Download free for 30 days

Sign in

Upload

Language (EN)

Support

Business

Mobile

Social Media

Marketing

Technology

Art & Photos

Career

Design

Education

Presentations & Public Speaking

Government & Nonprofit

Healthcare

Internet

Law

Leadership & Management

Automotive

Engineering

Software

Recruiting & HR

Retail

Sales

Services

Science

Small Business & Entrepreneurship

Food

Environment

Economy & Finance

Data & Analytics

Investor Relations

Sports

Spiritual

News & Politics

Travel

Self Improvement

Real Estate

Entertainment & Humor

Health & Medicine

Devices & Hardware

Lifestyle

Change Language

Language

English

Español

Português

Français

Deutsche

Cancel

Save

Submit search

EN

Uploaded by

KeppelCorporation

9,879 views

Keppel Ltd. 1H 2025 Results Presentation Slides

31 July 2025

Business

◦

Read more

0

Save

Share

Embed

Embed presentation

Download

Downloaded 21 times

1

/ 56

2

/ 56

3

/ 56

4

/ 56

5

/ 56

6

/ 56

7

/ 56

8

/ 56

9

/ 56

10

/ 56

11

/ 56

12

/ 56

13

/ 56

14

/ 56

15

/ 56

16

/ 56

17

/ 56

18

/ 56

19

/ 56

20

/ 56

21

/ 56

22

/ 56

23

/ 56

24

/ 56

25

/ 56

26

/ 56

27

/ 56

28

/ 56

29

/ 56

30

/ 56

31

/ 56

32

/ 56

33

/ 56

34

/ 56

35

/ 56

36

/ 56

37

/ 56

38

/ 56

39

/ 56

40

/ 56

41

/ 56

Most read

42

/ 56

43

/ 56

44

/ 56

45

/ 56

46

/ 56

47

/ 56

48

/ 56

49

/ 56

50

/ 56

51

/ 56

52

/ 56

53

/ 56

54

/ 56

55

/ 56

Most read

56

/ 56

Most read

More Related Content

PDF

Keppel Ltd. 2H24 and FY24 Presentation Slides.pdf

by

KeppelCorporation

PPTX

Navigating a digital-first home furnishings market

by

L.E.K. Consulting

PPTX

The 4th Annual New Mobility Study 2019

by

L.E.K. Consulting

PDF

EY Price Point: global oil and gas market outlook

by

EY

PDF

Strategy Study 2014 | A.T. Kearney

by

Kearney

PDF

The Merchandising Evolution (and why NDC Matters)

by

L.E.K. Consulting

PDF

5 Opportunities in the Nutritional Supplements Industry

by

L.E.K. Consulting

PDF

China: Opportunities and Hot-Spots in the MedTech (Medical Device), Pharmaceu...

by

L.E.K. Consulting

Keppel Ltd. 2H24 and FY24 Presentation Slides.pdf

by

KeppelCorporation

Navigating a digital-first home furnishings market

by

L.E.K. Consulting

The 4th Annual New Mobility Study 2019

by

L.E.K. Consulting

EY Price Point: global oil and gas market outlook

by

EY

Strategy Study 2014 | A.T. Kearney

by

Kearney

The Merchandising Evolution (and why NDC Matters)

by

L.E.K. Consulting

5 Opportunities in the Nutritional Supplements Industry

by

L.E.K. Consulting

China: Opportunities and Hot-Spots in the MedTech (Medical Device), Pharmaceu...

by

L.E.K. Consulting

What's hot

PDF

Federal Technology Vision 2021: Full U.S. Federal Survey Findings | Accenture

by

accenture

PDF

Infrastructure Victoria - AZ/ZEV International Scan

by

L.E.K. Consulting

PDF

IBOR transition: Opportunities and challenges for the asset management industry

by

EY

PDF

Cracking the Code on Consumer Fraud | Accenture

by

accenture

PDF

e-Conomy SEA 2021: Kỷ nguyên số của Đông Nam Á

by

MarketingTrips

PDF

The Bionic Future - Future Work Summit

by

Miguel Carrasco

PDF

18th Annual Global CEO Survey - Technology industry key findings

by

PwC

PDF

Accenture Consumer Behavior Research: The value shake-up

by

accenture

PPTX

The FDA and industry: A recipe for collaborating in the New Health Economy

by

PwC

PDF

Australia: Taking Bigger Steps | A.T. Kearney

by

Kearney

PPTX

Joining Forces: Interagency Collaboration and "Smart Power"

by

Booz Allen Hamilton

PDF

EY Price Point: global oil and gas market outlook, Q2 | April 2022

by

EY

PPTX

BCG-Future-of-FMCG-Web-20201029-1.pptx

by

Self-Employed

PPTX

EY's European Banking Barometer – 2015

by

EY

PDF

Top 8 Insights From the 2018 Beauty, Health & Wellness Survey

by

L.E.K. Consulting

PDF

2019 Media and Entertainment Study

by

L.E.K. Consulting

PDF

2016 Strategic Hospital Priorities Study

by

L.E.K. Consulting

PDF

White Star Capital SEA 2022 Venture Capital Landscape

by

Sanjay Zimmermann

PDF

Quarterly analyst themes of oil and gas earnings, Q1 2022

by

EY

PPTX

Chad Cameroon pipeline Project Case study

by

Sharkhuu Munkhbat

Federal Technology Vision 2021: Full U.S. Federal Survey Findings | Accenture

by

accenture

Infrastructure Victoria - AZ/ZEV International Scan

by

L.E.K. Consulting

IBOR transition: Opportunities and challenges for the asset management industry

by

EY

Cracking the Code on Consumer Fraud | Accenture

by

accenture

e-Conomy SEA 2021: Kỷ nguyên số của Đông Nam Á

by

MarketingTrips

The Bionic Future - Future Work Summit

by

Miguel Carrasco

18th Annual Global CEO Survey - Technology industry key findings

by

PwC

Accenture Consumer Behavior Research: The value shake-up

by

accenture

The FDA and industry: A recipe for collaborating in the New Health Economy

by

PwC

Australia: Taking Bigger Steps | A.T. Kearney

by

Kearney

Joining Forces: Interagency Collaboration and "Smart Power"

by

Booz Allen Hamilton

EY Price Point: global oil and gas market outlook, Q2 | April 2022

by

EY

BCG-Future-of-FMCG-Web-20201029-1.pptx

by

Self-Employed

EY's European Banking Barometer – 2015

by

EY

Top 8 Insights From the 2018 Beauty, Health & Wellness Survey

by

L.E.K. Consulting

2019 Media and Entertainment Study

by

L.E.K. Consulting

2016 Strategic Hospital Priorities Study

by

L.E.K. Consulting

White Star Capital SEA 2022 Venture Capital Landscape

by

Sanjay Zimmermann

Quarterly analyst themes of oil and gas earnings, Q1 2022

by

EY

Chad Cameroon pipeline Project Case study

by

Sharkhuu Munkhbat

Similar to Keppel Ltd. 1H 2025 Results Presentation Slides

PDF

Keppel Ltd. 1Q 2025 Business Update Presentation Slides

by

KeppelCorporation

PDF

Keppel Investor Day 2024 Presentation Slides

by

KeppelCorporation

PDF

Annual General Meeting Presentation Slides

by

KeppelCorporation

PDF

Keppel Ltd. 9M 2025 Business Update Presentation Slides

by

KeppelCorporation

PDF

Keppel Corporation - Annual General Meeting CEO's Presentation Slides

by

KeppelCorporation

PDF

Keppel Corporation 1Q23 Business Update

by

KeppelCorporation

PDF

Keppel Ltd. 1Q 2024 Business Update Presentation Slides

by

KeppelCorporation

PDF

Keppel Corporation 2H & FY2022 Results Presentation Slides

by

KeppelCorporation

PDF

Keppel Investor Day 2025 Presentation Slides GCAT.pdf

by

KeppelCorporation

PDF

Keppel Corporation's 2H & FY 2021 Financial Results Presentation Slides

by

KeppelCorporation

PDF

Keppel Corporation 1H 2023 Financial Results Presentation

by

KeppelCorporation

PDF

Keppel Ltd. AGM 2025 CEO Presentation Slides

by

KeppelCorporation

PDF

Keppel-Ltd-2h23-fy23-presentation-slides

by

KeppelCorporation

PDF

Presentation Slides for HSBC Global Investment Summit

by

KeppelCorporation

PDF

Keppel Corporation's Vision 2030 Briefing to Analysts

by

KeppelCorporation

PDF

Keppel Corporation UK Non-deal Roadshow 2019

by

KeppelCorporation

PDF

Keppel's Presentation Slides to Investors

by

KeppelCorporation

PDF

2 keppel ltd 1h24 presentation slides.pdf

by

KeppelCorporation

PDF

Keppel Corporation - Briefing to media and analysts on accelerating transform...

by

KeppelCorporation

PDF

KCL_AR2016_Full_Report.pdf

by

leqhuy78

Keppel Ltd. 1Q 2025 Business Update Presentation Slides

by

KeppelCorporation

Keppel Investor Day 2024 Presentation Slides

by

KeppelCorporation

Annual General Meeting Presentation Slides

by

KeppelCorporation

Keppel Ltd. 9M 2025 Business Update Presentation Slides

by

KeppelCorporation

Keppel Corporation - Annual General Meeting CEO's Presentation Slides

by

KeppelCorporation

Keppel Corporation 1Q23 Business Update

by

KeppelCorporation

Keppel Ltd. 1Q 2024 Business Update Presentation Slides

by

KeppelCorporation

Keppel Corporation 2H & FY2022 Results Presentation Slides

by

KeppelCorporation

Keppel Investor Day 2025 Presentation Slides GCAT.pdf

by

KeppelCorporation

Keppel Corporation's 2H & FY 2021 Financial Results Presentation Slides

by

KeppelCorporation

Keppel Corporation 1H 2023 Financial Results Presentation

by

KeppelCorporation

Keppel Ltd. AGM 2025 CEO Presentation Slides

by

KeppelCorporation

Keppel-Ltd-2h23-fy23-presentation-slides

by

KeppelCorporation

Presentation Slides for HSBC Global Investment Summit

by

KeppelCorporation

Keppel Corporation's Vision 2030 Briefing to Analysts

by

KeppelCorporation

Keppel Corporation UK Non-deal Roadshow 2019

by

KeppelCorporation

Keppel's Presentation Slides to Investors

by

KeppelCorporation

2 keppel ltd 1h24 presentation slides.pdf

by

KeppelCorporation

Keppel Corporation - Briefing to media and analysts on accelerating transform...

by

KeppelCorporation

KCL_AR2016_Full_Report.pdf

by

leqhuy78

More from KeppelCorporation

PDF

Keppel Ltd. 3Q 2024 Business Update Presentation Slides

by

KeppelCorporation

PDF

Keppel Corporation AGM 2023 Presentation Slides

by

KeppelCorporation

PDF

Keppel Corporation's 1H22 Financial Results

by

KeppelCorporation

PDF

Keppel 3Q & 9M 2023 Business Update Presentation Slides

by

KeppelCorporation

PDF

Keppel Corporation's Presentation Slides for US Non-Deal Roadshow

by

KeppelCorporation

PDF

Keppel Corporation 3Q & 9M 2022 Business Update Presentation Slides

by

KeppelCorporation

PDF

keppel-ltd-3q-2024-business-update-presentation-slides.pdf

by

KeppelCorporation

PDF

Keppel Corporation non-deal roadshow slides

by

KeppelCorporation

PDF

SIAS-Keppel Briefing to Retail Shareholders 2023.pdf

by

KeppelCorporation

PDF

Presentation at Citi-SGX-REITAS REITs Sponsors Forum

by

KeppelCorporation

PDF

Keppel_Proposed Divestment of M1 Limited

by

KeppelCorporation

PDF

Presentation on proposed acquisition of leading European asset manager Aermon...

by

KeppelCorporation

PDF

Keppel Capital's Presentation Slides for REITs Symposium in Singapore

by

KeppelCorporation

PDF

Keppel Corporation signs definitive agreements in connection with proposed co...

by

KeppelCorporation

Keppel Ltd. 3Q 2024 Business Update Presentation Slides

by

KeppelCorporation

Keppel Corporation AGM 2023 Presentation Slides

by

KeppelCorporation

Keppel Corporation's 1H22 Financial Results

by

KeppelCorporation

Keppel 3Q & 9M 2023 Business Update Presentation Slides

by

KeppelCorporation

Keppel Corporation's Presentation Slides for US Non-Deal Roadshow

by

KeppelCorporation

Keppel Corporation 3Q & 9M 2022 Business Update Presentation Slides

by

KeppelCorporation

keppel-ltd-3q-2024-business-update-presentation-slides.pdf

by

KeppelCorporation

Keppel Corporation non-deal roadshow slides

by

KeppelCorporation

SIAS-Keppel Briefing to Retail Shareholders 2023.pdf

by

KeppelCorporation

Presentation at Citi-SGX-REITAS REITs Sponsors Forum

by

KeppelCorporation

Keppel_Proposed Divestment of M1 Limited

by

KeppelCorporation

Presentation on proposed acquisition of leading European asset manager Aermon...

by

KeppelCorporation

Keppel Capital's Presentation Slides for REITs Symposium in Singapore

by

KeppelCorporation

Keppel Corporation signs definitive agreements in connection with proposed co...

by

KeppelCorporation

Recently uploaded

PDF

How to Verify Your PayPal Account in 2025.pdf

by

5hb3cqye5o4j0o2dne3x

PDF

Lion One Corporate Presentation November 2025 Revised

by

Adnet Communications

PDF

Where to Buy LinkedIn Accounts_ [12 Best Sites] (3).pdf

by

a32sop3orzibld4x34e4

PDF

Strategic Thinking in Action: A conversation with Steven Haines

by

Cambridge Product Management Network

PDF

Top 5 Places to Buy Aged LinkedIn Accounts and Should ....pdf

by

5hb3cqye5o4j0o2dne3x

PDF

Humans cannot be transformed but we can help them - PLM Roadmap PDT Europe 20...

by

Jos Voskuil

PDF

How to Buy Verified Wise Accounts ,in 2025.pdf

by

a32sop3orzibld4x34e4

DOCX

7 Surprising Ways Metaverse Development Solutions Are Transforming Online Bus...

by

Ryan Wilson

PPTX

Shark Tank Project Presentation Sample 1.pptx

by

Abhishek436880

PDF

by Best Platforms to Buy Twitter Accounts in 2025.pdf

by

a32sop3orzibld4x34e4

PDF

How to Safely Buy Twitter Accounts A Complete Guide in ...pdf

by

usatrustacc5

PDF

Benefits of Buying Old GitHub Accounts for Your Projects

by

https://usashopcity.com/

PDF

Buy LinkedIn Connections _ Grow Your Network Fast.pdf

by

dubivgplc4wloha4rxsm

PDF

How To Safely Buy Instagram Accounts In 2025.pdf

by

dubivgplc4wloha4rxsm

PDF

Buy Verified PayPal Account A Complete Guide to Online Finance.pdf

by

Can I buy a verified Wise account?

