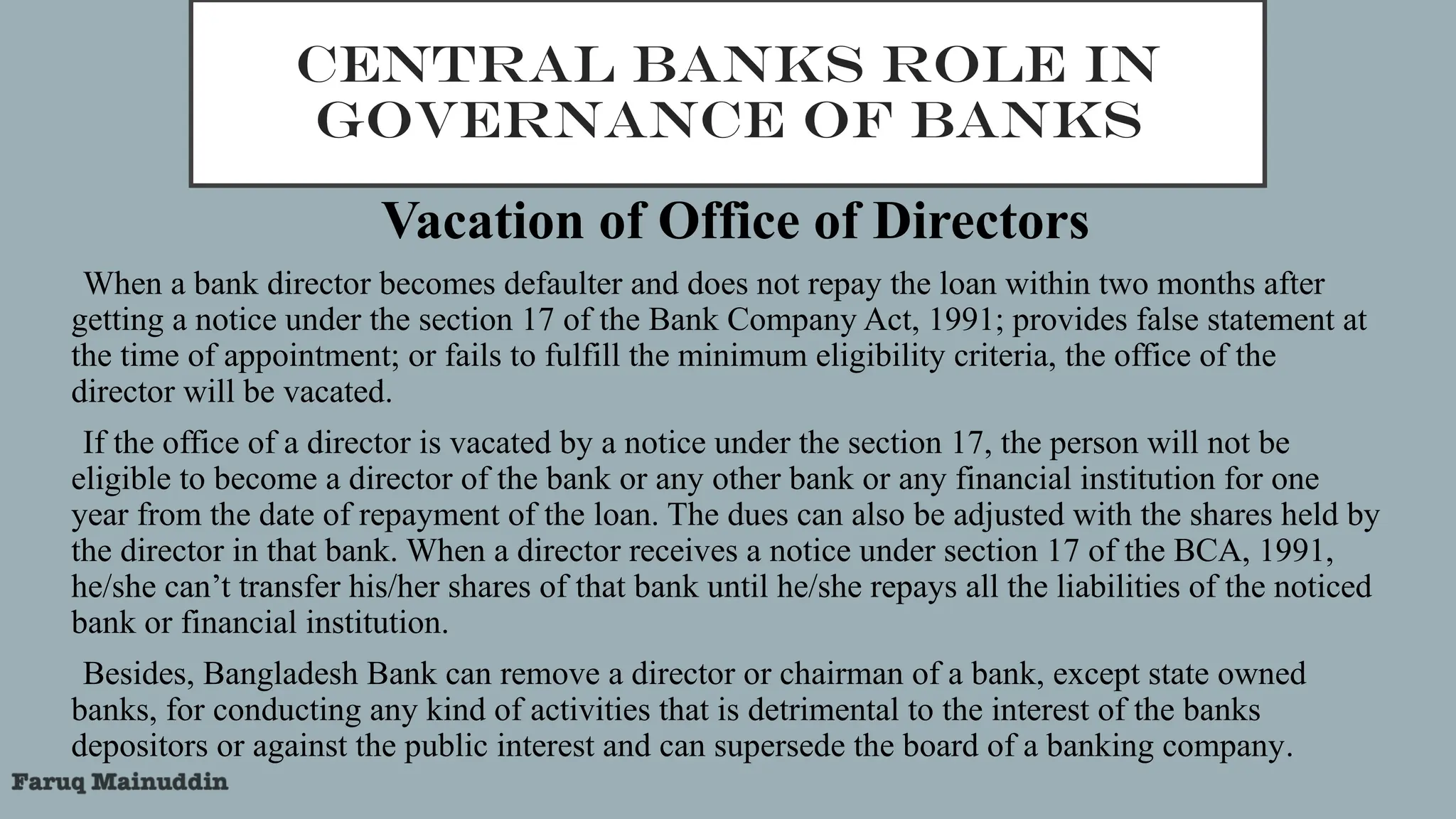

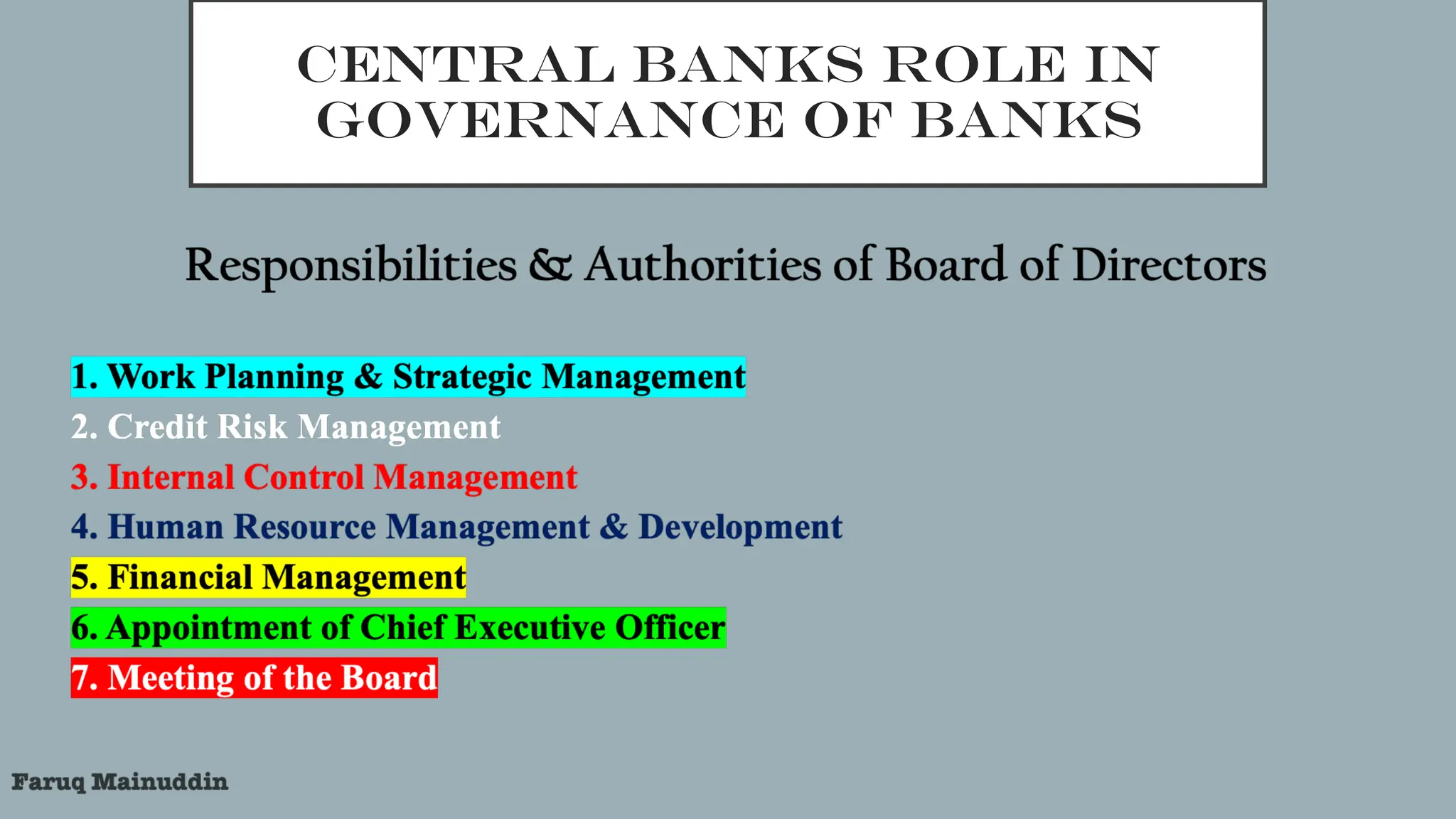

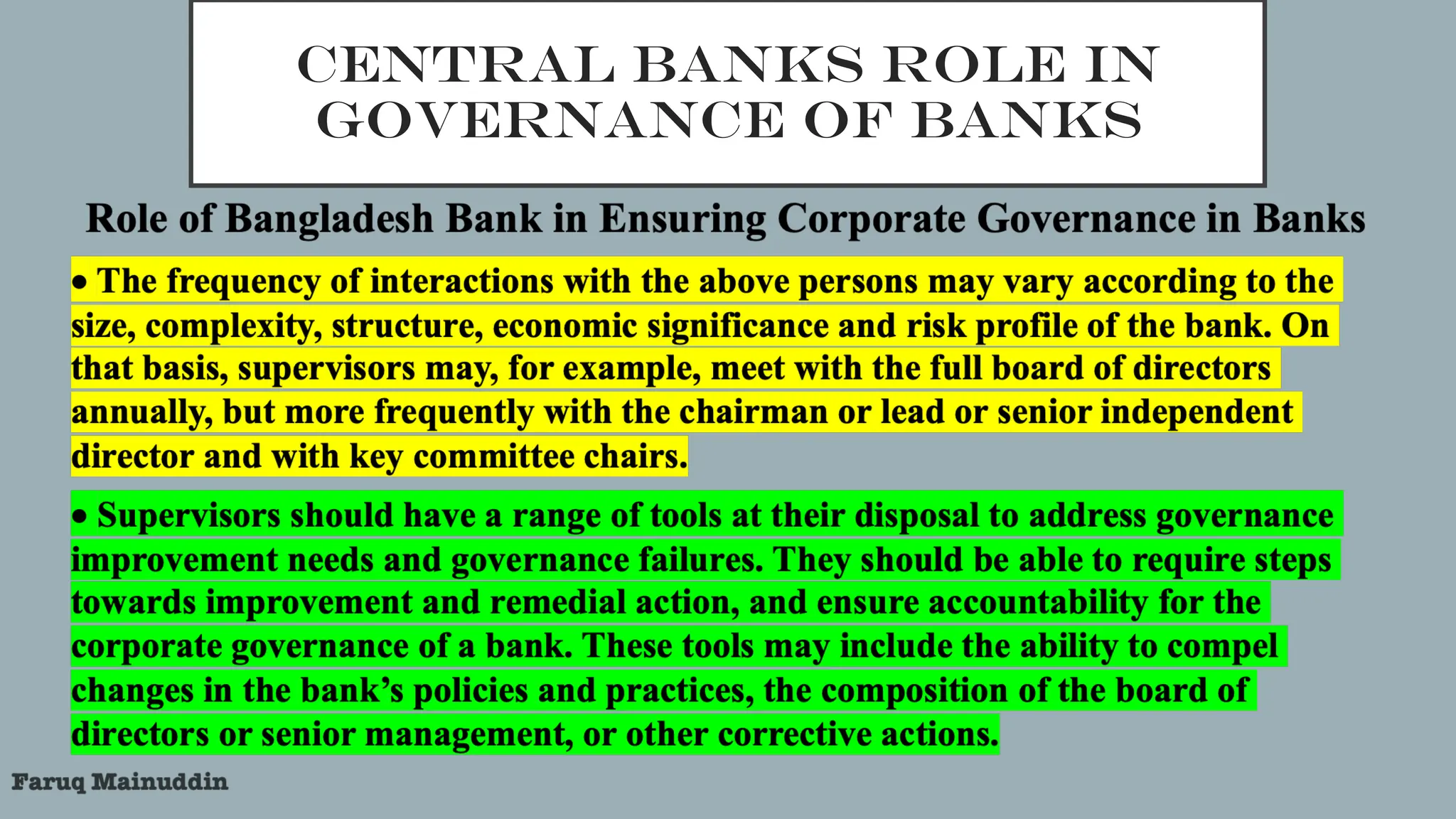

CENTRAL BANKS ROLEIN

GOVERNANCE OF BANKS

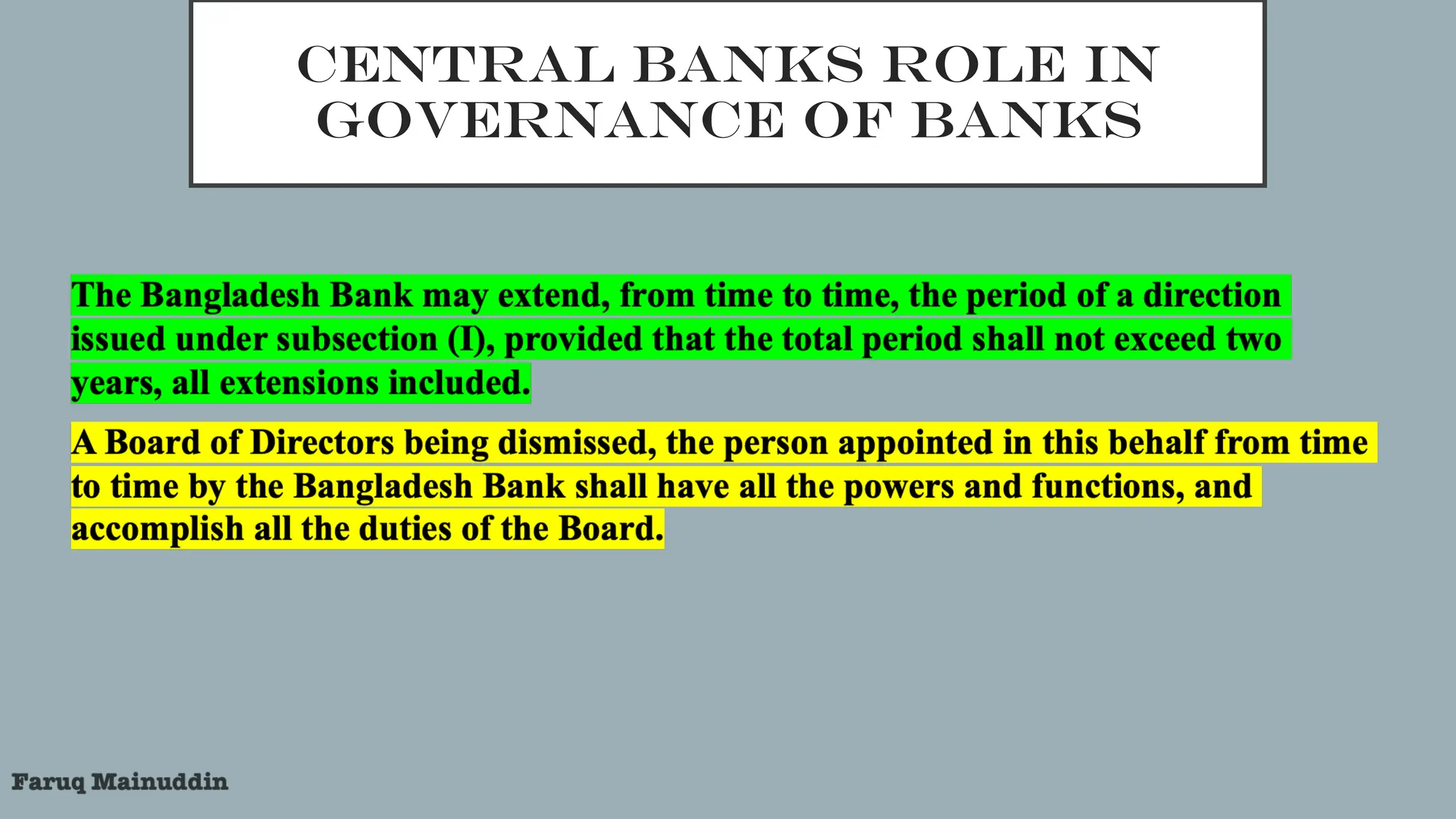

Vacation of Office of Directors

•When a bank director becomes defaulter and does not repay the loan within two months after

getting a notice under the section 17 of the Bank Company Act, 1991; provides false statement at

the time of appointment; or fails to fulfill the minimum eligibility criteria, the office of the

director will be vacated.

•If the office of a director is vacated by a notice under the section 17, the person will not be

eligible to become a director of the bank or any other bank or any financial institution for one

year from the date of repayment of the loan. The dues can also be adjusted with the shares held by

the director in that bank. When a director receives a notice under section 17 of the BCA, 1991,

he/she can’t transfer his/her shares of that bank until he/she repays all the liabilities of the noticed

bank or financial institution.

