Downloaded 288 times

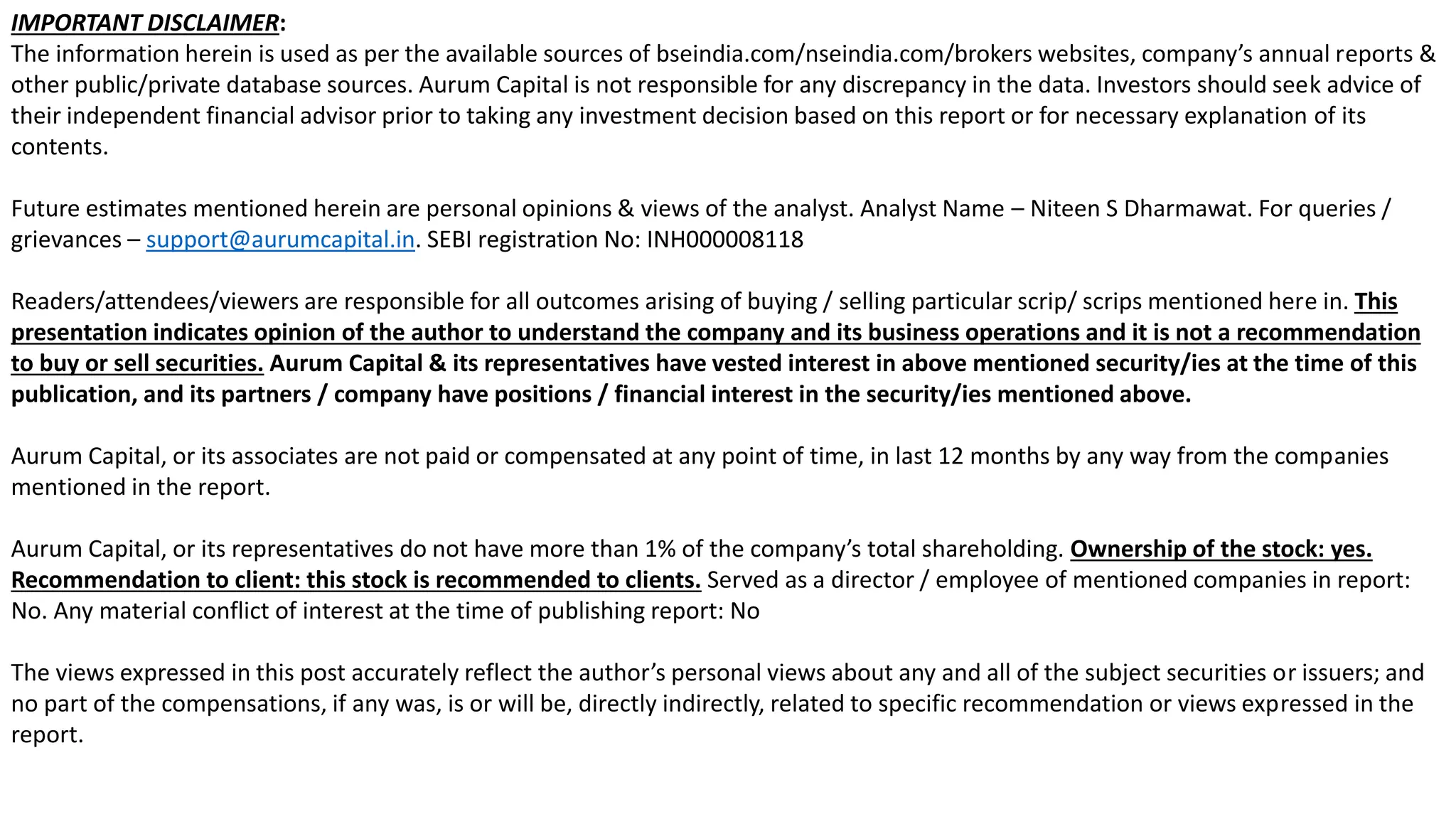

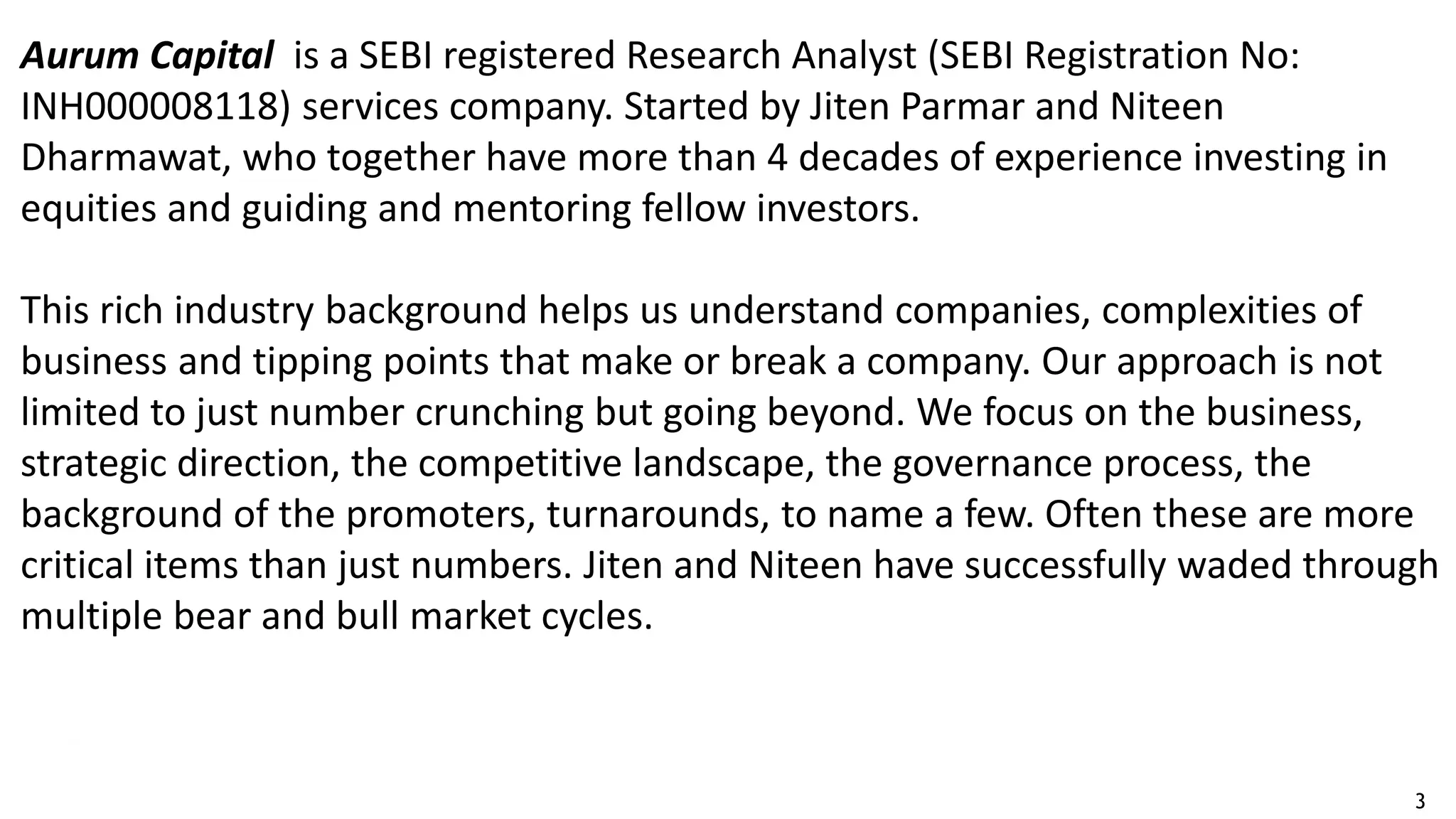

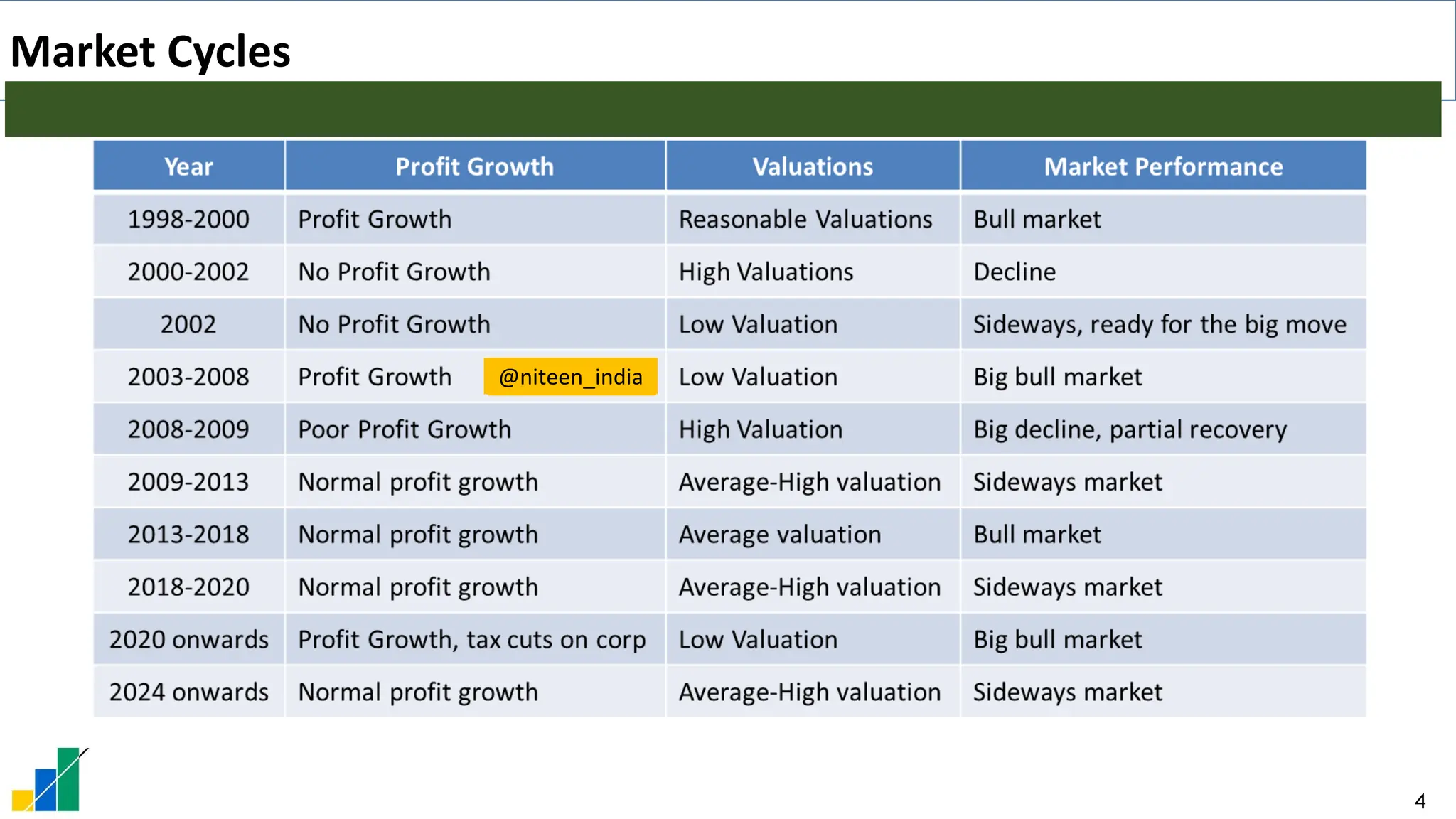