PDF

The Most Recommended Commerce Colleges of the Year in 2025.pdf

by

EducationView

PDF

Where to Buy LinkedIn Accounts_ [12 Best Sites] (2).pdf

by

dubivgplc4wloha4rxsm

PDF

How do I subscribe to Snapchat in usa 2025+_.pdf

by

dubivgplc4wloha4rxsm

DOCX

Trusted Top Site to Buy Verified PayPal Account Online Finance.docx

by

Can I buy a verified Wise account?

PDF

HIROSHI BRYAN VO - A Bilingual Voice Actor

by

HIROSHI BRYAN VO

How to Verify Your PayPal Account in 2025.pdf

by

5hb3cqye5o4j0o2dne3x

Lion One Corporate Presentation November 2025 Revised

by

Adnet Communications

Where to Buy LinkedIn Accounts_ [12 Best Sites] (3).pdf

by

a32sop3orzibld4x34e4

Strategic Thinking in Action: A conversation with Steven Haines

by

Cambridge Product Management Network

Top 5 Places to Buy Aged LinkedIn Accounts and Should ....pdf

by

5hb3cqye5o4j0o2dne3x

Humans cannot be transformed but we can help them - PLM Roadmap PDT Europe 20...

by

Jos Voskuil

How to Buy Verified Wise Accounts ,in 2025.pdf

by

a32sop3orzibld4x34e4

7 Surprising Ways Metaverse Development Solutions Are Transforming Online Bus...

by

Ryan Wilson

Shark Tank Project Presentation Sample 1.pptx

by

Abhishek436880

by Best Platforms to Buy Twitter Accounts in 2025.pdf

by

a32sop3orzibld4x34e4

How to Safely Buy Twitter Accounts A Complete Guide in ...pdf

by

usatrustacc5

Benefits of Buying Old GitHub Accounts for Your Projects

by

https://usashopcity.com/

Buy LinkedIn Connections _ Grow Your Network Fast.pdf

by

dubivgplc4wloha4rxsm

How To Safely Buy Instagram Accounts In 2025.pdf

by

dubivgplc4wloha4rxsm

Buy Verified PayPal Account A Complete Guide to Online Finance.pdf

by

Can I buy a verified Wise account?

The Most Recommended Commerce Colleges of the Year in 2025.pdf

by

EducationView

Where to Buy LinkedIn Accounts_ [12 Best Sites] (2).pdf

by

dubivgplc4wloha4rxsm

How do I subscribe to Snapchat in usa 2025+_.pdf

by

dubivgplc4wloha4rxsm

Trusted Top Site to Buy Verified PayPal Account Online Finance.docx

by

Can I buy a verified Wise account?

HIROSHI BRYAN VO - A Bilingual Voice Actor

by

HIROSHI BRYAN VO

Keppel Ltd. 1H 2025 Results Presentation Slides

1.

1H 2025 Financial Results 31

July 2025

2.

© Keppel 2 Content 02 Financial highlights 03 Appendices 01 Address by

CEO

3.

Address by CEO 01 3

4.

4 Building on strong

momentum © Keppel • Performance improved significantly with disciplined execution and sharpened focus on growing FUM and recurring income with asset-light strategy • Trusted investment partner with $91b in FUMi as at end-Jun 2025 • Substantial headway pivoting to asset-light model, announced $7.8b in asset monetisation to date • Confident of achieving $100b FUM and $10-12b asset monetisation targets by end-2026 Keppel achieved strong results in 1H25, on the back of our transformation. i Gross asset value of investments and uninvested capital commitments on a leveraged basis is used to project fully-invested FUM.

5.

• Earnings of

the New Keppel currently funded by only a part of our balance sheet • Non-Core Portfolio for Divestmenti has been segregated to provide greater transparency on the New Keppel’s performance as an asset-light global asset manager and operator • Non-core portfolio had a carrying value of $14.4b as at end-Jun 2025 • Includes legacy O&M assets, residential landbank, selected property developments and investment properties, and embedded cash and receivables of $2.9b • Many non-core assets are profitable but are not part of the New Keppel’s core business and strategy of being asset-light and recurring income-focused • We expect market will re-rate Keppel and accord a growth multiple as we accelerate the New Keppel’s growth. Monetisation of non-core portfolio should add further value © Keppel 5 The New Keppel i Non-Core Portfolio for Divestment comprises mainly legacy offshore & marine assets, residential landbank, selected property developments and investment properties, hospitality and logistics assets, associated cash and receivables, and other non-core investments that are not aligned with Keppel’s strategic focus as an asset-light global asset manager and operator.

6.

• Net profit

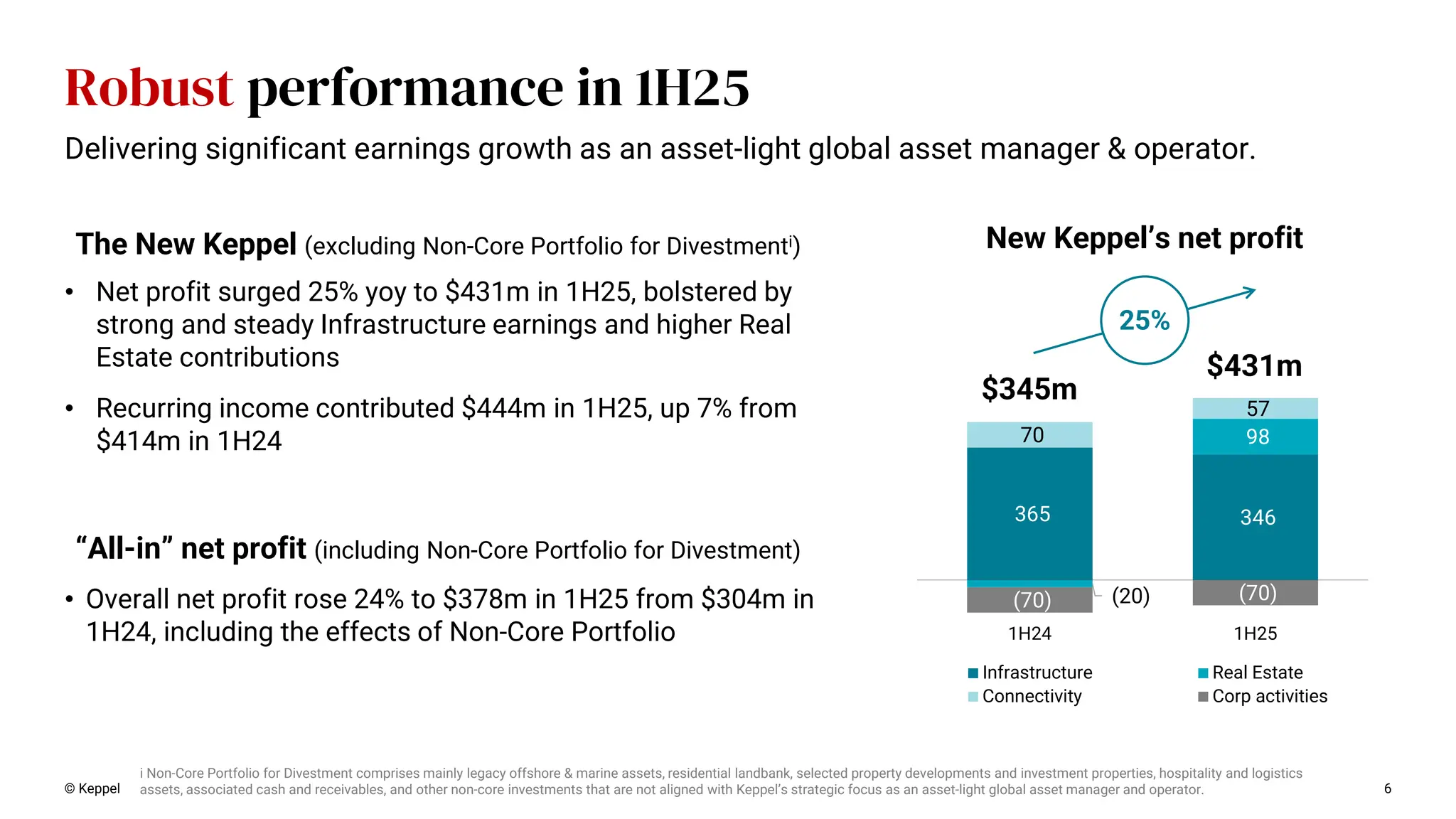

surged 25% yoy to $431m in 1H25, bolstered by strong and steady Infrastructure earnings and higher Real Estate contributions • Recurring income contributed $444m in 1H25, up 7% from $414m in 1H24 © Keppel 6 365 346 (20) 98 70 57 (70) (70) 1H24 1H25 Infrastructure Real Estate Connectivity Corp activities $431m $345m 25% The New Keppel (excluding Non-Core Portfolio for Divestmenti) Robust performance in 1H25 New Keppel’s net profit • Overall net profit rose 24% to $378m in 1H25 from $304m in 1H24, including the effects of Non-Core Portfolio “All-in” net profit (including Non-Core Portfolio for Divestment) Delivering significant earnings growth as an asset-light global asset manager & operator. i Non-Core Portfolio for Divestment comprises mainly legacy offshore & marine assets, residential landbank, selected property developments and investment properties, hospitality and logistics assets, associated cash and receivables, and other non-core investments that are not aligned with Keppel’s strategic focus as an asset-light global asset manager and operator.

7.

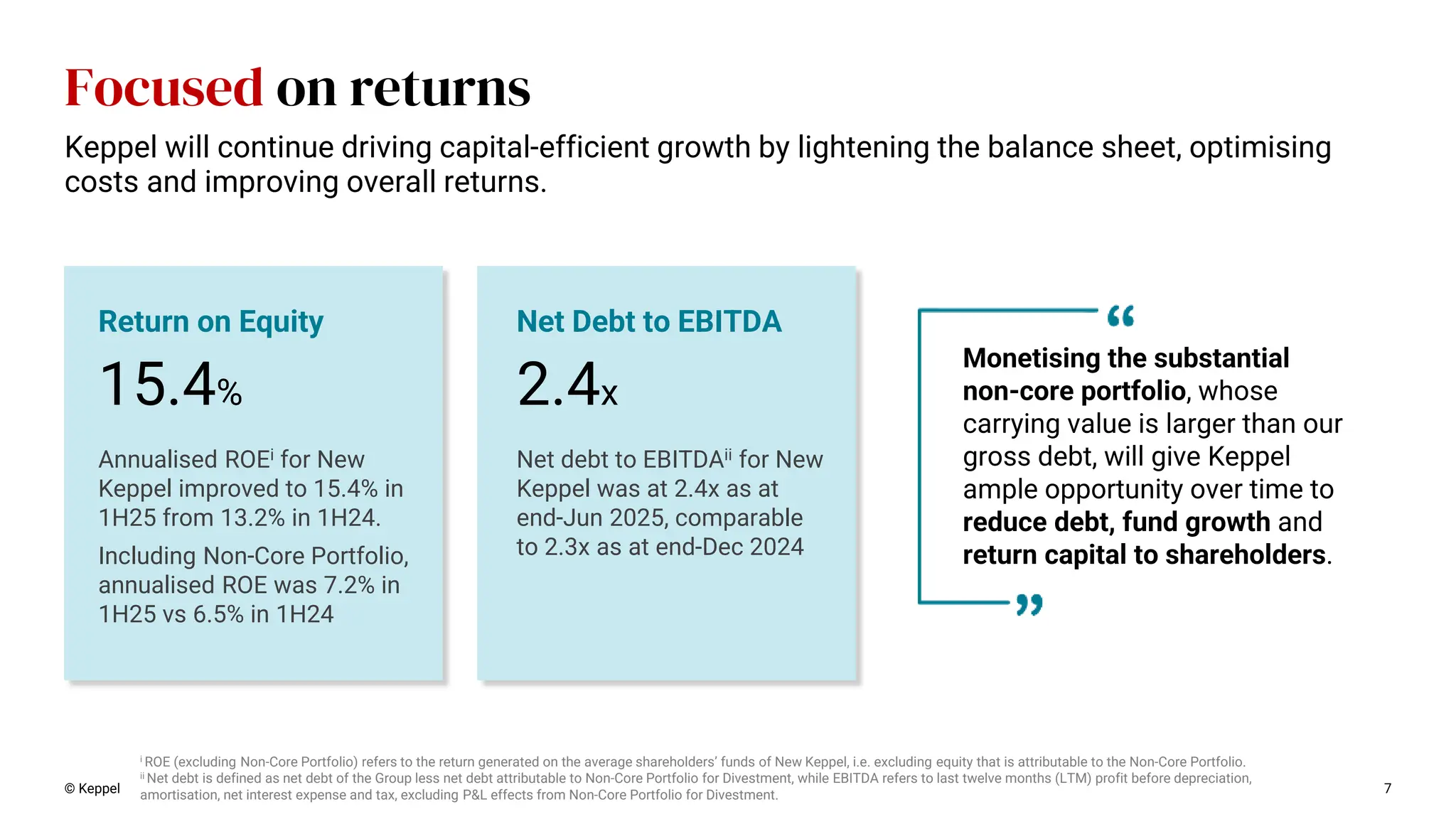

© Keppel 7 Focused

on returns 15.4% Return on Equity Annualised ROEi for New Keppel improved to 15.4% in 1H25 from 13.2% in 1H24. Including Non-Core Portfolio, annualised ROE was 7.2% in 1H25 vs 6.5% in 1H24 2.4x Net Debt to EBITDA Net debt to EBITDAii for New Keppel was at 2.4x as at end-Jun 2025, comparable to 2.3x as at end-Dec 2024 i ROE (excluding Non-Core Portfolio) refers to the return generated on the average shareholders’ funds of New Keppel, i.e. excluding equity that is attributable to the Non-Core Portfolio. ii Net debt is defined as net debt of the Group less net debt attributable to Non-Core Portfolio for Divestment, while EBITDA refers to last twelve months (LTM) profit before depreciation, amortisation, net interest expense and tax, excluding P&L effects from Non-Core Portfolio for Divestment. Keppel will continue driving capital-efficient growth by lightening the balance sheet, optimising costs and improving overall returns. Monetising the substantial non-core portfolio, whose carrying value is larger than our gross debt, will give Keppel ample opportunity over time to reduce debt, fund growth and return capital to shareholders.