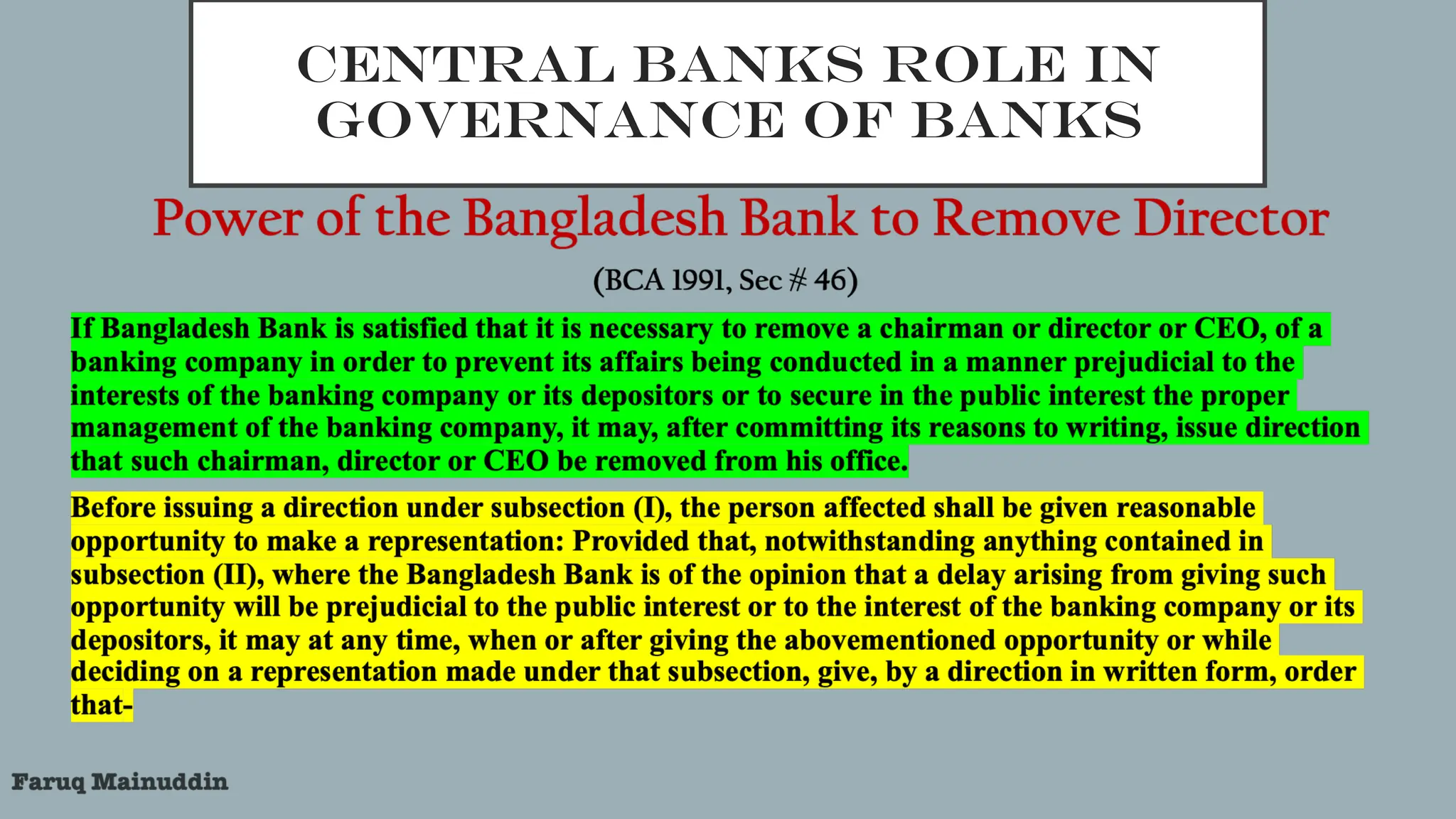

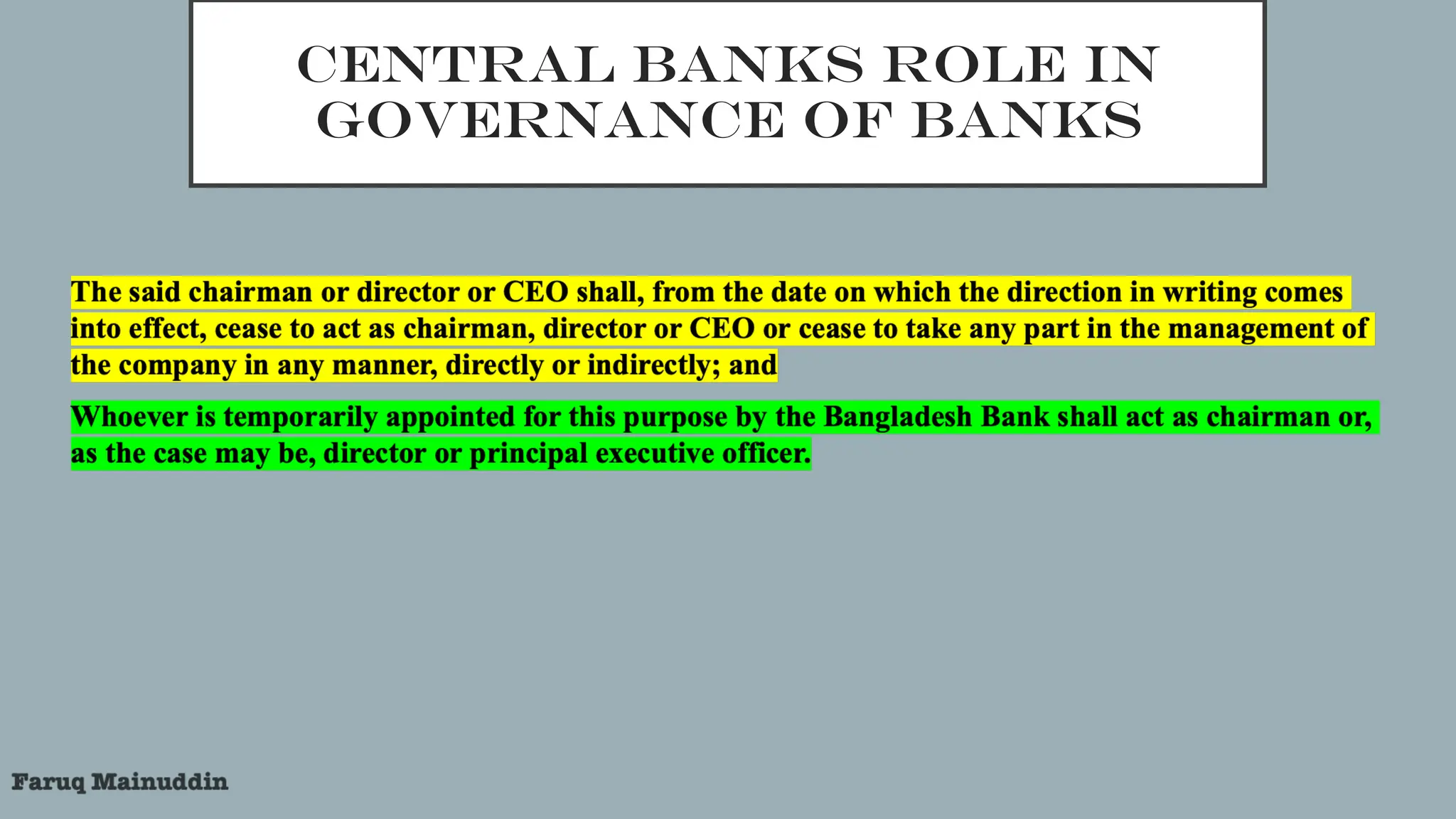

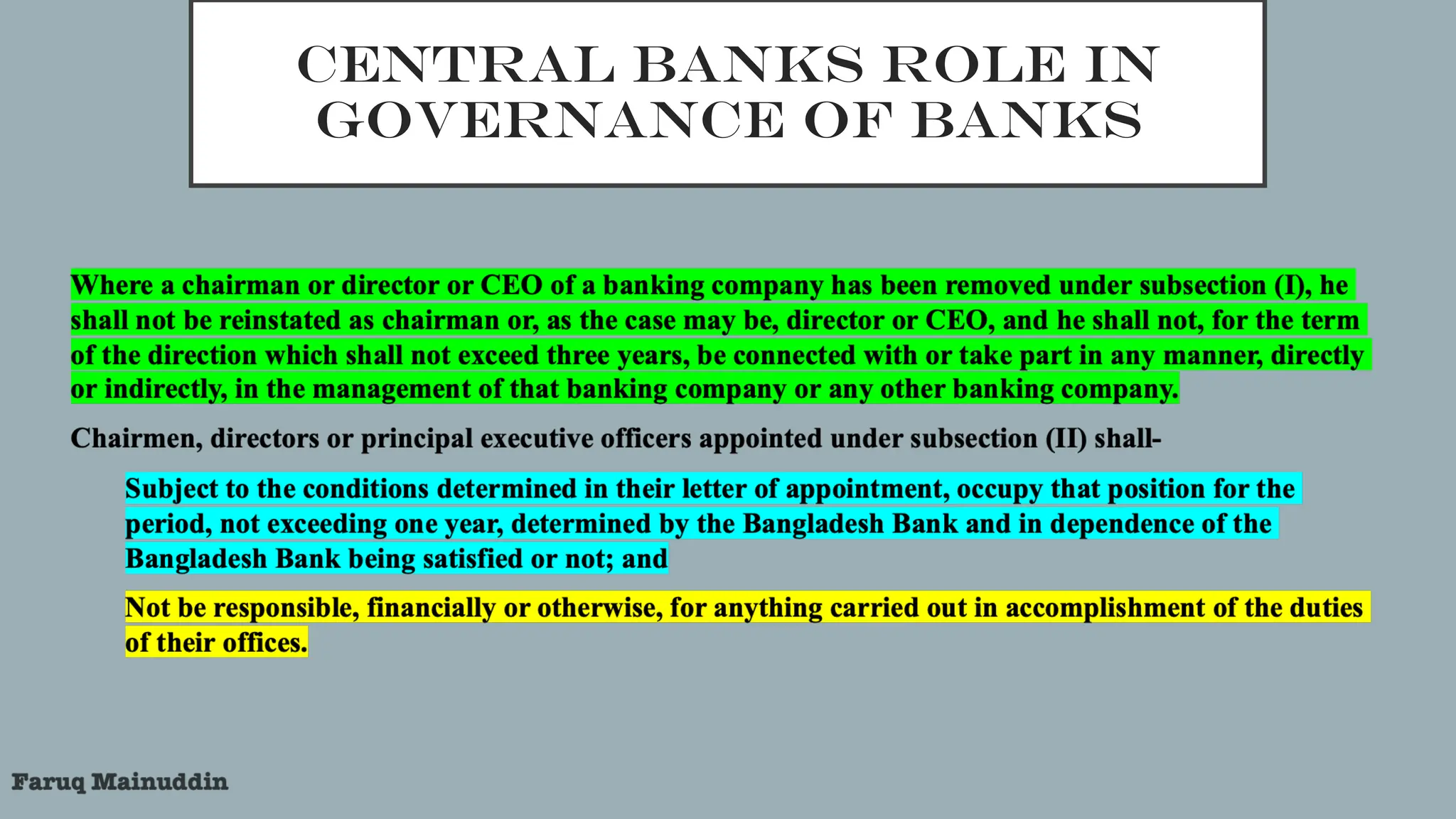

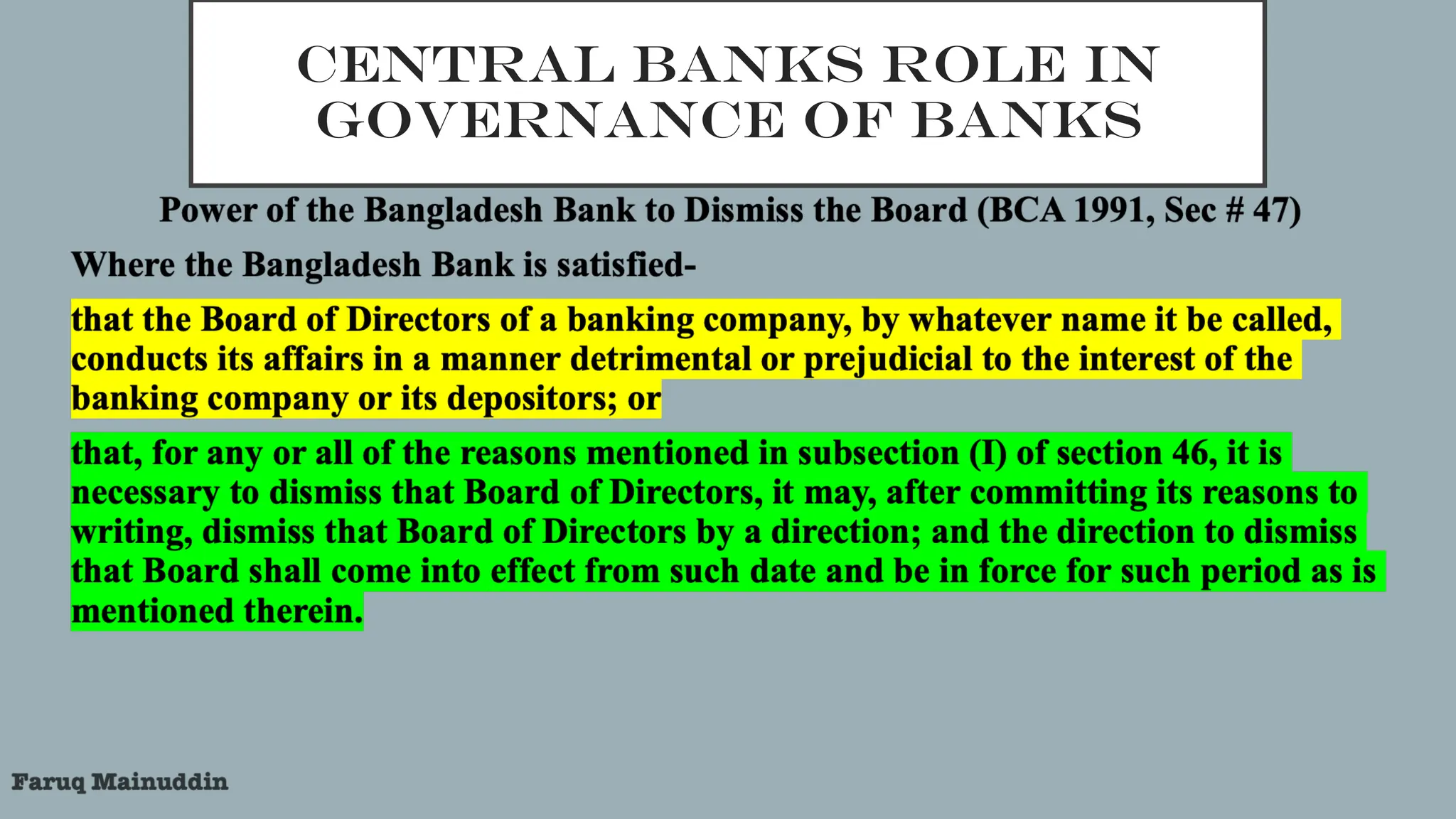

•Besides, Bangladesh Bank can remove a director or chairman of a bank, except state owned

banks, for conducting any kind of activities that is detrimental to the interest of the banks

depositors or against the public interest and can supersede the board of a banking company.

26.

