Quantifying Peace andits Benefits

The Institute for Economics & Peace (IEP) is an independent, non-partisan, non-profit think tank dedicated

to shifting the world’s focus to peace as a positive, achievable, and tangible measure of human well-being

and progress. IEP achieves its goals by developing new conceptual frameworks to define peacefulness;

providing metrics for measuring peace; and uncovering the relationships between business, peace and

prosperity as well as promoting a better understanding of the cultural, economic and political factors that

create peace.

IEP is headquartered in Sydney, with offices in New York, Brussels, The Hague, Mexico City and Nairobi.

It works with a wide range of partners internationally and collaborates with intergovernmental organisations

on measuring and communicating the economic value of peace.

For more information visit www.economicsandpeace.org

Please cite this report as:

Institute for Economics & Peace. Global Peace Index 2025: Identifying and Measuring the Factors that

Drive Peace, Sydney, June 2025. Available from: http://visionofhumanity.org/resources (accessed Date

Month Year).

3.

Contents

Results

Trends

Economic Impact

of Violence

WhyConflicts

Escalate

Positive Peace, Conflict and

Information Flows

Appendices

7

29

43

61

91

99

1 2025 Global Peace Index Rankings 8

Results 10

Regional Overview 13

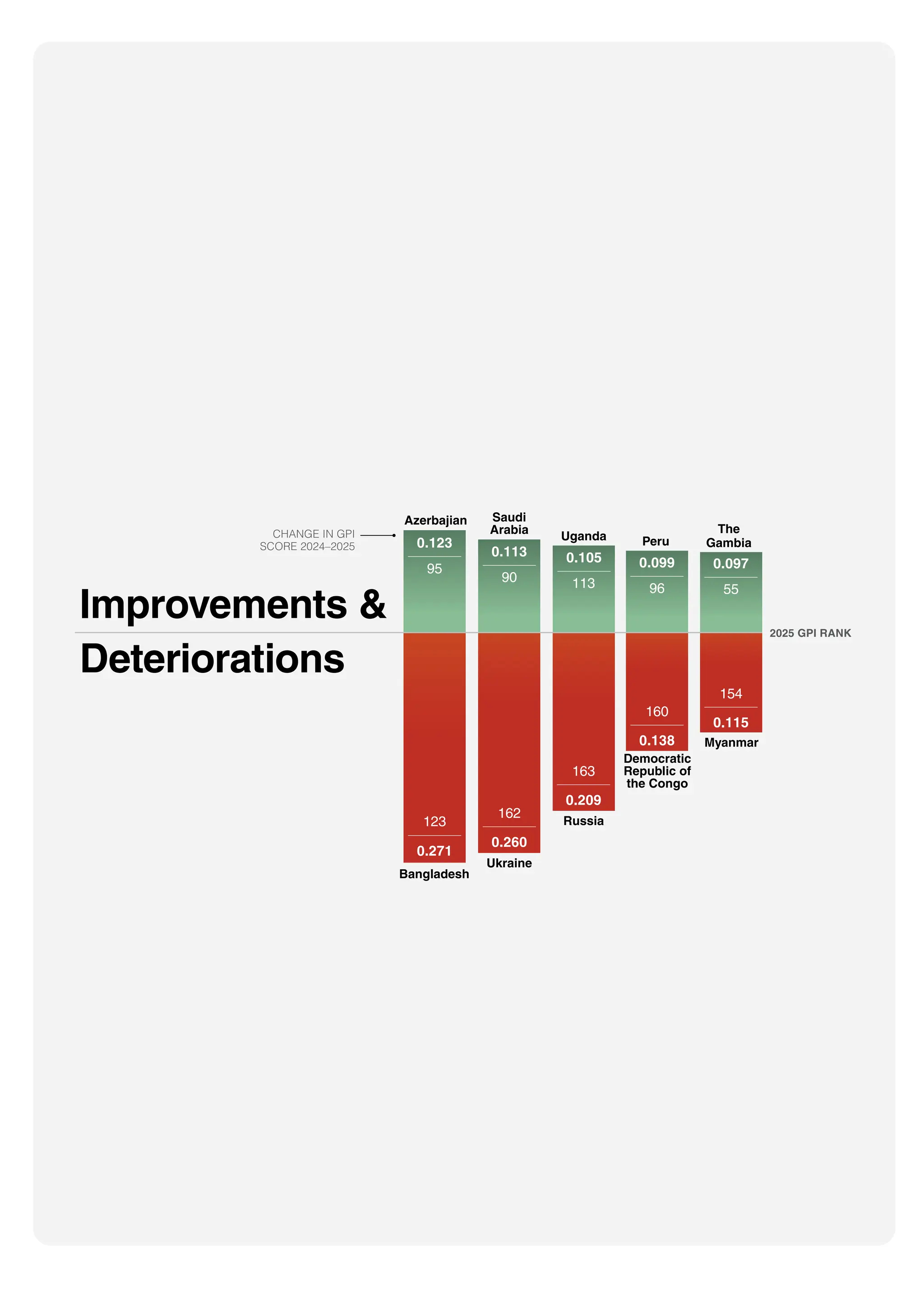

Improvements and Deteriorations 21

2025 Peace and Conflict Spotlight 26

GPI Trends 30

Domain Trends 32

Trends in Geopolitical Relations 37

The Economic Value of Peace 44

Global Economic Conditions and Rising Conflict Risk 52

Methodology at a Glance 58

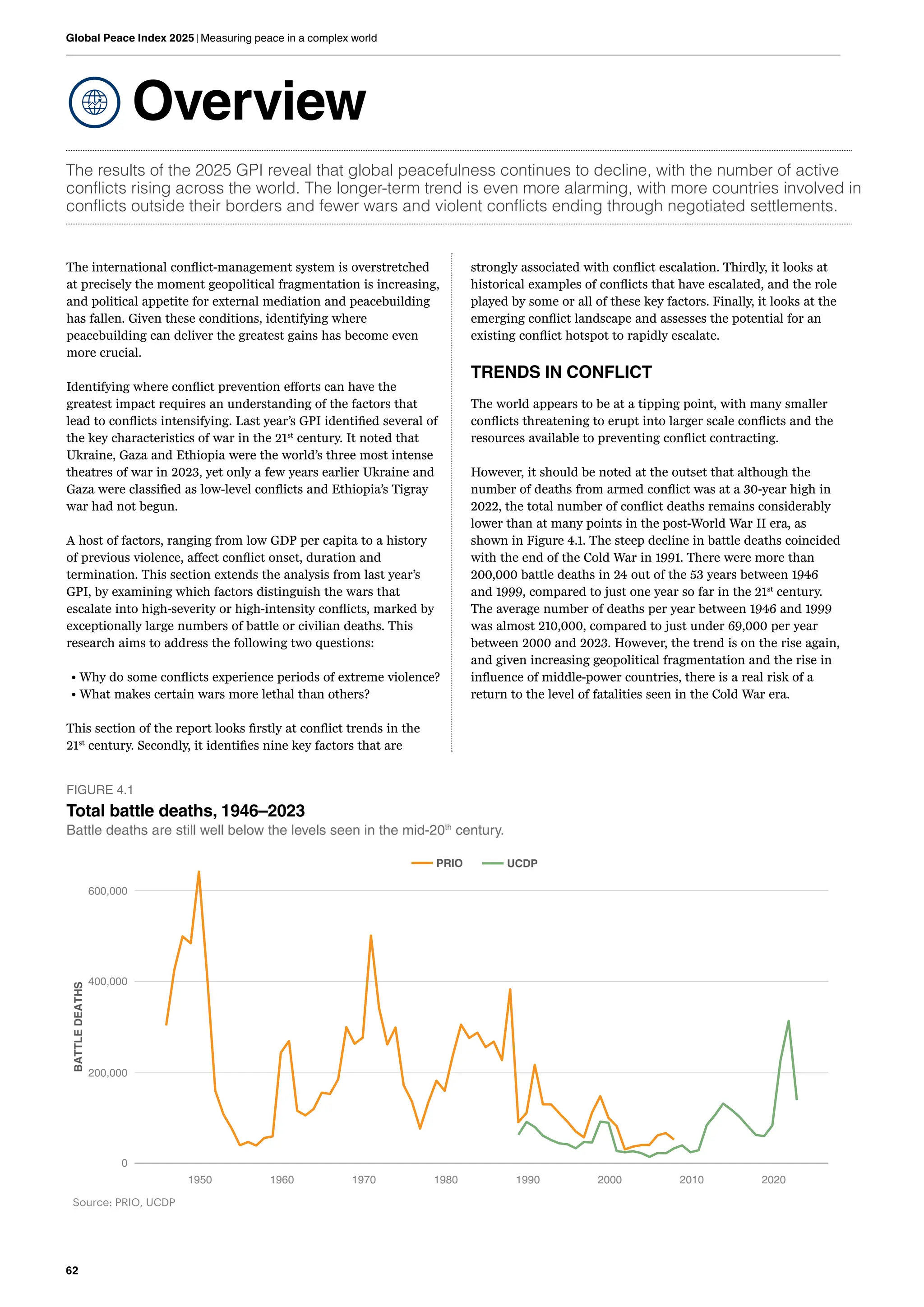

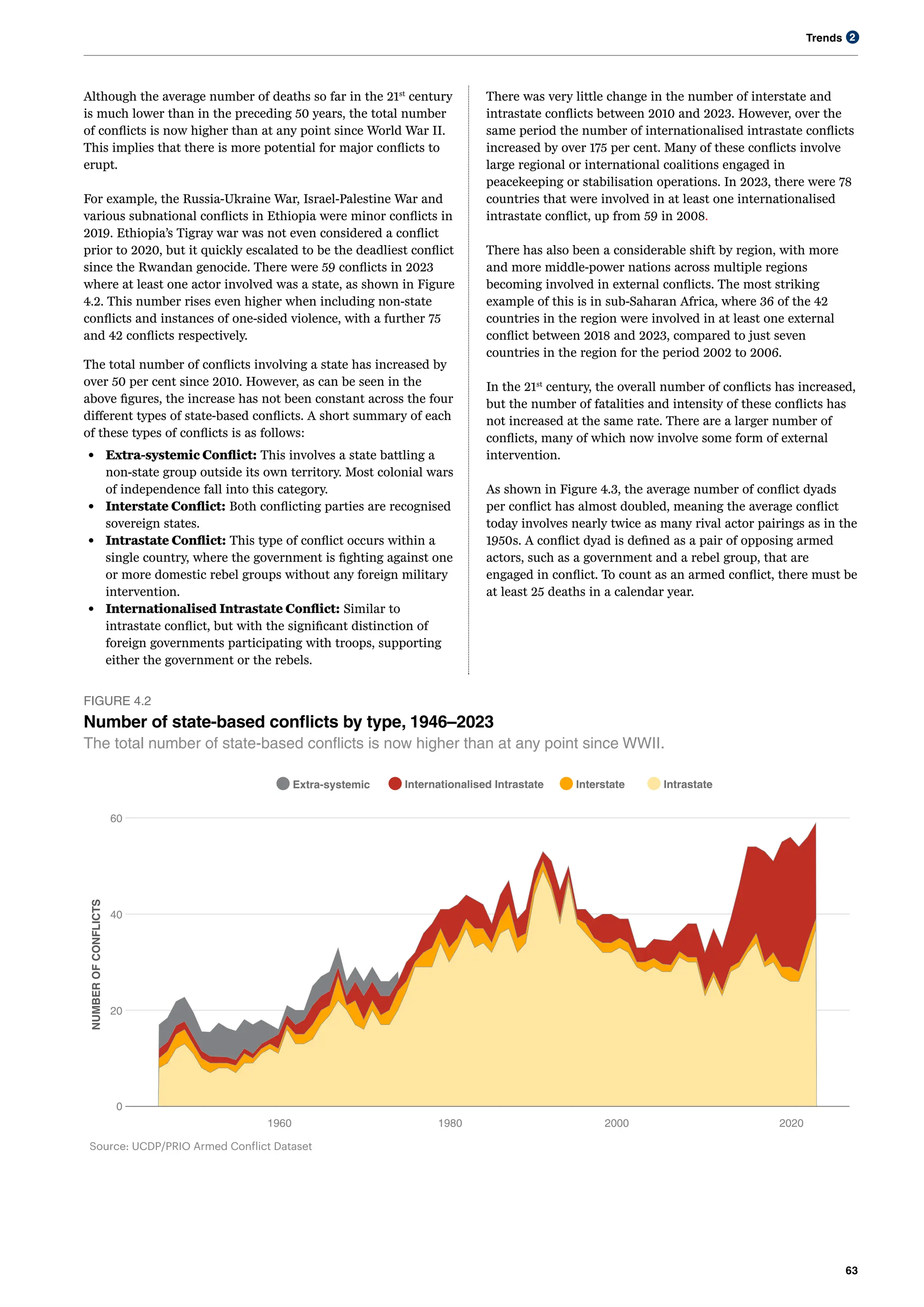

Overview 62

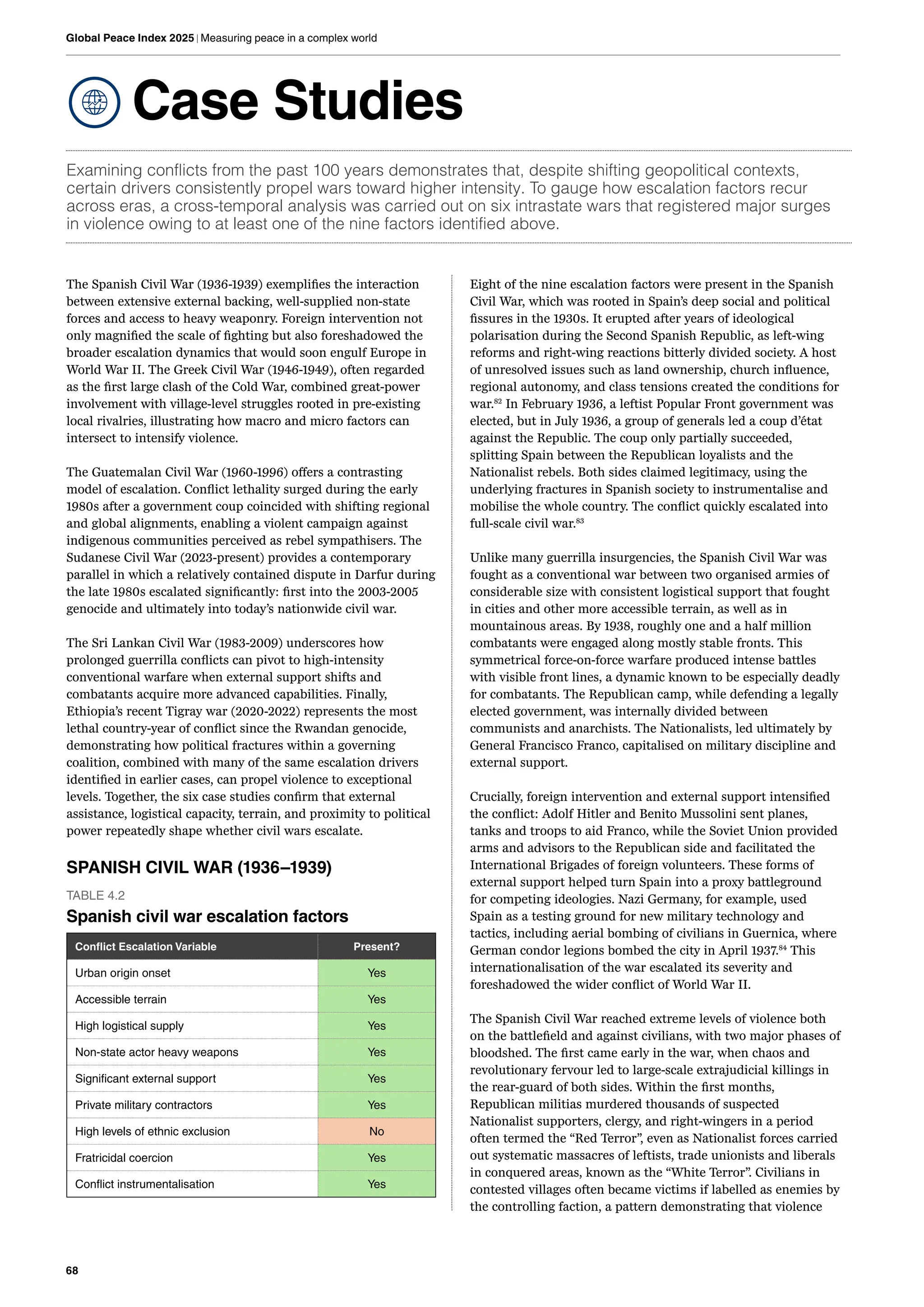

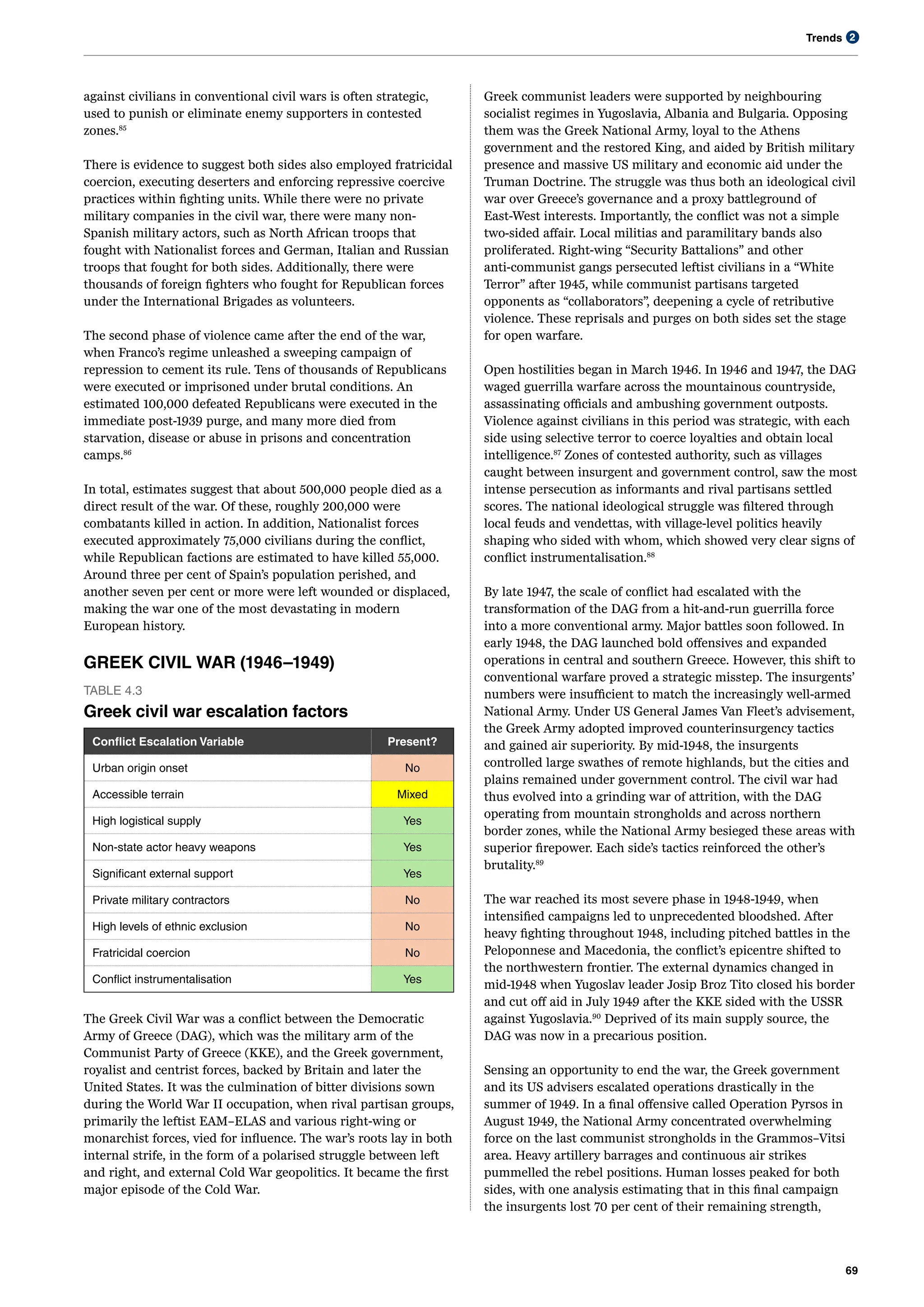

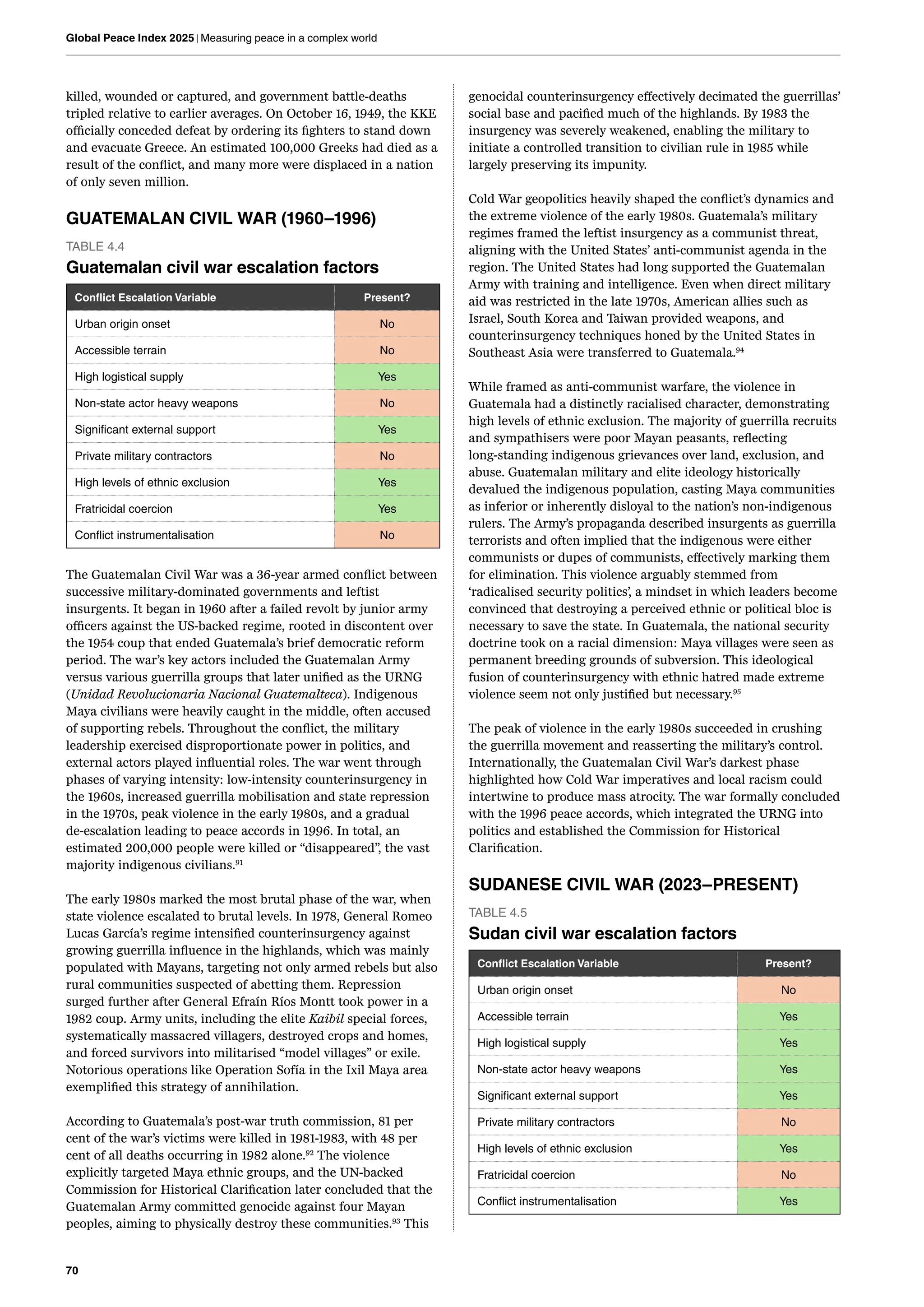

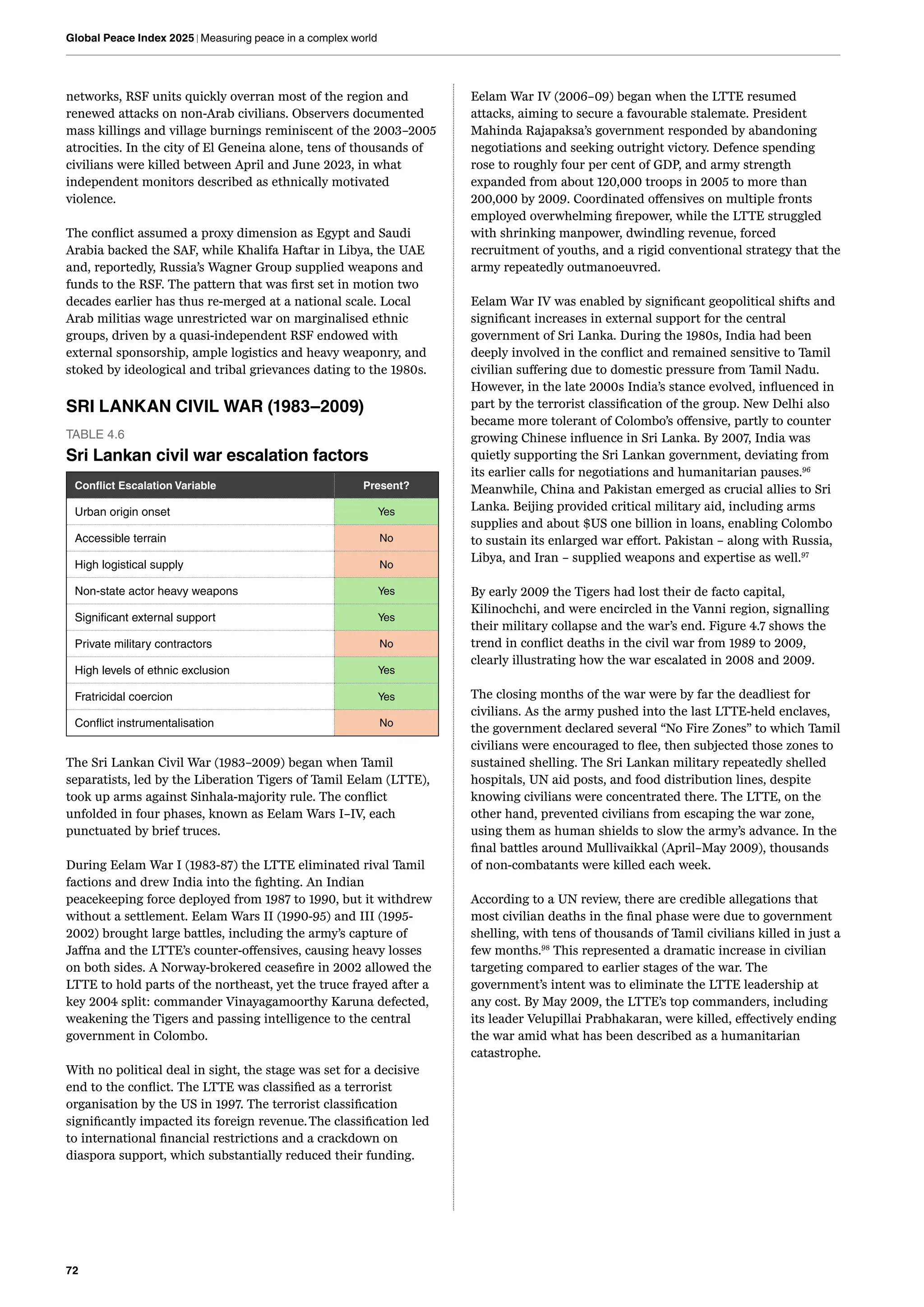

Conflict Escalation Factors 65

Case Studies 68

Escalation Hotspots 75

Conflict Escalation Matrix 88

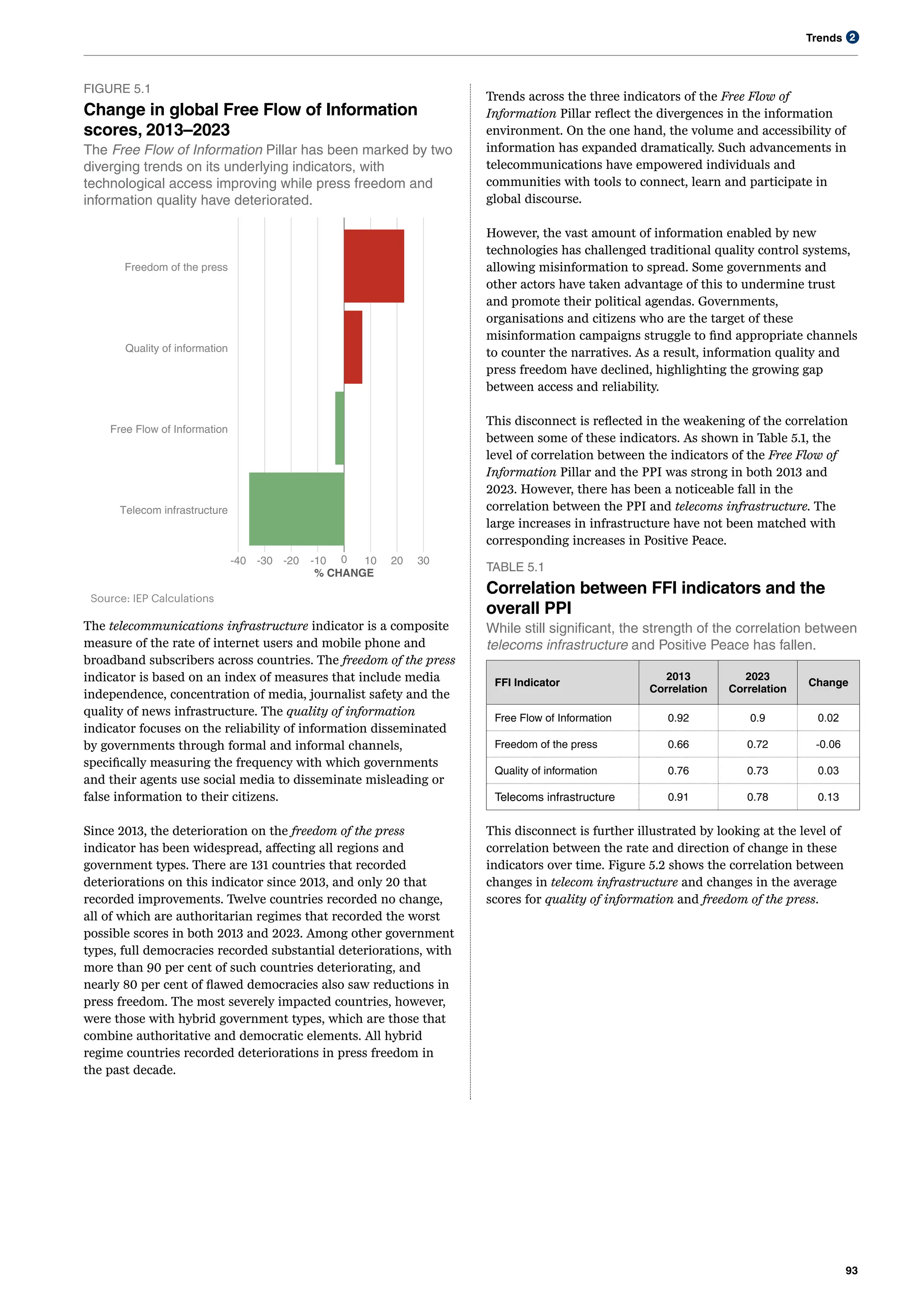

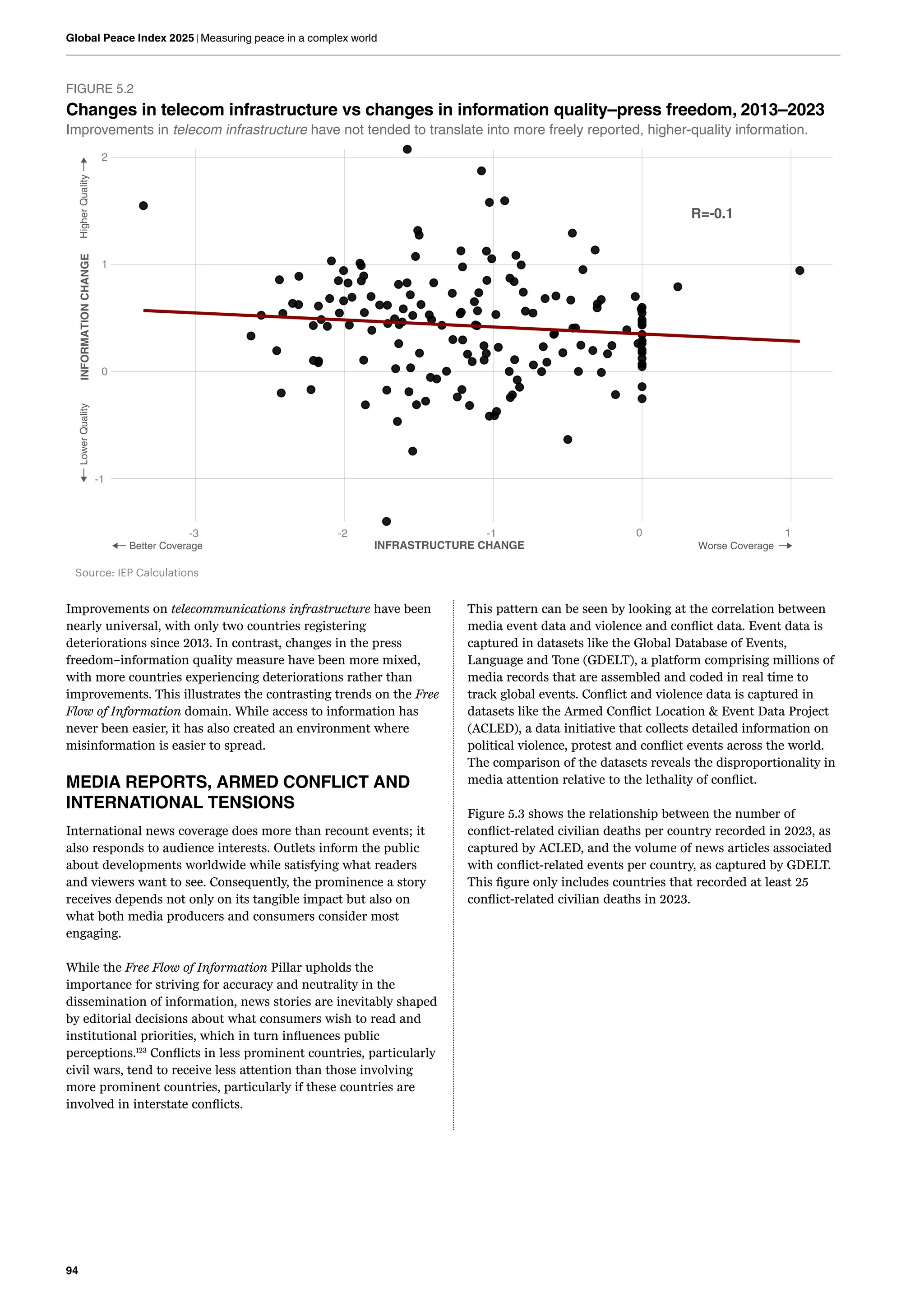

Information Flows: Divergent trends in access and quality 92

Media Reports, Armed Conflict and International Tensions 94

Appendix A: GPI Methodology 100

Appendix B: GPI Indicator Sources, Definitions & Scoring Criteria 104

Appendix C: GPI Domain Scores 111

Endnotes 114

Executive Summary 2

Key Findings 4

2

3

4

5

6

4.

2

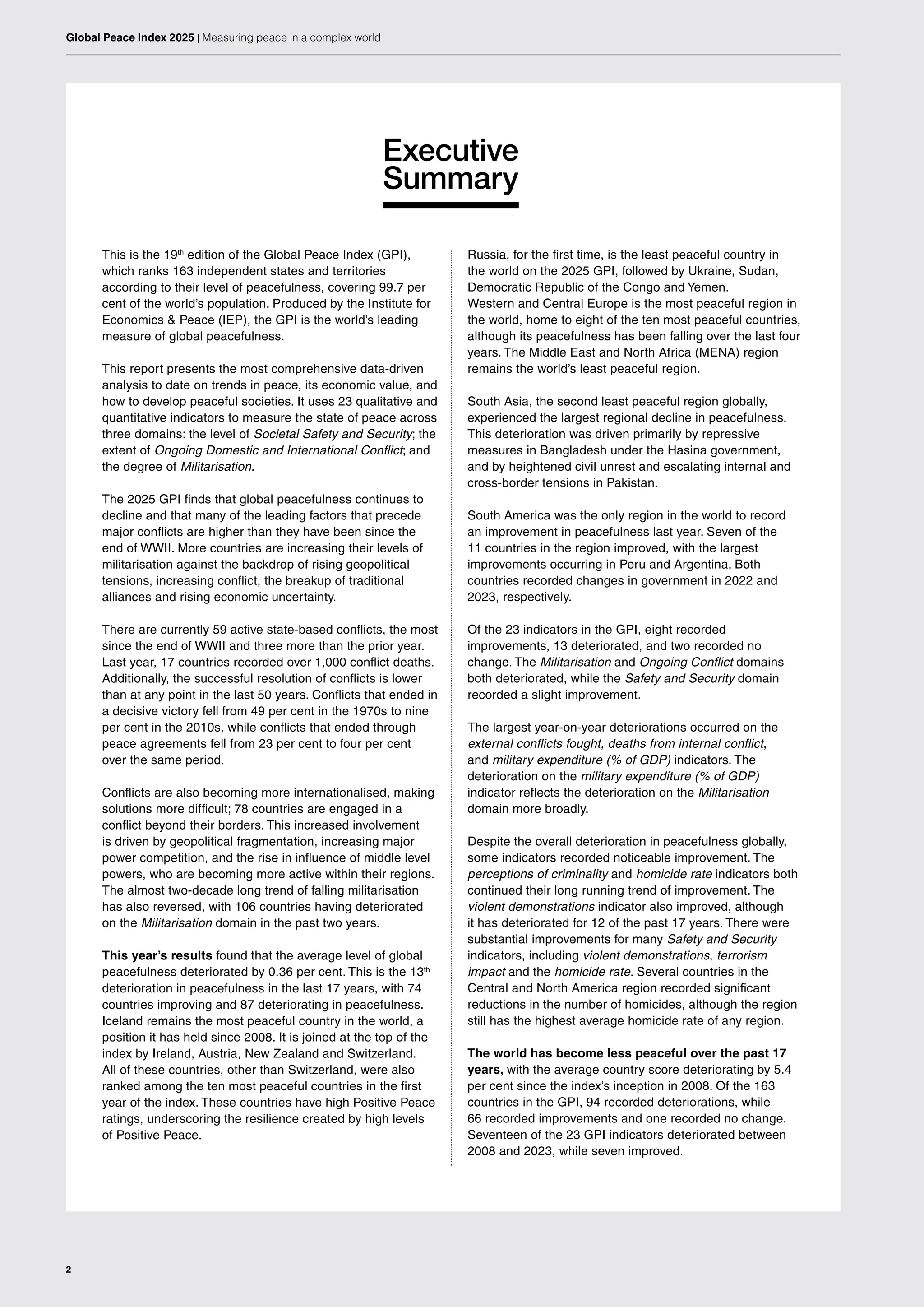

Global Peace Index2025 | Measuring peace in a complex world

Executive

Summary

This is the 19th

edition of the Global Peace Index (GPI),

which ranks 163 independent states and territories

according to their level of peacefulness, covering 99.7 per

cent of the world’s population. Produced by the Institute for

Economics & Peace (IEP), the GPI is the world’s leading

measure of global peacefulness.

This report presents the most comprehensive data-driven

analysis to date on trends in peace, its economic value, and

how to develop peaceful societies. It uses 23 qualitative and

quantitative indicators to measure the state of peace across

three domains: the level of Societal Safety and Security; the

extent of Ongoing Domestic and International Conflict; and

the degree of Militarisation.

The 2025 GPI finds that global peacefulness continues to

decline and that many of the leading factors that precede

major conflicts are higher than they have been since the

end of WWII. More countries are increasing their levels of

militarisation against the backdrop of rising geopolitical

tensions, increasing conflict, the breakup of traditional

alliances and rising economic uncertainty.

There are currently 59 active state-based conflicts, the most

since the end of WWII and three more than the prior year.

Last year, 17 countries recorded over 1,000 conflict deaths.

Additionally, the successful resolution of conflicts is lower

than at any point in the last 50 years. Conflicts that ended in

a decisive victory fell from 49 per cent in the 1970s to nine

per cent in the 2010s, while conflicts that ended through

peace agreements fell from 23 per cent to four per cent

over the same period.

Conflicts are also becoming more internationalised, making

solutions more difficult; 78 countries are engaged in a

conflict beyond their borders. This increased involvement