8.

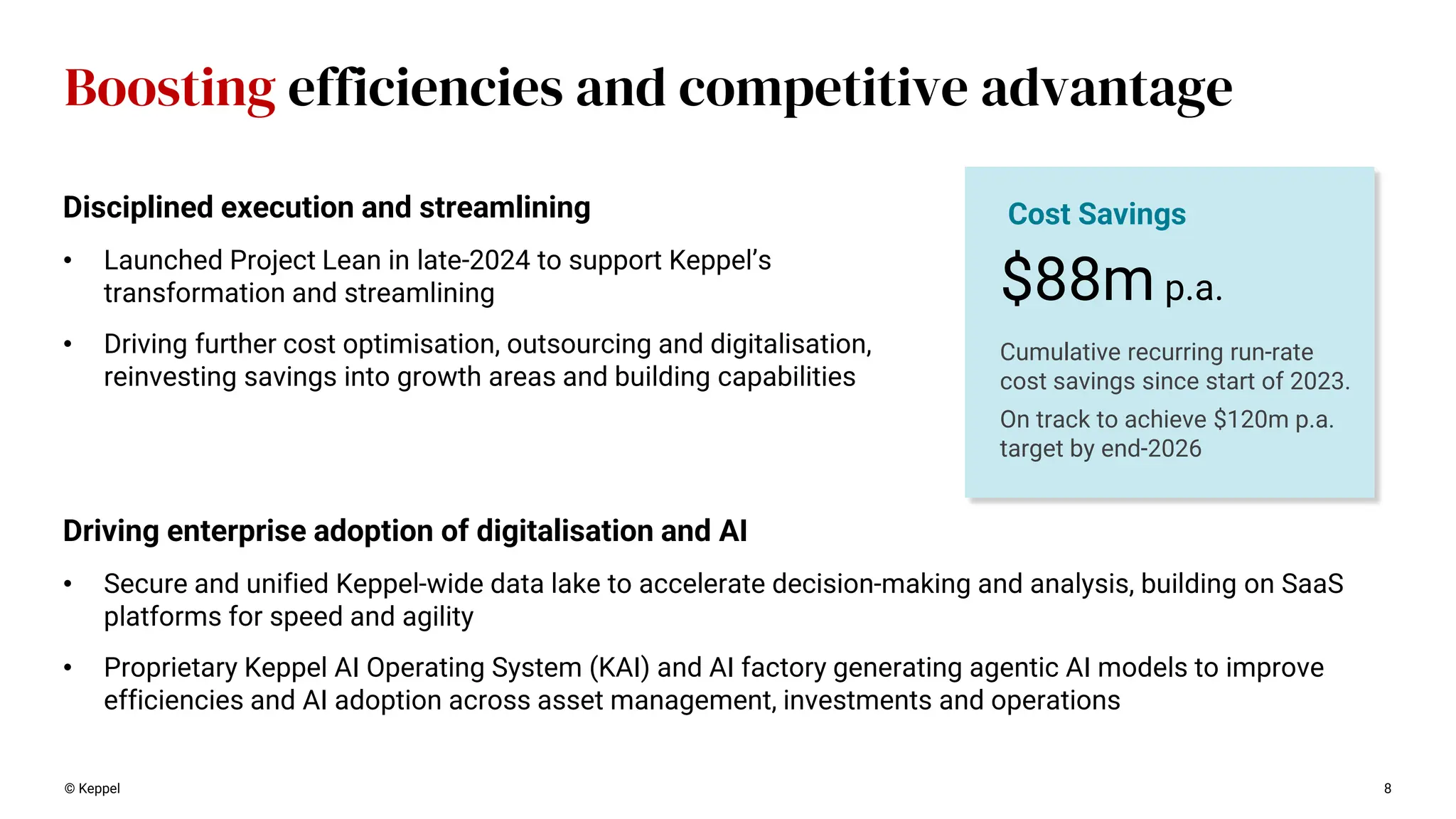

© Keppel 8 Boosting

efficiencies and competitive advantage Driving enterprise adoption of digitalisation and AI • Secure and unified Keppel-wide data lake to accelerate decision-making and analysis, building on SaaS platforms for speed and agility • Proprietary Keppel AI Operating System (KAI) and AI factory generating agentic AI models to improve efficiencies and AI adoption across asset management, investments and operations $88m p.a. Cost Savings Cumulative recurring run-rate cost savings since start of 2023. On track to achieve $120m p.a. target by end-2026 Disciplined execution and streamlining • Launched Project Lean in late-2024 to support Keppel’s transformation and streamlining • Driving further cost optimisation, outsourcing and digitalisation, reinvesting savings into growth areas and building capabilities

9.

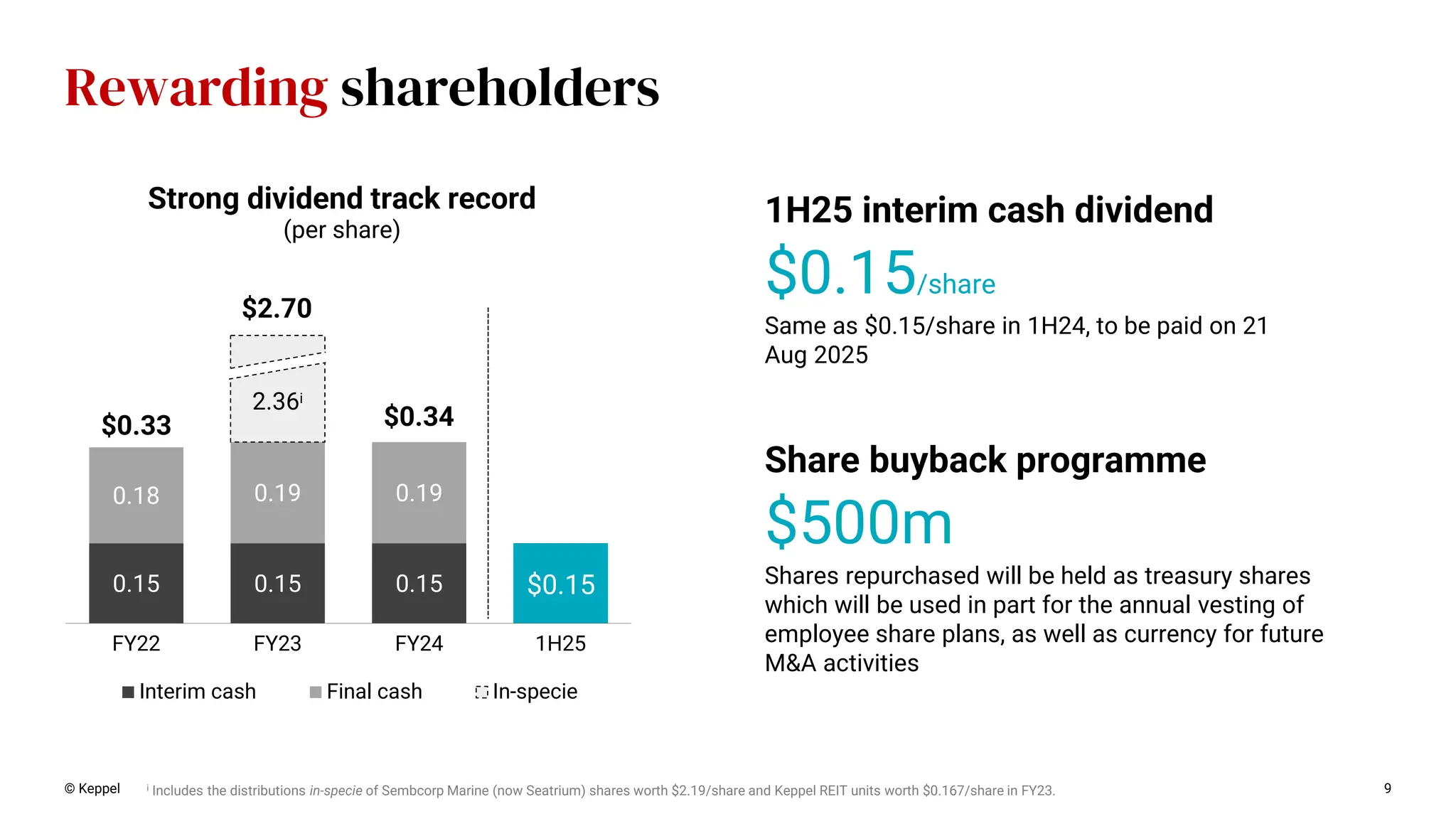

© Keppel 9 Rewarding

shareholders i Includes the distributions in-specie of Sembcorp Marine (now Seatrium) shares worth $2.19/share and Keppel REIT units worth $0.167/share in FY23. 0.15 0.15 0.15 0.18 0.19 0.19 2.36i FY22 FY23 FY24 1H25 Interim cash Final cash In-specie $0.33 $2.70 $0.34 Strong dividend track record (per share) $0.15 $0.15/share Same as $0.15/share in 1H24, to be paid on 21 Aug 2025 1H25 interim cash dividend $500m Shares repurchased will be held as treasury shares which will be used in part for the annual vesting of employee share plans, as well as currency for future M&A activities Share buyback programme

10.

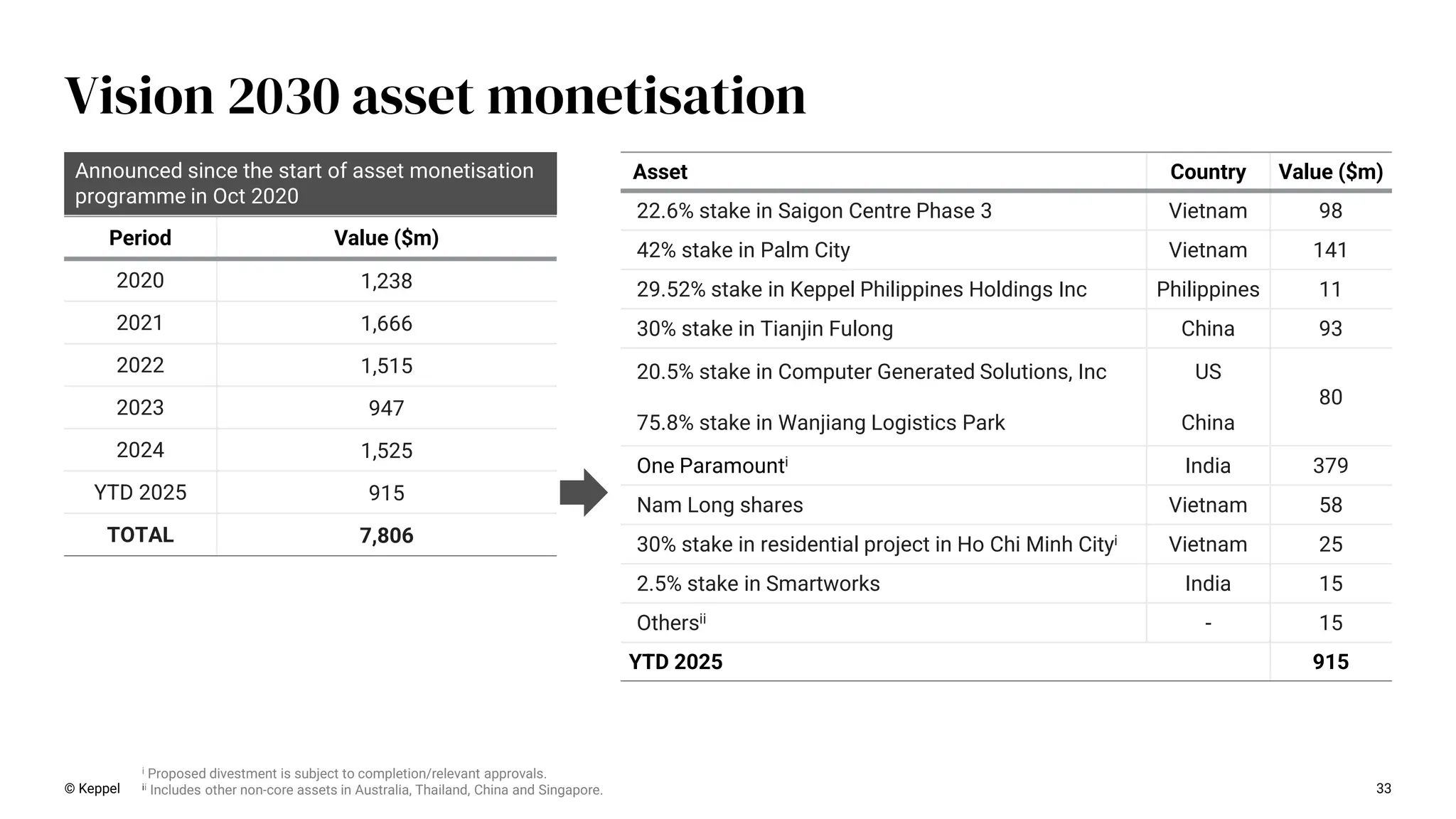

Accelerating asset monetisation ©

Keppel 10 Comprising real estate and connectivity assets expected to be finalised in 2H25 The Accelerating Monetisation Task Force will continue to focus on optimising the speed of divestment and exit value of Keppel’s non-core assets. Further deals under negotiation >$500m Including $477m announced in Jul 2025 from real estate assets namely a commercial building in India, and stakes in Smartworks, Nam Long and a residential project in Vietnam Asset monetisation announced YTD 2025 $915m

11.