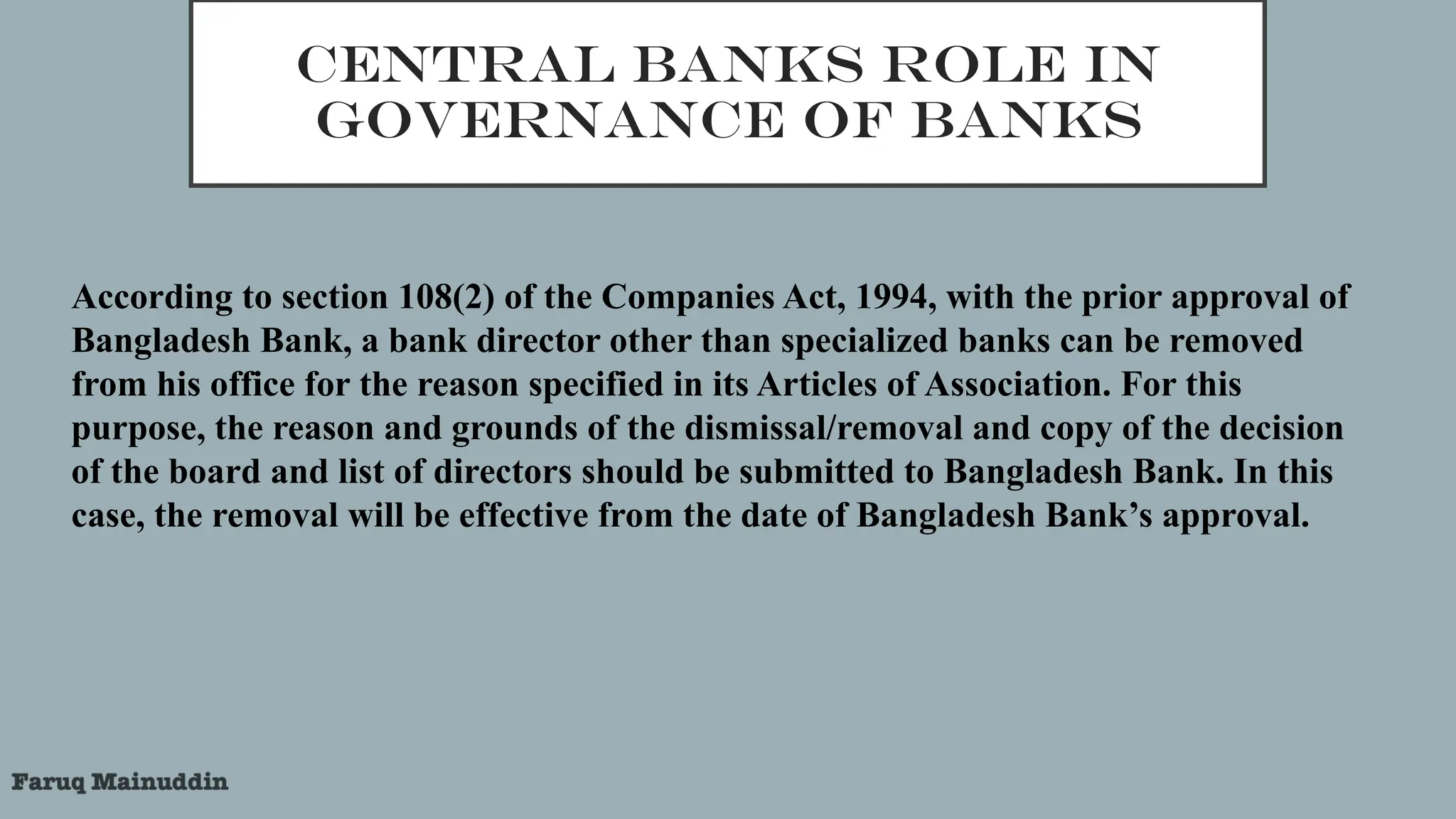

CENTRAL BANKS ROLEIN

GOVERNANCE OF BANKS

According to section 108(2) of the Companies Act, 1994, with the prior approval of

Bangladesh Bank, a bank director other than specialized banks can be removed

from his office for the reason specified in its Articles of Association. For this

purpose, the reason and grounds of the dismissal/removal and copy of the decision

of the board and list of directors should be submitted to Bangladesh Bank. In this

case, the removal will be effective from the date of Bangladesh Bank’s approval.

CENTRAL BANKS ROLEIN

GOVERNANCE OF BANKS

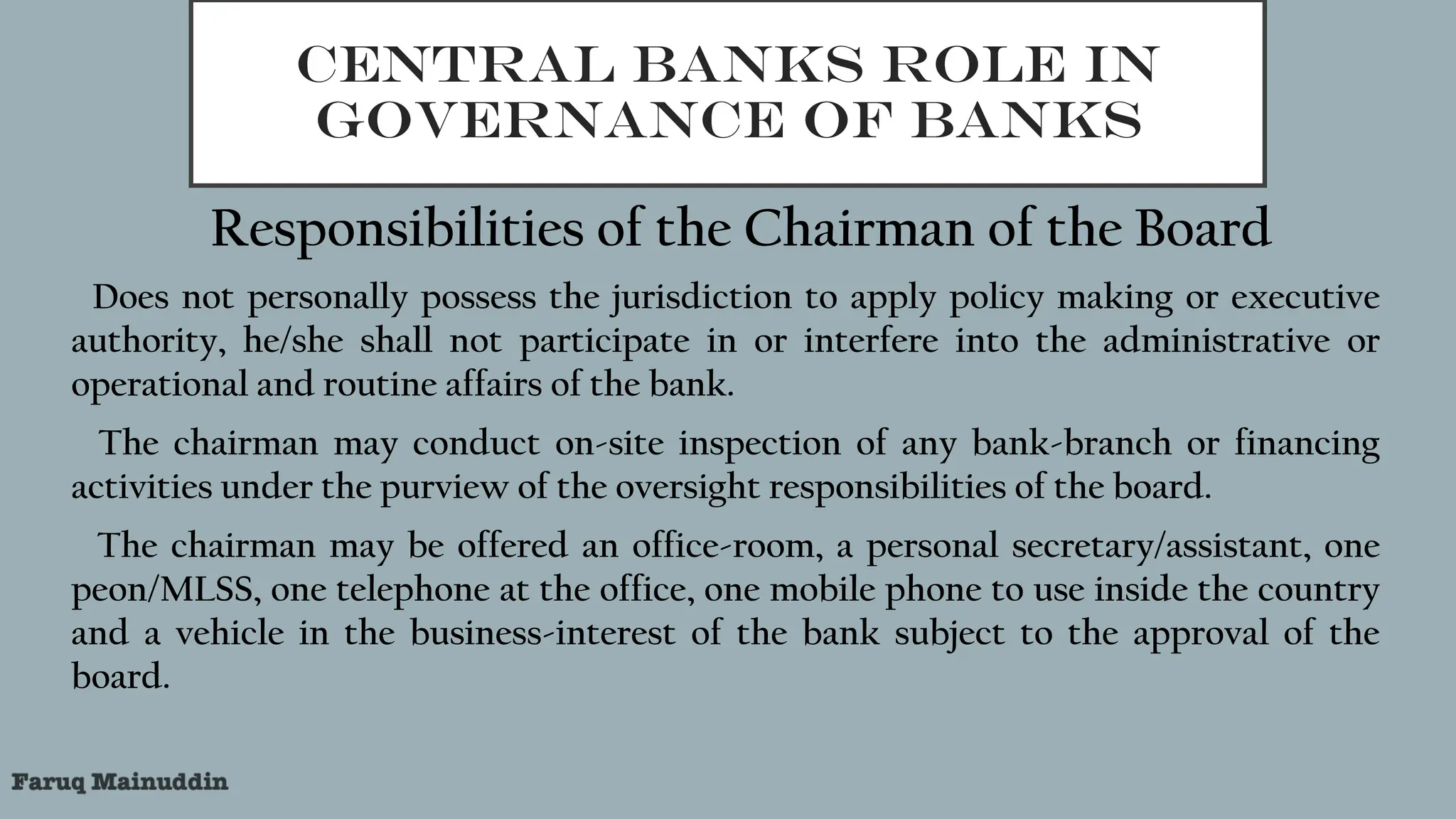

Responsibilities of the Chairman of the Board

1.Does not personally possess the jurisdiction to apply policy making or executive

authority, he/she shall not participate in or interfere into the administrative or

operational and routine affairs of the bank.

2.The chairman may conduct on-site inspection of any bank-branch or financing

activities under the purview of the oversight responsibilities of the board.

3.The chairman may be offered an office-room, a personal secretary/assistant, one

peon/MLSS, one telephone at the office, one mobile phone to use inside the country

and a vehicle in the business-interest of the bank subject to the approval of the

board.

29.

CENTRAL BANKS ROLEIN

GOVERNANCE OF BANKS

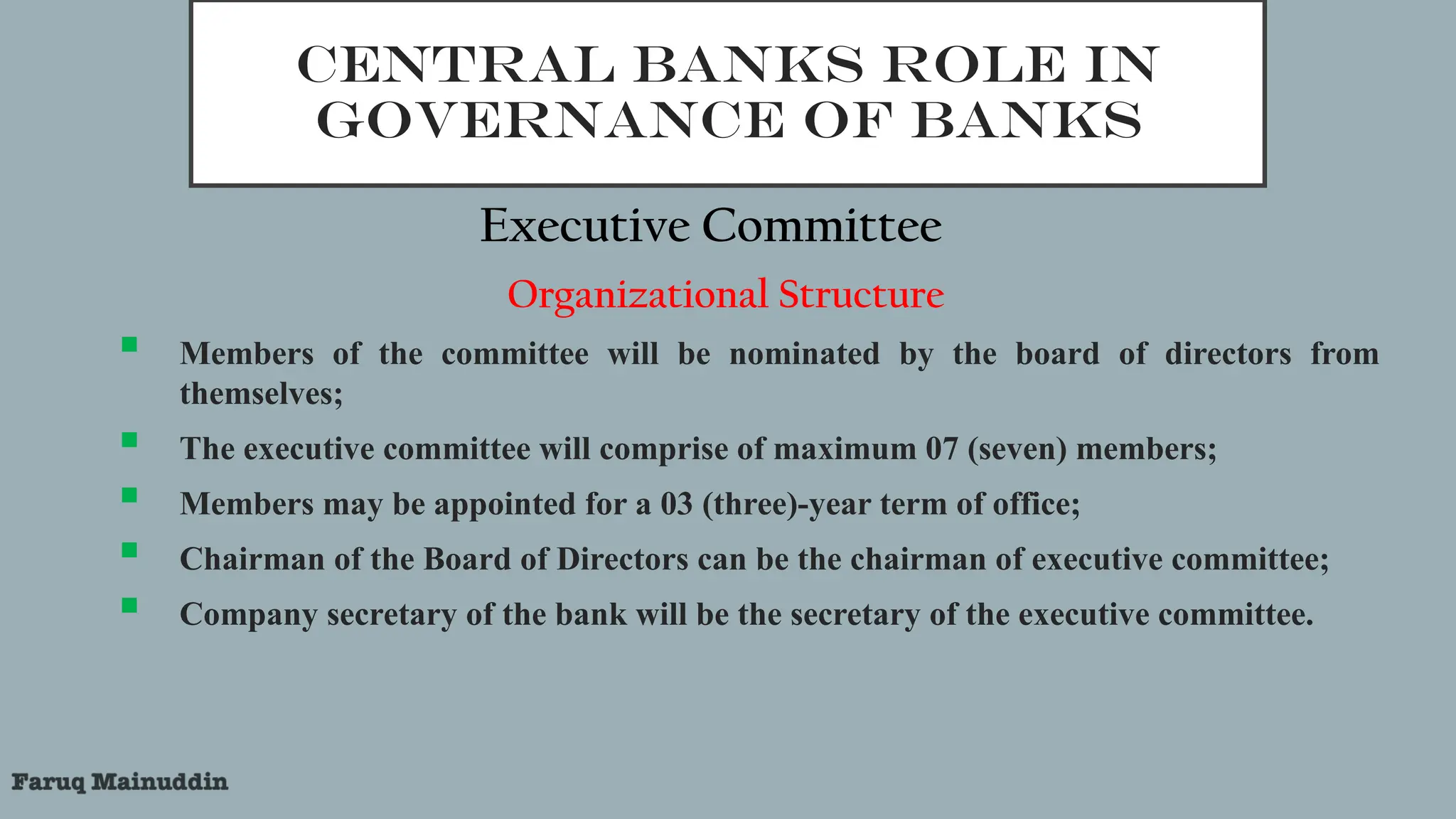

Executive Committee

Organizational Structure

Members of the committee will be nominated by the board of directors from

themselves;

The executive committee will comprise of maximum 07 (seven) members;

Members may be appointed for a 03 (three)-year term of office;

Chairman of the Board of Directors can be the chairman of executive committee;

Company secretary of the bank will be the secretary of the executive committee.

30.

CENTRAL BANKS ROLEIN

GOVERNANCE OF BANKS

Executive Committee………….contd.

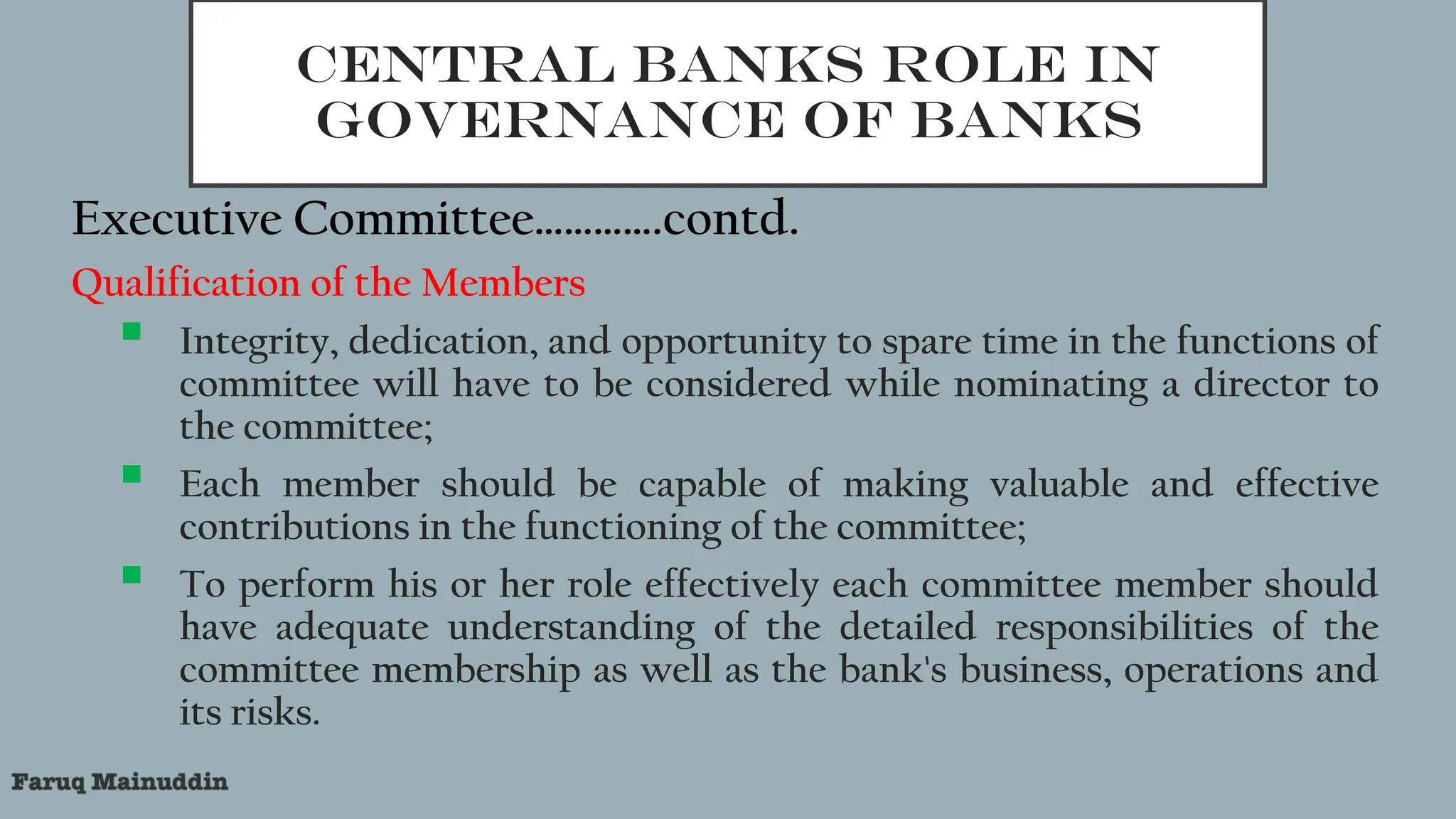

Qualification of the Members

Integrity, dedication, and opportunity to spare time in the functions of

committee will have to be considered while nominating a director to

the committee;

Each member should be capable of making valuable and effective

contributions in the functioning of the committee;

To perform his or her role effectively each committee member should

have adequate understanding of the detailed responsibilities of the

committee membership as well as the bank's business, operations and

its risks.

31.

CENTRAL BANKS ROLEIN

GOVERNANCE OF BANKS

Executive Committee………….contd.

Roles & Responsibilities of the Executive Committee

The executive committee can decide or can act in those cases as

instructed by the Board of directors that are not specifically assigned on

full board through the Bank Company Act, 1991 and other laws and

regulations.

The executive committee can take all necessary decision or can

approve cases within power delegated by the board of directors.

All decisions taken in the executive committee should be ratified in

the next board meeting.

32.

CENTRAL BANKS ROLEIN

GOVERNANCE OF BANKS

Executive Committee………….contd.

Meetings

The executive committee can sit any time as it may deem fit.