is driven by geopolitical fragmentation, increasing major

power competition, and the rise in influence of middle level

powers, who are becoming more active within their regions.

The almost two-decade long trend of falling militarisation

has also reversed, with 106 countries having deteriorated

on the Militarisation domain in the past two years.

This year’s results found that the average level of global

peacefulness deteriorated by 0.36 per cent. This is the 13th

deterioration in peacefulness in the last 17 years, with 74

countries improving and 87 deteriorating in peacefulness.

Iceland remains the most peaceful country in the world, a

position it has held since 2008. It is joined at the top of the

index by Ireland, Austria, New Zealand and Switzerland.

All of these countries, other than Switzerland, were also

ranked among the ten most peaceful countries in the first

year of the index. These countries have high Positive Peace

ratings, underscoring the resilience created by high levels

of Positive Peace.

Russia, for the first time, is the least peaceful country in

the world on the 2025 GPI, followed by Ukraine, Sudan,

Democratic Republic of the Congo and Yemen.

Western and Central Europe is the most peaceful region in

the world, home to eight of the ten most peaceful countries,

although its peacefulness has been falling over the last four

years. The Middle East and North Africa (MENA) region

remains the world’s least peaceful region.

South Asia, the second least peaceful region globally,

experienced the largest regional decline in peacefulness.

This deterioration was driven primarily by repressive

measures in Bangladesh under the Hasina government,

and by heightened civil unrest and escalating internal and

cross-border tensions in Pakistan.

South America was the only region in the world to record

an improvement in peacefulness last year. Seven of the

11 countries in the region improved, with the largest

improvements occurring in Peru and Argentina. Both

countries recorded changes in government in 2022 and

2023, respectively.

Of the 23 indicators in the GPI, eight recorded

improvements, 13 deteriorated, and two recorded no

change. The Militarisation and Ongoing Conflict domains

both deteriorated, while the Safety and Security domain

recorded a slight improvement.

The largest year-on-year deteriorations occurred on the

external conflicts fought, deaths from internal conflict,

and military expenditure (% of GDP) indicators. The

deterioration on the military expenditure (% of GDP)

indicator reflects the deterioration on the Militarisation

domain more broadly.

Despite the overall deterioration in peacefulness globally,

some indicators recorded noticeable improvement. The

perceptions of criminality and homicide rate indicators both

continued their long running trend of improvement. The

violent demonstrations indicator also improved, although

it has deteriorated for 12 of the past 17 years. There were

substantial improvements for many Safety and Security

indicators, including violent demonstrations, terrorism

impact and the homicide rate. Several countries in the

Central and North America region recorded significant

reductions in the number of homicides, although the region

still has the highest average homicide rate of any region.

The world has become less peaceful over the past 17

years, with the average country score deteriorating by 5.4

per cent since the index’s inception in 2008. Of the 163

countries in the GPI, 94 recorded deteriorations, while

66 recorded improvements and one recorded no change.

Seventeen of the 23 GPI indicators deteriorated between

2008 and 2023, while seven improved.

5.

Executive Summary

3

There arenow 34

countries who are

considered to have

substantial influence

in another country, up

from six in the 1970s.

The world is moving

into the age of ‘global

power fragmentation’.

Two of the three GPI domains deteriorated since 2008, with

Ongoing Conflict deteriorating by 17.5 per cent and Safety

and Security deteriorating by 2.5 per cent. Militarisation

was the only domain to improve, although this trend has

reversed over the past four years. Some of the largest

indicator deteriorations were for external conflicts fought,

internal conflicts fought, and the number of refugees and

IDPs.