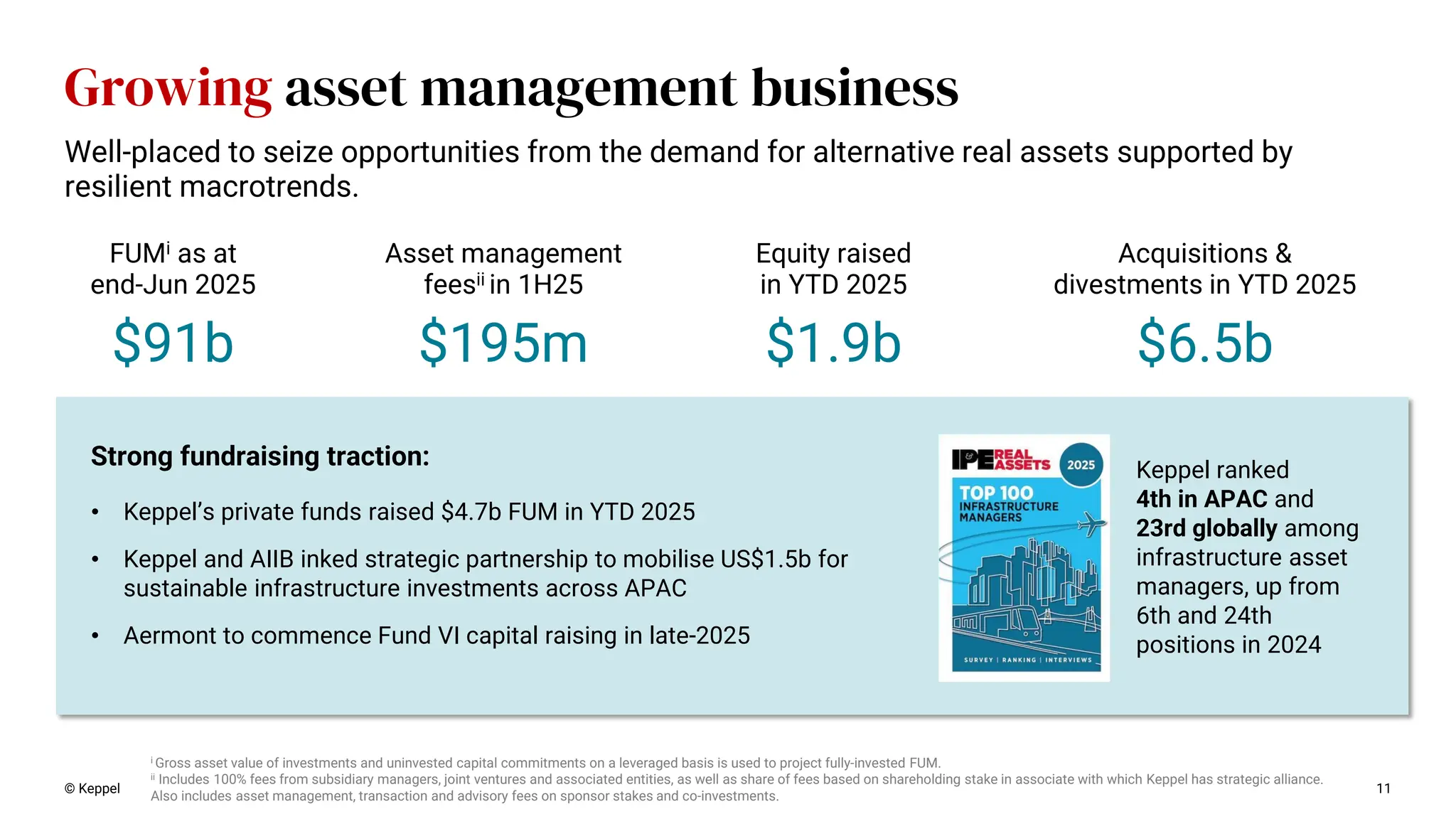

Growing asset management

business © Keppel 11 i Gross asset value of investments and uninvested capital commitments on a leveraged basis is used to project fully-invested FUM. ii Includes 100% fees from subsidiary managers, joint ventures and associated entities, as well as share of fees based on shareholding stake in associate with which Keppel has strategic alliance. Also includes asset management, transaction and advisory fees on sponsor stakes and co-investments. $1.9b Equity raised in YTD 2025 $6.5b Acquisitions & divestments in YTD 2025 $195m Asset management feesii in 1H25 Well-placed to seize opportunities from the demand for alternative real assets supported by resilient macrotrends. • Keppel’s private funds raised $4.7b FUM in YTD 2025 • Keppel and AIIB inked strategic partnership to mobilise US$1.5b for sustainable infrastructure investments across APAC • Aermont to commence Fund VI capital raising in late-2025 $91b FUMi as at end-Jun 2025 Strong fundraising traction: Keppel ranked 4th in APAC and 23rd globally among infrastructure asset managers, up from 6th and 24th positions in 2024

12.

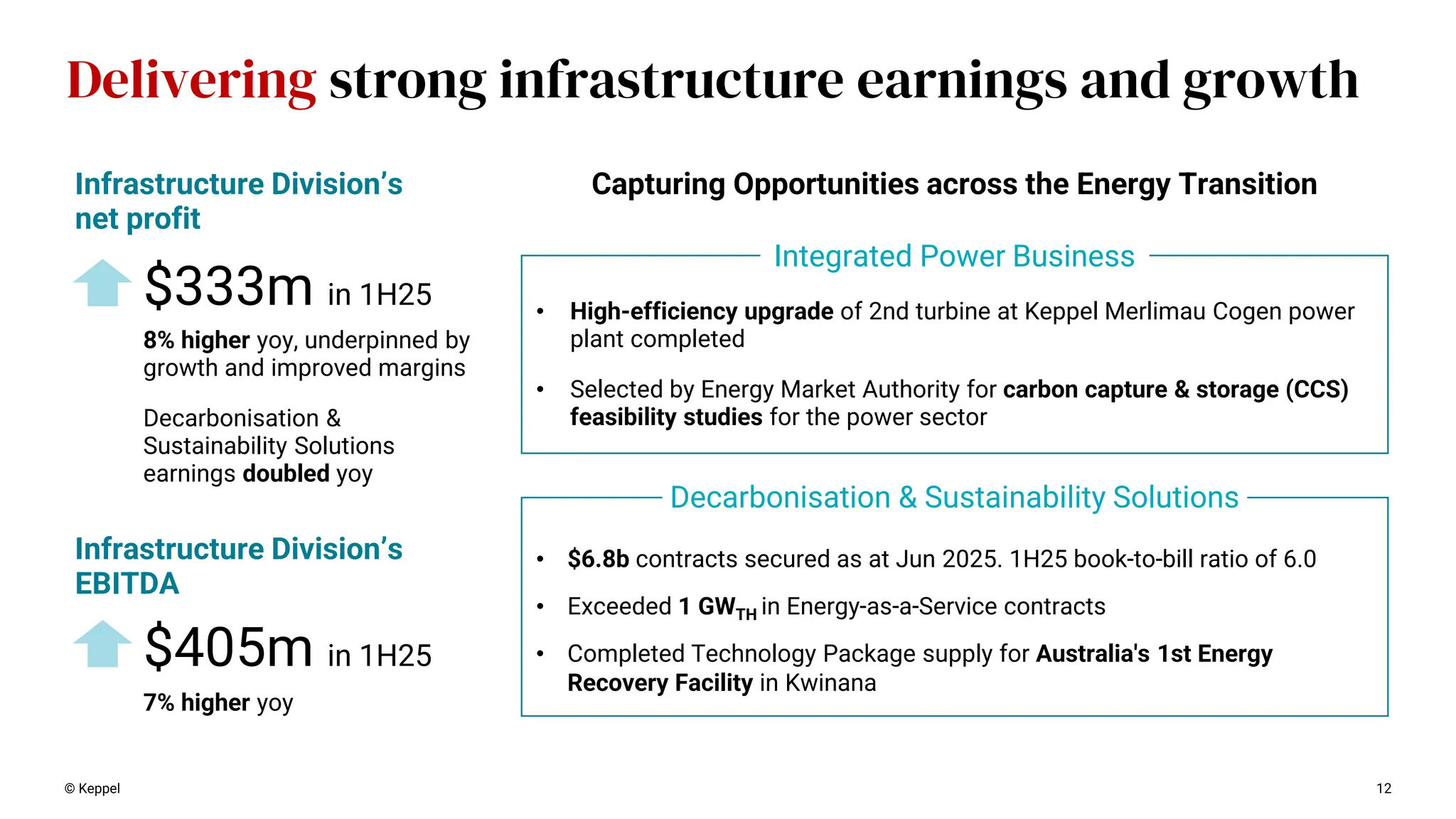

© Keppel 12 Delivering

strong infrastructure earnings and growth Infrastructure Division’s net profit Infrastructure Division’s EBITDA $333m in 1H25 $405m in 1H25 8% higher yoy, underpinned by growth and improved margins Decarbonisation & Sustainability Solutions earnings doubled yoy 7% higher yoy • $6.8b contracts secured as at Jun 2025. 1H25 book-to-bill ratio of 6.0 • Exceeded 1 GWTH in Energy-as-a-Service contracts • Completed Technology Package supply for Australia's 1st Energy Recovery Facility in Kwinana Capturing Opportunities across the Energy Transition Integrated Power Business • High-efficiency upgrade of 2nd turbine at Keppel Merlimau Cogen power plant completed • Selected by Energy Market Authority for carbon capture & storage (CCS) feasibility studies for the power sector Decarbonisation & Sustainability Solutions

13.

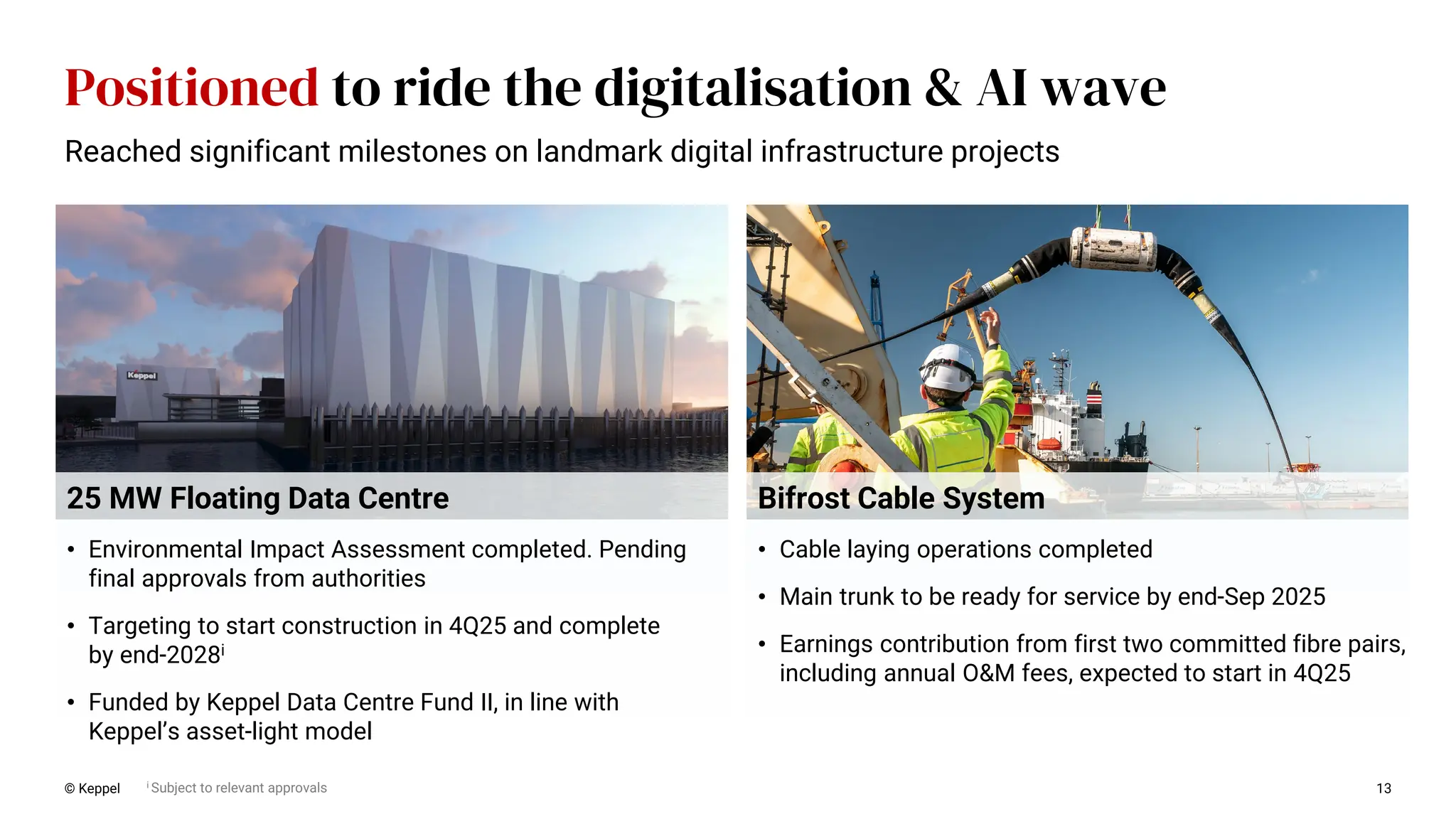

© Keppel 13 Positioned

to ride the digitalisation & AI wave i Subject to relevant approvals Bifrost Cable System • Cable laying operations completed • Main trunk to be ready for service by end-Sep 2025 • Earnings contribution from first two committed fibre pairs, including annual O&M fees, expected to start in 4Q25 25 MW Floating Data Centre • Environmental Impact Assessment completed. Pending final approvals from authorities • Targeting to start construction in 4Q25 and complete by end-2028i • Funded by Keppel Data Centre Fund II, in line with Keppel’s asset-light model Reached significant milestones on landmark digital infrastructure projects

14.