The committee may invite Chief Executive Officer, Head of internal audit or any

other Officer to its meetings, if it deems necessary;

To ensure active participation and contribution by the members, a detailed

memorandum should be distributed to committee members well in advance before

each meeting;

All decisions/observations of the committee should be noted in minutes.

33.

CENTRAL BANKS ROLEIN

GOVERNANCE OF BANKS

Audit Committee

Organizational Structure

Members of the committee will be nominated by the board of directors from

the directors;

The audit committee will comprise of maximum 05 (five) members, with

minimum 2 (two) independent director;

Audit committee will comprise with directors who are not executive

committee members;

Members may be appointed for a 03 (three) year term of office;

Company secretary of the bank will be the secretary of the audit committee.

34.

CENTRAL BANKS ROLEIN

GOVERNANCE OF BANKS

Audit Committee…….contd.

Qualification of the Members

Integrity, dedication, and opportunity to spare time in the functions of committee will

have to be considered while nominating a director to the committee ;

Each member should be capable of making valuable and effective contributions in the

functioning of the committee;

To perform his or her role effectively each committee member should have adequate

understanding of the detailed responsibilities of the committee membership as well as the

bank's business, operations and its risks.

Professionally Experienced persons in banking/financial institutions specially having

educational qualification in Finance, Banking, Management, Economics, Accounting will get

preference in forming the committee.

35.

CENTRAL BANKS ROLEIN

GOVERNANCE OF BANKS

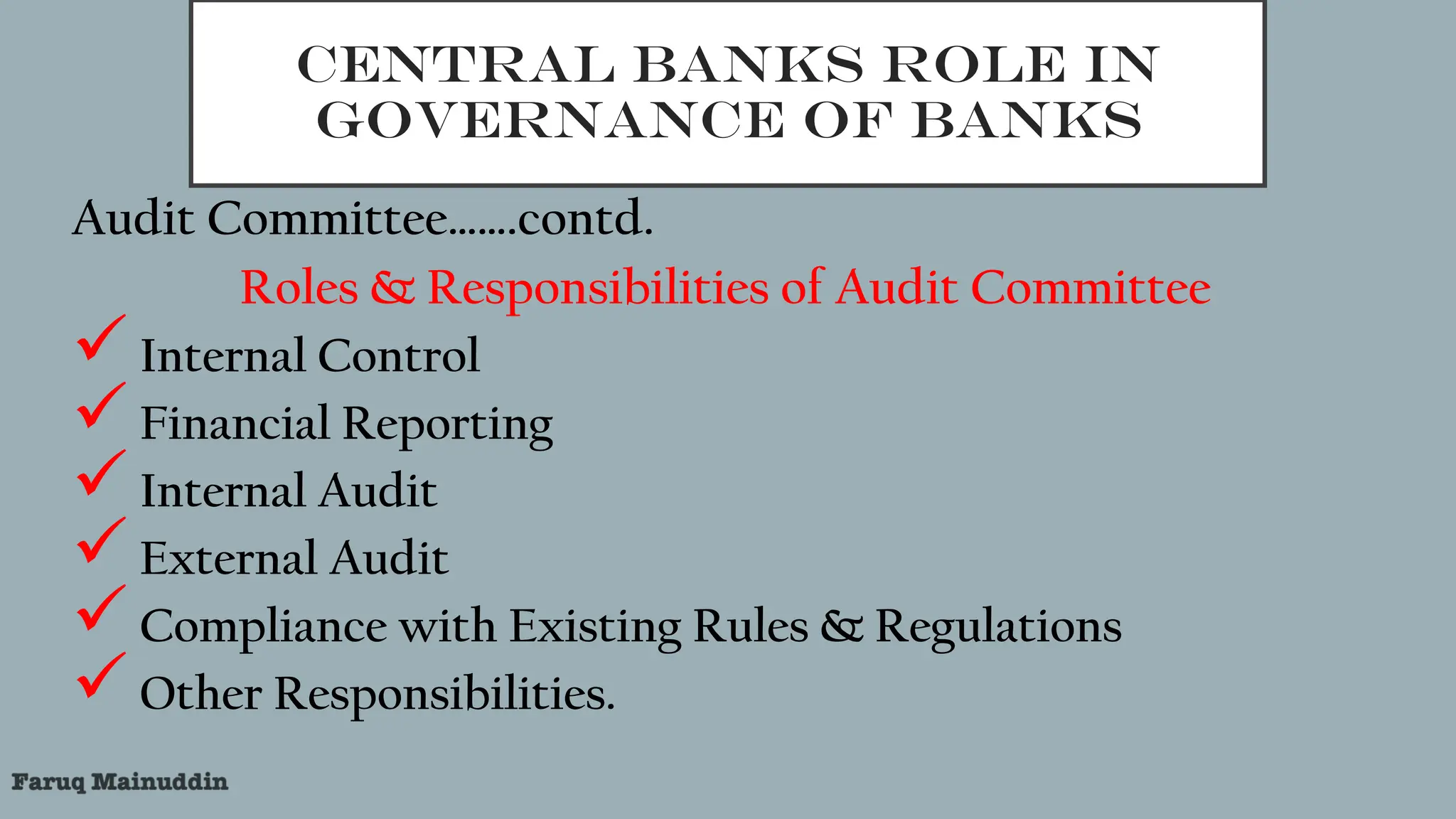

Audit Committee…….contd.

Roles & Responsibilities of Audit Committee

Internal Control

Financial Reporting

Internal Audit

External Audit

Compliance with Existing Rules & Regulations

Other Responsibilities.

36.

CENTRAL BANKS ROLEIN

GOVERNANCE OF BANKS

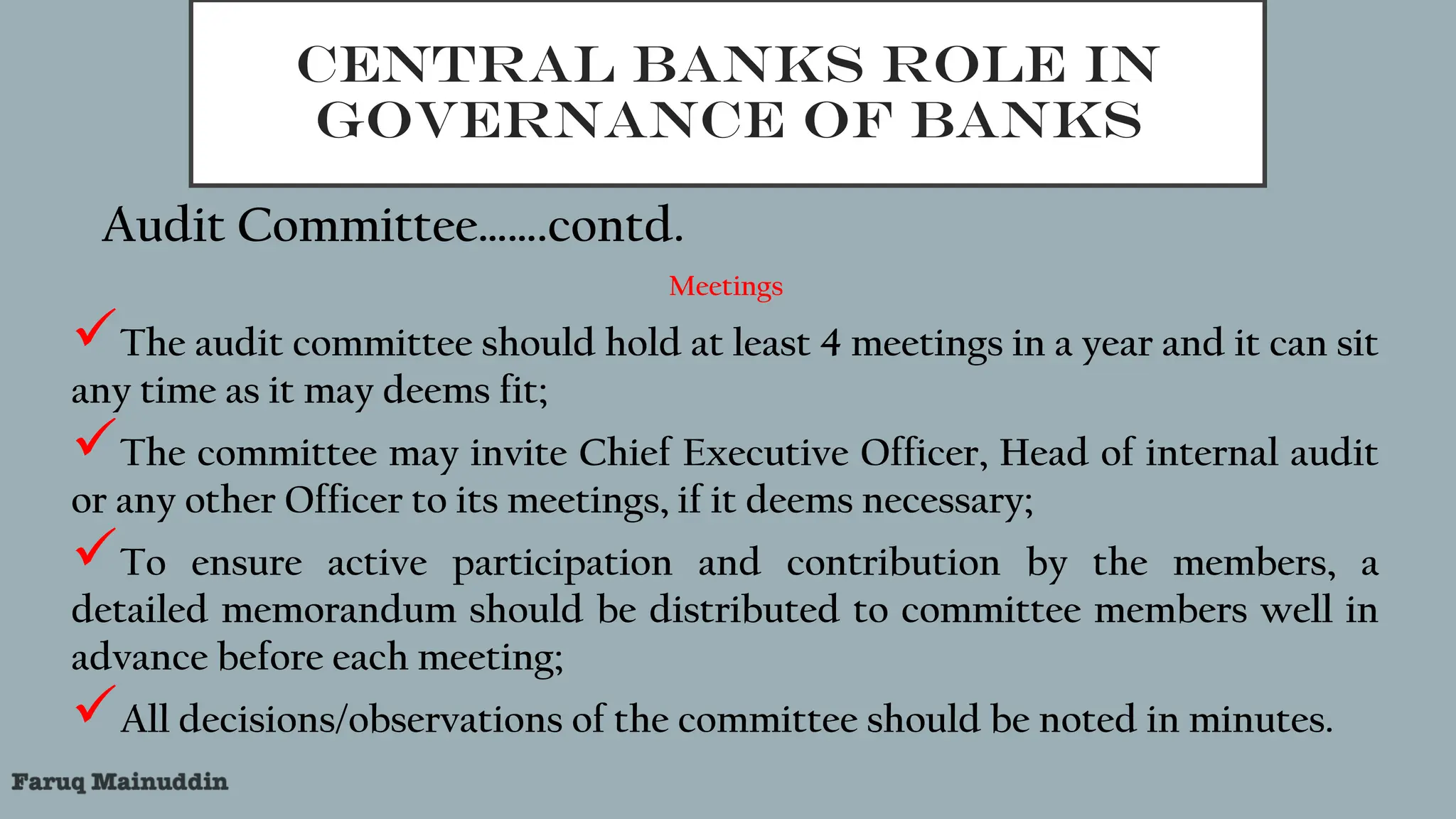

Audit Committee…….contd.

Meetings

The audit committee should hold at least 4 meetings in a year and it can sit

any time as it may deems fit;

The committee may invite Chief Executive Officer, Head of internal audit

or any other Officer to its meetings, if it deems necessary;

To ensure active participation and contribution by the members, a

detailed memorandum should be distributed to committee members well in

advance before each meeting;

All decisions/observations of the committee should be noted in minutes.

37.

CENTRAL BANKS ROLEIN

GOVERNANCE OF BANKS

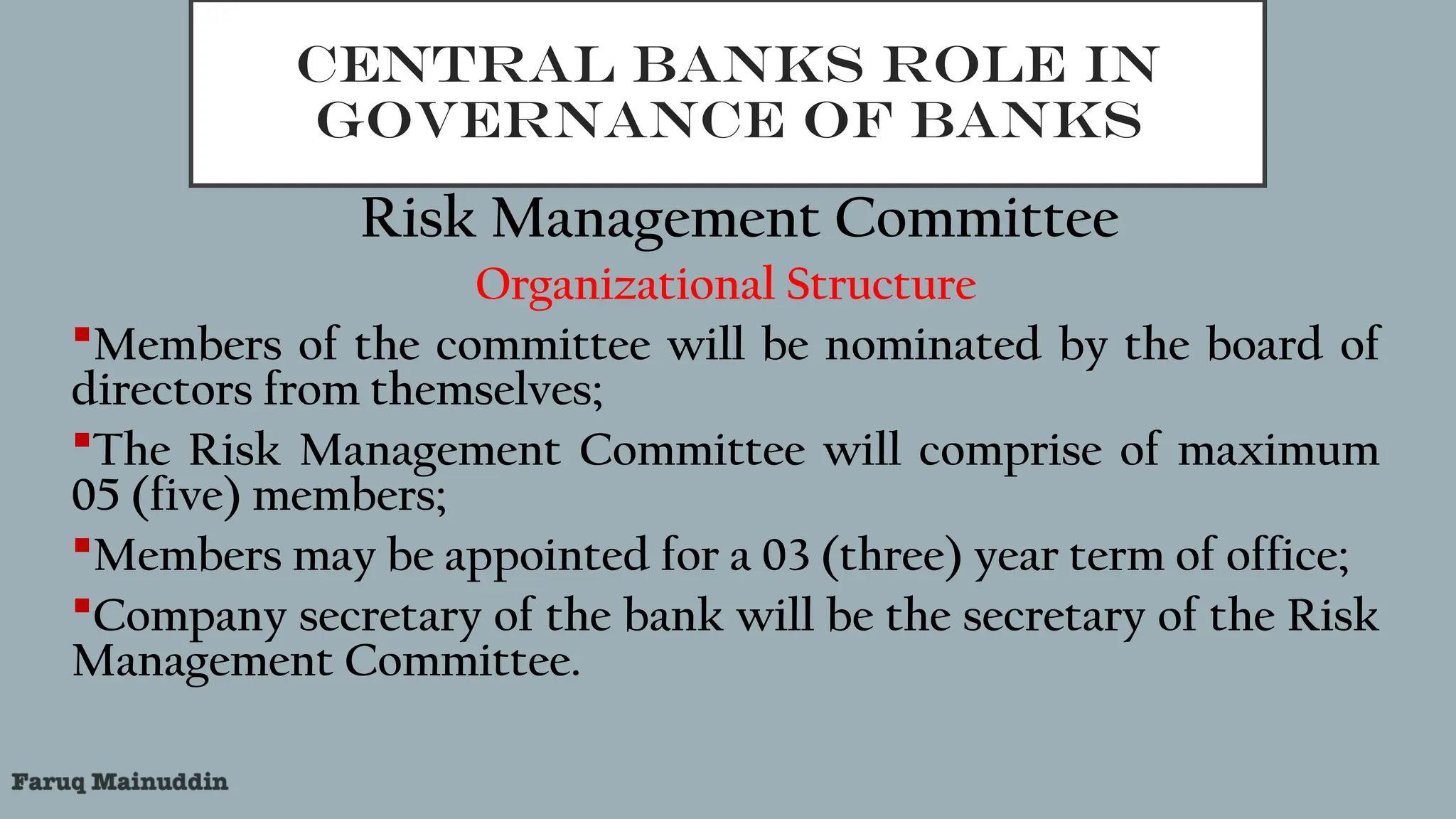

Risk Management Committee

Organizational Structure

Members of the committee will be nominated by the board of

directors from themselves;

The Risk Management Committee will comprise of maximum

05 (five) members;

Members may be appointed for a 03 (three) year term of office;

Company secretary of the bank will be the secretary of the Risk

Management Committee.

38.

CENTRAL BANKS ROLEIN

GOVERNANCE OF BANKS

Risk Management Committee……..contd.

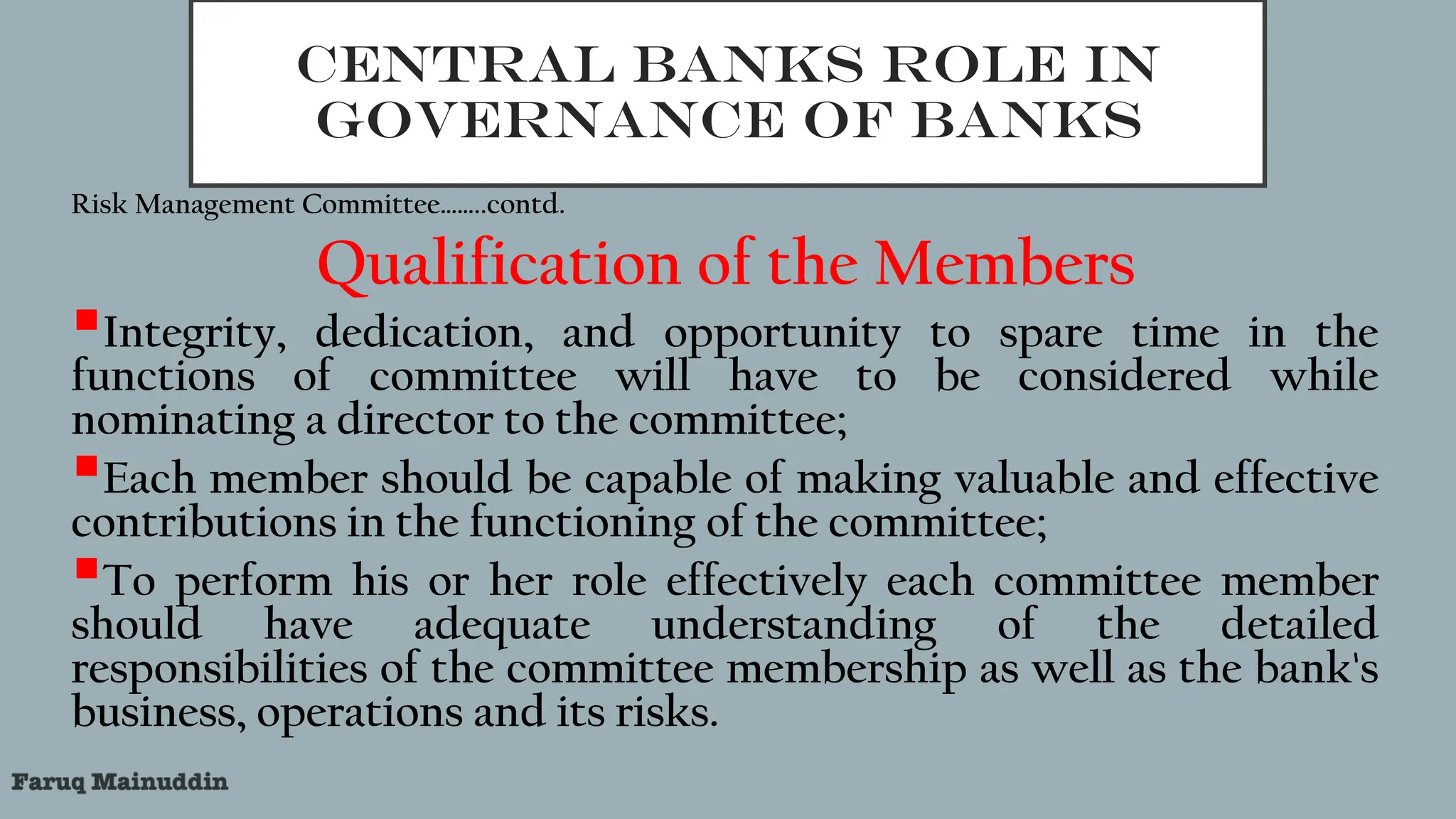

Qualification of the Members

Integrity, dedication, and opportunity to spare time in the

functions of committee will have to be considered while

nominating a director to the committee;

Each member should be capable of making valuable and effective

contributions in the functioning of the committee;

To perform his or her role effectively each committee member

should have adequate understanding of the detailed

responsibilities of the committee membership as well as the bank's

business, operations and its risks.