The past year has seen some major shifts in international

affairs. The 2025 GPI report looks at these structural trends

to provide a better insight into contemporary factors that

affect conflict:

• Geopolitical fragmentation has substantially increased.

This is most noticeable on the relations between

neighbouring states indicator, which has substantially

deteriorated since 2008, with 59 countries recording

poorer ties with neighbours while only 19 improved.

• There have been notable reductions in global

integration for economics, trade, diplomacy and military

cooperation. They have been steadily falling since the

2008 Global Financial Crisis.

• The rising wealth of many countries

means that they have the economic

power for expanded international

influence, especially within their local

regions.

• Global trade as a share of global GDP

has flatlined for the last decade at

roughly 60 per cent, while restrictive

trade practices rose to more than 3,000

in 2023, nearly triple the 2019 figure.

• Developing countries spend an average

of 42 per cent of government revenue

on servicing debt. The largest creditor

is China.

• Expenditure on peacebuilding and peacekeeping was

just 0.52 per cent of total military spending in 2024,

compared to 0.83 per cent ten years ago. The number

of deployed peacekeeping troops has also fallen by

42 per cent over the past decade, while the number of

conflicts has risen steadily.

• Every nuclear-armed state has held or expanded its

arsenal since 2022, and great-power rivalry is fuelling

an arms race in advanced technologies, from AI-

enabled drones to counter-space systems.

• Internationalised intrastate conflicts, in which foreign

troops fight inside another state, have increased 175

per cent since 2010, drawing 78 countries into wars

beyond their borders.

There are now 34 countries who are considered to have

substantial influence in another country, up from six in the

1970s. Combined with the US and China having reached

or being near the limits of their influence, the world is

moving into the age of ‘global power fragmentation’.

China’s gross debt, estimated at approximately 300 per

cent of GDP, alongside signs of a significant asset bubble,

draws parallels with Japan’s economic conditions in the

late1980s. More power will shift to rising middle economies,

while most western powers struggle economically. How this

power dynamic unfolds, and its effect on conflict, remains to

be seen.

To better understand why violent conflicts can intensify

rapidly, IEP identified nine conflict escalation factors,

ranging from external military support and logistics, to

ethnic exclusion and conflict instrumentalisation. These

drivers were decisive in historic escalations. Based on

the presence of these factors, current conflicts that have

the potential to substantially escalate are South Sudan,

Ethiopia/Eritrea, the Democratic Republic of the Congo, and

Syria.

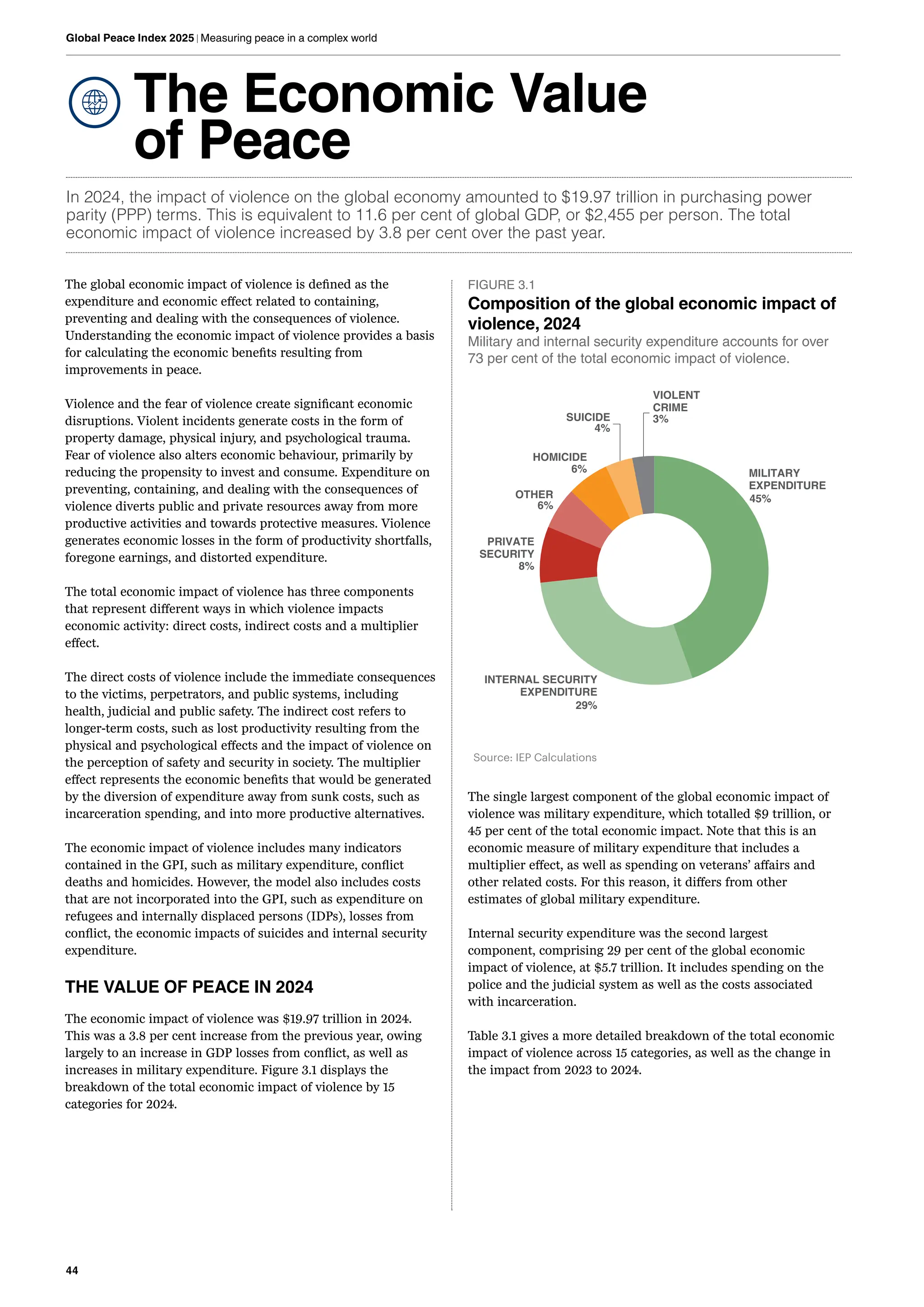

The economic impact of violence on the global economy

in 2024 was $19.97 trillion in purchasing power parity

(PPP) terms. This figure is equivalent to 11.6 per cent of the

world’s economic activity (gross world product), or $2,446

per person. Military and internal security expenditure

accounts for over 74 per cent of the figure, with the impact

of military spending alone accounting for $9 trillion in PPP

terms the past year.

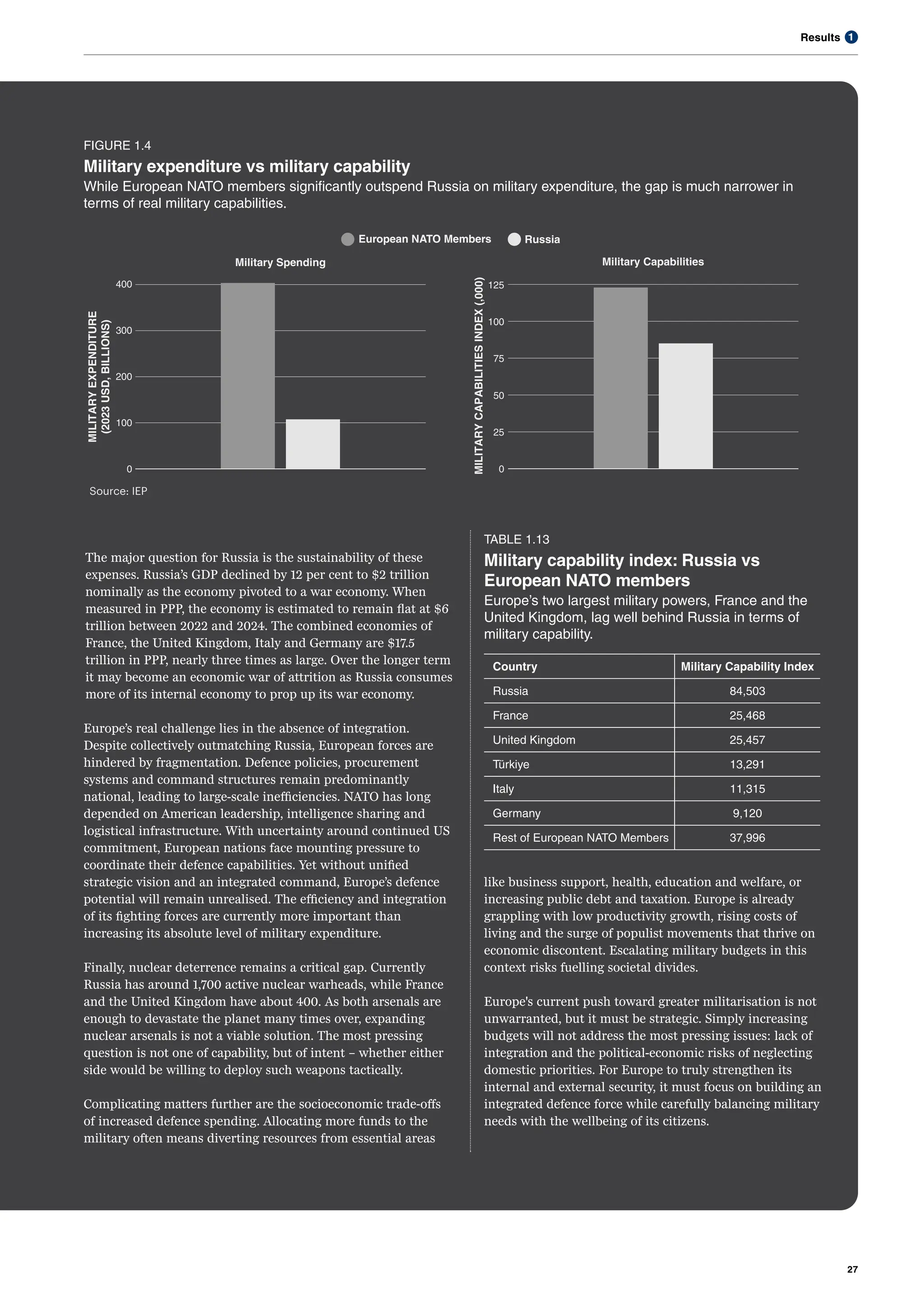

In Europe, adequate military expenditure

is essential to meet emerging threats.

However, Europe’s major challenge

is not increasing military expenditure.

It must also increase the efficiency,

integration and cohesiveness of its

military efforts. European NATO states

outspend Moscow by a wide margin, yet

their combined military capability only

modestly exceeds Russia’s. More raw

military expenditure will not solve this.

Additionally, many European countries

are experiencing increasing polarisation,

and military expenditure crowds out

investment in other productive areas including education,

health and business development. Items that underpin

social cohesion. Given the size of the budget outlays the

societal trade-offs need to be carefully considered.

In summary, the international order is approaching a tipping

point where rising economic fragmentation, accelerating re-

armament and multiple competing spheres of influence are

creating the conditions for the onset of large-scale conflict,

and the associated economic destruction. Underscoring

this is the sheer volume and geographic spread of currently

active conflicts, alongside reductions in proactive conflict

prevention initiatives, including reductions in funding for

peacebuilding and development aid.

The key to building peacefulness in times of conflict

and uncertainty is Positive Peace: the attitudes,

institutions and structures that create and sustain peaceful

societies. Positive Peace is strongly correlated with higher

GDP growth, lower interest rates, societal wellbeing and

more resilience to shocks. Although levels of Positive

Peace improved for over a decade up to 2019, they have

since been in decline, including in both North America and

Europe. Without adequate investment, further deterioration

in peacefulness appears likely.

6.

4

Global Peace Index2025 | Measuring peace in a complex world

Key Findings

Section 1 – Results

• The average level of country peacefulness deteriorated by 0.36 per

cent in the 2025 Global Peace Index. This is the sixth consecutive

year that global peacefulness has deteriorated.

• The average country score on the GPI has also deteriorated for 13

of the past 17 years, and has not improved on average in any year

since the 2013 GPI.

• In the past year, 74 countries recorded an improvement, while 87

countries recorded a deterioration in peacefulness. There are now

97 countries in the world that are less peaceful now than they were

at the inception of the index in 2008.

• In the past year, peacefulness improved slightly on average on the

Safety and Security domain but deteriorated on both the Ongoing

Conflict and Militarisation domains.

• This is the second consecutive year that the Militarisation domain

deteriorated on average, a reversal of the decade long trend that

had seen levels of Militarisation improving across much of the world.

• Of the 23 GPI indicators, eight recorded an improvement, 13

recorded a deterioration, and two recorded no change over the past

year. The largest deterioration was on external conflicts fought, while

the biggest improvement was on the perceptions of criminality

indicator.

• There were four indicators with average deteriorations of over two

per cent in the past year: external conflicts fought, deaths from

internal conflict, military expenditure, and weapons imports.

• There were 98 countries that were at least partially involved in some

form of external conflict over the past five years, up from 59 in 2008.

In most cases countries were offering support to an existing

government against armed rebels or terrorist groups.

• Military expenditure (% of GDP) recorded the second largest yearly

deterioration since the inception of the GPI. Eighty-four countries

increased their relative military expenditure, compared to just 50

where it decreased.

• There were 17 countries with over 1,000 internal conflict deaths in

2024, the highest since 1999, and a further 18 countries that

recorded over one hundred deaths in the last year.

• Many European countries are increasing their military expenditure

as a result of the war in Ukraine. However, raw military expenditure

is not the most pressing issue.

• Europe is experiencing increasing social tensions and declining

public trust in its institutions. The reallocation of public funds from

employment, healthcare and education towards defence heightens

the risk of further exacerbating these tensions.

• Europe’s real defence challenge lies in the absence of integration.

Despite collectively outmatching Russia, European forces are

hindered by fragmentation.

• Europe’s current military expenditure is almost four times that of

Russia, but its combined military capacity is only one third higher.

• Without unified strategic vision and command systems to direct

integrated military capabilities, Europe’s defence potential will

remain unrealised. The efficiency and integration of its fighting

forces are currently more important than increasing its absolute level

of military expenditure.

Section 2 – Trends

• Global stability has deteriorated over the past 17 years, marked by

substantial increases in political instability, the number and intensity

of conflicts, deaths from conflict, and increasing geopolitical

fragmentation.

• Peace has deteriorated every year since 2014. Over this period, 100

countries deteriorated and only 62 improved.

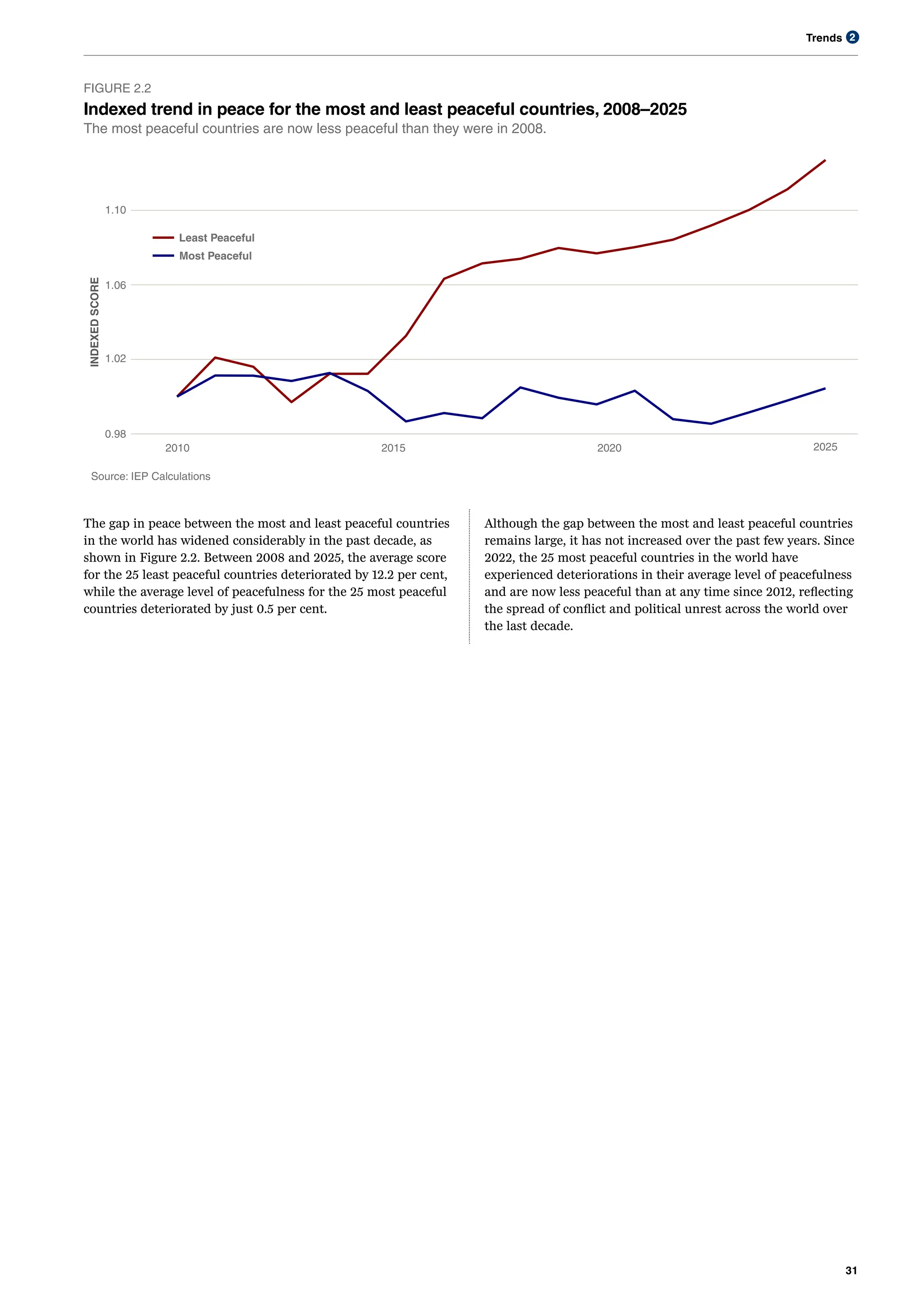

• The gap between the most and least peaceful countries continues

to grow, with ‘peace inequality’ widening by 11.7 per cent in the past

two decades. The 25 most peaceful countries deteriorated by 0.5

per cent, while the least peaceful deteriorated by 12.2 per cent.

• Two of the three GPI domains have deteriorated since 2008, with

Ongoing Conflict and Safety and Security deteriorating by 17.5 per

cent and 2.5 per cent, respectively. Only the Militarisation domain

improved, with peacefulness increasing on that domain by 2.7 per

cent.

• Though the Militarisation domain improved since 2008, that trend

has begun to reverse over the last five years as many countries

respond to an increasing number of threats and rising geopolitical

uncertainty.

• Conversely, although the Safety and Security domain deteriorated,

several indicators have shown sustained improvement, most notably

the homicide rate and perceptions of criminality indicators.

• Across the 23 GPI indicators, external conflicts fought and internal

conflicts fought had the largest deteriorations. This reflects not only

the spread of conflict around the world, but the increasing

involvement of external actors in civil conflicts.

• Deaths from internal conflict increased by over 438 per cent in the

past 17 years, with 75 countries recording at least one conflict death

in the past year.

• Around the world, there are now over 122 million people that have

been forcibly displaced. There are now 17 countries where more

than five per cent of the population are either refugees or have been

internally displaced. The number of people forcibly displaced has

increased by over 185 per cent since the inception of the GPI.

• Eight of the ten largest weapons exporters on a per capita basis are

Western democracies, including France, Sweden, Italy, the

Netherlands, Germany and Norway.

• In the past 17 years, more countries deteriorated on violent

demonstrations than any other indicator, with 109 deteriorating and

only 23 improving. The rise of technology was a critical enabler of

global protests and mass mobilisation.

• Global economic stagnation, increasing debt, and the

weaponisation of economic interdependence via trade wars, are key

factors shaping the economic landscape of geopolitics in the 21st

century.

• Geopolitical fragmentation is rising, with levels now exceeding those

seen during the Cold War. The rise in fragmentation has been

especially noticeable since 2008, after it had been steadily

decreasing since the end of the Cold War.

• Global trade has plateaued at around 60 per cent of global GDP

over the past decade, following rapid growth after 1990.

• Global military spending hit a record $2.7 trillion in 2024, a nine per

cent increase from the previous year, driven largely by conflicts such

as the war in Ukraine.

7.

Key Findings

5

• Competitionfor influence is intensifying in regions like Africa, South

Asia and South America. In the Sahel, instability and scarce

resources are drawing in rival powers and fuelling a complex struggle

for control.

• The number of globally influential countries has nearly tripled since

the Cold War, rising from 13 to 34 by 2023, with nations like Türkiye,

the UAE, Vietnam, South Africa, Brazil and Indonesia expanding their

influence.