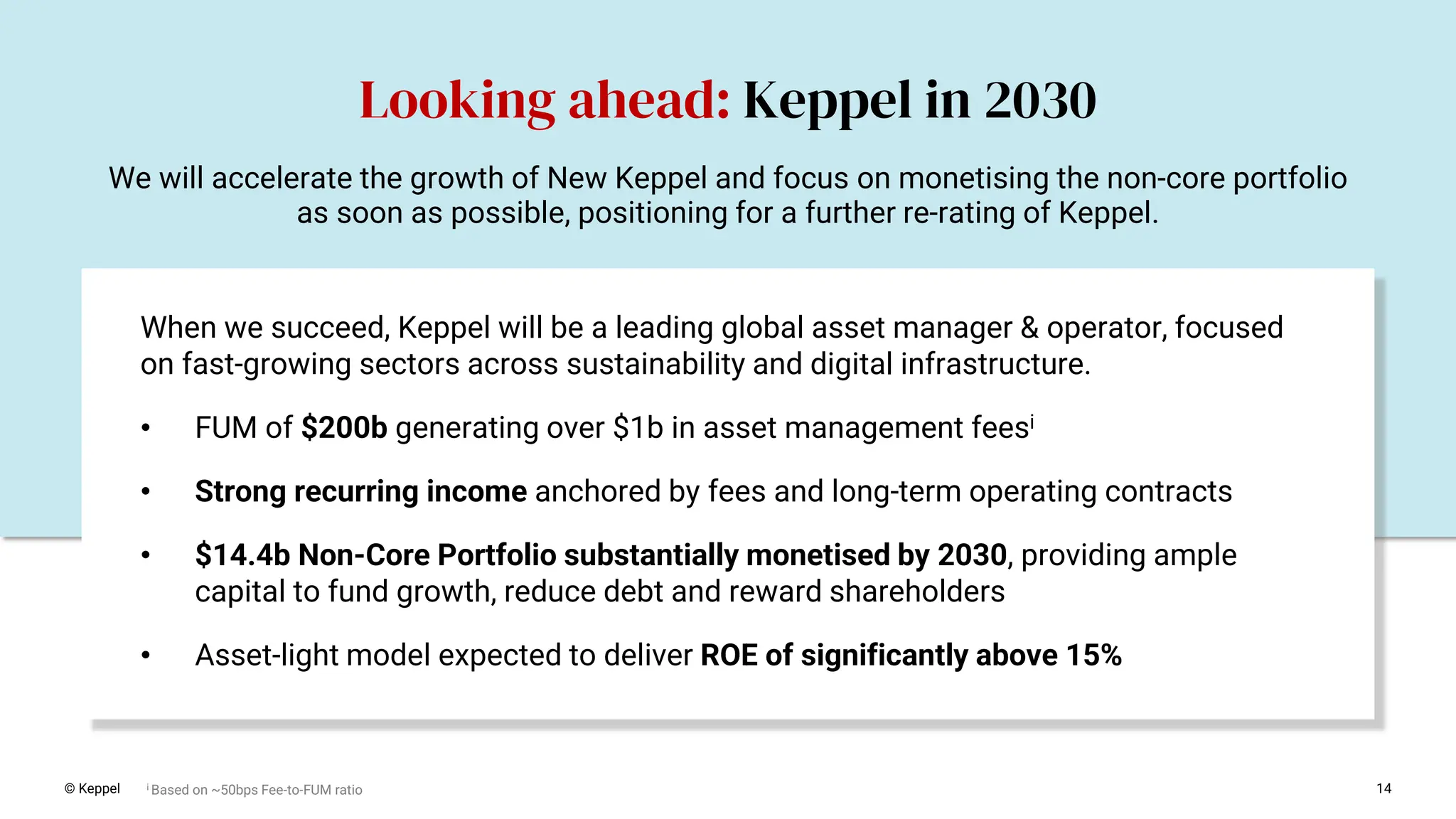

© Keppel 14 Looking

ahead: Keppel in 2030 We will accelerate the growth of New Keppel and focus on monetising the non-core portfolio as soon as possible, positioning for a further re-rating of Keppel. When we succeed, Keppel will be a leading global asset manager & operator, focused on fast-growing sectors across sustainability and digital infrastructure. • FUM of $200b generating over $1b in asset management feesi • Strong recurring income anchored by fees and long-term operating contracts • $14.4b Non-Core Portfolio substantially monetised by 2030, providing ample capital to fund growth, reduce debt and reward shareholders • Asset-light model expected to deliver ROE of significantly above 15% i Based on ~50bps Fee-to-FUM ratio

15.

Financial highlights 02 15

16.

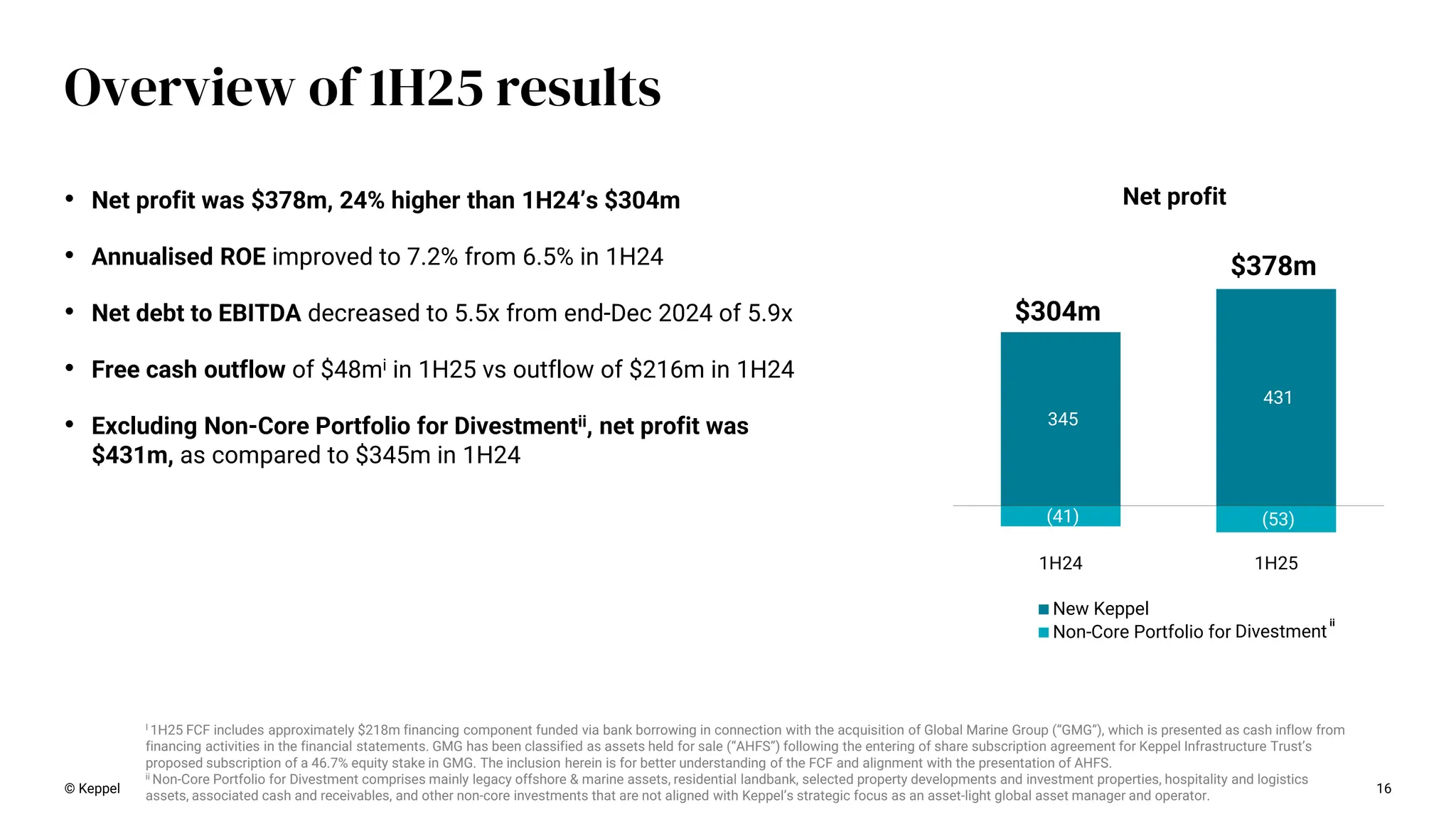

Net profit 16 Overview of

1H25 results © Keppel • Net profit was $378m, 24% higher than 1H24’s $304m • Annualised ROE improved to 7.2% from 6.5% in 1H24 • Net debt to EBITDA decreased to 5.5x from end-Dec 2024 of 5.9x • Free cash outflow of $48mi in 1H25 vs outflow of $216m in 1H24 • Excluding Non-Core Portfolio for Divestmentii, net profit was $431m, as compared to $345m in 1H24 345 431 (41) (53) 1H24 1H25 New Keppel Non-Core Portfolio for Divestment $378m $304m I 1H25 FCF includes approximately $218m financing component funded via bank borrowing in connection with the acquisition of Global Marine Group (“GMG”), which is presented as cash inflow from financing activities in the financial statements. GMG has been classified as assets held for sale (“AHFS”) following the entering of share subscription agreement for Keppel Infrastructure Trust’s proposed subscription of a 46.7% equity stake in GMG. The inclusion herein is for better understanding of the FCF and alignment with the presentation of AHFS. ii Non-Core Portfolio for Divestment comprises mainly legacy offshore & marine assets, residential landbank, selected property developments and investment properties, hospitality and logistics assets, associated cash and receivables, and other non-core investments that are not aligned with Keppel’s strategic focus as an asset-light global asset manager and operator. ii

17.