39.

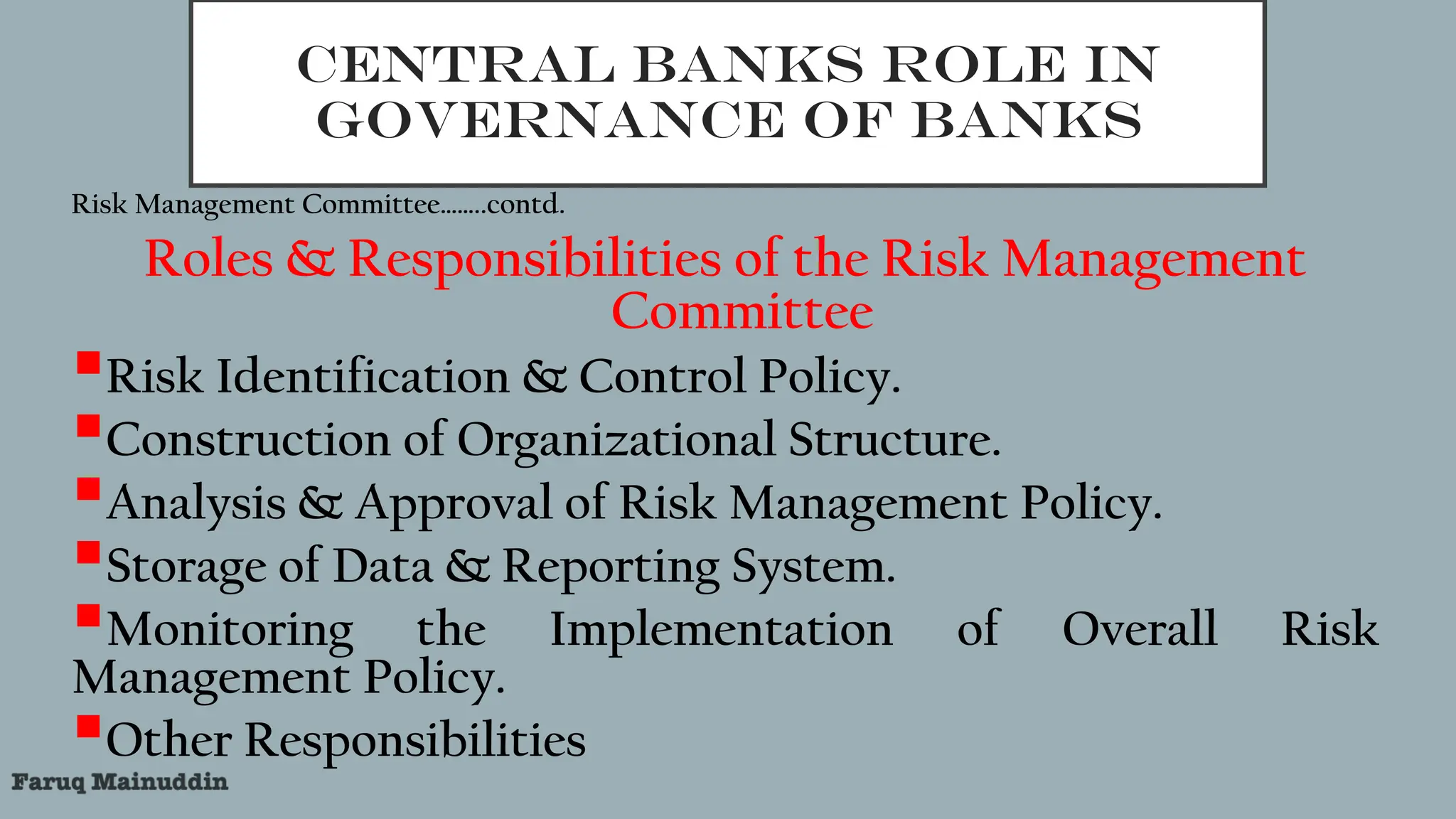

CENTRAL BANKS ROLEIN

GOVERNANCE OF BANKS

Risk Management Committee……..contd.

Roles & Responsibilities of the Risk Management

Committee

Risk Identification & Control Policy.

Construction of Organizational Structure.

Analysis & Approval of Risk Management Policy.

Storage of Data & Reporting System.

Monitoring the Implementation of Overall Risk

Management Policy.

Other Responsibilities

40.

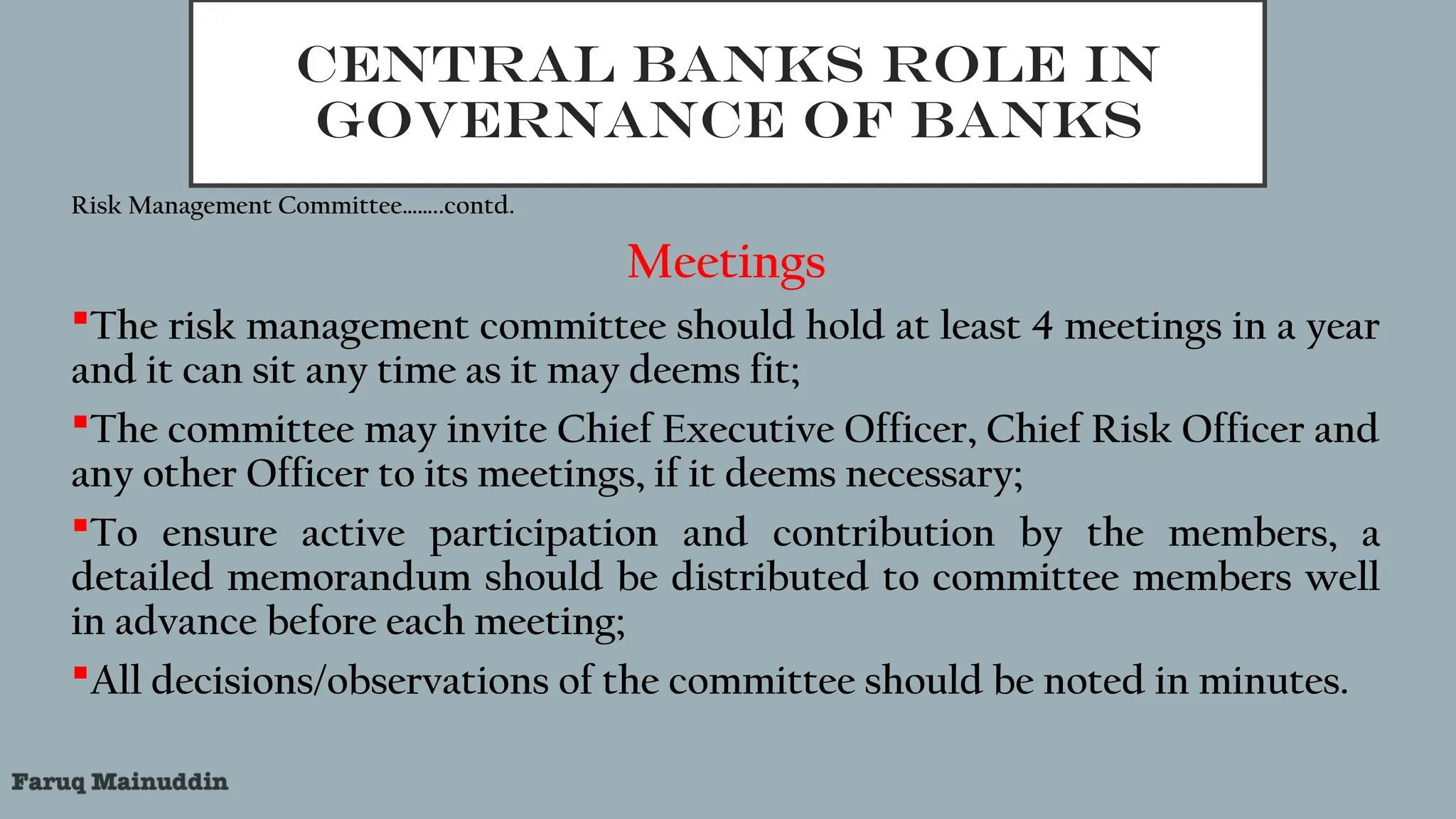

CENTRAL BANKS ROLEIN

GOVERNANCE OF BANKS

Risk Management Committee……..contd.

Meetings

The risk management committee should hold at least 4 meetings in a year

and it can sit any time as it may deems fit;

The committee may invite Chief Executive Officer, Chief Risk Officer and

any other Officer to its meetings, if it deems necessary;

To ensure active participation and contribution by the members, a

detailed memorandum should be distributed to committee members well

in advance before each meeting;

All decisions/observations of the committee should be noted in minutes.

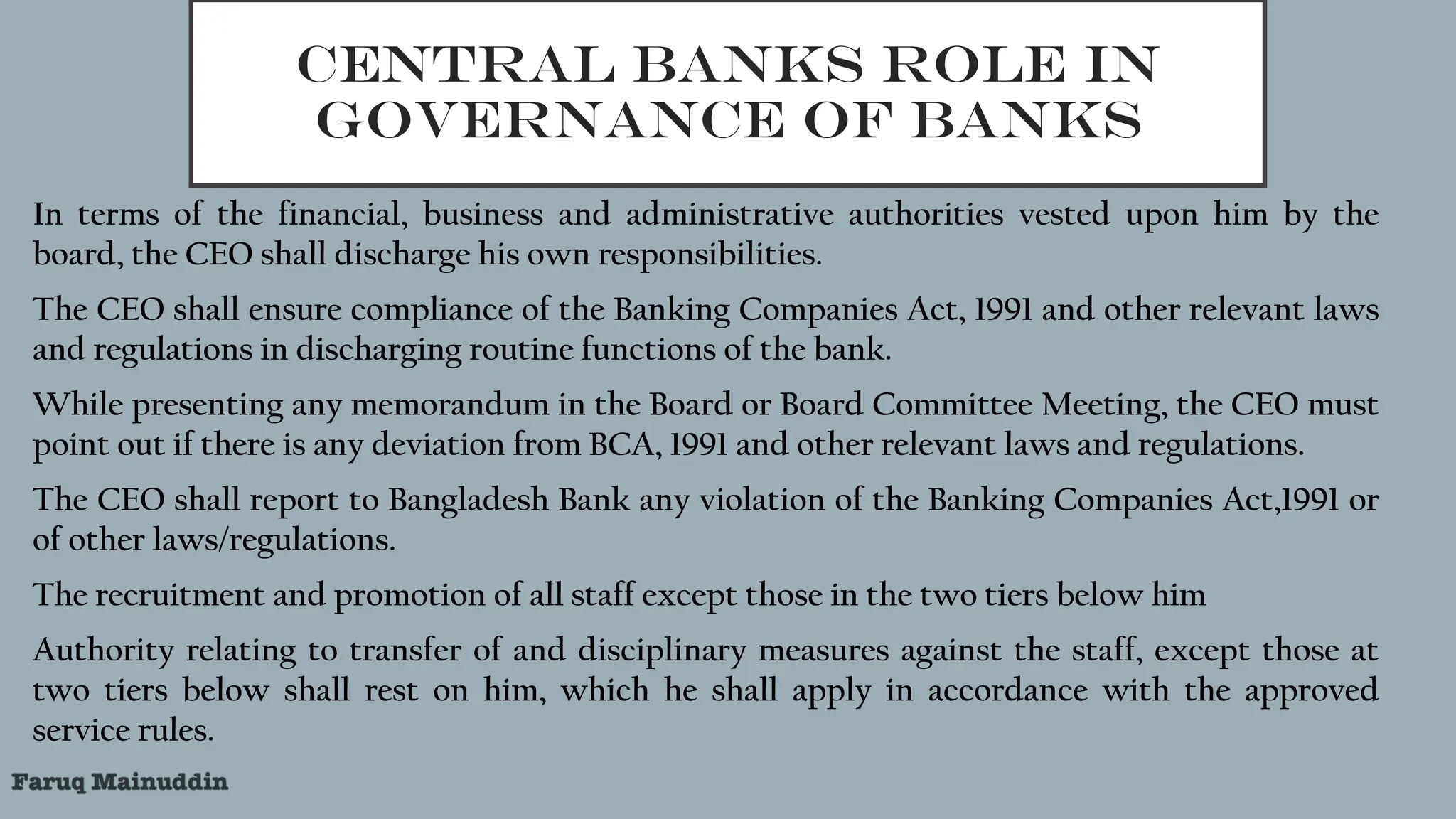

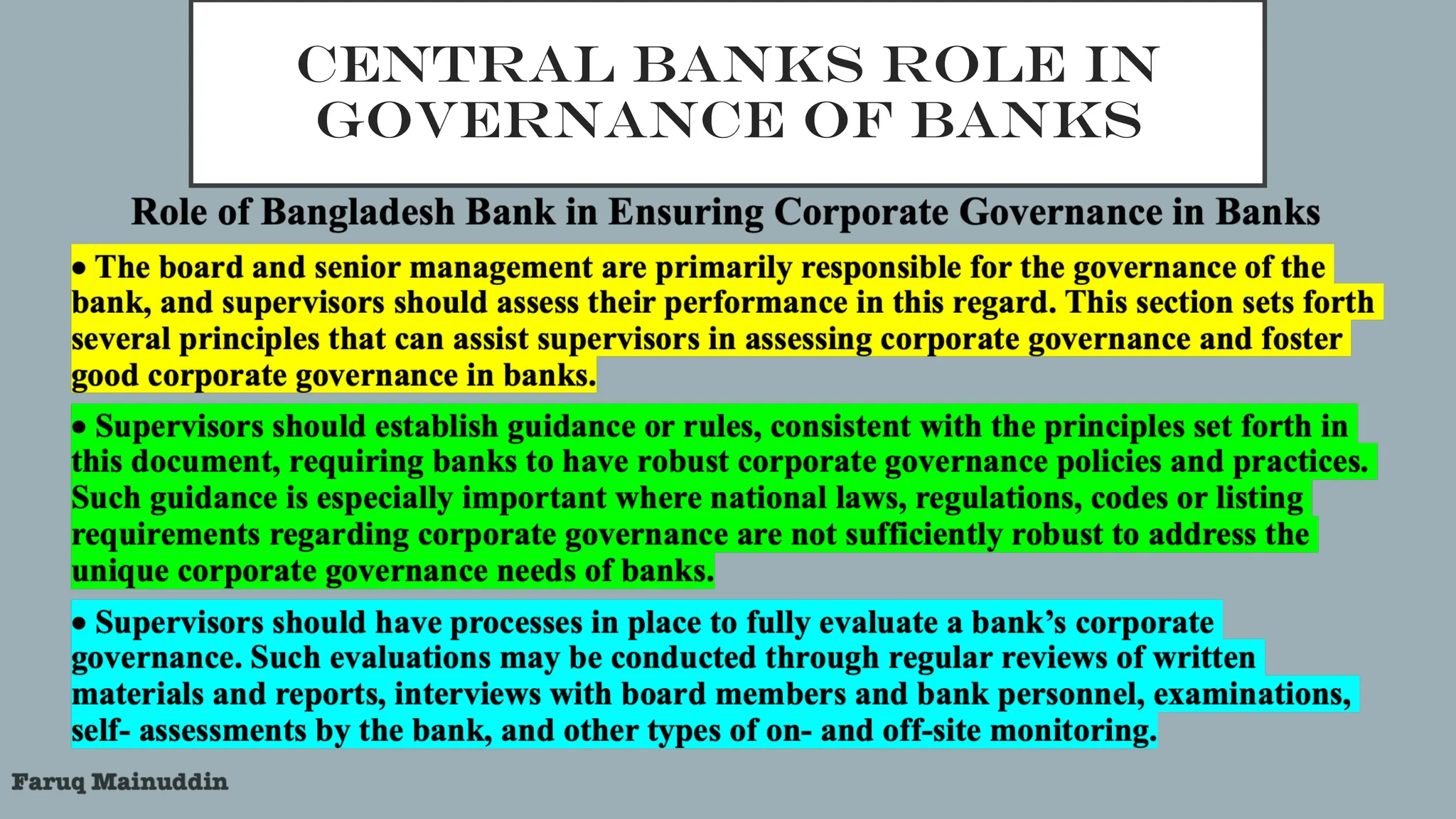

CENTRAL BANKS ROLEIN

GOVERNANCE OF BANKS

In terms of the financial, business and administrative authorities vested upon him by the

board, the CEO shall discharge his own responsibilities.