Section 3 – Economic Impact of Violence

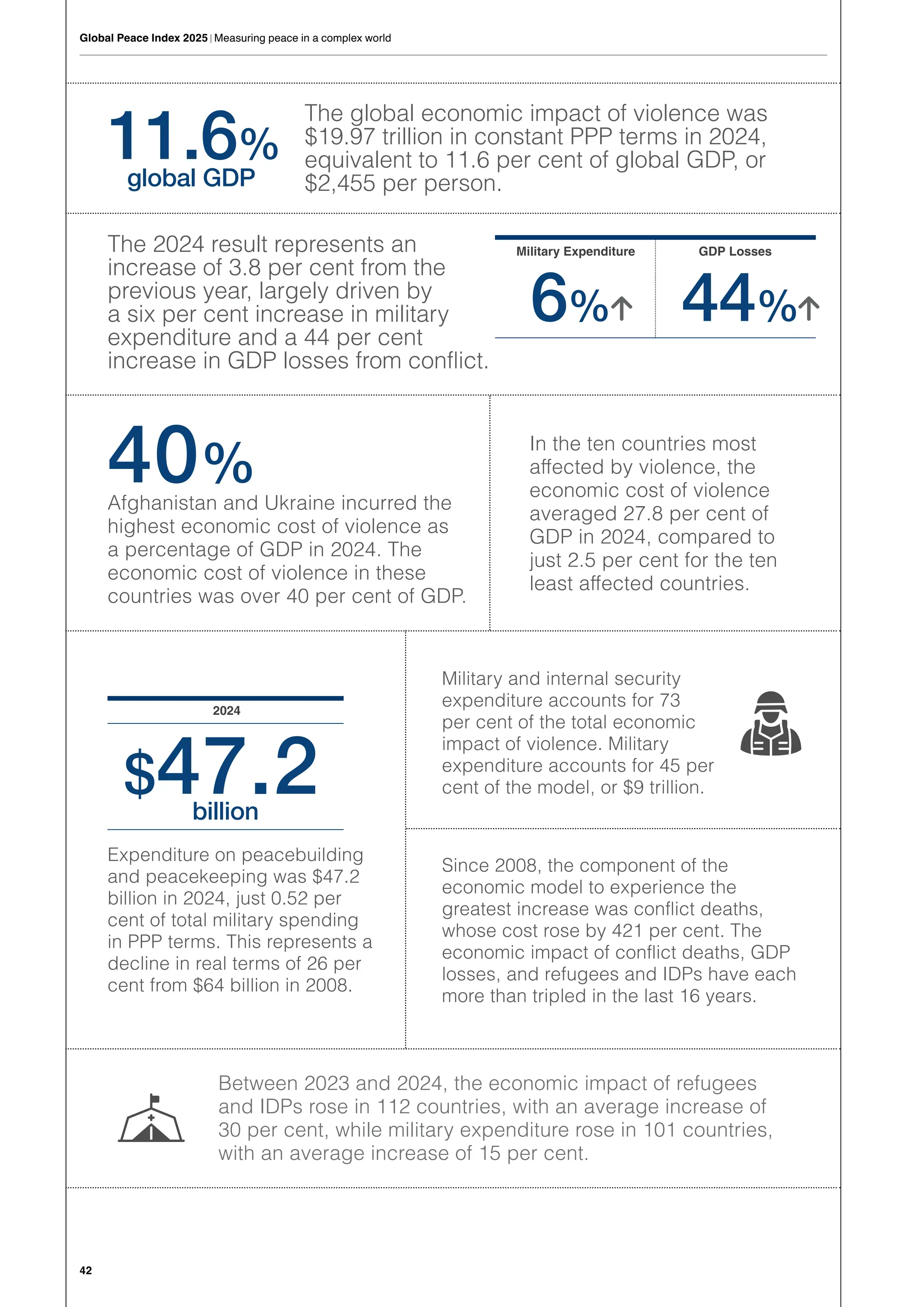

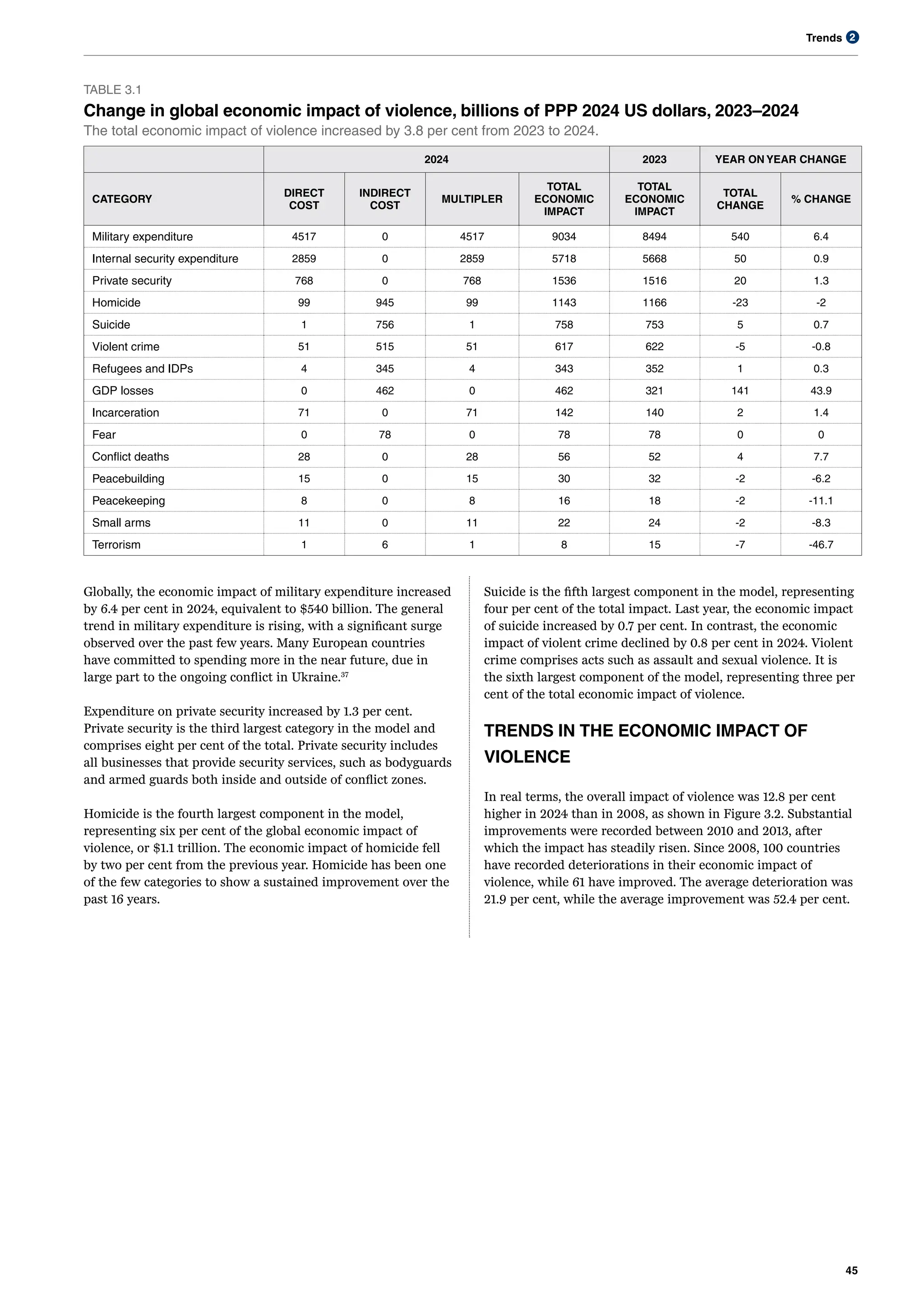

• The global economic impact of violence was $19.97 trillion in

constant PPP terms in 2024, equivalent to 11.6 per cent of global

GDP, or $2,455 per person.

• The 2024 result represents an increase of 3.8 per cent from the

previous year, largely driven by a six per cent increase in military

expenditure and a 44 per cent increase in GDP losses from conflict.

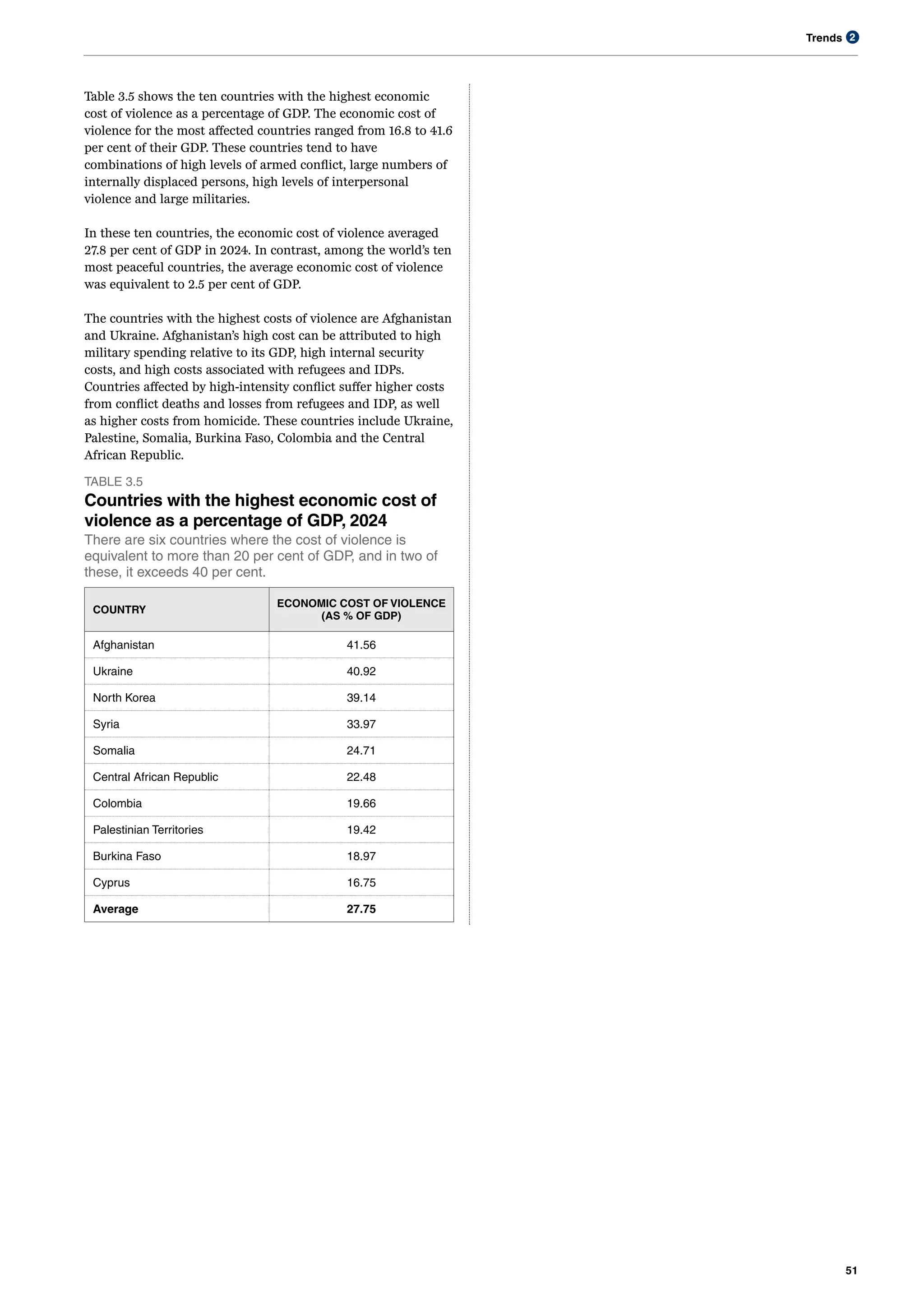

• Afghanistan and Ukraine incurred the highest economic cost of

violence as a percentage of GDP in 2024. The economic cost of

violence in these countries was over 40 per cent of GDP.

• In the ten countries most affected by violence, the economic cost of

violence averaged 27.8 per cent of GDP in 2024, compared to just

2.5 per cent for the ten least affected countries.

• Expenditure on peacebuilding and peacekeeping was $47.2 billion in

2024, just 0.52 per cent of total military spending in PPP terms. This

represents a decline in real terms of 26 per cent from $64 billion in

2008.

• Military and internal security expenditure accounts for 73 per cent of

the total economic impact of violence. Military expenditure accounts

for 45 per cent of the model, or $9 trillion.

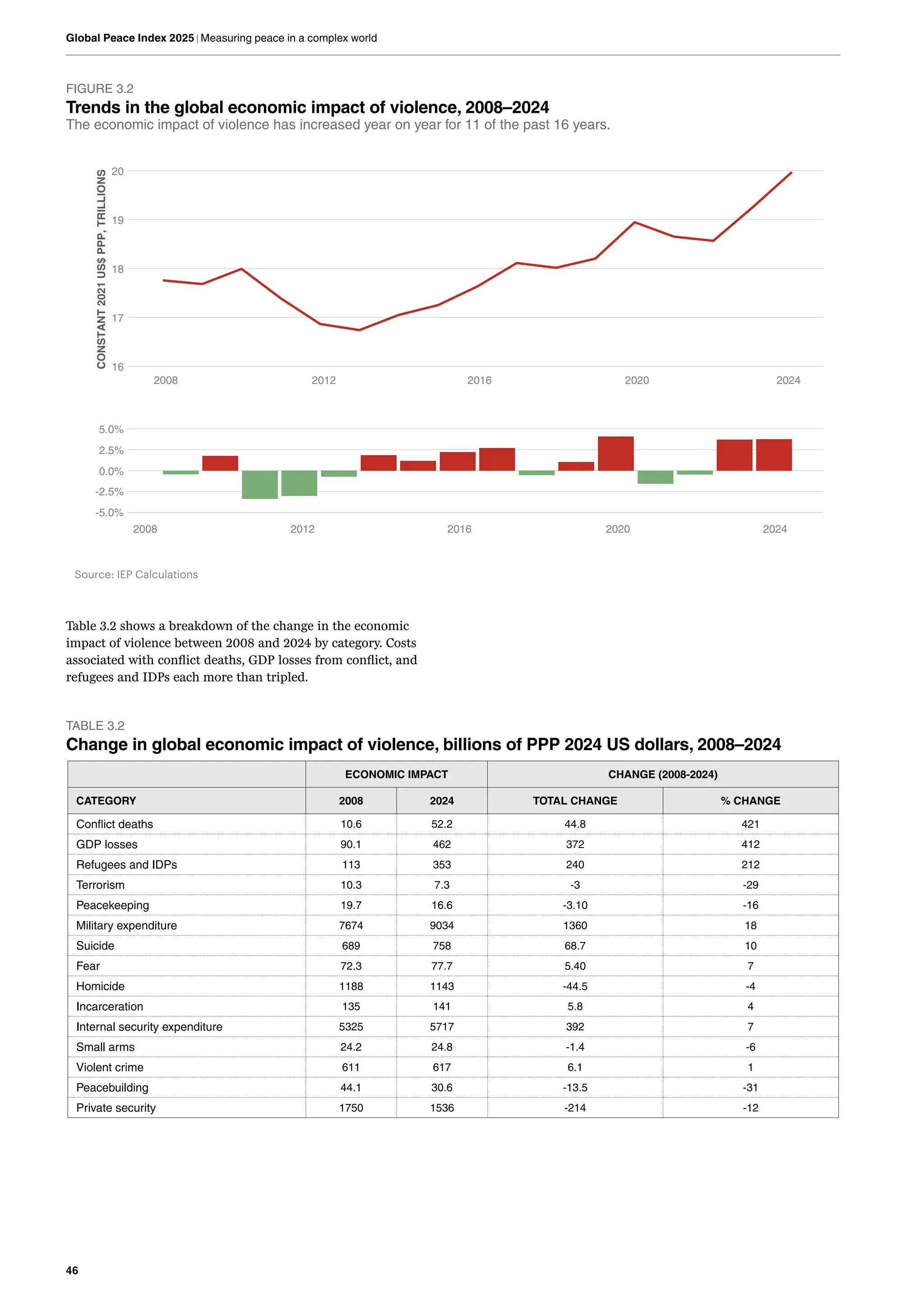

• Since 2008, the component of the economic model to experience the

greatest increase was conflict deaths, whose cost rose by 421 per

cent. The economic impact of conflict deaths, GDP losses, and

refugees and IDPs, have each more than tripled in the last 16 years.

• Between 2023 and 2024, the economic impact of refugees and IDPs

rose in 112 countries, with an average increase of 30 per cent, while

military expenditure rose in 101 countries, with an average increase

of 15 per cent.

• Many of the macro-economic adjustments happening globally are

likely to increase the risk of conflict in the near future.

• In 2024, global GDP growth remained modest at 3.3 per cent, while

inflation stayed elevated at 5.8 per cent, despite easing from its 2022

peak.

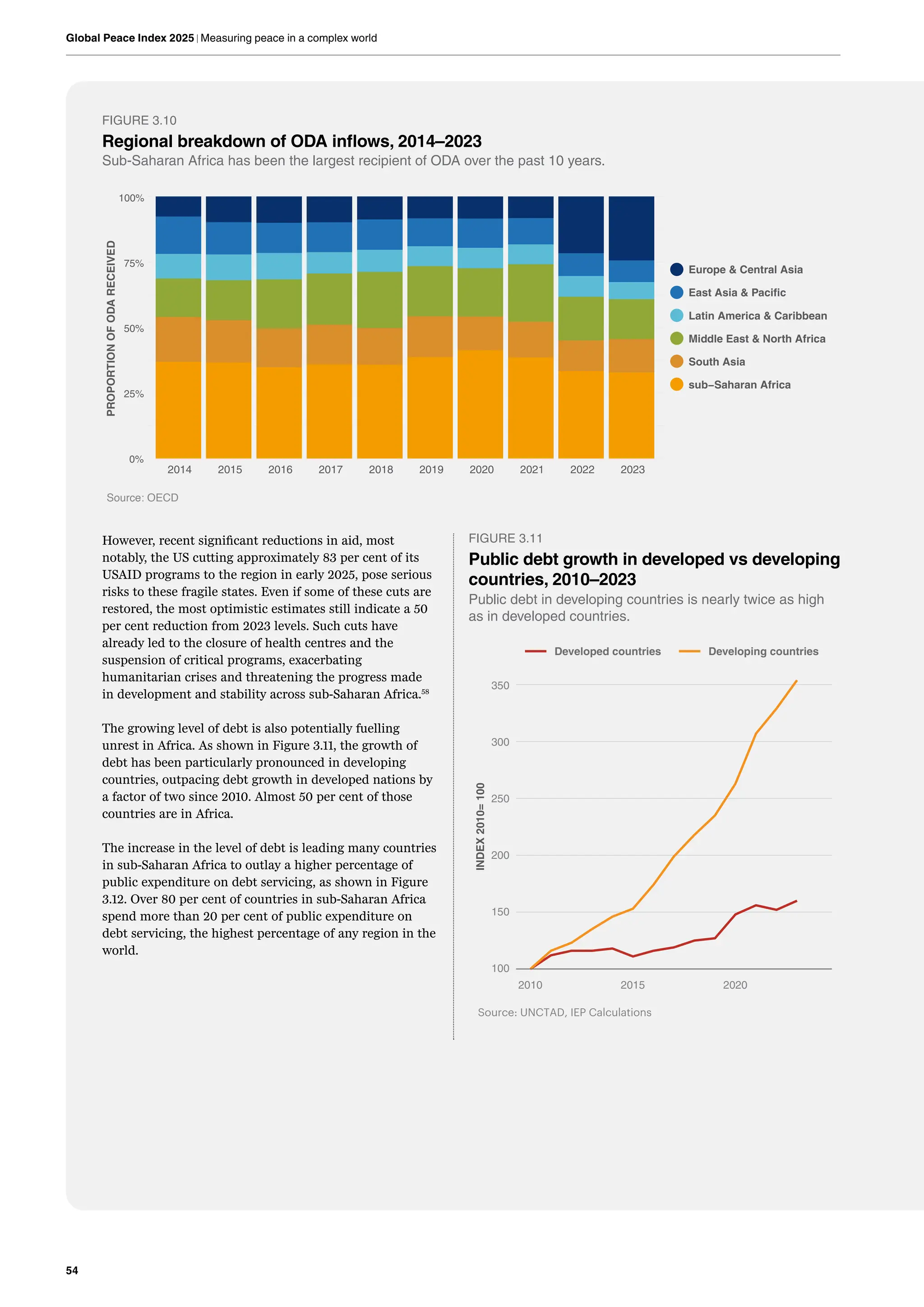

• Sub-Saharan Africa has been the largest recipient of Official

Development Assistance over the past decade, but recent aid cuts

will affect essential services and development.

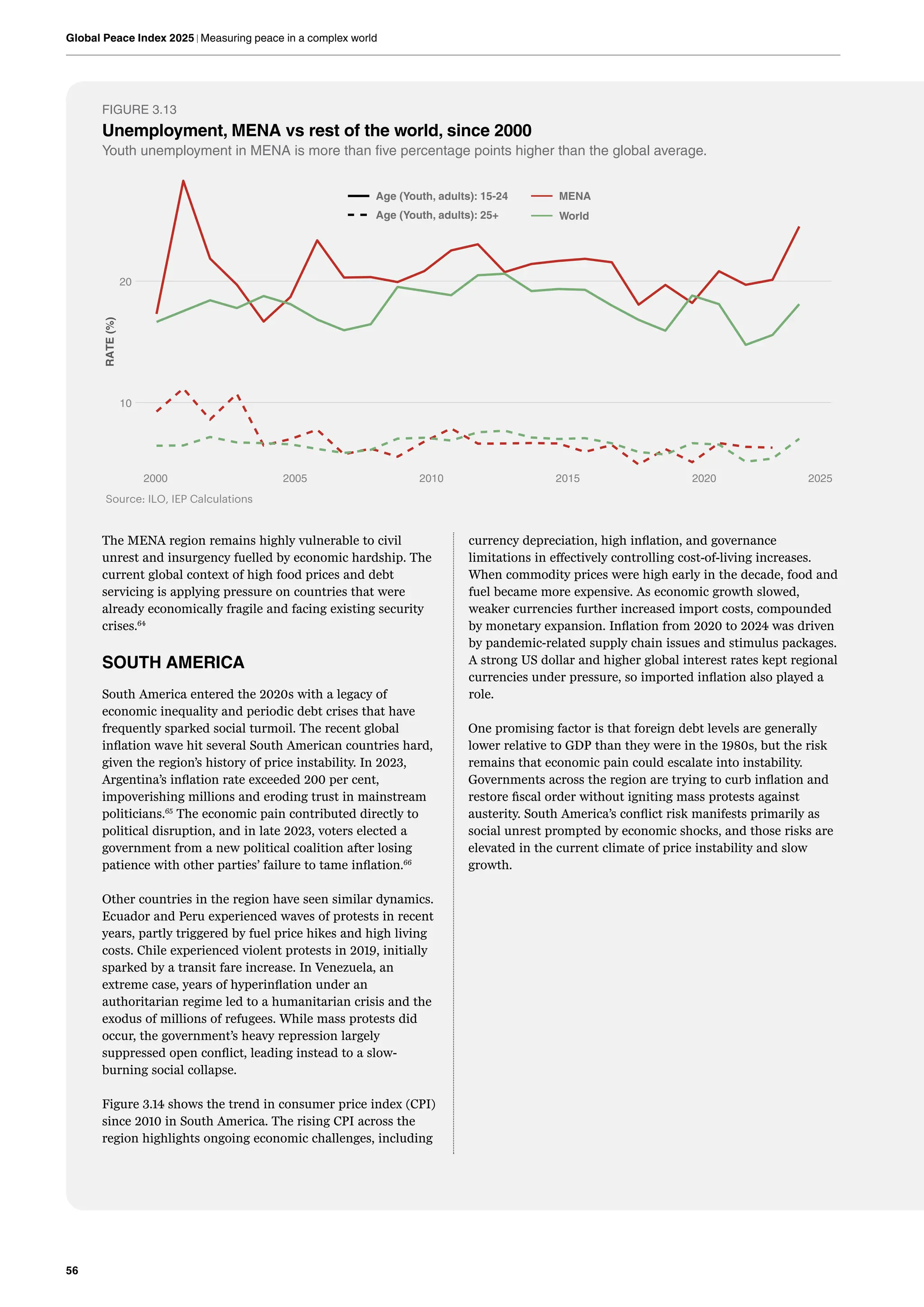

• Youth unemployment in the Middle East and North Africa remained

high, at 24.5 per cent in 2023, which was more than ten percentage

points above the global average.