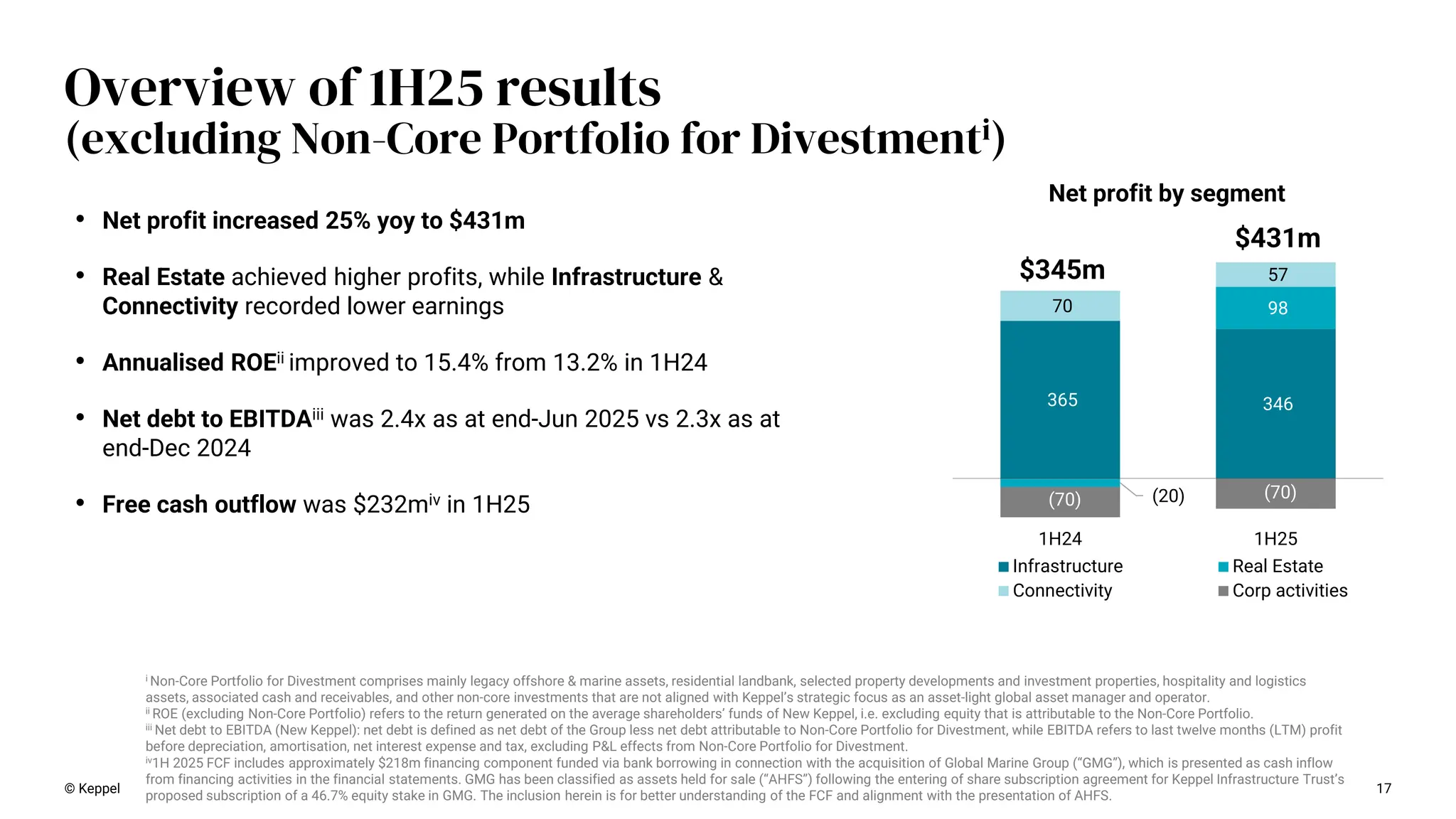

365 346 (20) 98 70 57 (70) (70) 1H24

1H25 Infrastructure Real Estate Connectivity Corp activities $431m $345m 17 Overview of 1H25 results (excluding Non-Core Portfolio for Divestmenti) Net profit by segment © Keppel • Net profit increased 25% yoy to $431m • Real Estate achieved higher profits, while Infrastructure & Connectivity recorded lower earnings • Annualised ROEii improved to 15.4% from 13.2% in 1H24 • Net debt to EBITDAiii was 2.4x as at end-Jun 2025 vs 2.3x as at end-Dec 2024 • Free cash outflow was $232miv in 1H25 i Non-Core Portfolio for Divestment comprises mainly legacy offshore & marine assets, residential landbank, selected property developments and investment properties, hospitality and logistics assets, associated cash and receivables, and other non-core investments that are not aligned with Keppel’s strategic focus as an asset-light global asset manager and operator. ii ROE (excluding Non-Core Portfolio) refers to the return generated on the average shareholders’ funds of New Keppel, i.e. excluding equity that is attributable to the Non-Core Portfolio. iii Net debt to EBITDA (New Keppel): net debt is defined as net debt of the Group less net debt attributable to Non-Core Portfolio for Divestment, while EBITDA refers to last twelve months (LTM) profit before depreciation, amortisation, net interest expense and tax, excluding P&L effects from Non-Core Portfolio for Divestment. iv1H 2025 FCF includes approximately $218m financing component funded via bank borrowing in connection with the acquisition of Global Marine Group (“GMG”), which is presented as cash inflow from financing activities in the financial statements. GMG has been classified as assets held for sale (“AHFS”) following the entering of share subscription agreement for Keppel Infrastructure Trust’s proposed subscription of a 46.7% equity stake in GMG. The inclusion herein is for better understanding of the FCF and alignment with the presentation of AHFS.

18.

Horizontal reporting (excluding Non-Core

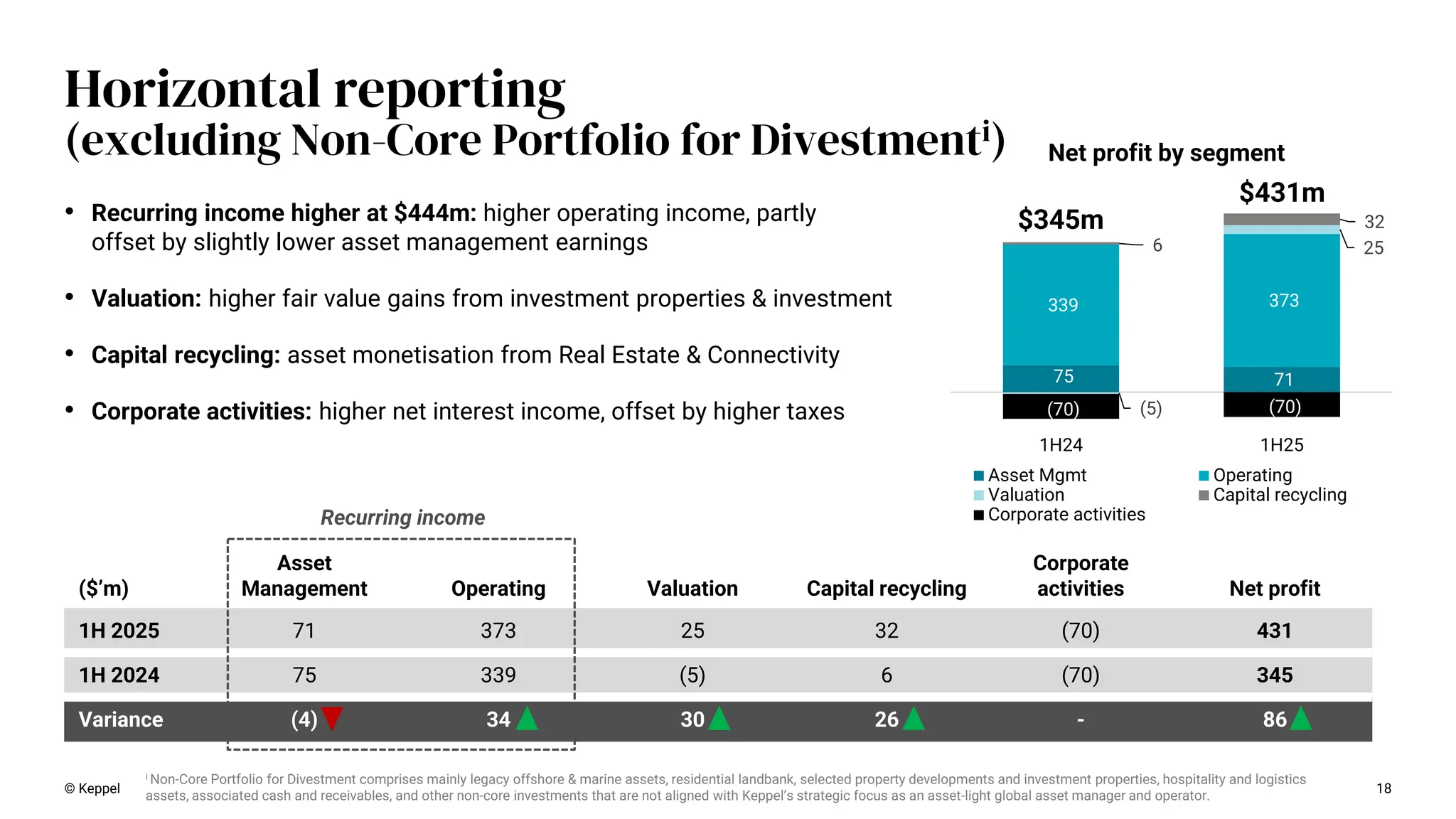

Portfolio for Divestmenti) © Keppel 18 Net profit by segment 75 71 339 373 (5) 25 6 32 (70) (70) 1H24 1H25 Asset Mgmt Operating Valuation Capital recycling Corporate activities $345m $431m • Recurring income higher at $444m: higher operating income, partly offset by slightly lower asset management earnings • Valuation: higher fair value gains from investment properties & investment • Capital recycling: asset monetisation from Real Estate & Connectivity • Corporate activities: higher net interest income, offset by higher taxes ($’m) Asset Management Operating Valuation Capital recycling Corporate activities Net profit 1H 2025 71 373 25 32 (70) 431 1H 2024 75 339 (5) 6 (70) 345 Variance (4) 34 30 26 - 86 Recurring income i Non-Core Portfolio for Divestment comprises mainly legacy offshore & marine assets, residential landbank, selected property developments and investment properties, hospitality and logistics assets, associated cash and receivables, and other non-core investments that are not aligned with Keppel’s strategic focus as an asset-light global asset manager and operator.

19.

© Keppel 19 1H

2025 net profit (horizontal reporting) i Includes asset management, transaction and advisory fees on sponsor stakes and co-investments. ii Includes returns (net of financing costs attributable to such stakes) from equity accounted stakes in listed and private funds – Infrastructure [$6m from listed funds]; Real Estate [$15m from listed funds], and Connectivity [$16m from listed funds]. iii Includes overheads and financing costs which have not been attributed to segments. iv Non-Core Portfolio for Divestment comprises mainly legacy offshore & marine assets, residential landbank, selected property developments and investment properties, hospitality and logistics assets, associated cash and receivables, and other non-core investments that are not aligned with Keppel’s strategic focus as an asset-light global asset manager and operator. ($’m) Asset Managementi Operatingii Valuation Capital recycling Net profit Infrastructure 16 333 (3) – 346 80% Real Estate 41 - 27 30 98 23% Connectivity 14 40 1 2 57 13% Corporate activitiesiii (70) (16%) New Keppel 71 373 25 32 431 100% Non-Core Portfolio for Divestmentiv (53) Net profit 71 373 25 32 378

20.

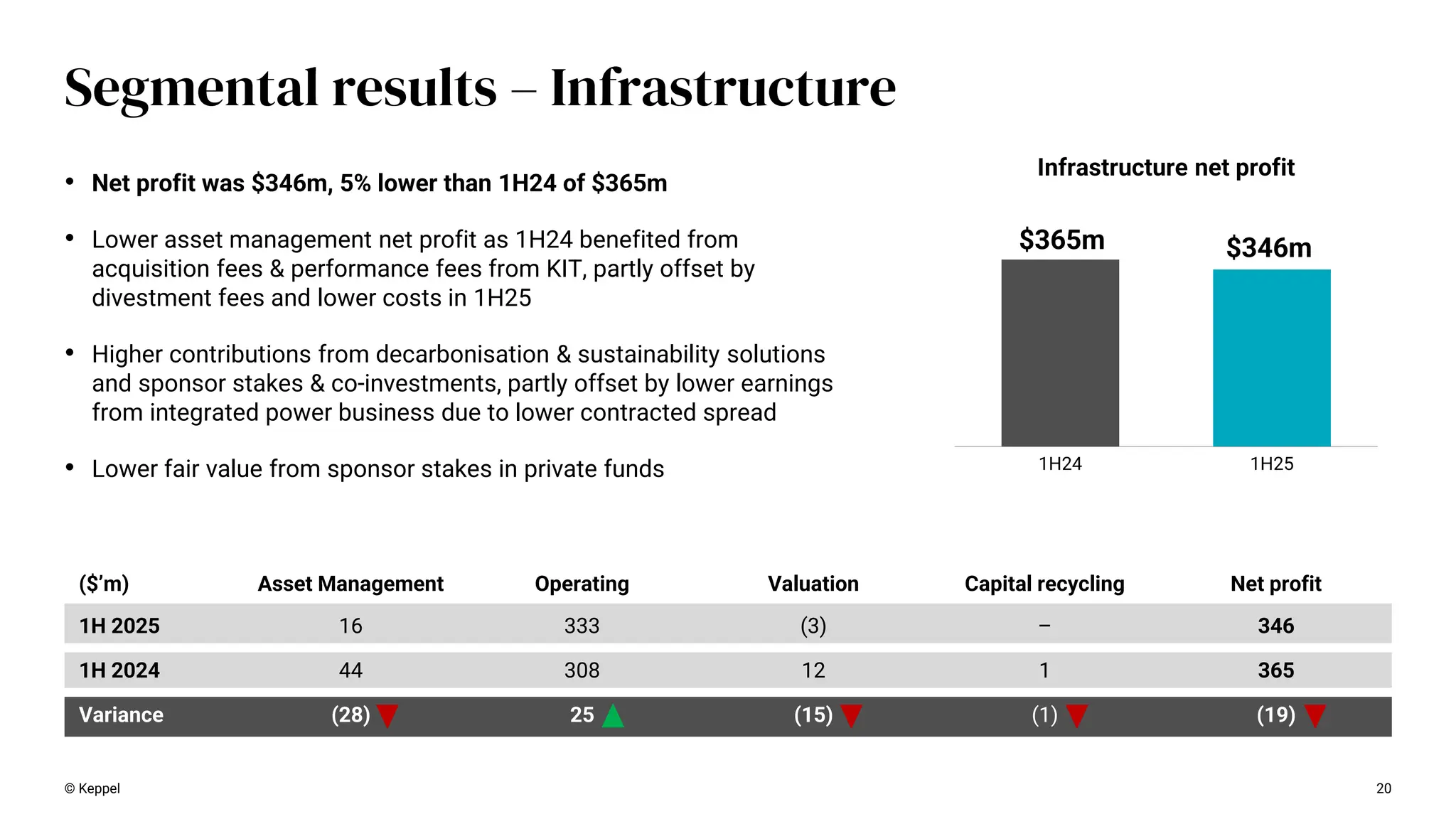

1H24 1H25 $365m $346m 20 Segmental

results – Infrastructure Infrastructure net profit © Keppel • Net profit was $346m, 5% lower than 1H24 of $365m • Lower asset management net profit as 1H24 benefited from acquisition fees & performance fees from KIT, partly offset by divestment fees and lower costs in 1H25 • Higher contributions from decarbonisation & sustainability solutions and sponsor stakes & co-investments, partly offset by lower earnings from integrated power business due to lower contracted spread • Lower fair value from sponsor stakes in private funds ($’m) Asset Management Operating Valuation Capital recycling Net profit 1H 2025 16 333 (3) – 346 1H 2024 44 308 12 1 365 Variance (28) 25 (15) (1) (19)

21.