The CEO shall ensure compliance of the Banking Companies Act, 1991 and other relevant laws

and regulations in discharging routine functions of the bank.

While presenting any memorandum in the Board or Board Committee Meeting, the CEO must

point out if there is any deviation from BCA, 1991 and other relevant laws and regulations.

The CEO shall report to Bangladesh Bank any violation of the Banking Companies Act,1991 or

of other laws/regulations.

The recruitment and promotion of all staff except those in the two tiers below him

Authority relating to transfer of and disciplinary measures against the staff, except those at

two tiers below shall rest on him, which he shall apply in accordance with the approved

service rules.

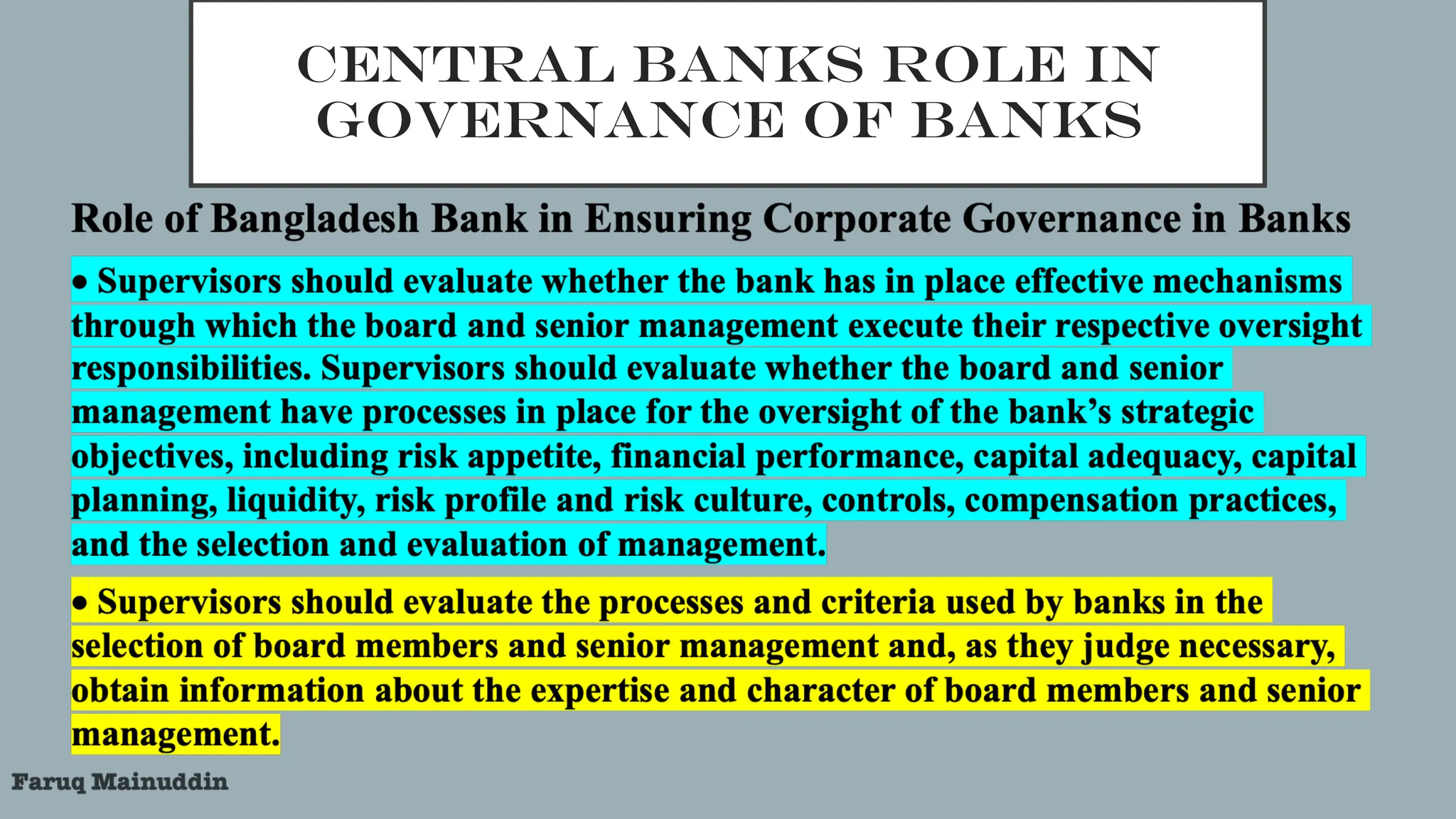

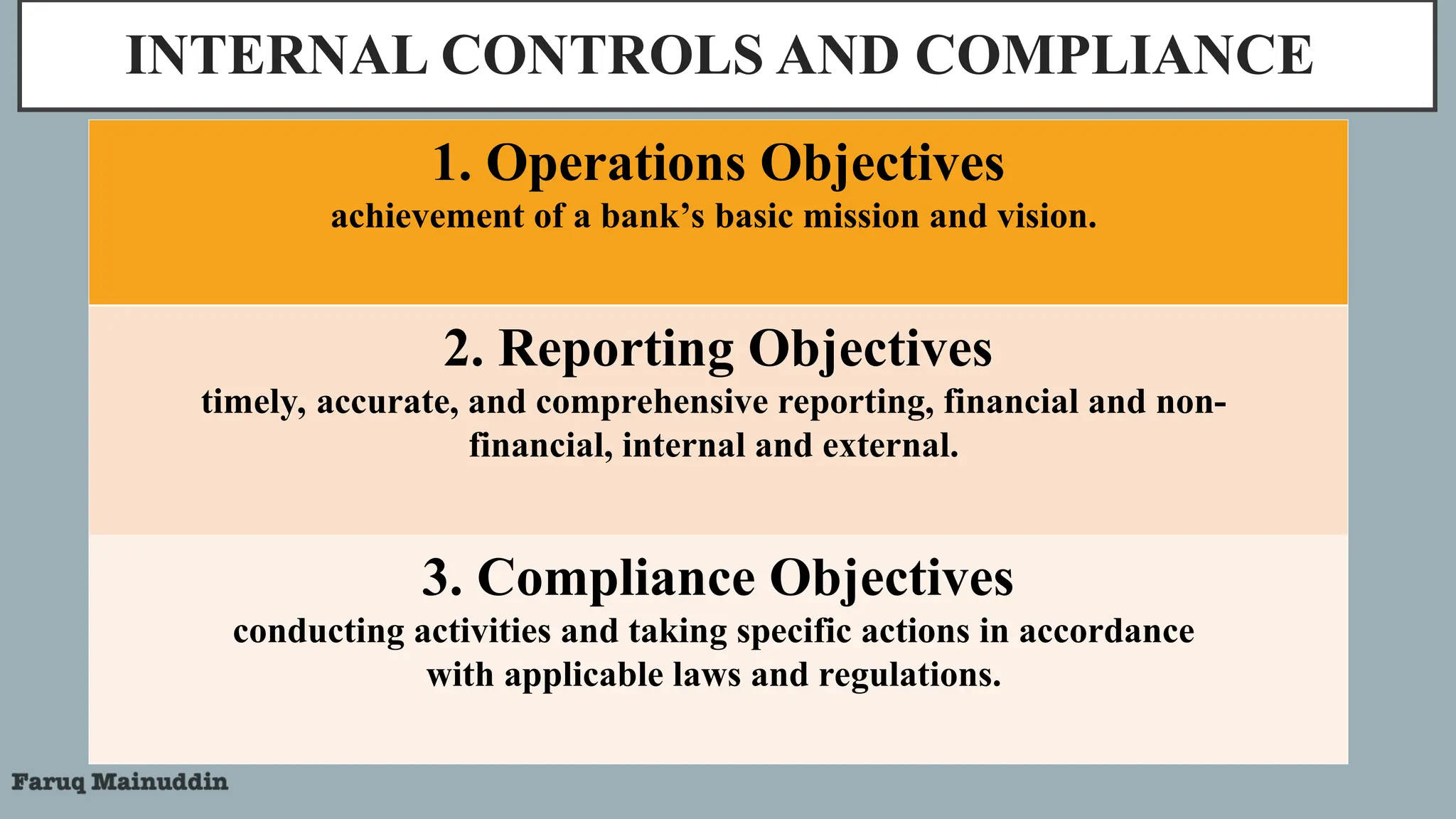

INTERNAL CONTROLS ANDCOMPLIANCE

1. Operations Objectives

achievement of a bank’s basic mission and vision.

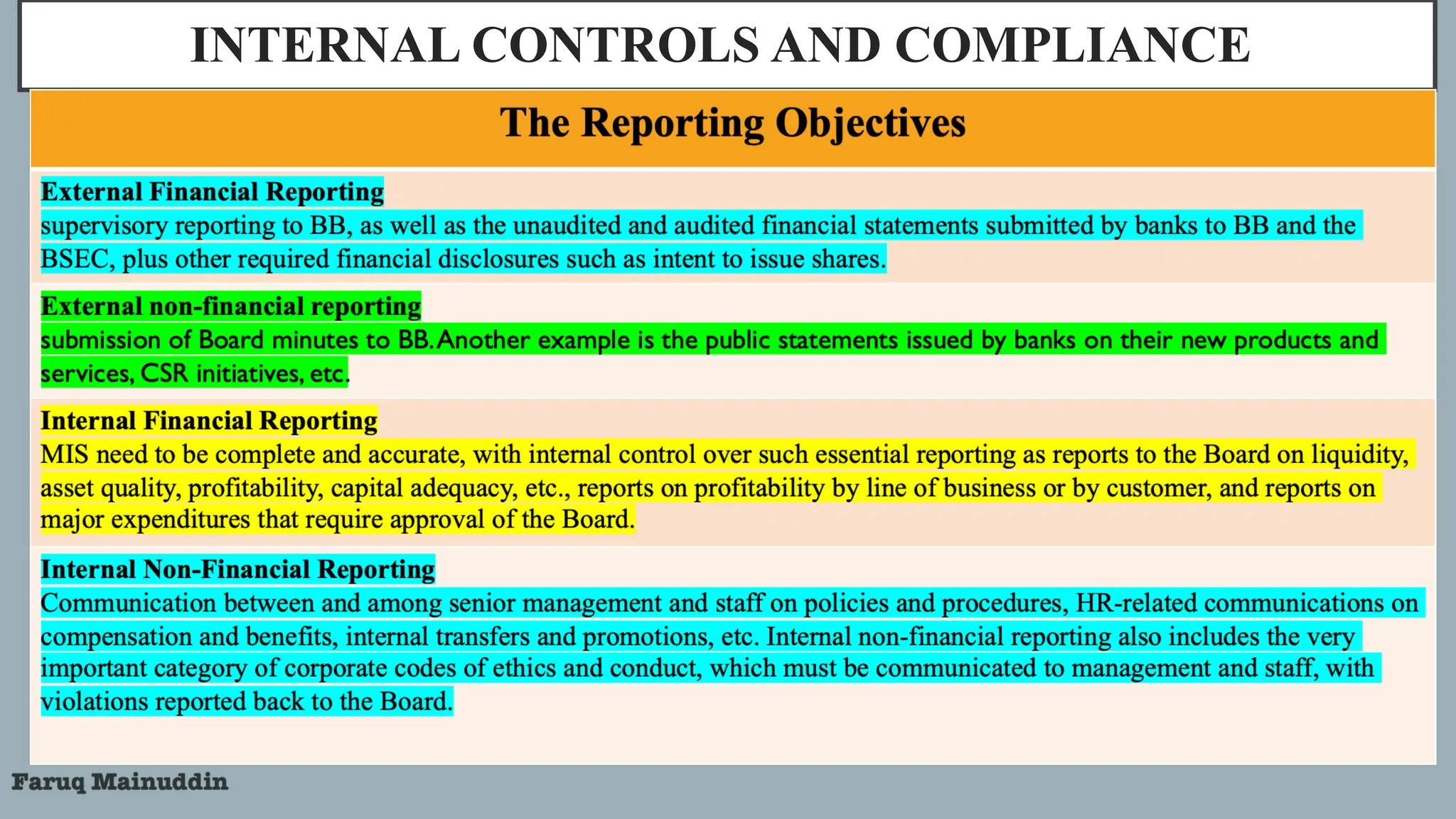

2. Reporting Objectives

timely, accurate, and comprehensive reporting, financial and non-

financial, internal and external.

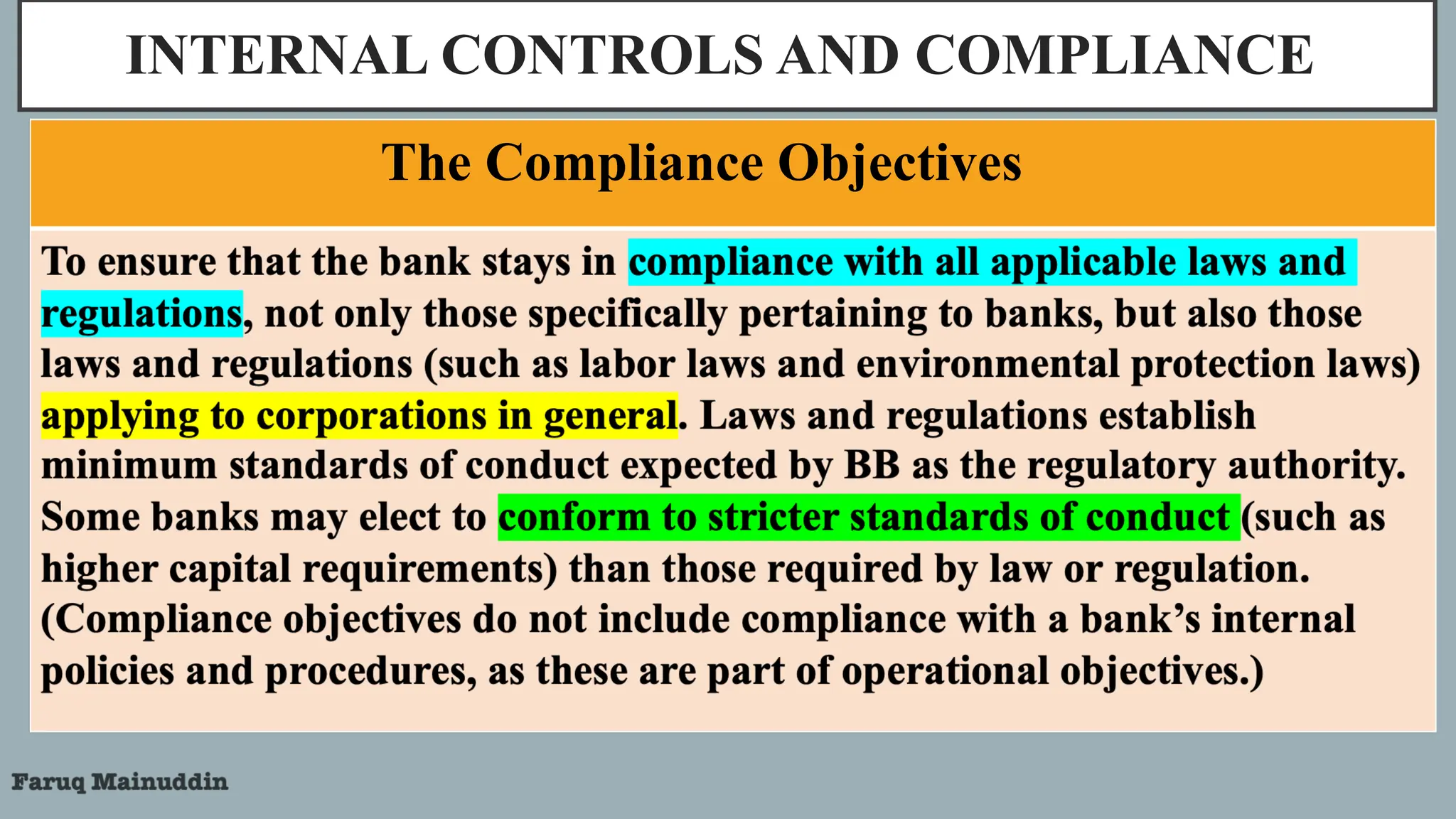

3. Compliance Objectives

conducting activities and taking specific actions in accordance

with applicable laws and regulations.