• While total global debt as proportion of GDP has declined slightly

since 2020, public debt continues to rise, reaching $97 trillion in

2023. Debt in developing countries has been growing twice as fast as

in advanced economies since 2010.

• Debt service is placing increasing pressure on public finances, with

economically developing countries spending an average of 42 per

cent of government revenue on servicing debt.

Section 4 – Why Conflicts Escalate

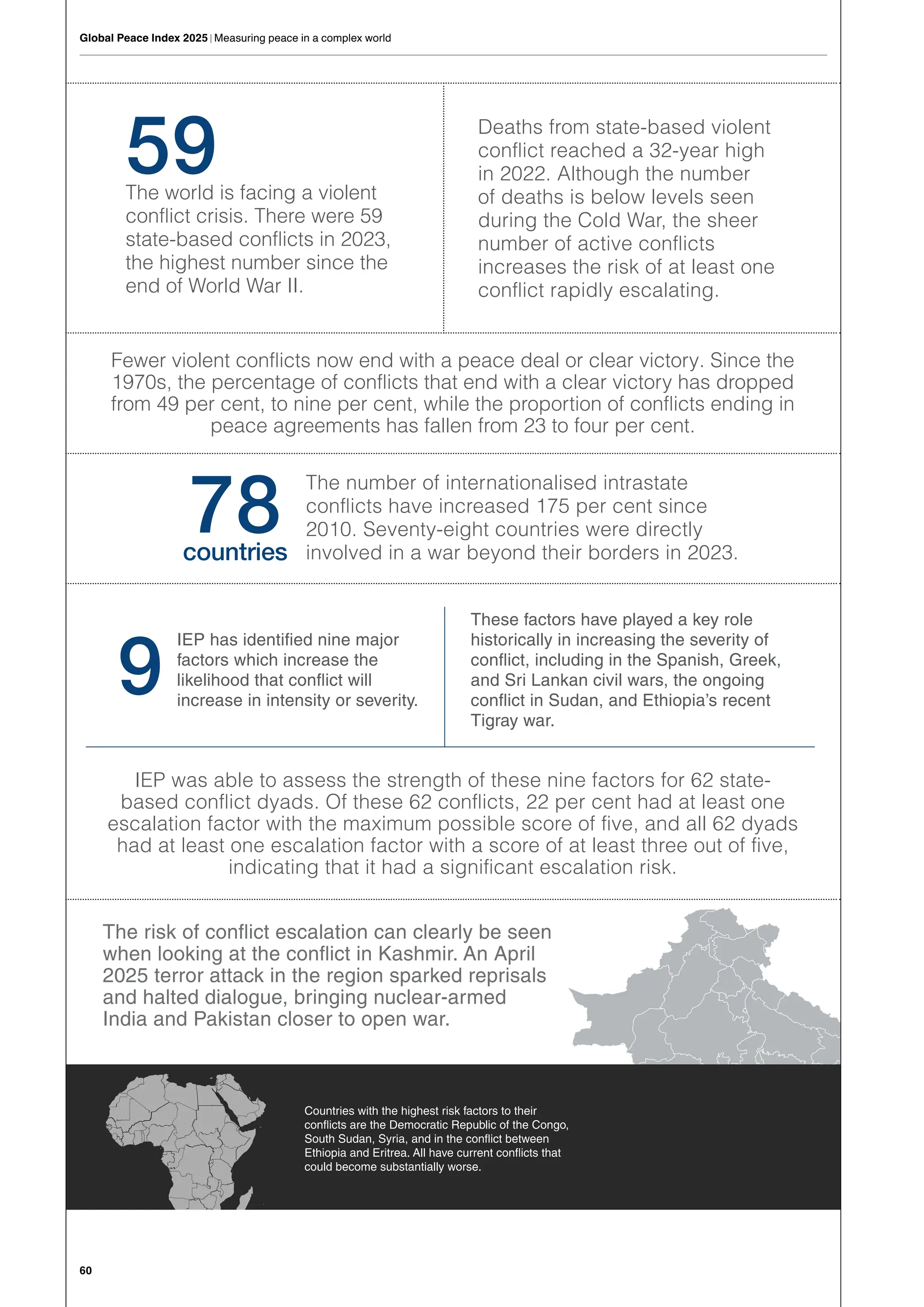

• The world is facing a violent conflict crisis. There were 59 state-based

conflicts in 2023, the highest number since the end of World War II.

• Deaths from state-based violent conflict reached a 32-year high in

2022. Although the number of deaths is below levels seen during

the Cold War, the sheer number of active conflicts increases the

risk of at least one conflict rapidly escalating.

• Fewer violent conflicts now end with a peace deal or clear victory.

Since the 1970s, the percentage of conflicts that end with a clear

victory has dropped from 49 per cent to nine per cent, while the

proportion of conflicts ending in peace agreements has fallen from

23 per cent to four per cent.

• The number of internationalised intrastate conflicts have increased

175 per cent since 2010. Seventy-eight countries were directly

involved in a war beyond their borders in 2023.

• IEP has identified nine major factors which increase the likelihood

that conflict will increase in intensity or severity.

• These factors have played a key role historically in increasing the

severity of conflict, including in the Spanish, Greek, and Sri Lankan

civil wars, the ongoing conflict in Sudan, and Ethiopia’s recent

Tigray war.

• IEP was able to assess the strength of these nine factors for 62

state-based conflict dyads. Of these 62 conflicts, 22 per cent had at

least one escalation factor with the maximum possible score of five,

and all 62 dyads had at least one escalation factor with a score of

at least three out of five, indicating that it had a significant

escalation risk.

• The risk of conflict escalation can clearly be seen when looking at

the conflict in Kashmir. An April 2025 terror attack in the region

sparked reprisals and halted dialogue, bringing nuclear-armed

India and Pakistan closer to open war.

• Countries facing the highest conflict risk factors are the Democratic

Republic of the Congo, South Sudan, Syria, and the ongoing

conflict between Ethiopia and Eritrea. All have current conflicts that

could become substantially worse.

Section 5 – Positive Peace and the Media

• The Free Flow of Information is foundational to peace. Societies

with open, better information systems consistently rank higher on

the Global Peace Index.

• Reliable information flows support both domestic stability and

global action. Everything from business efficiency to prompt

humanitarian responses rely on up to date and accurate

information.

• Trends in the Free Flow of Information Pillar are mixed. While

access to telecommunications has improved more than any other

indicator in the Positive Peace Index, press freedom and

information quality have seen the steepest declines.

• Media coverage of conflict remains highly unbalanced. In 2023,

civilian deaths in high-income countries received 100 times more

media articles than a similar number of deaths in low-income

countries.

• Civil conflicts are under-reported. They receive less attention on

average than conflicts between states, even when they have

substantially higher numbers of fatalities.

• Major power rivalries dominate headlines. Media reporting on

international affairs focuses heavily on competitive interactions

between global powers.

• While the expansion of telecommunications and social media offers

unparalleled access to information, it is often accompanied by

low-quality, inflammatory or partisan content, deepening social

divides.

8.

There were 17countries with over

1,000 internal conflict deaths in 2024,

the highest since 1999 and a further

18 countries that recorded over one

hundred deaths in the last year.

There were 98 countries that were at least partially

involved in some form of external conflict over the

past five years, up from 59 in 2008. In most cases

countries were offering support to an existing

government against armed rebels or terrorist groups.

Without unified strategic vision and command systems to direct

integrated military capabilities, Europe’s defence potential will

remain unrealised. The efficiency and integration of its fighting

forces are currently more important than increasing its absolute

level of military expenditure.

Europe’s real defence challenge

lies in the absence of integration.

Despite collectively outmatching

Russia, European forces are

hindered by fragmentation.

There were four indicators with average

deteriorations of over two per cent in

the past year: external conflicts fought,

deaths from internal conflict, military

expenditure, and weapons imports.

The average level of country

peacefulness deteriorated

by 0.36 per cent in the 2025

Global Peace Index. This is

the sixth consecutive year

that global peacefulness

has deteriorated.

The average country score on

the GPI has also deteriorated for

13 of the past 17 years, and has

not improved on average in any

year since the 2013 GPI.

This is the second consecutive

year that the Militarisation domain

deteriorated on average, a reversal

of the decade long trend that

had seen levels of Militarisation

improving across much of the world.

Military expenditure (% of GDP) recorded

the second largest yearly deterioration

since the inception of the GPI.

84 countries increased their relative

military expenditure, compared to just 50

where it decreased.

In the past year 74 countries

recorded an improvement, while 87

countries recorded a deterioration

in peacefulness. There are now 97

countries in the world that are less

peaceful now than they were at the

inception of the index in 2008.

In the past year peacefulness

improved slightly on average on

the Safety and Security domain but

deteriorated on both the Ongoing

Conflict and Militarisation domains.

74

0.36

84

87

50 17

Improvements

Increased

Deteriorations

Decreased Countries

Of the 23 GPI indicators, eight recorded an

improvement, 13 recorded a deterioration,

and two recorded no change over the

past year. The largest deterioration was on

external conflicts fought, while the biggest

improvement was on the perceptions of

criminality indicator.

8 13 2

Improvements Deteriorations No Change

6

Global Peace Index 2025 | Measuring peace in a complex world

8

Global Peace Index2025 | Measuring peace in a complex world

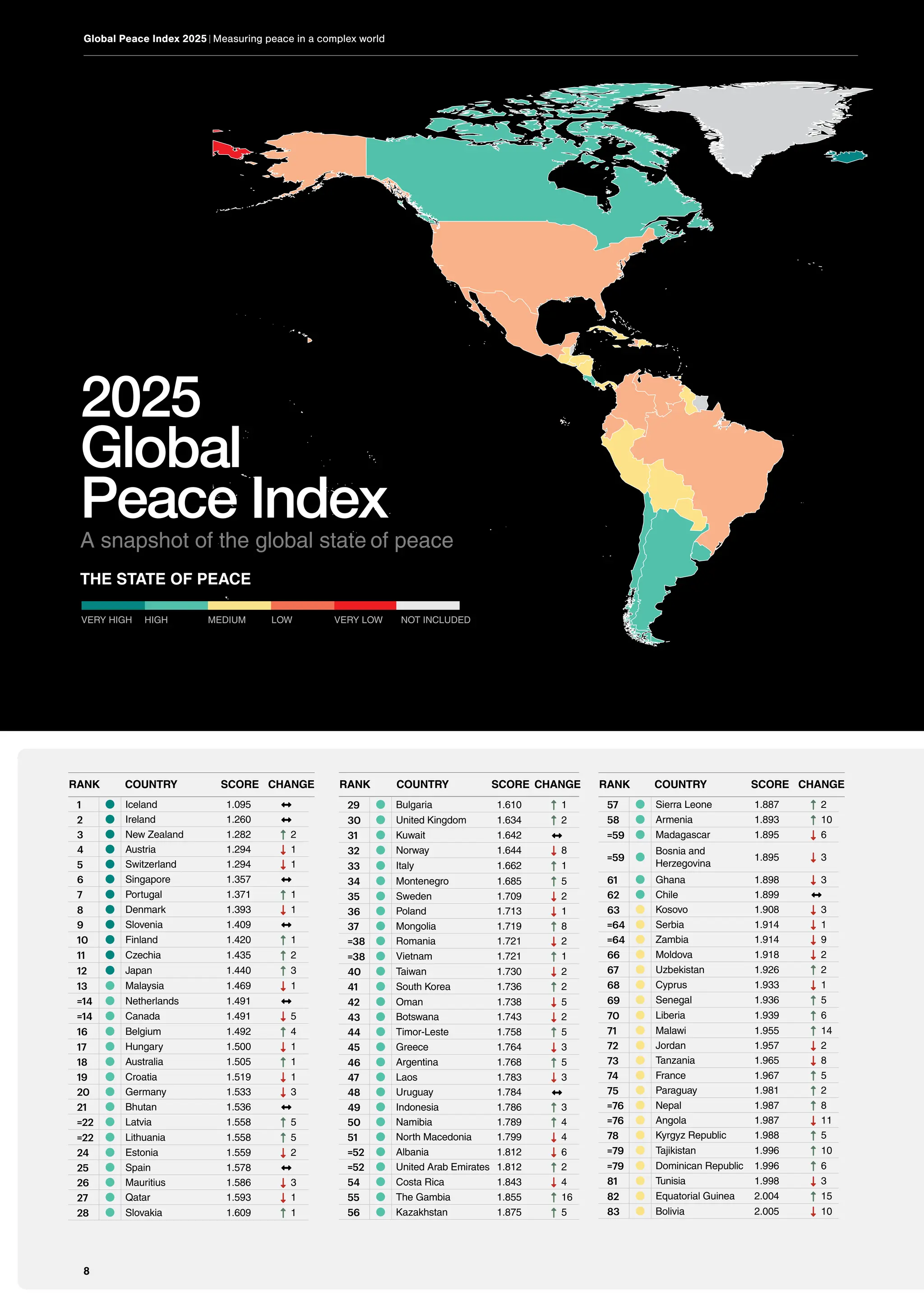

1 Iceland 1.095 ↔

2 Ireland 1.260 ↔

3 New Zealand 1.282 UP-LONG 2

4 Austria 1.294 DOWN-LONG 1

5 Switzerland 1.294 DOWN-LONG 1

6 Singapore 1.357 ↔

7 Portugal 1.371 UP-LONG 1

8 Denmark 1.393 DOWN-LONG 1

9 Slovenia 1.409 ↔

10 Finland 1.420 UP-LONG 1

11 Czechia 1.435 UP-LONG 2

12 Japan 1.440 UP-LONG 3

13 Malaysia 1.469 DOWN-LONG 1

=14 Netherlands 1.491 ↔

=14 Canada 1.491 DOWN-LONG 5

16 Belgium 1.492 UP-LONG 4

17 Hungary 1.500 DOWN-LONG 1

18 Australia 1.505 UP-LONG 1

19 Croatia 1.519 DOWN-LONG 1

20 Germany 1.533 DOWN-LONG 3

21 Bhutan 1.536 ↔

=22 Latvia 1.558 UP-LONG 5

=22 Lithuania 1.558 UP-LONG 5

24 Estonia 1.559 DOWN-LONG 2

25 Spain 1.578 ↔

26 Mauritius 1.586 DOWN-LONG 3

27 Qatar 1.593 DOWN-LONG 1

28 Slovakia 1.609 UP-LONG 1

29 Bulgaria 1.610 UP-LONG 1

30 United Kingdom 1.634 UP-LONG 2

31 Kuwait 1.642 ↔

32 Norway 1.644 DOWN-LONG 8

33 Italy 1.662 UP-LONG 1

34 Montenegro 1.685 UP-LONG 5

35 Sweden 1.709 DOWN-LONG 2

36 Poland 1.713 DOWN-LONG 1

37 Mongolia 1.719 UP-LONG 8

=38 Romania 1.721 DOWN-LONG 2

=38 Vietnam 1.721 UP-LONG 1

40 Taiwan 1.730 DOWN-LONG 2

41 South Korea 1.736 UP-LONG 2

42 Oman 1.738 DOWN-LONG 5

43 Botswana 1.743 DOWN-LONG 2

44 Timor-Leste 1.758 UP-LONG 5

45 Greece 1.764 DOWN-LONG 3

46 Argentina 1.768 UP-LONG 5

47 Laos 1.783 DOWN-LONG 3

48 Uruguay 1.784 ↔

49 Indonesia 1.786 UP-LONG 3

50 Namibia 1.789 UP-LONG 4

51 North Macedonia 1.799 DOWN-LONG 4

=52 Albania 1.812 DOWN-LONG 6

=52 United Arab Emirates 1.812 UP-LONG 2

54 Costa Rica 1.843 DOWN-LONG 4

55 The Gambia 1.855 UP-LONG 16

56 Kazakhstan 1.875 UP-LONG 5

57 Sierra Leone 1.887 UP-LONG 2

58 Armenia 1.893 UP-LONG 10

=59 Madagascar 1.895 DOWN-LONG 6

=59

Bosnia and

Herzegovina

1.895 DOWN-LONG 3

61 Ghana 1.898 DOWN-LONG 3

62 Chile 1.899 ↔

63 Kosovo 1.908 DOWN-LONG 3

=64 Serbia 1.914 DOWN-LONG 1

=64 Zambia 1.914 DOWN-LONG 9

66 Moldova 1.918 DOWN-LONG 2

67 Uzbekistan 1.926 UP-LONG 2

68 Cyprus 1.933 DOWN-LONG 1

69 Senegal 1.936 UP-LONG 5

70 Liberia 1.939 UP-LONG 6

71 Malawi 1.955 UP-LONG 14

72 Jordan 1.957 DOWN-LONG 2

73 Tanzania 1.965 DOWN-LONG 8

74 France 1.967 UP-LONG 5

75 Paraguay 1.981 UP-LONG 2

=76 Nepal 1.987 UP-LONG 8

=76 Angola 1.987 DOWN-LONG 11

78 Kyrgyz Republic 1.988 UP-LONG 5

=79 Tajikistan 1.996 UP-LONG 10

=79 Dominican Republic 1.996 UP-LONG 6

81 Tunisia 1.998 DOWN-LONG 3

82 Equatorial Guinea 2.004 UP-LONG 15

83 Bolivia 2.005 DOWN-LONG 10

2025

Global

Peace Index

A snapshot of the global state of peace

THE STATE OF PEACE

NOT INCLUDED

VERY HIGH HIGH MEDIUM LOW VERY LOW

RANK COUNTRY SCORE CHANGE

RANK COUNTRY SCORE CHANGE

RANK COUNTRY SCORE CHANGE

Global Peace Index 2025 | Measuring peace in a complex world

8

11.