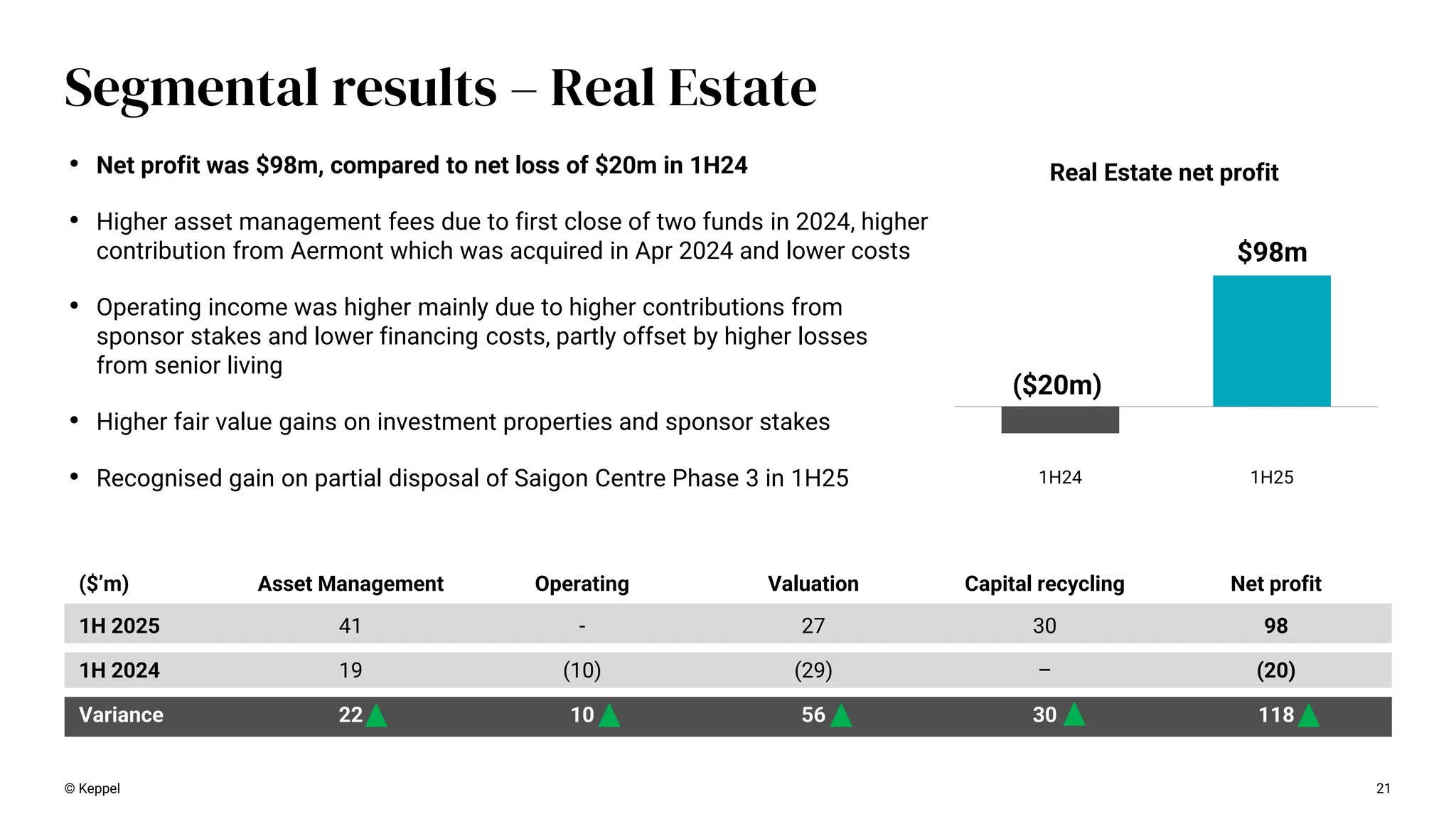

1H24 1H25 ($20m) $98m 21 Segmental results

– Real Estate Real Estate net profit © Keppel • Net profit was $98m, compared to net loss of $20m in 1H24 • Higher asset management fees due to first close of two funds in 2024, higher contribution from Aermont which was acquired in Apr 2024 and lower costs • Operating income was higher mainly due to higher contributions from sponsor stakes and lower financing costs, partly offset by higher losses from senior living • Higher fair value gains on investment properties and sponsor stakes • Recognised gain on partial disposal of Saigon Centre Phase 3 in 1H25 ($’m) Asset Management Operating Valuation Capital recycling Net profit 1H 2025 41 - 27 30 98 1H 2024 19 (10) (29) – (20) Variance 22 10 56 30 118

22.

22 Segmental results –

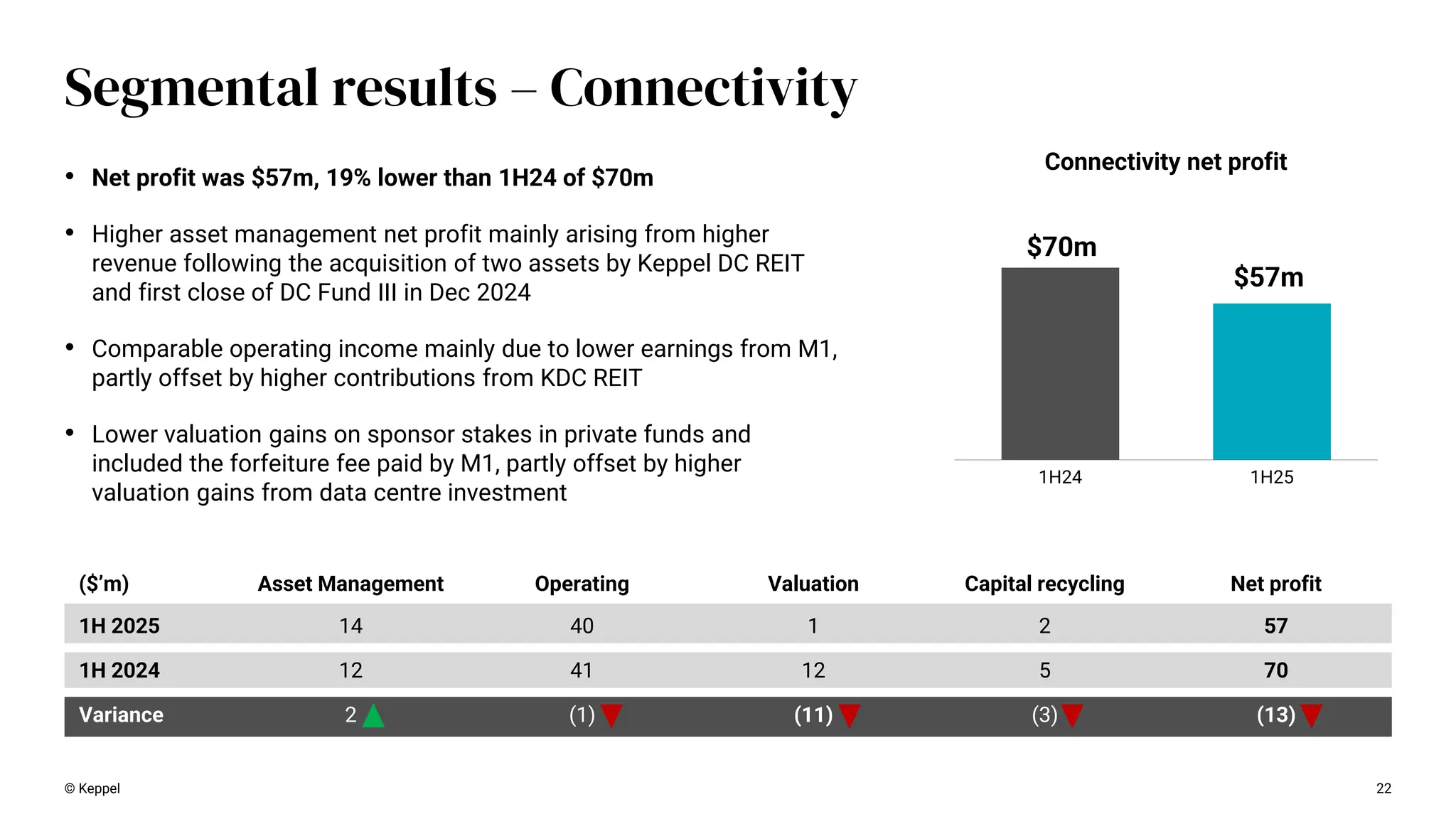

Connectivity 1H24 1H25 $70m $57m Connectivity net profit © Keppel • Net profit was $57m, 19% lower than 1H24 of $70m • Higher asset management net profit mainly arising from higher revenue following the acquisition of two assets by Keppel DC REIT and first close of DC Fund III in Dec 2024 • Comparable operating income mainly due to lower earnings from M1, partly offset by higher contributions from KDC REIT • Lower valuation gains on sponsor stakes in private funds and included the forfeiture fee paid by M1, partly offset by higher valuation gains from data centre investment ($’m) Asset Management Operating Valuation Capital recycling Net profit 1H 2025 14 40 1 2 57 1H 2024 12 41 12 5 70 Variance 2 (1) (11) (3) (13)

23.

($’m) Legacy O&M

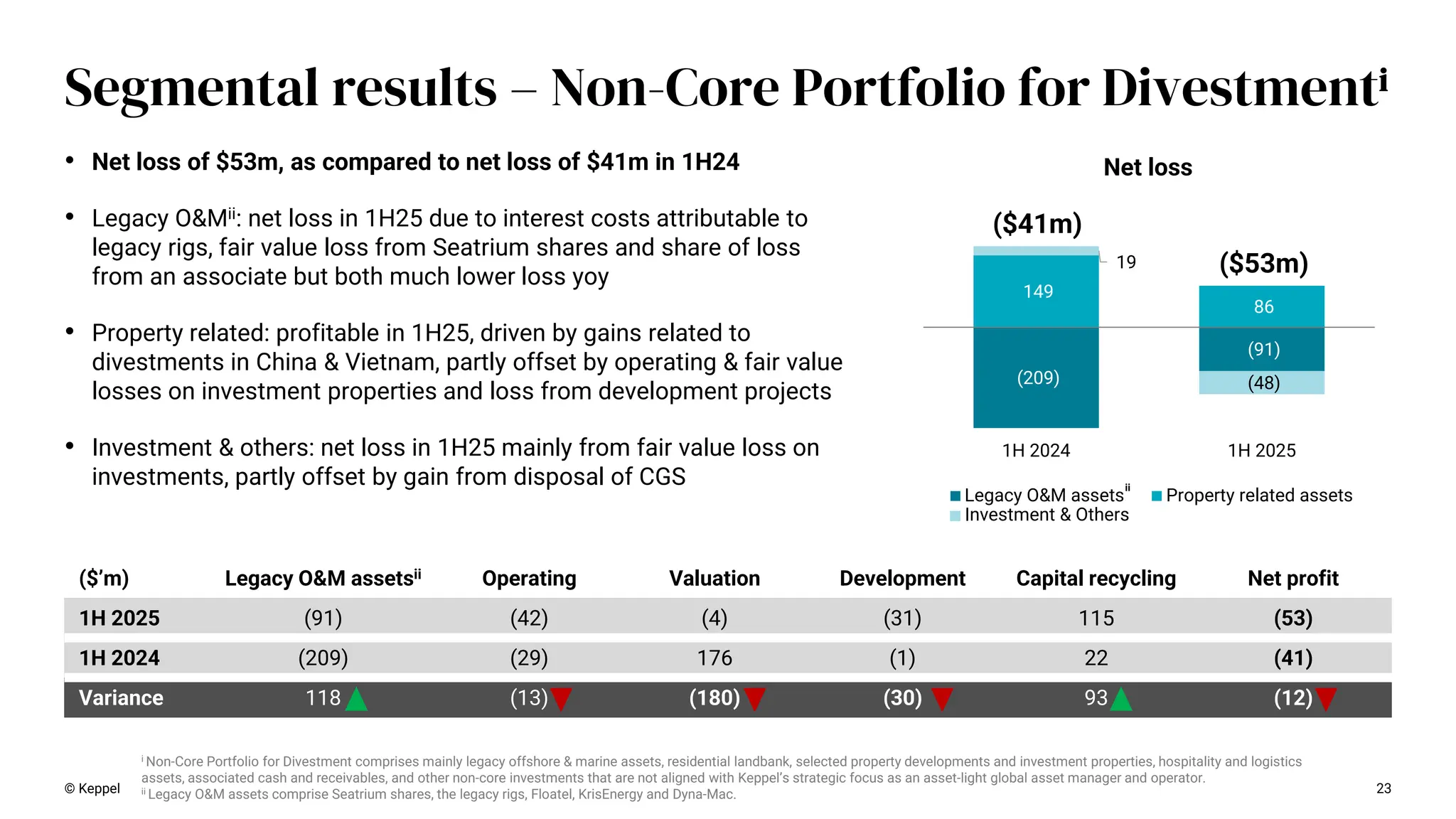

assetsii Operating Valuation Development Capital recycling Net profit 1H 2025 (91) (42) (4) (31) 115 (53) 1H 2024 (209) (29) 176 (1) 22 (41) Variance 118 (13) (180) (30) 93 (12) • Net loss of $53m, as compared to net loss of $41m in 1H24 • Legacy O&Mii: net loss in 1H25 due to interest costs attributable to legacy rigs, fair value loss from Seatrium shares and share of loss from an associate but both much lower loss yoy • Property related: profitable in 1H25, driven by gains related to divestments in China & Vietnam, partly offset by operating & fair value losses on investment properties and loss from development projects • Investment & others: net loss in 1H25 mainly from fair value loss on investments, partly offset by gain from disposal of CGS © Keppel 23 Segmental results – Non-Core Portfolio for Divestmenti (209) (91) 149 86 19 (48) 1H 2024 1H 2025 Legacy O&M assets Property related assets ($41m) ($53m) ii i Non-Core Portfolio for Divestment comprises mainly legacy offshore & marine assets, residential landbank, selected property developments and investment properties, hospitality and logistics assets, associated cash and receivables, and other non-core investments that are not aligned with Keppel’s strategic focus as an asset-light global asset manager and operator. ii Legacy O&M assets comprise Seatrium shares, the legacy rigs, Floatel, KrisEnergy and Dyna-Mac. Net loss Investment & Others

24.