55.

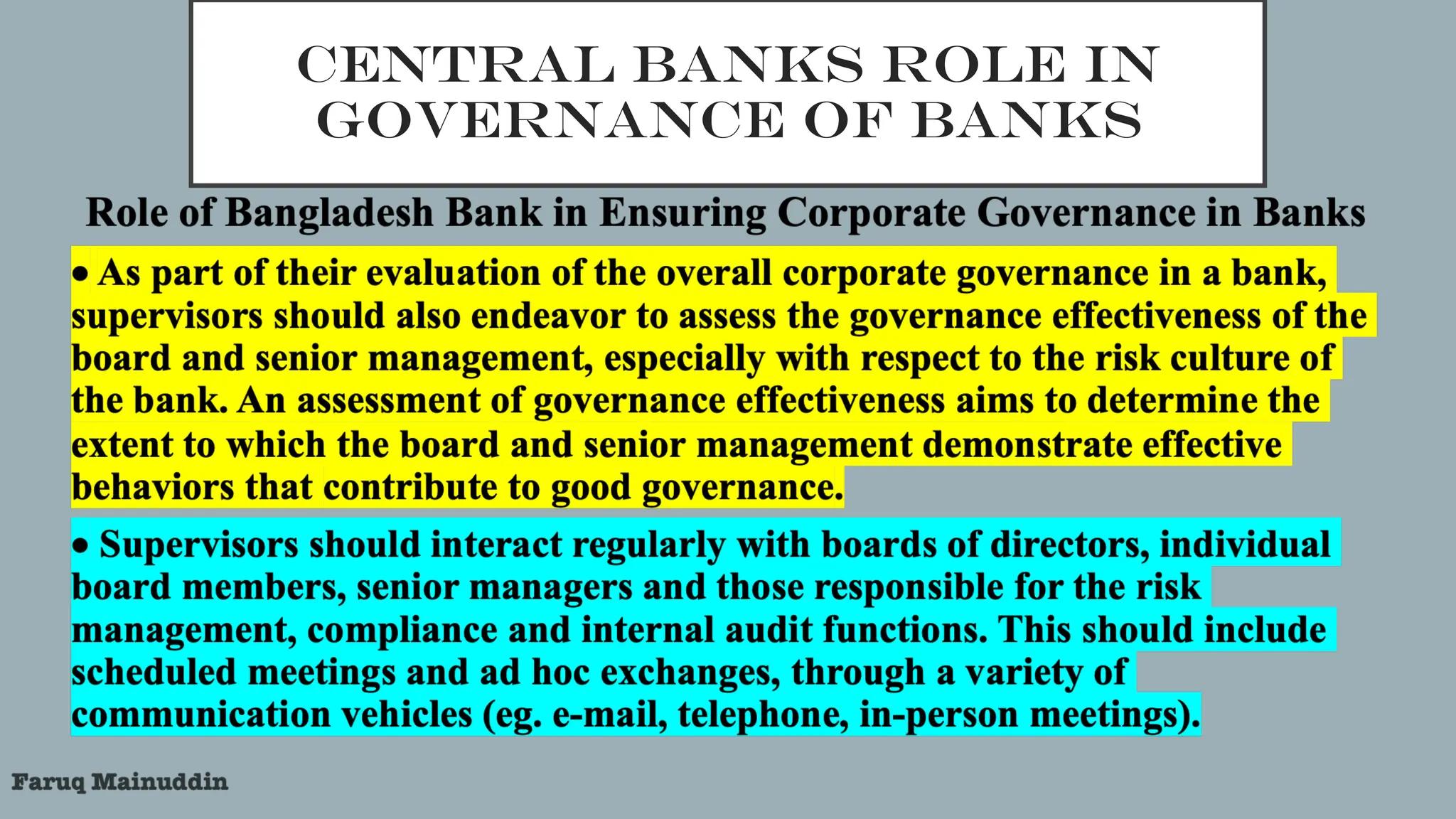

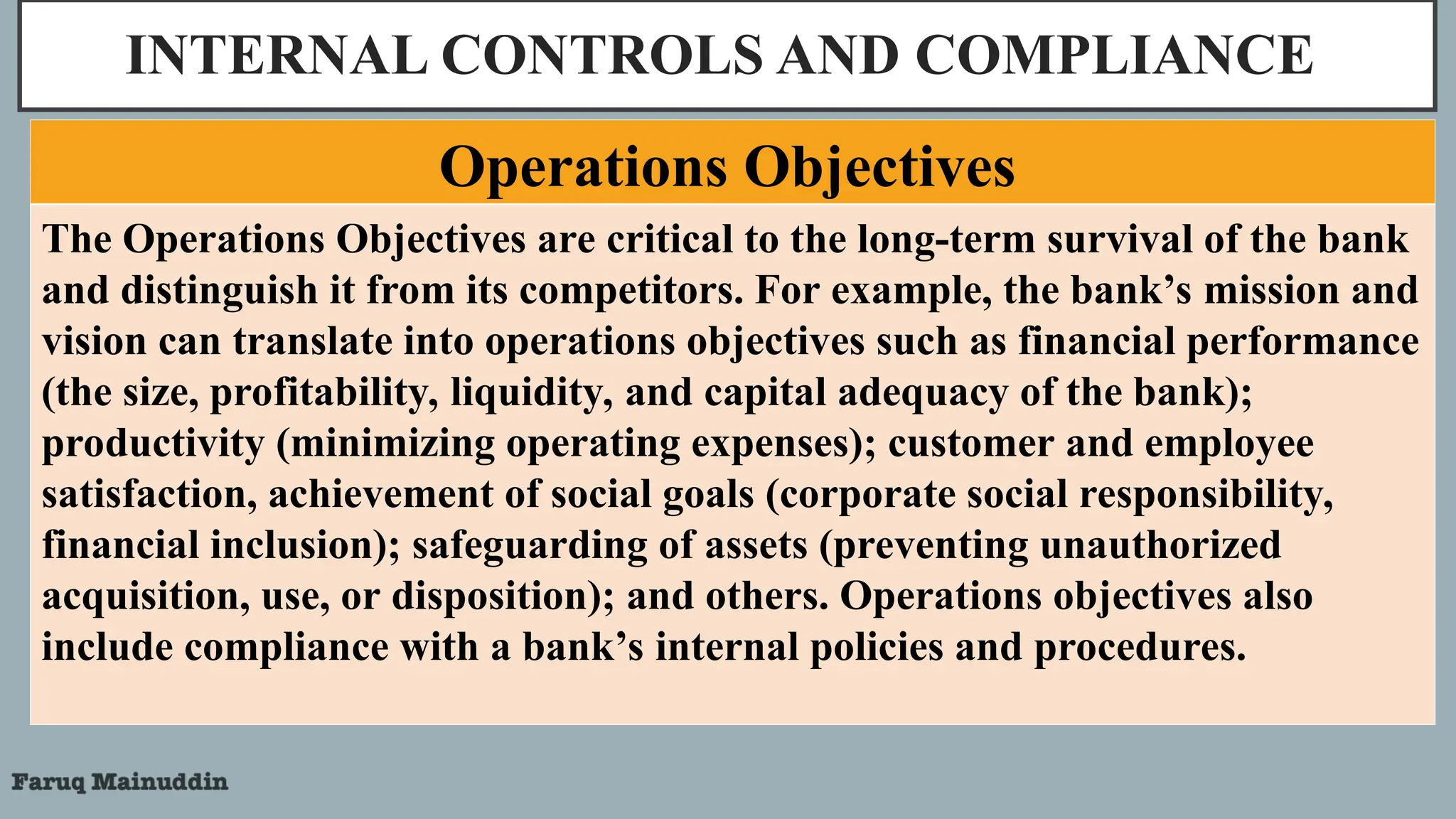

INTERNAL CONTROLS ANDCOMPLIANCE

The Operations Objectives are critical to the long-term survival of the bank

and distinguish it from its competitors. For example, the bank’s mission and

vision can translate into operations objectives such as financial performance

(the size, profitability, liquidity, and capital adequacy of the bank);

productivity (minimizing operating expenses); customer and employee

satisfaction, achievement of social goals (corporate social responsibility,

financial inclusion); safeguarding of assets (preventing unauthorized

acquisition, use, or disposition); and others. Operations objectives also

include compliance with a bank’s internal policies and procedures.

Operations Objectives

INTERNAL CONTROLS ANDCOMPLIANCE

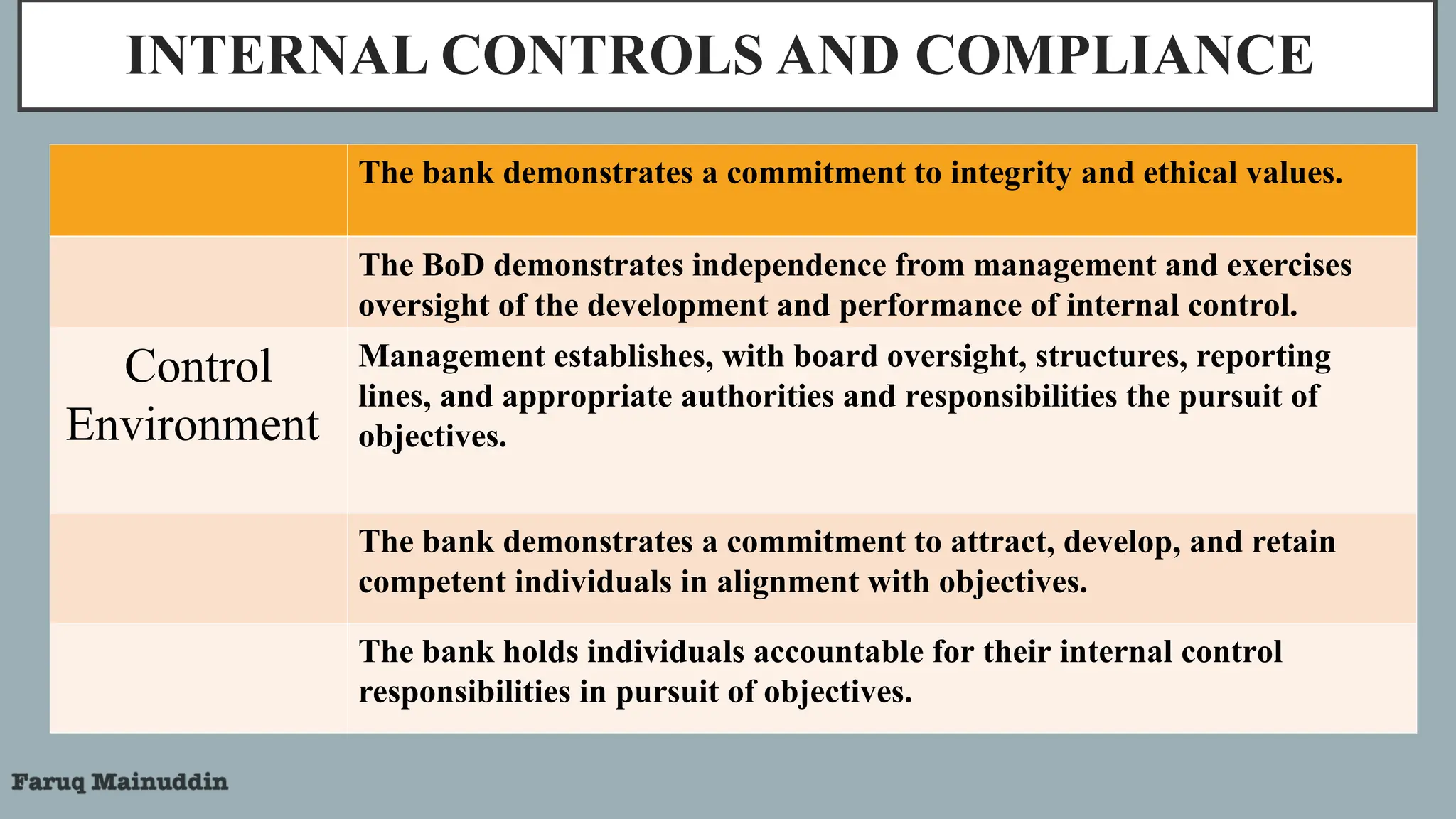

The bank demonstrates a commitment to integrity and ethical values.

The BoD demonstrates independence from management and exercises

oversight of the development and performance of internal control.

Control

Environment

Management establishes, with board oversight, structures, reporting

lines, and appropriate authorities and responsibilities the pursuit of

objectives.

The bank demonstrates a commitment to attract, develop, and retain

competent individuals in alignment with objectives.

The bank holds individuals accountable for their internal control

responsibilities in pursuit of objectives.

59.

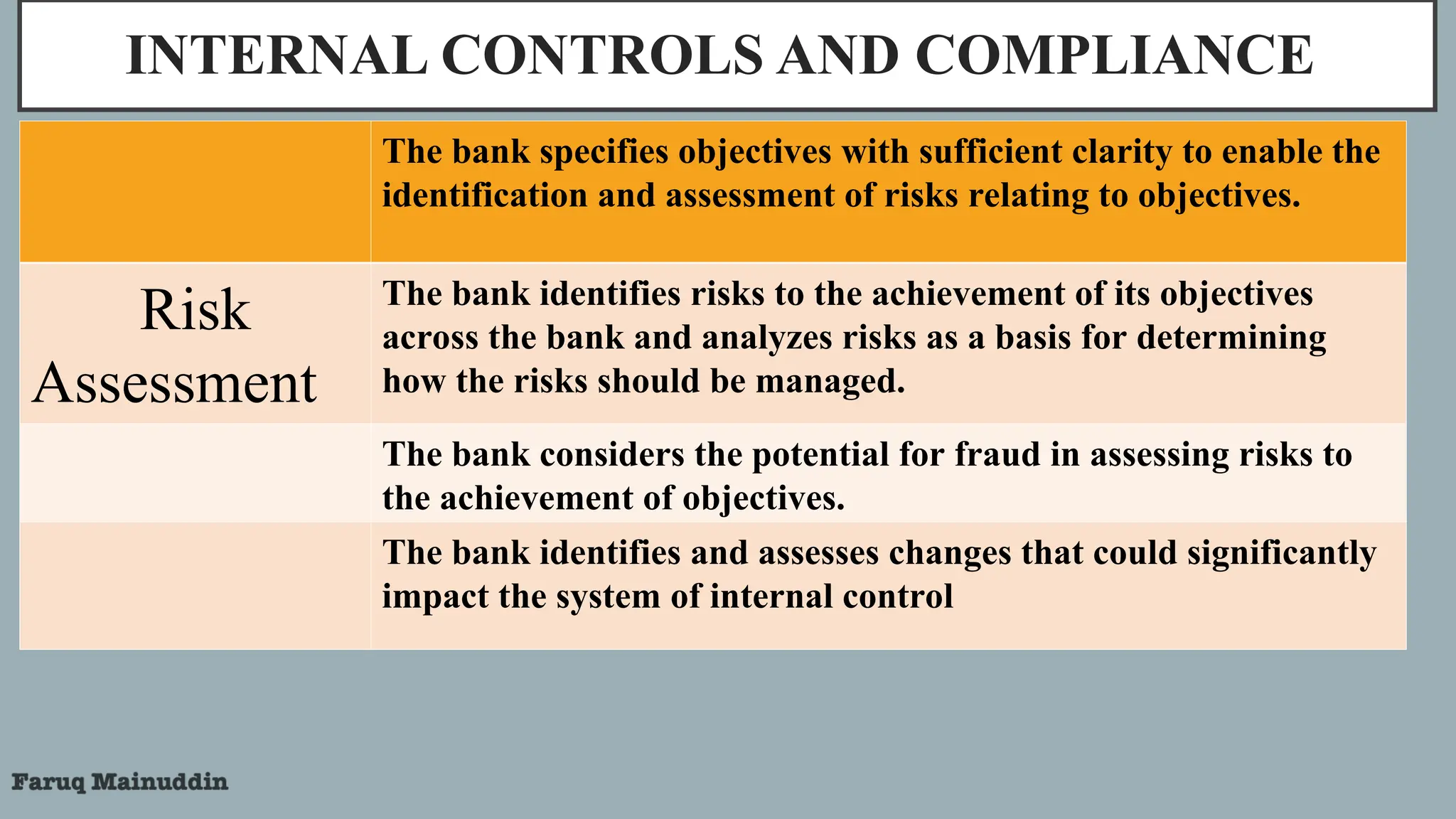

INTERNAL CONTROLS ANDCOMPLIANCE

The bank specifies objectives with sufficient clarity to enable the

identification and assessment of risks relating to objectives.