RANK COUNTRY SCORECHANGE RANK COUNTRY SCORE CHANGE RANK COUNTRY SCORE CHANGE

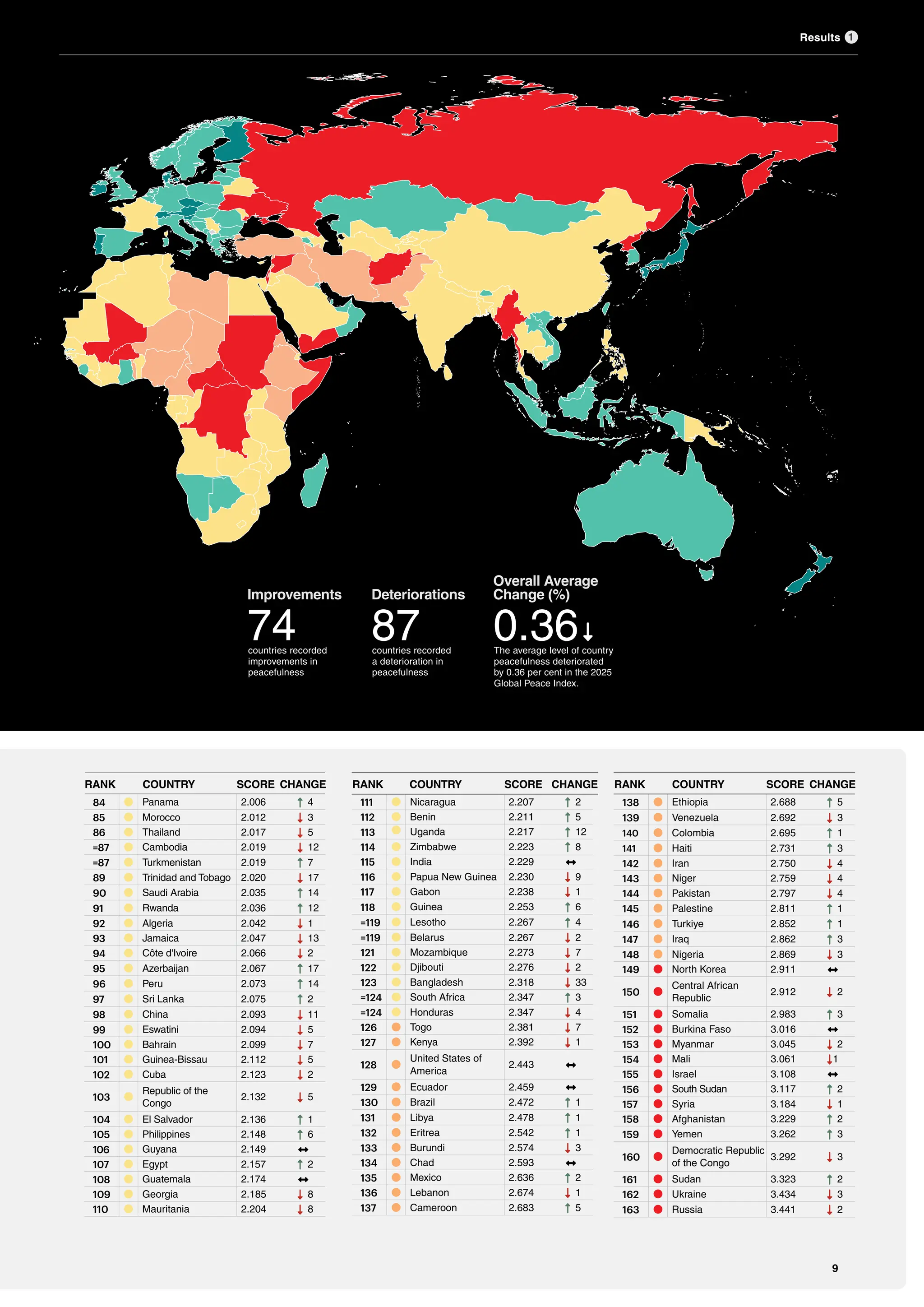

84 Panama 2.006 UP-LONG 4

85 Morocco 2.012 DOWN-LONG 3

86 Thailand 2.017 DOWN-LONG 5

=87 Cambodia 2.019 DOWN-LONG 12

=87 Turkmenistan 2.019 UP-LONG 7

89 Trinidad and Tobago 2.020 DOWN-LONG 17

90 Saudi Arabia 2.035 UP-LONG 14

91 Rwanda 2.036 UP-LONG 12

92 Algeria 2.042 DOWN-LONG 1

93 Jamaica 2.047 DOWN-LONG 13

94 Côte d'Ivoire 2.066 DOWN-LONG 2

95 Azerbaijan 2.067 UP-LONG 17

96 Peru 2.073 UP-LONG 14

97 Sri Lanka 2.075 UP-LONG 2

98 China 2.093 DOWN-LONG 11

99 Eswatini 2.094 DOWN-LONG 5

100 Bahrain 2.099 DOWN-LONG 7

101 Guinea-Bissau 2.112 DOWN-LONG 5

102 Cuba 2.123 DOWN-LONG 2

103

Republic of the

Congo

2.132 DOWN-LONG 5

104 El Salvador 2.136 UP-LONG 1

105 Philippines 2.148 UP-LONG 6

106 Guyana 2.149 ↔

107 Egypt 2.157 UP-LONG 2

108 Guatemala 2.174 ↔

109 Georgia 2.185 DOWN-LONG 8

110 Mauritania 2.204 DOWN-LONG 8

111 Nicaragua 2.207 UP-LONG 2

112 Benin 2.211 UP-LONG 5

113 Uganda 2.217 UP-LONG 12

114 Zimbabwe 2.223 UP-LONG 8

115 India 2.229 ↔

116 Papua New Guinea 2.230 DOWN-LONG 9

117 Gabon 2.238 DOWN-LONG 1

118 Guinea 2.253 UP-LONG 6

=119 Lesotho 2.267 UP-LONG 4

=119 Belarus 2.267 DOWN-LONG 2

121 Mozambique 2.273 DOWN-LONG 7

122 Djibouti 2.276 DOWN-LONG 2

123 Bangladesh 2.318 DOWN-LONG 33

=124 South Africa 2.347 UP-LONG 3

=124 Honduras 2.347 DOWN-LONG 4

126 Togo 2.381 DOWN-LONG 7

127 Kenya 2.392 DOWN-LONG 1

128

United States of

America

2.443 ↔

129 Ecuador 2.459 ↔

130 Brazil 2.472 UP-LONG 1

131 Libya 2.478 UP-LONG 1

132 Eritrea 2.542 UP-LONG 1

133 Burundi 2.574 DOWN-LONG 3

134 Chad 2.593 ↔

135 Mexico 2.636 UP-LONG 2

136 Lebanon 2.674 DOWN-LONG 1

137 Cameroon 2.683 UP-LONG 5

138 Ethiopia 2.688 UP-LONG 5

139 Venezuela 2.692 DOWN-LONG 3

140 Colombia 2.695 UP-LONG 1

141 Haiti 2.731 UP-LONG 3

142 Iran 2.750 DOWN-LONG 4

143 Niger 2.759 DOWN-LONG 4

144 Pakistan 2.797 DOWN-LONG 4

145 Palestine 2.811 UP-LONG 1

146 Turkiye 2.852 UP-LONG 1

147 Iraq 2.862 UP-LONG 3

148 Nigeria 2.869 DOWN-LONG 3

149 North Korea 2.911 ↔

150

Central African

Republic

2.912 DOWN-LONG 2

151 Somalia 2.983 UP-LONG 3

152 Burkina Faso 3.016 ↔

153 Myanmar 3.045 DOWN-LONG 2

154 Mali 3.061 DOWN-LONG1

155 Israel 3.108 ↔

156 South Sudan 3.117 UP-LONG 2

157 Syria 3.184 DOWN-LONG 1

158 Afghanistan 3.229 UP-LONG 2

159 Yemen 3.262 UP-LONG 3

160

Democratic Republic

of the Congo

3.292 DOWN-LONG 3

161 Sudan 3.323 UP-LONG 2

162 Ukraine 3.434 DOWN-LONG 3

163 Russia 3.441 DOWN-LONG 2

74

countries recorded

improvements in

peacefulness

Improvements

87

countries recorded

a deterioration in

peacefulness

Deteriorations

0.36

The average level of country

peacefulness deteriorated

by 0.36 per cent in the 2025

Global Peace Index.

Overall Average

Change (%)

9

1

Results

UP-LONG

12.

10

Global Peace Index2025 | Measuring peace in a complex world Results

Results

The 2025 GPI finds that the world became less peaceful for the 13th

time in the last 17 years, with the

average level of country peacefulness deteriorating by 0.36 per cent over the prior year. This is the sixth

consecutive year that global peacefulness has deteriorated. Figure 1.1 shows the change in the average

levels of peacefulness for each of the GPI domains, as well as the percentage of countries that improved

or deteriorated. In total, peacefulness improved in 74 countries and deteriorated in 87.

FIGURE 1.1

Year-on-year change in GPI score by domain,

2025

Safety and Security was the only domain to record an

improvement.

-0.01 0.00 0.01 0.02

CHANGE

IN

SCORE

Source: IEP

Safety and Security

Overall Score

Militarisation

Ongoing Conflict

Perceptions of Criminality

Violent Demonstrations

Political Terror Scale

Armed Services Personnel Rate

Homicide Rate

Police Rate

Nuclear and Heavy Weapons

Political Instability

Access to Small Arms

Intensity of Internal Conflict

Incarceration Rate

Terrorism Impact

Refugees and IDPs

UN Peacekeeping Funding

Neighbouring Countries Relations

Violent Crime

Internal Conflicts Fought

Weapons Exports

Deaths From External Conflict

Weapons Imports

Military Expenditure (% GDP)

Deaths From Internal Conflict

External Conflicts Fought

-2% 0% 2%

% CHANGE IN AVERAGE SCORE

Source: IEP

Improvement Deterioration

The Ongoing Conflict domain recorded the largest deterioration,

with the average score on the domain deteriorating by 1.3 per

cent. While most attention has been focused on the wars in

Gaza and Ukraine, conflict remains widespread across the

globe, with 78 countries recording a deterioration from the 2024

to the 2025 GPI. The main driver of rising Ongoing Conflict was

an increase in the number of external conflicts fought, with 46

countries experiencing more external conflict this year than last

year. The biggest deteriorations on this domain occurred in

Russia, Bangladesh and Ukraine. Every indicator on the

Ongoing Conflict domain deteriorated on average, apart from

intensity of internal conflict, which recorded no change.

The Militarisation domain continued to deteriorate over the

past year, with 86 countries recording deteriorations. Average

military expenditure as a percentage of GDP reached its highest

level since 2010, increasing by 2.5 per cent over the past year.

Norway, Denmark and Bangladesh recorded the largest

deteriorations on the Militarisation domain in 2025. The

deterioration on this domain is a reversal of the trend seen for

much of the past 15 years, as many countries have begun to

move towards higher levels of military spending given the

increase in conflict and geopolitical unrest across the globe.

FIGURE 1.2

Percentage change in score by indicator, 2024–2025

Thirteen of the 23 GPI indicators recorded an improvement over the past year.

13.

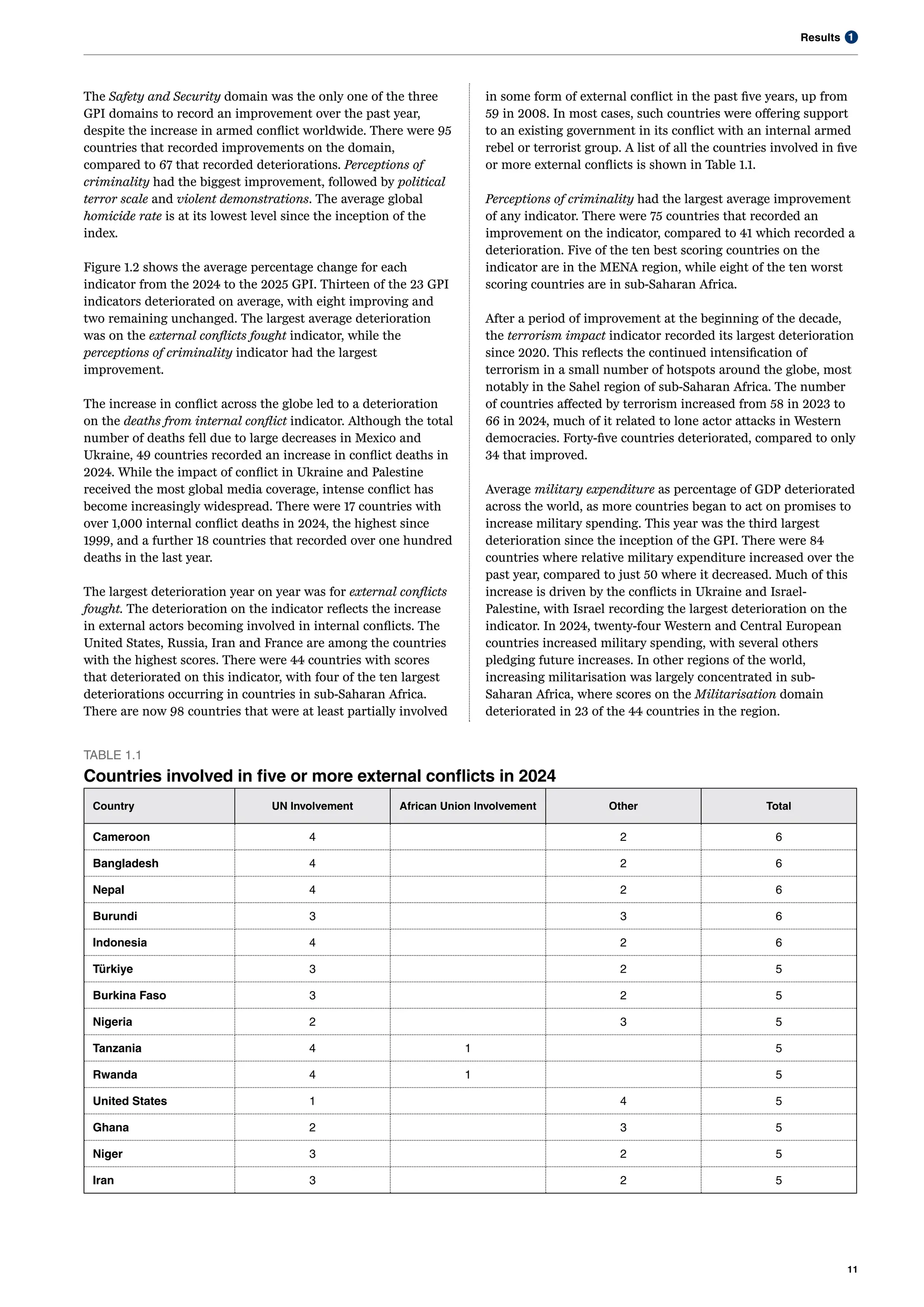

1

Results

11

The Safety andSecurity domain was the only one of the three

GPI domains to record an improvement over the past year,

despite the increase in armed conflict worldwide. There were 95

countries that recorded improvements on the domain,

compared to 67 that recorded deteriorations. Perceptions of

criminality had the biggest improvement, followed by political

terror scale and violent demonstrations. The average global

homicide rate is at its lowest level since the inception of the

index.

Figure 1.2 shows the average percentage change for each

indicator from the 2024 to the 2025 GPI. Thirteen of the 23 GPI

indicators deteriorated on average, with eight improving and

two remaining unchanged. The largest average deterioration

was on the external conflicts fought indicator, while the

perceptions of criminality indicator had the largest

improvement.

The increase in conflict across the globe led to a deterioration

on the deaths from internal conflict indicator. Although the total

number of deaths fell due to large decreases in Mexico and

Ukraine, 49 countries recorded an increase in conflict deaths in

2024. While the impact of conflict in Ukraine and Palestine

received the most global media coverage, intense conflict has

become increasingly widespread. There were 17 countries with

over 1,000 internal conflict deaths in 2024, the highest since

1999, and a further 18 countries that recorded over one hundred

deaths in the last year.

The largest deterioration year on year was for external conflicts

fought. The deterioration on the indicator reflects the increase

in external actors becoming involved in internal conflicts. The

United States, Russia, Iran and France are among the countries

with the highest scores. There were 44 countries with scores

that deteriorated on this indicator, with four of the ten largest

deteriorations occurring in countries in sub-Saharan Africa.

There are now 98 countries that were at least partially involved

in some form of external conflict in the past five years, up from

59 in 2008. In most cases, such countries were offering support

to an existing government in its conflict with an internal armed

rebel or terrorist group. A list of all the countries involved in five

or more external conflicts is shown in Table 1.1.

TABLE 1.1

Countries involved in five or more external conflicts in 2024

Country UN Involvement African Union Involvement Other Total

Cameroon 4 2 6

Bangladesh 4 2 6

Nepal 4 2 6

Burundi 3 3 6

Indonesia 4 2 6

Türkiye 3 2 5

Burkina Faso 3 2 5

Nigeria 2 3 5

Tanzania 4 1 5

Rwanda 4 1 5

United States 1 4 5

Ghana 2 3 5

Niger 3 2 5

Iran 3 2 5

Perceptions of criminality had the largest average improvement

of any indicator. There were 75 countries that recorded an

improvement on the indicator, compared to 41 which recorded a

deterioration. Five of the ten best scoring countries on the

indicator are in the MENA region, while eight of the ten worst

scoring countries are in sub-Saharan Africa.

After a period of improvement at the beginning of the decade,

the terrorism impact indicator recorded its largest deterioration

since 2020. This reflects the continued intensification of

terrorism in a small number of hotspots around the globe, most

notably in the Sahel region of sub-Saharan Africa. The number

of countries affected by terrorism increased from 58 in 2023 to

66 in 2024, much of it related to lone actor attacks in Western

democracies. Forty-five countries deteriorated, compared to only

34 that improved.

Average military expenditure as percentage of GDP deteriorated

across the world, as more countries began to act on promises to

increase military spending. This year was the third largest

deterioration since the inception of the GPI. There were 84

countries where relative military expenditure increased over the

past year, compared to just 50 where it decreased. Much of this

increase is driven by the conflicts in Ukraine and Israel-

Palestine, with Israel recording the largest deterioration on the

indicator. In 2024, twenty-four Western and Central European

countries increased military spending, with several others

pledging future increases. In other regions of the world,

increasing militarisation was largely concentrated in sub-

Saharan Africa, where scores on the Militarisation domain

deteriorated in 23 of the 44 countries in the region.

14.

12

Global Peace Index2025 | Measuring peace in a complex world

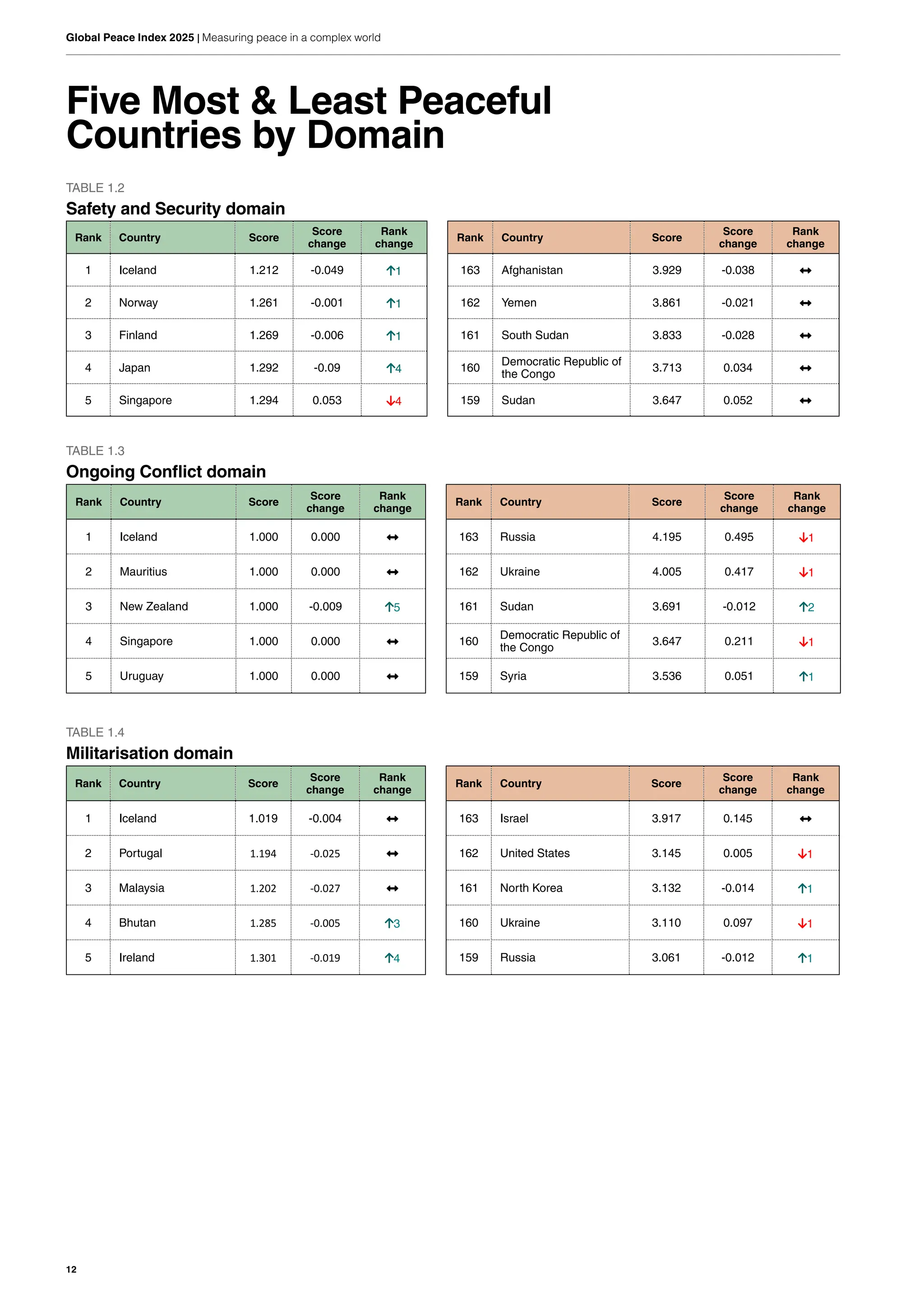

Five Most & Least Peaceful

Countries by Domain

TABLE 1.2

Safety and Security domain

Rank Country Score

Score

change

Rank

change

Rank Country Score

Score

change

Rank

change

1 Iceland 1.212 -0.049 ↑1 163 Afghanistan 3.929 -0.038 ↔

2 Norway 1.261 -0.001 ↑1 162 Yemen 3.861 -0.021 ↔

3 Finland 1.269 -0.006 ↑1 161 South Sudan 3.833 -0.028 ↔

4 Japan 1.292 -0.09 ↑4 160

Democratic Republic of

the Congo

3.713 0.034 ↔

5 Singapore 1.294 0.053 ↓4 159 Sudan 3.647 0.052 ↔

TABLE 1.3

Ongoing Conflict domain

Rank Country Score

Score

change

Rank

change

Rank Country Score

Score

change

Rank

change

1 Iceland 1.000 0.000 ↔ 163 Russia 4.195 0.495 ↓1

2 Mauritius 1.000 0.000 ↔ 162 Ukraine 4.005 0.417 ↓1

3 New Zealand 1.000 -0.009 ↑5 161 Sudan 3.691 -0.012 ↑2

4 Singapore 1.000 0.000 ↔ 160

Democratic Republic of

the Congo

3.647 0.211 ↓1

5 Uruguay 1.000 0.000 ↔ 159 Syria 3.536 0.051 ↑1

TABLE 1.4

Militarisation domain

Rank Country Score

Score

change

Rank

change

Rank Country Score

Score

change

Rank

change

1 Iceland 1.019 -0.004 ↔ 163 Israel 3.917 0.145 ↔

2 Portugal 1.194 -0.025 ↔ 162 United States 3.145 0.005 ↓1

3 Malaysia 1.202 -0.027 ↔ 161 North Korea 3.132 -0.014 ↑1

4 Bhutan 1.285 -0.005 ↑3 160 Ukraine 3.110 0.097 ↓1

5 Ireland 1.301 -0.019 ↑4 159 Russia 3.061 -0.012 ↑1

15.

1

Results

13

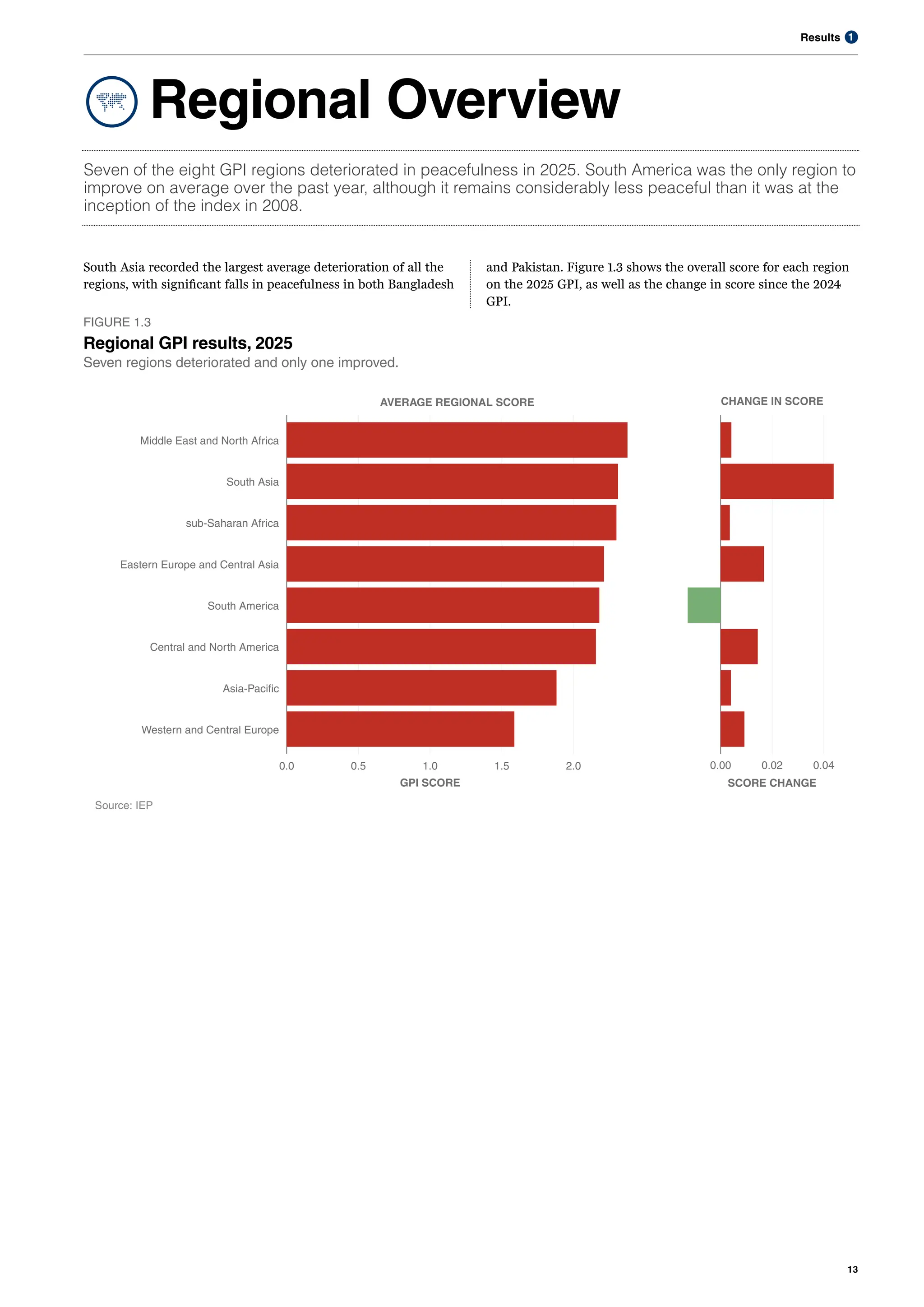

Regional Overview

Seven ofthe eight GPI regions deteriorated in peacefulness in 2025. South America was the only region to

improve on average over the past year, although it remains considerably less peaceful than it was at the

inception of the index in 2008.