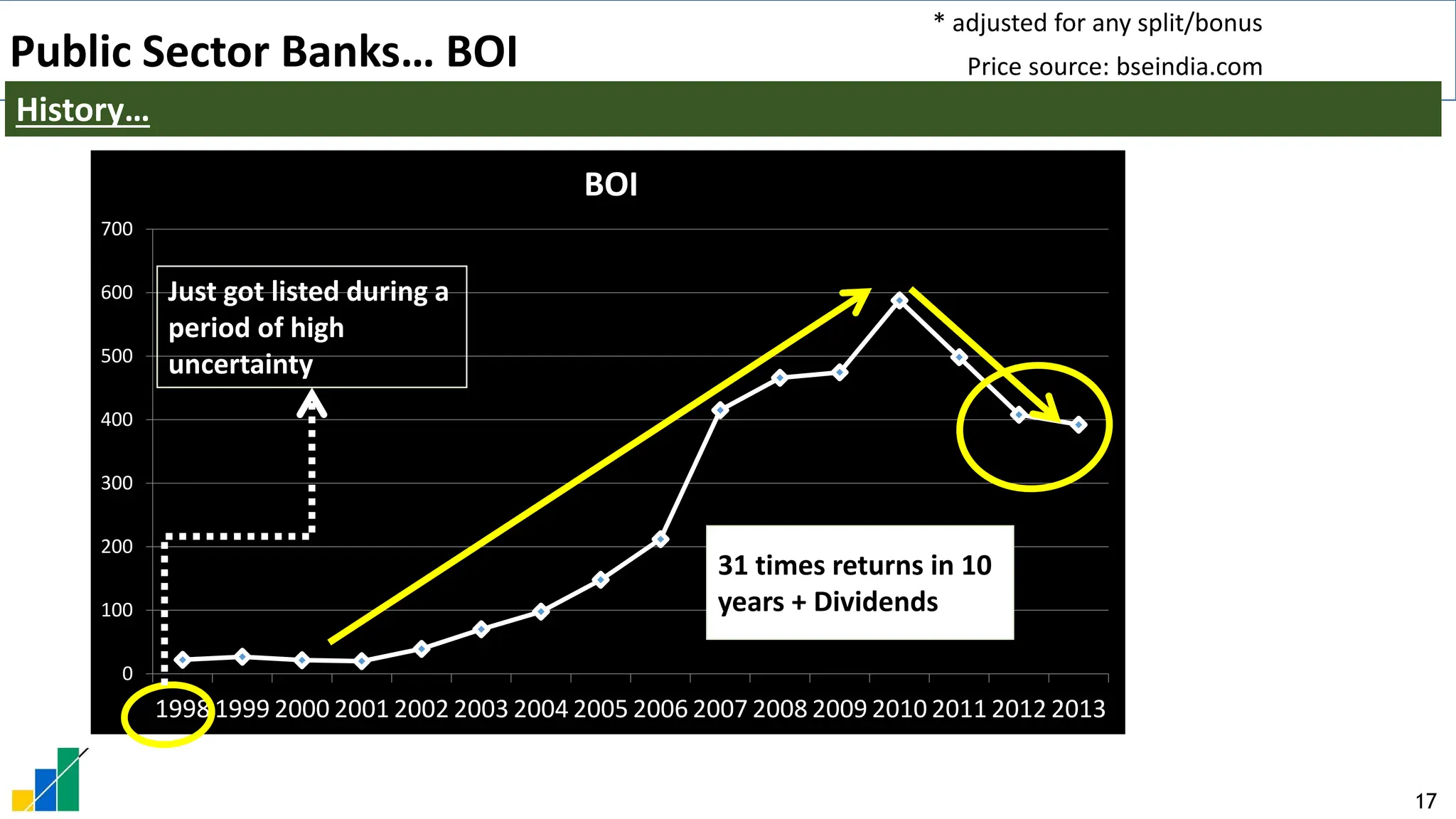

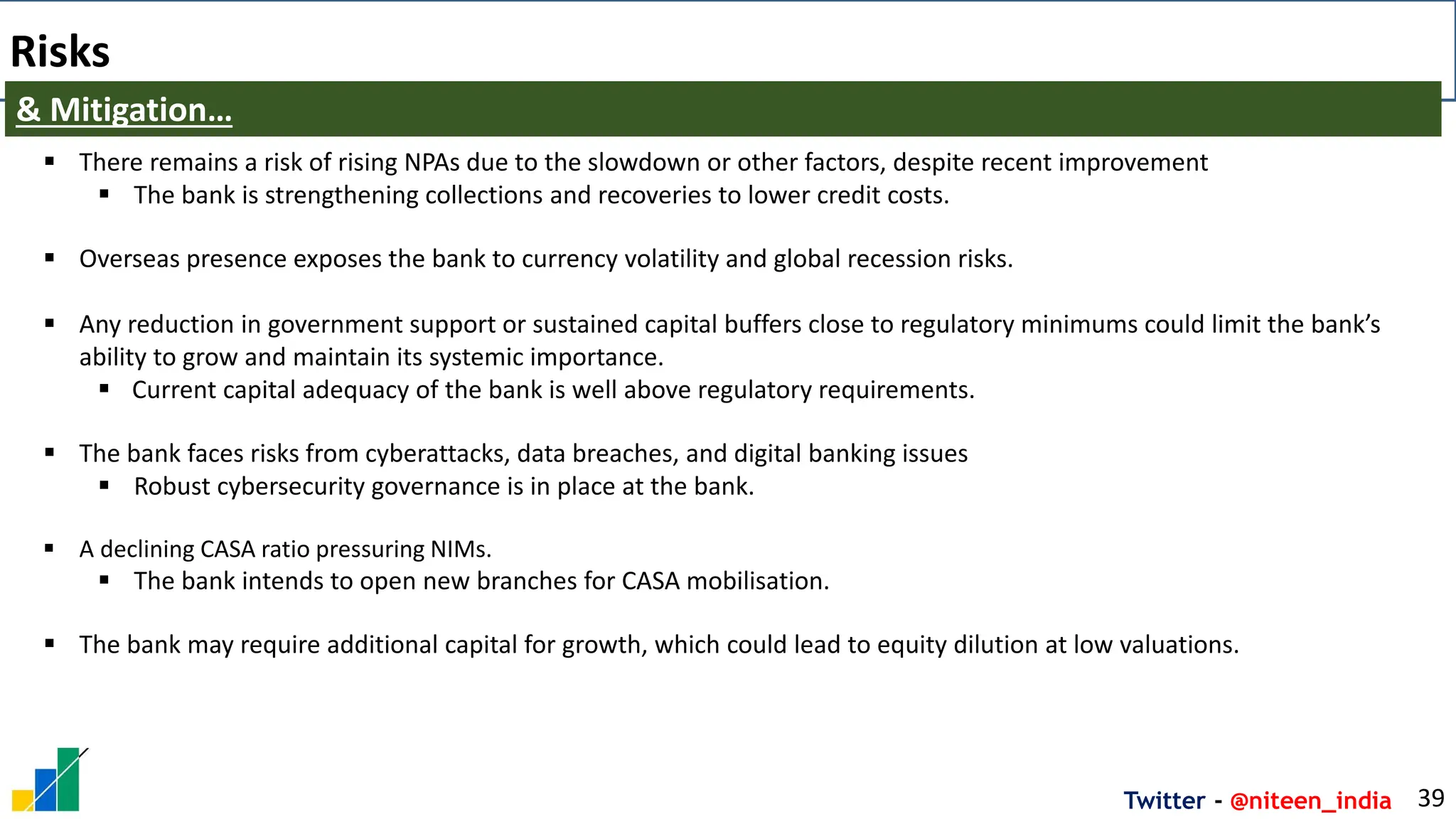

Niteen S Dharmawat, Co Founder, Aurum Capital, presented the business analysis of Bank of India Ltd in the Investing Accelerator Summit in Goa on 30 Aug 2025. Please go through the Disclosure. This is not a buy/sell/hold recommendation. It is the business analysis of the company.

![Where to Buy LinkedIn Accounts_ [12 Best Sites] (3).pdf](https://cdn.slidesharecdn.com/ss_thumbnails/wheretobuylinkedinaccounts12bestsites3-251124162550-95b6ddfa-thumbnail.jpg?width=640&height=640&fit=bounds)