Risk

Assessment

The bank identifies risks to the achievement of its objectives

across the bank and analyzes risks as a basis for determining

how the risks should be managed.

The bank considers the potential for fraud in assessing risks to

the achievement of objectives.

The bank identifies and assesses changes that could significantly

impact the system of internal control

60.

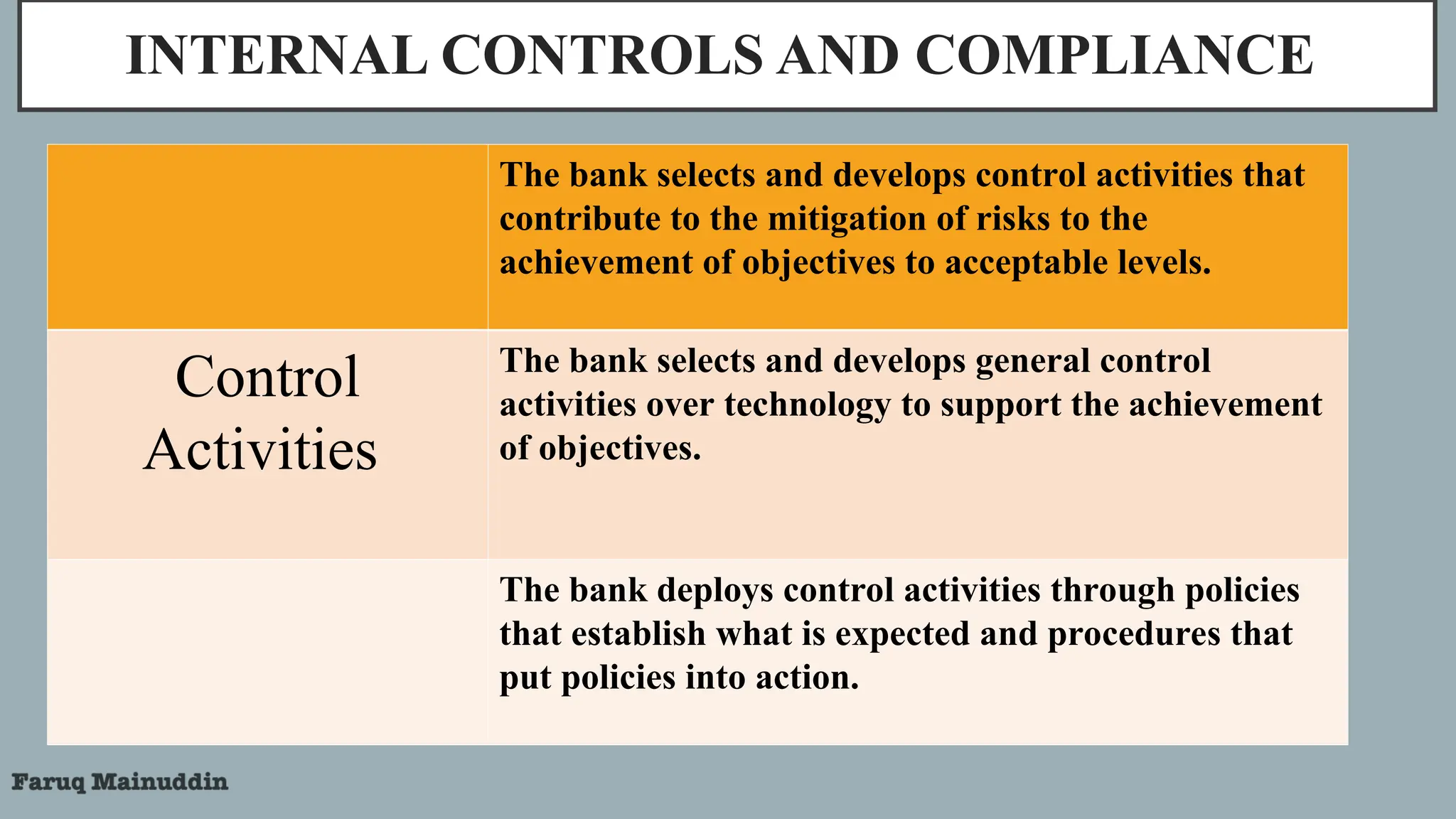

INTERNAL CONTROLS ANDCOMPLIANCE

The bank selects and develops control activities that

contribute to the mitigation of risks to the

achievement of objectives to acceptable levels.

Control

Activities

The bank selects and develops general control

activities over technology to support the achievement

of objectives.

The bank deploys control activities through policies

that establish what is expected and procedures that

put policies into action.

61.

INTERNAL CONTROLS ANDCOMPLIANCE

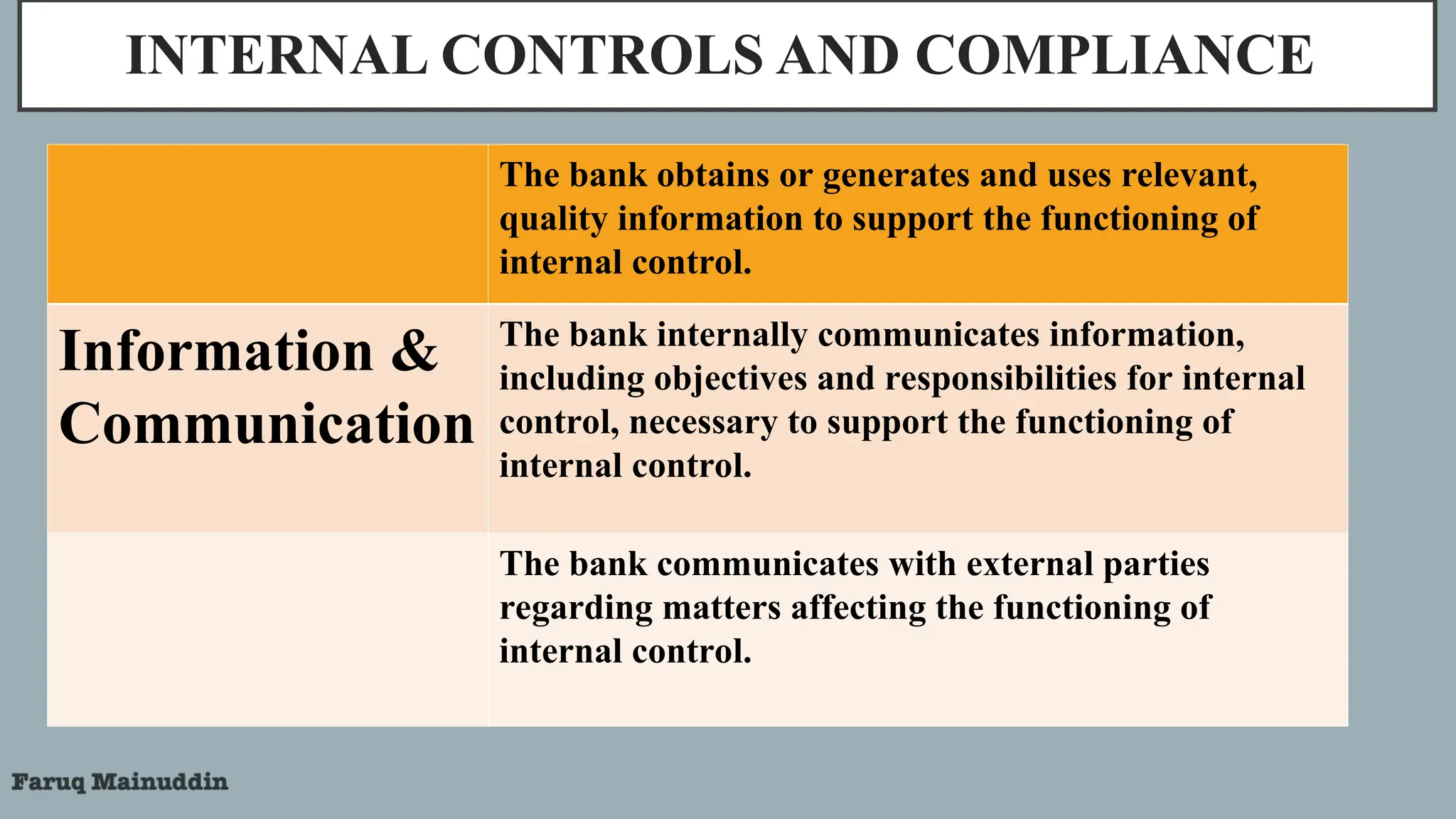

The bank obtains or generates and uses relevant,

quality information to support the functioning of

internal control.

Information &

Communication

The bank internally communicates information,

including objectives and responsibilities for internal

control, necessary to support the functioning of

internal control.

The bank communicates with external parties

regarding matters affecting the functioning of

internal control.

62.

INTERNAL CONTROLS ANDCOMPLIANCE

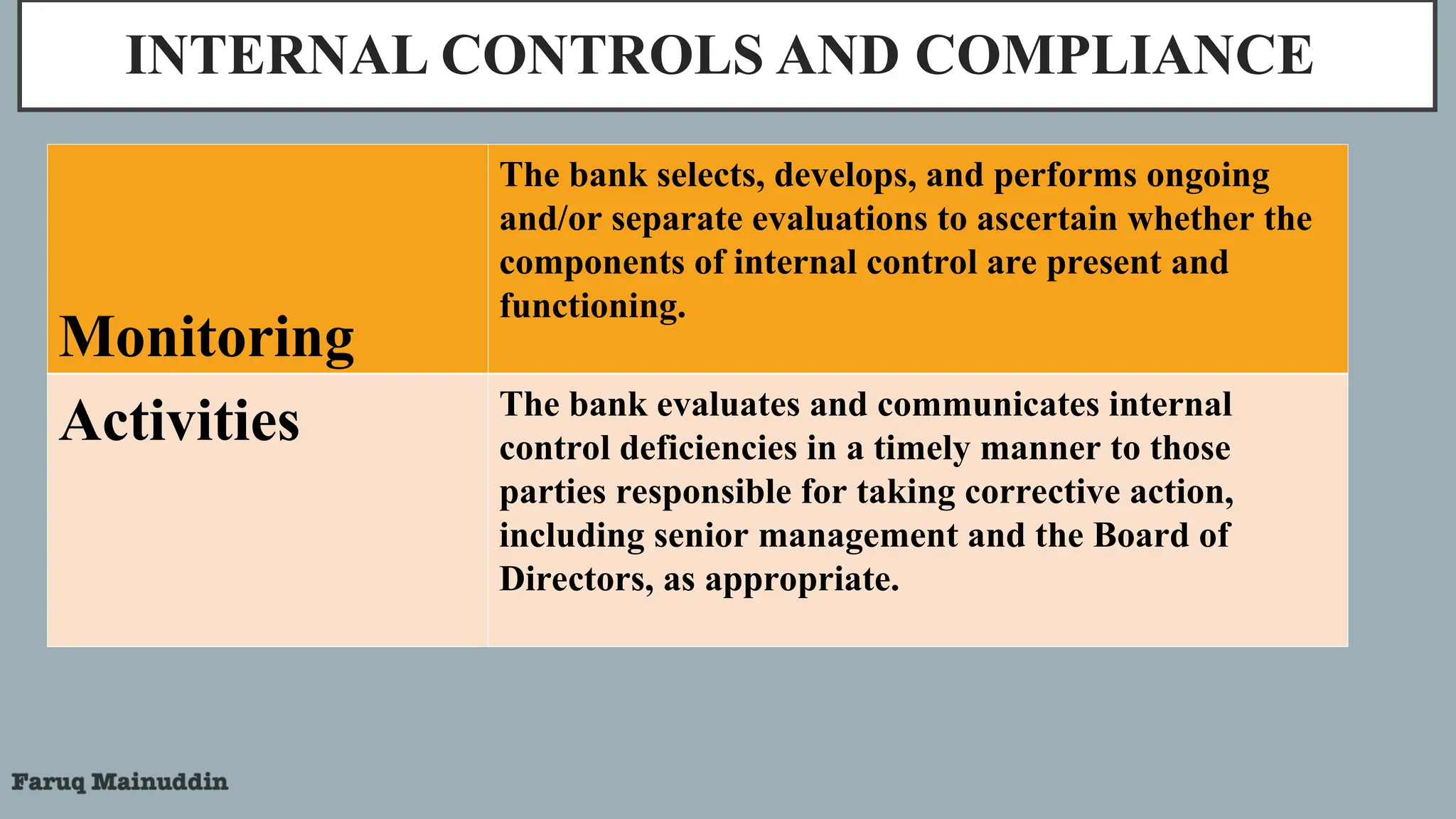

Monitoring

The bank selects, develops, and performs ongoing

and/or separate evaluations to ascertain whether the

components of internal control are present and

functioning.

Activities The bank evaluates and communicates internal

control deficiencies in a timely manner to those

parties responsible for taking corrective action,

including senior management and the Board of

Directors, as appropriate.

63.

INTERNAL CONTROLS ANDCOMPLIANCE

Financial Reporting

• Audit committee will check whether the financial statements

reflect the complete and concrete information and determine

whether the statements are prepared according to existing rules &

regulations and standards enforced in the country and as per

relevant prescribed accounting standards set by Bangladesh Bank;

• Discuss with management and the external auditors to review the

financial statements before its finalization.

64.

INTERNAL CONTROLS ANDCOMPLIANCE

Internal Audit

• Audit committee will monitor whether internal audit working independently

from the management.

• Review the activities of the internal audit and the organizational structure and

ensure that no unjustified restriction or limitation hinders the internal audit

process;

• Examine the efficiency and effectiveness of internal audit function;

• Examine whether the findings and recommendations made by the internal

auditors are duly considered by the management or not.

65.

INTERNAL CONTROLS ANDCOMPLIANCE

External Audit

• Review the performance of the external auditors and their audit reports

• Examine whether the findings and recommendations made by the

external auditors are duly considered by the management or not.

• Make recommendations to the board regarding the appointment of the

external auditors.

66.

INTERNAL CONTROLS ANDCOMPLIANCE

Compliance with Existing Rules & Regulations

• Review whether the laws and regulations framed by the regulatory

authorities (central bank and other bodies) and internal regulations

approved by the board are being complied with.

67.

INTERNAL CONTROLS ANDCOMPLIANCE

Other Responsibilities

• Submit compliance report to the board on quarterly basis on regularization of

the omission, fraud and forgeries and other irregularities detected by the internal

and external auditors and inspectors of regulatory authorities;

• External and internal auditors will submit their related assessment report, if the

committee solicit;

• Perform other oversight functions as desired by the Board of Directors and

evaluate the committee's own performance on a regular basis.

68.

INTERNAL CONTROLS ANDCOMPLIANCE

Management Information System (MIS)

• An effective internal control system requires that there is an efficient reporting system of information

that is relevant to decision making. The information should be reliable, timely accessible and provided

in a consistent format.

• Information would have to include external market information about events and conditions that are

relevant to decision making. Internal information should include financial, operational and compliance

data.

• There should be appropriate committees within the organization which would evaluate data received

through various information systems. This will ensure supply of correct and accurate information to

the management.

• Internal information must cover all significant activities of the bank. Electronic data must be secured,

monitored independently and supported by contingency arrangements.

• Most importantly the channels of communication must ensure that all staff fully understand and

adhere to policies and procedures affecting their duties and responsibilities and that other relevant

information are reaching the appropriate personnel.