South Asia recorded the largest average deterioration of all the

regions, with significant falls in peacefulness in both Bangladesh

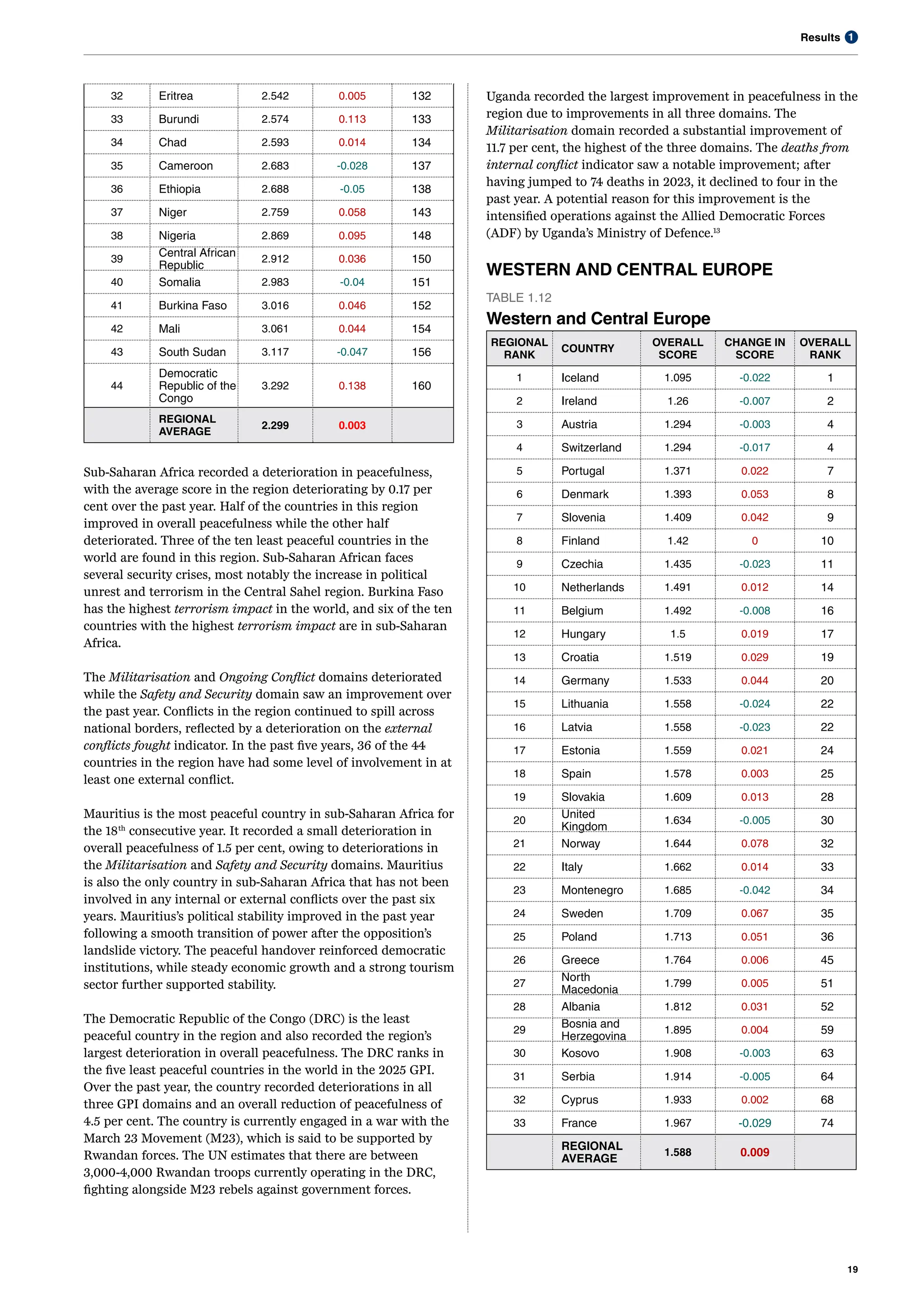

Western and Central Europe

Asia-Pacific

Central and North America

South America

Eastern Europe and Central Asia

sub-Saharan Africa

South Asia

Middle East and North Africa

0.0 0.5 1.0 1.5 2.0

GPI SCORE

AVERAGE REGIONAL SCORE

Source: IEP

0.00 0.02 0.04

SCORE CHANGE

CHANGE IN SCORE

FIGURE 1.3

Regional GPI results, 2025

Seven regions deteriorated and only one improved.

and Pakistan. Figure 1.3 shows the overall score for each region

on the 2025 GPI, as well as the change in score since the 2024

GPI.

16.

14

Global Peace Index2025 | Measuring peace in a complex world

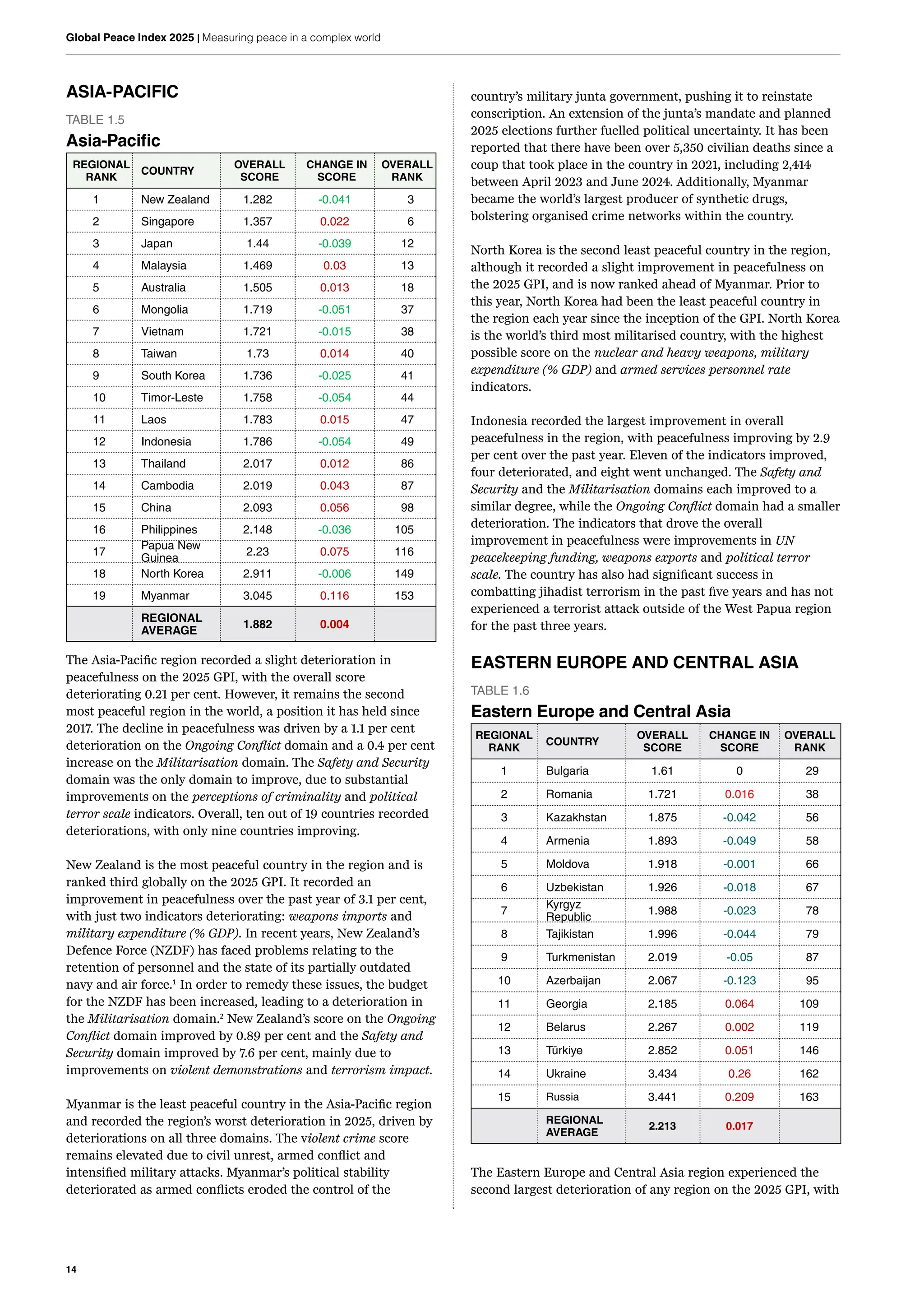

ASIA-PACIFIC

TABLE 1.5

Asia-Pacific

REGIONAL

RANK

COUNTRY

OVERALL

SCORE

CHANGE IN

SCORE

OVERALL

RANK

1 New Zealand 1.282 -0.041 3

2 Singapore 1.357 0.022 6

3 Japan 1.44 -0.039 12

4 Malaysia 1.469 0.03 13

5 Australia 1.505 0.013 18

6 Mongolia 1.719 -0.051 37

7 Vietnam 1.721 -0.015 38

8 Taiwan 1.73 0.014 40

9 South Korea 1.736 -0.025 41

10 Timor-Leste 1.758 -0.054 44

11 Laos 1.783 0.015 47

12 Indonesia 1.786 -0.054 49

13 Thailand 2.017 0.012 86

14 Cambodia 2.019 0.043 87

15 China 2.093 0.056 98

16 Philippines 2.148 -0.036 105

17

Papua New

Guinea

2.23 0.075 116

18 North Korea 2.911 -0.006 149

19 Myanmar 3.045 0.116 153

REGIONAL

AVERAGE

1.882 0.004

The Asia-Pacific region recorded a slight deterioration in

peacefulness on the 2025 GPI, with the overall score

deteriorating 0.21 per cent. However, it remains the second

most peaceful region in the world, a position it has held since

2017. The decline in peacefulness was driven by a 1.1 per cent

deterioration on the Ongoing Conflict domain and a 0.4 per cent

increase on the Militarisation domain. The Safety and Security

domain was the only domain to improve, due to substantial

improvements on the perceptions of criminality and political

terror scale indicators. Overall, ten out of 19 countries recorded

deteriorations, with only nine countries improving.

New Zealand is the most peaceful country in the region and is

ranked third globally on the 2025 GPI. It recorded an

improvement in peacefulness over the past year of 3.1 per cent,

with just two indicators deteriorating: weapons imports and

military expenditure (% GDP). In recent years, New Zealand’s

Defence Force (NZDF) has faced problems relating to the

retention of personnel and the state of its partially outdated

navy and air force.1

In order to remedy these issues, the budget

for the NZDF has been increased, leading to a deterioration in

the Militarisation domain.2

New Zealand’s score on the Ongoing

Conflict domain improved by 0.89 per cent and the Safety and

Security domain improved by 7.6 per cent, mainly due to

improvements on violent demonstrations and terrorism impact.

Myanmar is the least peaceful country in the Asia-Pacific region

and recorded the region’s worst deterioration in 2025, driven by

deteriorations on all three domains. The violent crime score

remains elevated due to civil unrest, armed conflict and

intensified military attacks. Myanmar’s political stability

deteriorated as armed conflicts eroded the control of the

country’s military junta government, pushing it to reinstate

conscription. An extension of the junta’s mandate and planned

2025 elections further fuelled political uncertainty. It has been

reported that there have been over 5,350 civilian deaths since a

coup that took place in the country in 2021, including 2,414

between April 2023 and June 2024. Additionally, Myanmar

became the world’s largest producer of synthetic drugs,

bolstering organised crime networks within the country.

North Korea is the second least peaceful country in the region,

although it recorded a slight improvement in peacefulness on

the 2025 GPI, and is now ranked ahead of Myanmar. Prior to

this year, North Korea had been the least peaceful country in

the region each year since the inception of the GPI. North Korea

is the world’s third most militarised country, with the highest

possible score on the nuclear and heavy weapons, military

expenditure (% GDP) and armed services personnel rate

indicators.

Indonesia recorded the largest improvement in overall

peacefulness in the region, with peacefulness improving by 2.9

per cent over the past year. Eleven of the indicators improved,

four deteriorated, and eight went unchanged. The Safety and

Security and the Militarisation domains each improved to a

similar degree, while the Ongoing Conflict domain had a smaller

deterioration. The indicators that drove the overall

improvement in peacefulness were improvements in UN

peacekeeping funding, weapons exports and political terror

scale. The country has also had significant success in

combatting jihadist terrorism in the past five years and has not

experienced a terrorist attack outside of the West Papua region

for the past three years.

EASTERN EUROPE AND CENTRAL ASIA

TABLE 1.6

Eastern Europe and Central Asia

REGIONAL

RANK

COUNTRY

OVERALL

SCORE

CHANGE IN

SCORE

OVERALL

RANK

1 Bulgaria 1.61 0 29

2 Romania 1.721 0.016 38

3 Kazakhstan 1.875 -0.042 56

4 Armenia 1.893 -0.049 58

5 Moldova 1.918 -0.001 66

6 Uzbekistan 1.926 -0.018 67

7

Kyrgyz

Republic

1.988 -0.023 78

8 Tajikistan 1.996 -0.044 79

9 Turkmenistan 2.019 -0.05 87

10 Azerbaijan 2.067 -0.123 95

11 Georgia 2.185 0.064 109

12 Belarus 2.267 0.002 119

13 Türkiye 2.852 0.051 146

14 Ukraine 3.434 0.26 162

15 Russia 3.441 0.209 163

REGIONAL

AVERAGE

2.213 0.017

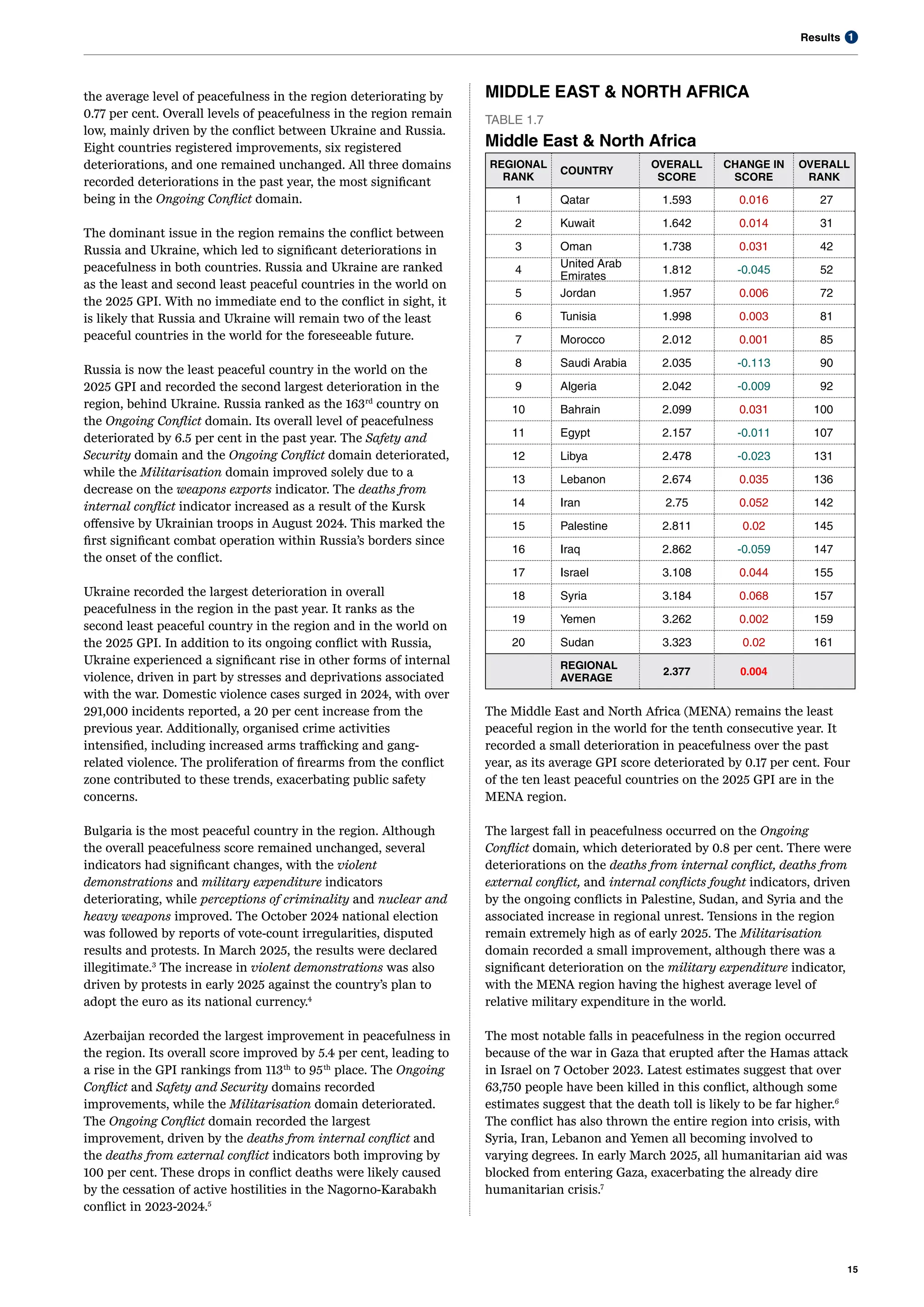

The Eastern Europe and Central Asia region experienced the

second largest deterioration of any region on the 2025 GPI, with

17.

1

Results

15

the average levelof peacefulness in the region deteriorating by

0.77 per cent. Overall levels of peacefulness in the region remain

low, mainly driven by the conflict between Ukraine and Russia.

Eight countries registered improvements, six registered

deteriorations, and one remained unchanged. All three domains

recorded deteriorations in the past year, the most significant

being in the Ongoing Conflict domain.

The dominant issue in the region remains the conflict between

Russia and Ukraine, which led to significant deteriorations in

peacefulness in both countries. Russia and Ukraine are ranked

as the least and second least peaceful countries in the world on

the 2025 GPI. With no immediate end to the conflict in sight, it

is likely that Russia and Ukraine will remain two of the least

peaceful countries in the world for the foreseeable future.

Russia is now the least peaceful country in the world on the

2025 GPI and recorded the second largest deterioration in the

region, behind Ukraine. Russia ranked as the 163rd

country on

the Ongoing Conflict domain. Its overall level of peacefulness

deteriorated by 6.5 per cent in the past year. The Safety and

Security domain and the Ongoing Conflict domain deteriorated,

while the Militarisation domain improved solely due to a

decrease on the weapons exports indicator. The deaths from

internal conflict indicator increased as a result of the Kursk

offensive by Ukrainian troops in August 2024. This marked the

first significant combat operation within Russia’s borders since

the onset of the conflict.

Ukraine recorded the largest deterioration in overall

peacefulness in the region in the past year. It ranks as the

second least peaceful country in the region and in the world on

the 2025 GPI. In addition to its ongoing conflict with Russia,

Ukraine experienced a significant rise in other forms of internal

violence, driven in part by stresses and deprivations associated

with the war. Domestic violence cases surged in 2024, with over

291,000 incidents reported, a 20 per cent increase from the

previous year. Additionally, organised crime activities

intensified, including increased arms trafficking and gang-

related violence. The proliferation of firearms from the conflict

zone contributed to these trends, exacerbating public safety

concerns.

Bulgaria is the most peaceful country in the region. Although

the overall peacefulness score remained unchanged, several

indicators had significant changes, with the violent

demonstrations and military expenditure indicators

deteriorating, while perceptions of criminality and nuclear and

heavy weapons improved. The October 2024 national election

was followed by reports of vote-count irregularities, disputed

results and protests. In March 2025, the results were declared

illegitimate.3

The increase in violent demonstrations was also

driven by protests in early 2025 against the country’s plan to

adopt the euro as its national currency.4

Azerbaijan recorded the largest improvement in peacefulness in

the region. Its overall score improved by 5.4 per cent, leading to

a rise in the GPI rankings from 113th

to 95th

place. The Ongoing

Conflict and Safety and Security domains recorded

improvements, while the Militarisation domain deteriorated.

The Ongoing Conflict domain recorded the largest

improvement, driven by the deaths from internal conflict and

the deaths from external conflict indicators both improving by

100 per cent. These drops in conflict deaths were likely caused

by the cessation of active hostilities in the Nagorno-Karabakh

conflict in 2023-2024.5

MIDDLE EAST & NORTH AFRICA

TABLE 1.7

Middle East & North Africa

REGIONAL

RANK

COUNTRY

OVERALL

SCORE

CHANGE IN

SCORE

OVERALL

RANK

1 Qatar 1.593 0.016 27

2 Kuwait 1.642 0.014 31

3 Oman 1.738 0.031 42

4

United Arab

Emirates

1.812 -0.045 52

5 Jordan 1.957 0.006 72

6 Tunisia 1.998 0.003 81

7 Morocco 2.012 0.001 85

8 Saudi Arabia 2.035 -0.113 90

9 Algeria 2.042 -0.009 92

10 Bahrain 2.099 0.031 100

11 Egypt 2.157 -0.011 107

12 Libya 2.478 -0.023 131

13 Lebanon 2.674 0.035 136

14 Iran 2.75 0.052 142

15 Palestine 2.811 0.02 145

16 Iraq 2.862 -0.059 147

17 Israel 3.108 0.044 155

18 Syria 3.184 0.068 157

19 Yemen 3.262 0.002 159

20 Sudan 3.323 0.02 161

REGIONAL

AVERAGE

2.377 0.004

The Middle East and North Africa (MENA) remains the least

peaceful region in the world for the tenth consecutive year. It

recorded a small deterioration in peacefulness over the past

year, as its average GPI score deteriorated by 0.17 per cent. Four

of the ten least peaceful countries on the 2025 GPI are in the

MENA region.

The largest fall in peacefulness occurred on the Ongoing

Conflict domain, which deteriorated by 0.8 per cent. There were

deteriorations on the deaths from internal conflict, deaths from

external conflict, and internal conflicts fought indicators, driven

by the ongoing conflicts in Palestine, Sudan, and Syria and the

associated increase in regional unrest. Tensions in the region

remain extremely high as of early 2025. The Militarisation

domain recorded a small improvement, although there was a

significant deterioration on the military expenditure indicator,

with the MENA region having the highest average level of

relative military expenditure in the world.

The most notable falls in peacefulness in the region occurred

because of the war in Gaza that erupted after the Hamas attack

in Israel on 7 October 2023. Latest estimates suggest that over

63,750 people have been killed in this conflict, although some

estimates suggest that the death toll is likely to be far higher.6

The conflict has also thrown the entire region into crisis, with

Syria, Iran, Lebanon and Yemen all becoming involved to

varying degrees. In early March 2025, all humanitarian aid was

blocked from entering Gaza, exacerbating the already dire

humanitarian crisis.7

18.

16

Global Peace Index2025 | Measuring peace in a complex world

Qatar is the most peaceful country in the MENA region, and the

27th

most peaceful country overall. It is one of the three countries

in the region that is ranked among the 50 most peaceful

countries in the world. However, it recorded a 0.99 per cent

deterioration in overall peacefulness in the past year. This was

driven by a deterioration on the Safety and Security domain,

because of deteriorating political instability. Political

uncertainty increased after a constitutional referendum

abolished legislative elections.

Sudan is the least peaceful country in the region and ranks as

the third least peaceful country overall on the 2025 GPI.

Peacefulness in Sudan fell by 0.54 per cent over the past year,

owing to substantial deteriorations on the nuclear and heavy

weapons, refugees and IDP and internal conflicts fought

indicators. Additionally, violent crime deteriorated largely due to

the ongoing civil war between the Sudanese Armed Forces (SAF)

and the paramilitary Rapid Support Forces (RSF). Conflict broke

out in April 2023 between the SAF and RSF after a plan was

proposed to dissolve the RSF and integrate it with the army. The

armed conflict has led to the displacement of millions of people,

with an estimated 6,800 deaths from internal conflict recorded

in 2024. The increasing civil unrest and lawlessness has meant

that humanitarian agencies and multilateral organisations are

unable to safely operate in most locations, including in the

capital city of Khartoum.

Saudi Arabia recorded the largest improvement in peacefulness

in the region, with improvements recorded across all three GPI

domains. The primary driver of the improvement in peacefulness

was a decrease on deaths from internal conflict, which recorded

an improvement of 100 per cent. Political stability improved as

the government’s Vision 2030 reforms and diplomatic outreach

strengthened governance and regional cooperation. The country

has restored ties with Lebanon and Iran, and it has served as a

mediating party in some international conflicts amid the

substantial geopolitical tensions in the region.

Syria recorded the largest deterioration in peacefulness in the

region and ranks in the ten least peaceful countries in the world

on the 2025 GPI. The decline in peacefulness over the past year

was driven by deteriorations on the Ongoing Conflict domain

and the Safety and Security domain. Violent demonstrations

significantly increased, as did deaths from internal conflict.

Recent figures estimate that since 2011, more than 14 million

Syrians have fled the country and 70 per cent of the population

needs humanitarian aid. In December 2024, the government of

Bashar al-Assad was overthrown after 24 years of rule. Since

then, more than one million Syrians have returned to Syria.8

A

new transitional government was sworn into power at the end of

March 2025.9

During the change of government, tensions rose

and fighting broke out over control of the Syria-Lebanese border,

but a ceasefire agreement between the two parties was reached

on 17 March 2025.10

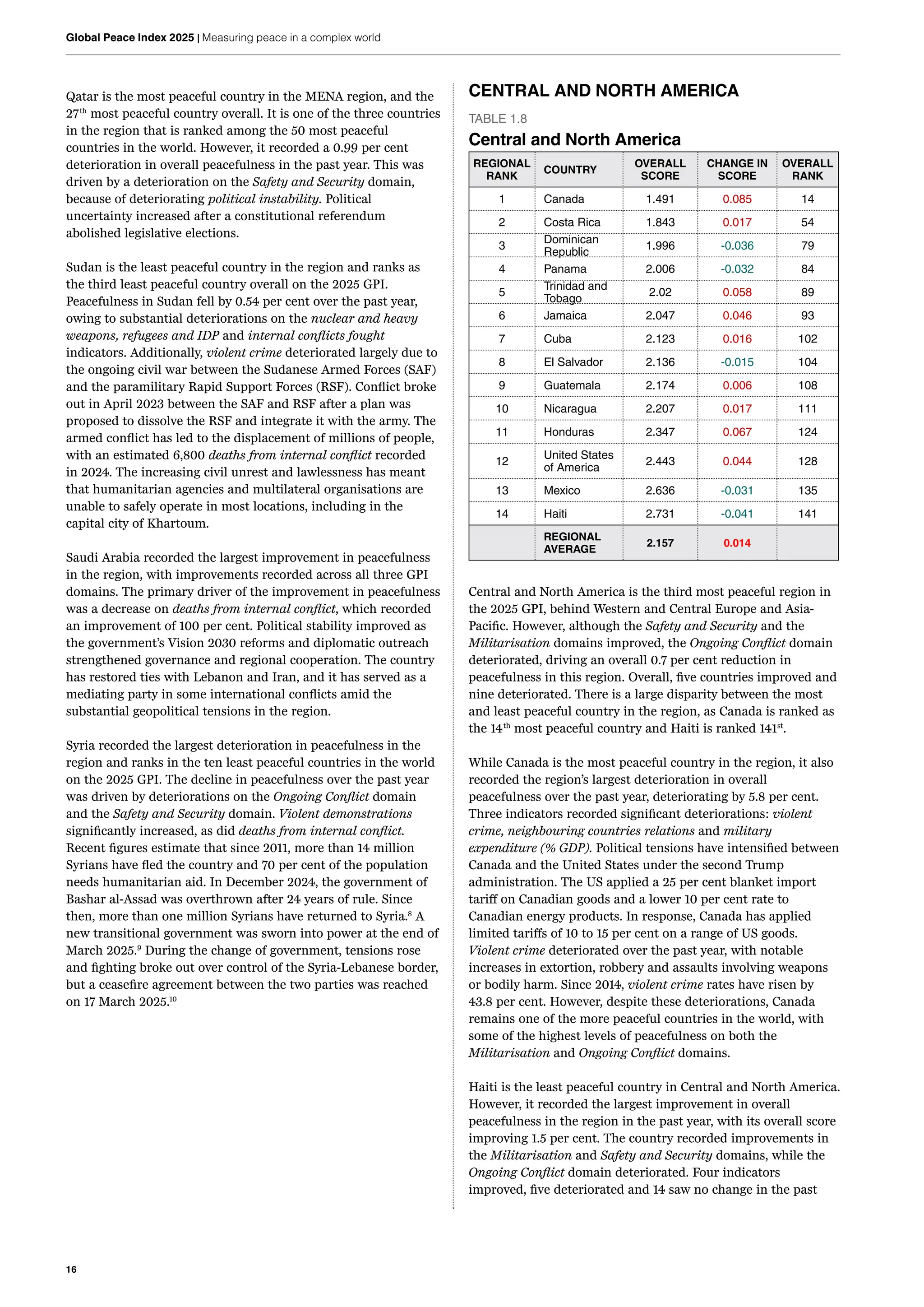

CENTRAL AND NORTH AMERICA

TABLE 1.8

Central and North America

REGIONAL

RANK

COUNTRY

OVERALL

SCORE

CHANGE IN

SCORE

OVERALL

RANK

1 Canada 1.491 0.085 14

2 Costa Rica 1.843 0.017 54

3

Dominican

Republic

1.996 -0.036 79

4 Panama 2.006 -0.032 84

5

Trinidad and

Tobago

2.02 0.058 89

6 Jamaica 2.047 0.046 93

7 Cuba 2.123 0.016 102

8 El Salvador 2.136 -0.015 104

9 Guatemala 2.174 0.006 108

10 Nicaragua 2.207 0.017 111

11 Honduras 2.347 0.067 124

12

United States

of America

2.443 0.044 128

13 Mexico 2.636 -0.031 135

14 Haiti 2.731 -0.041 141

REGIONAL

AVERAGE

2.157 0.014

Central and North America is the third most peaceful region in

the 2025 GPI, behind Western and Central Europe and Asia-

Pacific. However, although the Safety and Security and the

Militarisation domains improved, the Ongoing Conflict domain

deteriorated, driving an overall 0.7 per cent reduction in

peacefulness in this region. Overall, five countries improved and

nine deteriorated. There is a large disparity between the most

and least peaceful country in the region, as Canada is ranked as

the 14th

most peaceful country and Haiti is ranked 141st

.

While Canada is the most peaceful country in the region, it also

recorded the region’s largest deterioration in overall

peacefulness over the past year, deteriorating by 5.8 per cent.

Three indicators recorded significant deteriorations: violent

crime, neighbouring countries relations and military

expenditure (% GDP). Political tensions have intensified between

Canada and the United States under the second Trump

administration. The US applied a 25 per cent blanket import

tariff on Canadian goods and a lower 10 per cent rate to

Canadian energy products. In response, Canada has applied

limited tariffs of 10 to 15 per cent on a range of US goods.

Violent crime deteriorated over the past year, with notable

increases in extortion, robbery and assaults involving weapons

or bodily harm. Since 2014, violent crime rates have risen by

43.8 per cent. However, despite these deteriorations, Canada

remains one of the more peaceful countries in the world, with

some of the highest levels of peacefulness on both the

Militarisation and Ongoing Conflict domains.

Haiti is the least peaceful country in Central and North America.

However, it recorded the largest improvement in overall

peacefulness in the region in the past year, with its overall score

improving 1.5 per cent. The country recorded improvements in

the Militarisation and Safety and Security domains, while the

Ongoing Conflict domain deteriorated. Four indicators

improved, five deteriorated and 14 saw no change in the past

19.

1

Results

17

year. Haiti hasbeen in a state of crisis since 2021, when

president Jovenel Moïse was assassinated. Rates of violent crime

have soared amid rampant gang activity. However, Haiti's

political instability improved in the past year due to the

establishment of a Transitional Presidential Council in April

2024, to oversee governance until elections in 2026.

Additionally, the UN, led by Kenyan peacekeeping forces, helped

curb escalating gang violence that had previously paralysed

economic activities and displaced over 700,000 people. These

combined efforts have contributed to a modest stabilisation in

Haiti's political landscape.

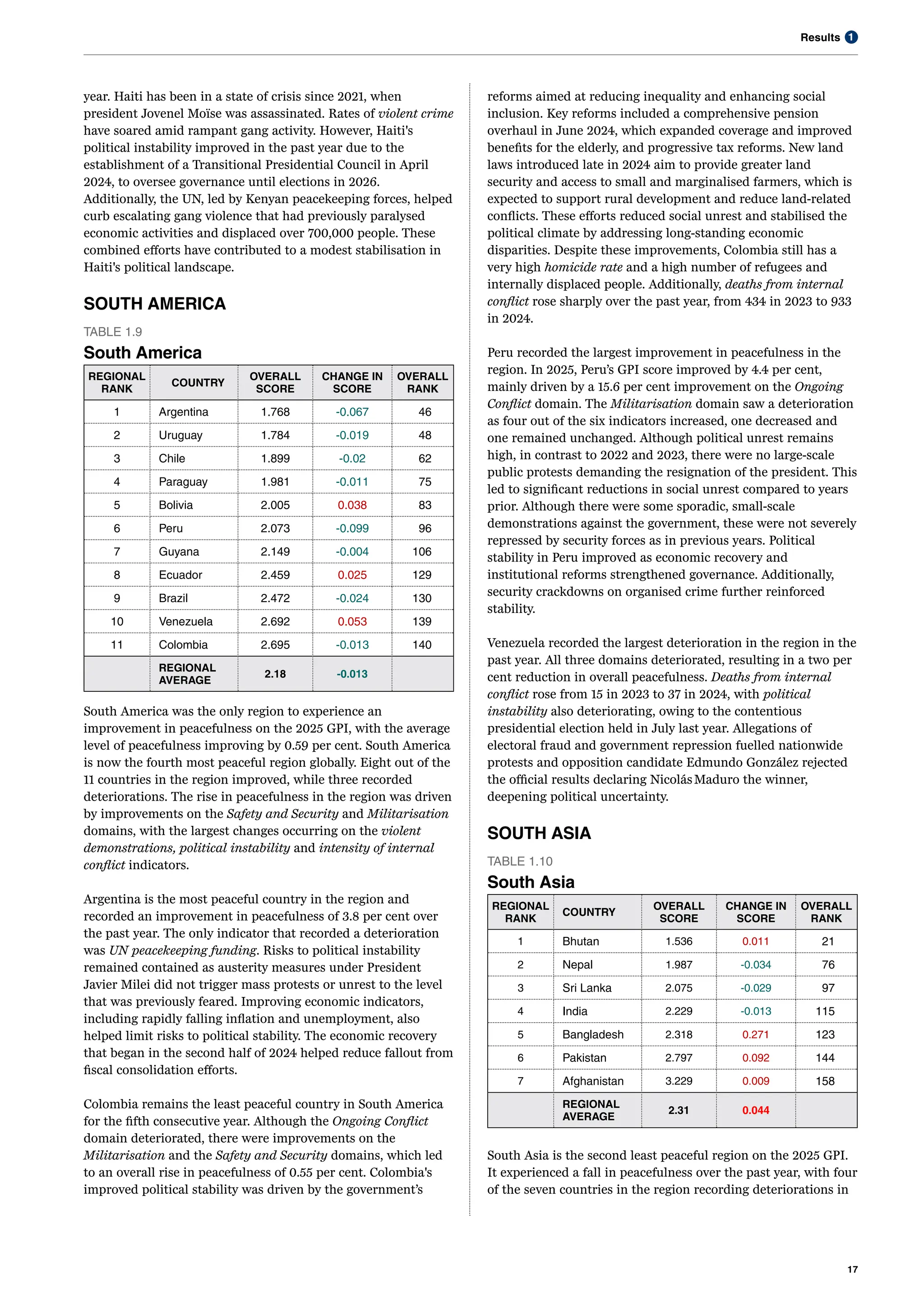

SOUTH AMERICA

TABLE 1.9

South America

REGIONAL

RANK

COUNTRY

OVERALL

SCORE

CHANGE IN

SCORE

OVERALL

RANK

1 Argentina 1.768 -0.067 46

2 Uruguay 1.784 -0.019 48

3 Chile 1.899 -0.02 62

4 Paraguay 1.981 -0.011 75

5 Bolivia 2.005 0.038 83

6 Peru 2.073 -0.099 96

7 Guyana 2.149 -0.004 106

8 Ecuador 2.459 0.025 129

9 Brazil 2.472 -0.024 130

10 Venezuela 2.692 0.053 139

11 Colombia 2.695 -0.013 140

REGIONAL

AVERAGE

2.18 -0.013

South America was the only region to experience an

improvement in peacefulness on the 2025 GPI, with the average

level of peacefulness improving by 0.59 per cent. South America

is now the fourth most peaceful region globally. Eight out of the

11 countries in the region improved, while three recorded

deteriorations. The rise in peacefulness in the region was driven

by improvements on the Safety and Security and Militarisation

domains, with the largest changes occurring on the violent

demonstrations, political instability and intensity of internal

conflict indicators.

Argentina is the most peaceful country in the region and

recorded an improvement in peacefulness of 3.8 per cent over

the past year. The only indicator that recorded a deterioration

was UN peacekeeping funding. Risks to political instability

remained contained as austerity measures under President

Javier Milei did not trigger mass protests or unrest to the level

that was previously feared. Improving economic indicators,

including rapidly falling inflation and unemployment, also

helped limit risks to political stability. The economic recovery

that began in the second half of 2024 helped reduce fallout from

fiscal consolidation efforts.

Colombia remains the least peaceful country in South America

for the fifth consecutive year. Although the Ongoing Conflict

domain deteriorated, there were improvements on the

Militarisation and the Safety and Security domains, which led

to an overall rise in peacefulness of 0.55 per cent. Colombia's

improved political stability was driven by the government’s

reforms aimed at reducing inequality and enhancing social

inclusion. Key reforms included a comprehensive pension

overhaul in June 2024, which expanded coverage and improved

benefits for the elderly, and progressive tax reforms. New land

laws introduced late in 2024 aim to provide greater land

security and access to small and marginalised farmers, which is

expected to support rural development and reduce land-related

conflicts. These efforts reduced social unrest and stabilised the

political climate by addressing long-standing economic

disparities. Despite these improvements, Colombia still has a

very high homicide rate and a high number of refugees and

internally displaced people. Additionally, deaths from internal

conflict rose sharply over the past year, from 434 in 2023 to 933

in 2024.

Peru recorded the largest improvement in peacefulness in the

region. In 2025, Peru’s GPI score improved by 4.4 per cent,

mainly driven by a 15.6 per cent improvement on the Ongoing

Conflict domain. The Militarisation domain saw a deterioration

as four out of the six indicators increased, one decreased and

one remained unchanged. Although political unrest remains

high, in contrast to 2022 and 2023, there were no large-scale

public protests demanding the resignation of the president. This

led to significant reductions in social unrest compared to years

prior. Although there were some sporadic, small-scale

demonstrations against the government, these were not severely

repressed by security forces as in previous years. Political

stability in Peru improved as economic recovery and

institutional reforms strengthened governance. Additionally,

security crackdowns on organised crime further reinforced

stability.

Venezuela recorded the largest deterioration in the region in the

past year. All three domains deteriorated, resulting in a two per

cent reduction in overall peacefulness. Deaths from internal

conflict rose from 15 in 2023 to 37 in 2024, with political

instability also deteriorating, owing to the contentious

presidential election held in July last year. Allegations of

electoral fraud and government repression fuelled nationwide

protests and opposition candidate Edmundo González rejected

the official results declaring NicolásMaduro the winner,

deepening political uncertainty.

SOUTH ASIA

TABLE 1.10

South Asia

REGIONAL

RANK

COUNTRY

OVERALL

SCORE

CHANGE IN

SCORE

OVERALL

RANK

1 Bhutan 1.536 0.011 21

2 Nepal 1.987 -0.034 76

3 Sri Lanka 2.075 -0.029 97

4 India 2.229 -0.013 115

5 Bangladesh 2.318 0.271 123

6 Pakistan 2.797 0.092 144

7 Afghanistan 3.229 0.009 158

REGIONAL

AVERAGE

2.31 0.044

South Asia is the second least peaceful region on the 2025 GPI.

It experienced a fall in peacefulness over the past year, with four

of the seven countries in the region recording deteriorations in

20.

18

Global Peace Index2025 | Measuring peace in a complex world

overall score. All three domains deteriorated, with the largest

change on the Ongoing Conflict domain, with a 4.9 per cent

increase due to none of the indicators in this domain improving

in the past year.

Afghanistan is the least peaceful country in the region, a

position it has held since the inception of the GPI. Afghanistan

ranks as the fifth least peaceful country in the world and has the

lowest ranking globally on the Safety and Security domain. In

the past year, peacefulness in Afghanistan deteriorated by 0.28

per cent. Afghanistan is the only country in the South Asia

region to have the worst possible scores on the access to small

arms, violent crimes, political instability, political terror scale,

refugees and IDPs and military expenditure (% GDP) indicators.

Although the level of conflict in Afghanistan has fallen since the

Taliban came to power, poor governance and humanitarian

crises are fuelling political unrest. In March 2025, the World

Health Organization in Afghanistan warned that funding

shortages may cause 80 per cent of the agency’s health services

there to close by June, exacerbating the health crisis already

present in the country.11

Nepal recorded the largest improvement in overall peacefulness

in South Asia, reversing the deterioration in peacefulness that

was seen in the prior year. The improvement over the past year

was mainly driven by an improvement on the Militarisation

domain, particularly due to a decline on weapons imports and

improved UN peacekeeping funding. Additionally, the terrorism

impact indicator recorded a substantial improvement over the

past year. Nepal has been increasing its focus on

counterterrorism in recent years, conducting joint military

exercises with India from late December 2024 to early January

2025 that focused on counterterrorism, jungle warfare and

operational skills.12

Bangladesh recorded the largest deterioration in peacefulness of

any country in the region and of any country on the 2025 GPI,

registering a 13 per cent reduction in overall peacefulness. It

recorded deteriorations on all domains, with the largest

occurring on the Ongoing Conflict domain. There were 436

deaths from internal conflicts, as compared to just 12 in the

previous year. Internal conflict in Bangladesh escalated as

student-led protests over government job quotas continued,

despite a Supreme Court ruling reducing them. Bangladesh

experienced a significant escalation in violent crime and

political instability. Attacks on minority communities also

escalated, with over 2,010 incidents recorded in August 2024.

Political violence surged, with an estimated 1,400 deaths linked

to clashes involving security forces and political groups.

Allegations of systematic extrajudicial killings further

undermined public trust in law enforcement. Bangladesh’s

political stability deteriorated in 2024 due to rising risks of

social unrest, opposition fragmentation, and security

crackdowns. Weeks of street protests, an opposition walk-out,

and a ruling-coalition split forced Bangladesh’s president to oust

the prime minister and draft Nobel laureate Dr Muhammad

Yunus as caretaker of an interim government. Yunus must now

pacify feuding parties and student groups, steady an economy

strained by forex shortages and food inflation, and rebuild trust

in a partisan election commission. High living costs and the