Appendices -Operational updates 03 24

25.

i Gross asset

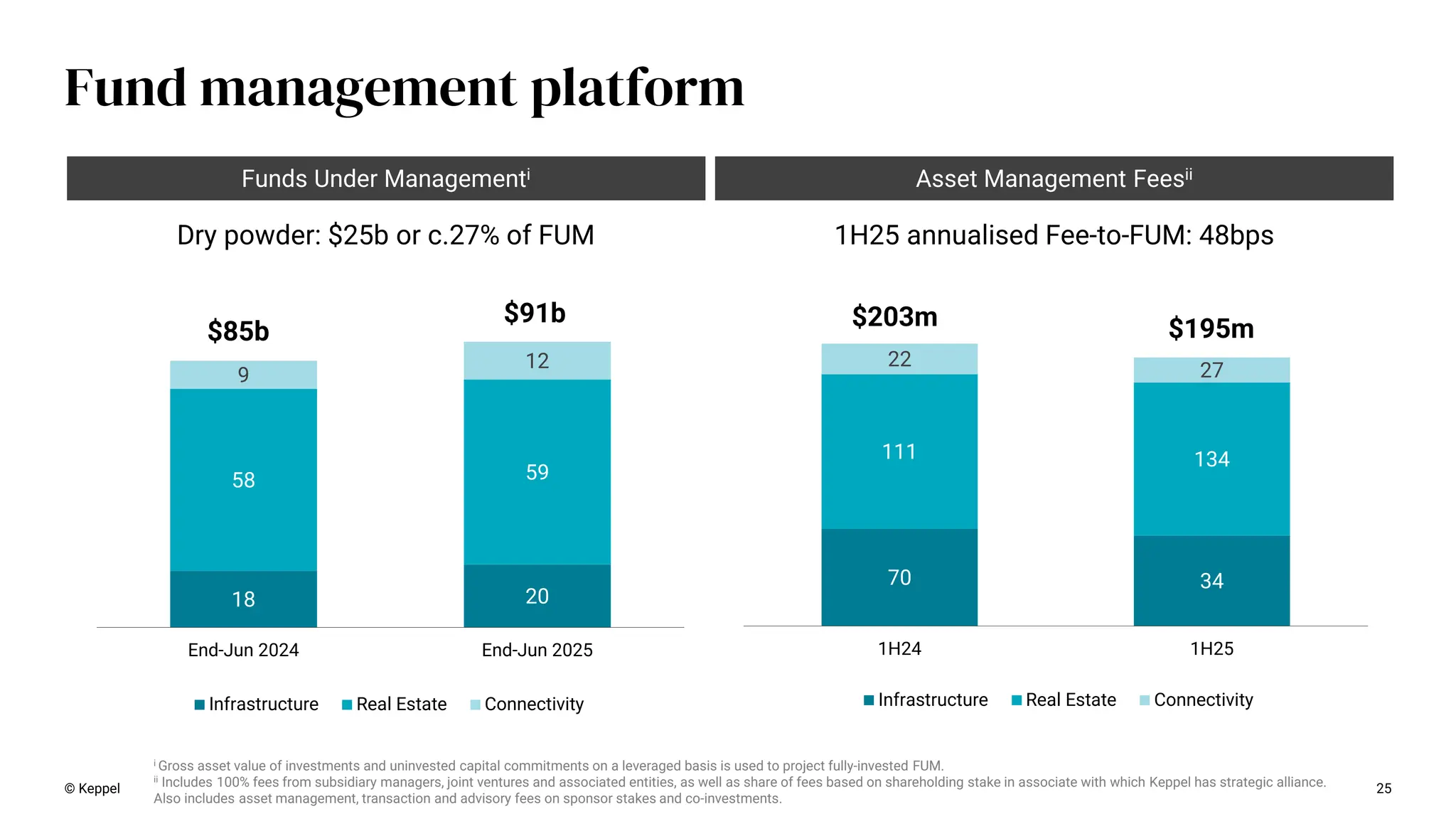

value of investments and uninvested capital commitments on a leveraged basis is used to project fully-invested FUM. ii Includes 100% fees from subsidiary managers, joint ventures and associated entities, as well as share of fees based on shareholding stake in associate with which Keppel has strategic alliance. Also includes asset management, transaction and advisory fees on sponsor stakes and co-investments. 70 34 111 134 22 27 1H24 1H25 Infrastructure Real Estate Connectivity $203m $195m 18 20 58 59 9 12 End-Jun 2024 End-Jun 2025 Infrastructure Real Estate Connectivity $85b $91b 1H25 annualised Fee-to-FUM: 48bps Dry powder: $25b or c.27% of FUM 25 © Keppel Fund management platform Asset Management Feesii Funds Under Managementi

26.

26 List of REITs/Trust No

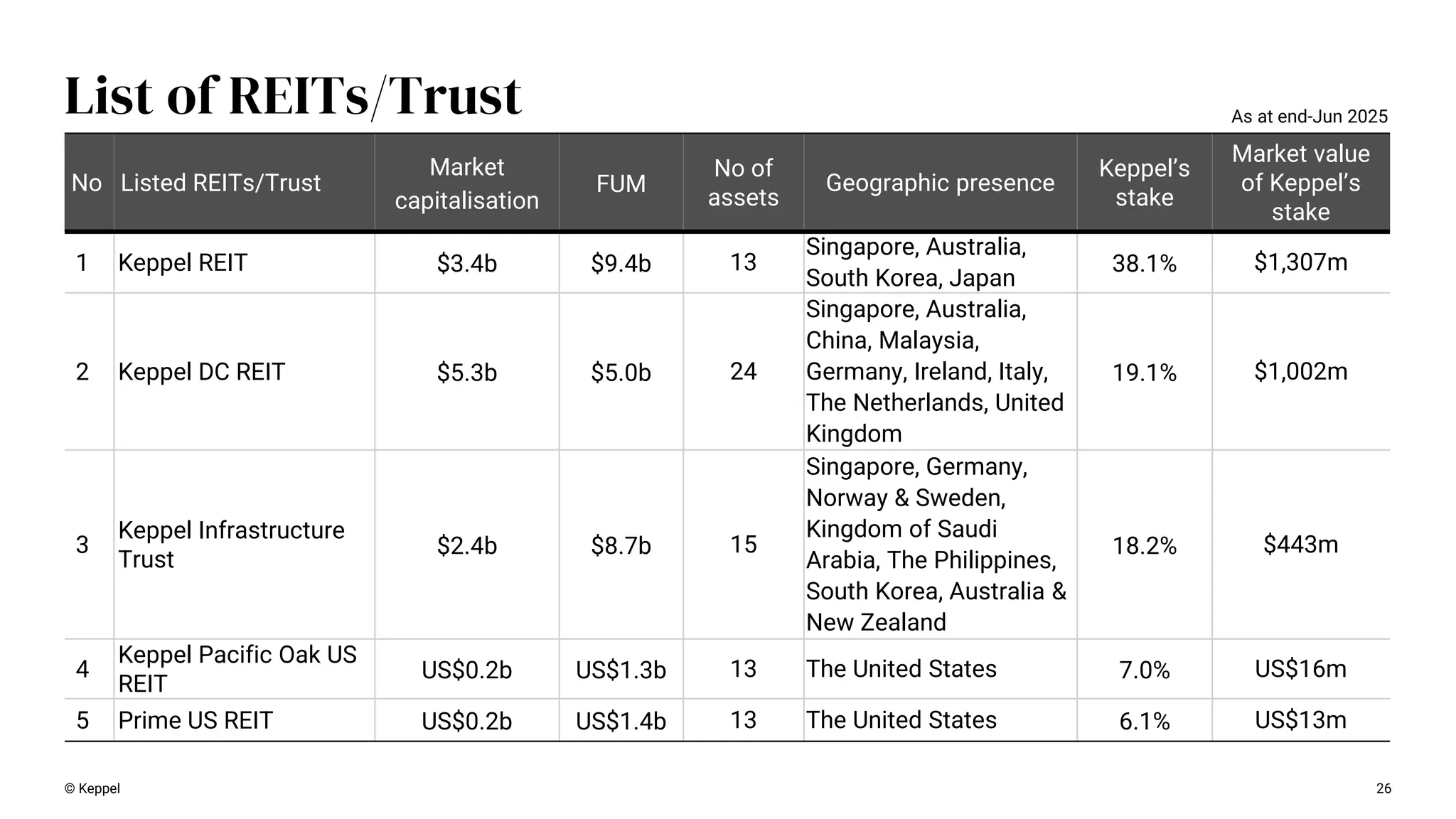

Listed REITs/Trust Market capitalisation FUM No of assets Geographic presence Keppel’s stake Market value of Keppel’s stake 1 Keppel REIT $3.4b $9.4b 13 Singapore, Australia, South Korea, Japan 38.1% $1,307m 2 Keppel DC REIT $5.3b $5.0b 24 Singapore, Australia, China, Malaysia, Germany, Ireland, Italy, The Netherlands, United Kingdom 19.1% $1,002m 3 Keppel Infrastructure Trust $2.4b $8.7b 15 Singapore, Germany, Norway & Sweden, Kingdom of Saudi Arabia, The Philippines, South Korea, Australia & New Zealand 18.2% $443m 4 Keppel Pacific Oak US REIT US$0.2b US$1.3b 13 The United States 7.0% US$16m 5 Prime US REIT US$0.2b US$1.4b 13 The United States 6.1% US$13m As at end-Jun 2025 © Keppel

27.

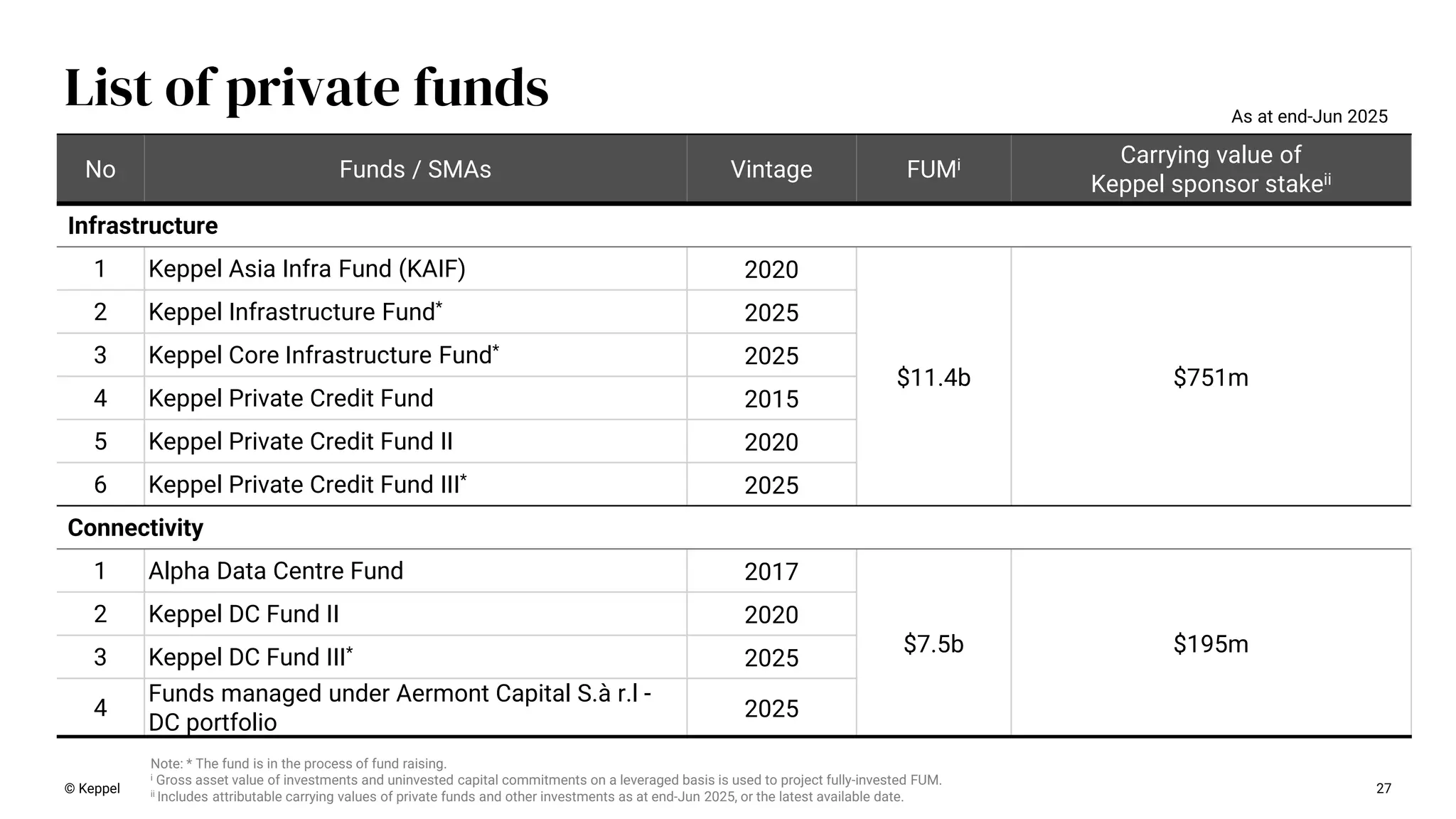

© Keppel 27 List

of private funds No Funds / SMAs Vintage FUMi Carrying value of Keppel sponsor stakeii Infrastructure 1 Keppel Asia Infra Fund (KAIF) 2020 $11.4b $751m 2 Keppel Infrastructure Fund* 2025 3 Keppel Core Infrastructure Fund* 2025 4 Keppel Private Credit Fund 2015 5 Keppel Private Credit Fund II 2020 6 Keppel Private Credit Fund III* 2025 Connectivity 1 Alpha Data Centre Fund 2017 $7.5b $195m 2 Keppel DC Fund II 2020 3 Keppel DC Fund III* 2025 4 Funds managed under Aermont Capital S.à r.l - DC portfolio 2025 Note: * The fund is in the process of fund raising. i Gross asset value of investments and uninvested capital commitments on a leveraged basis is used to project fully-invested FUM. ii Includes attributable carrying values of private funds and other investments as at end-Jun 2025, or the latest available date. As at end-Jun 2025

28.

© Keppel 28 List

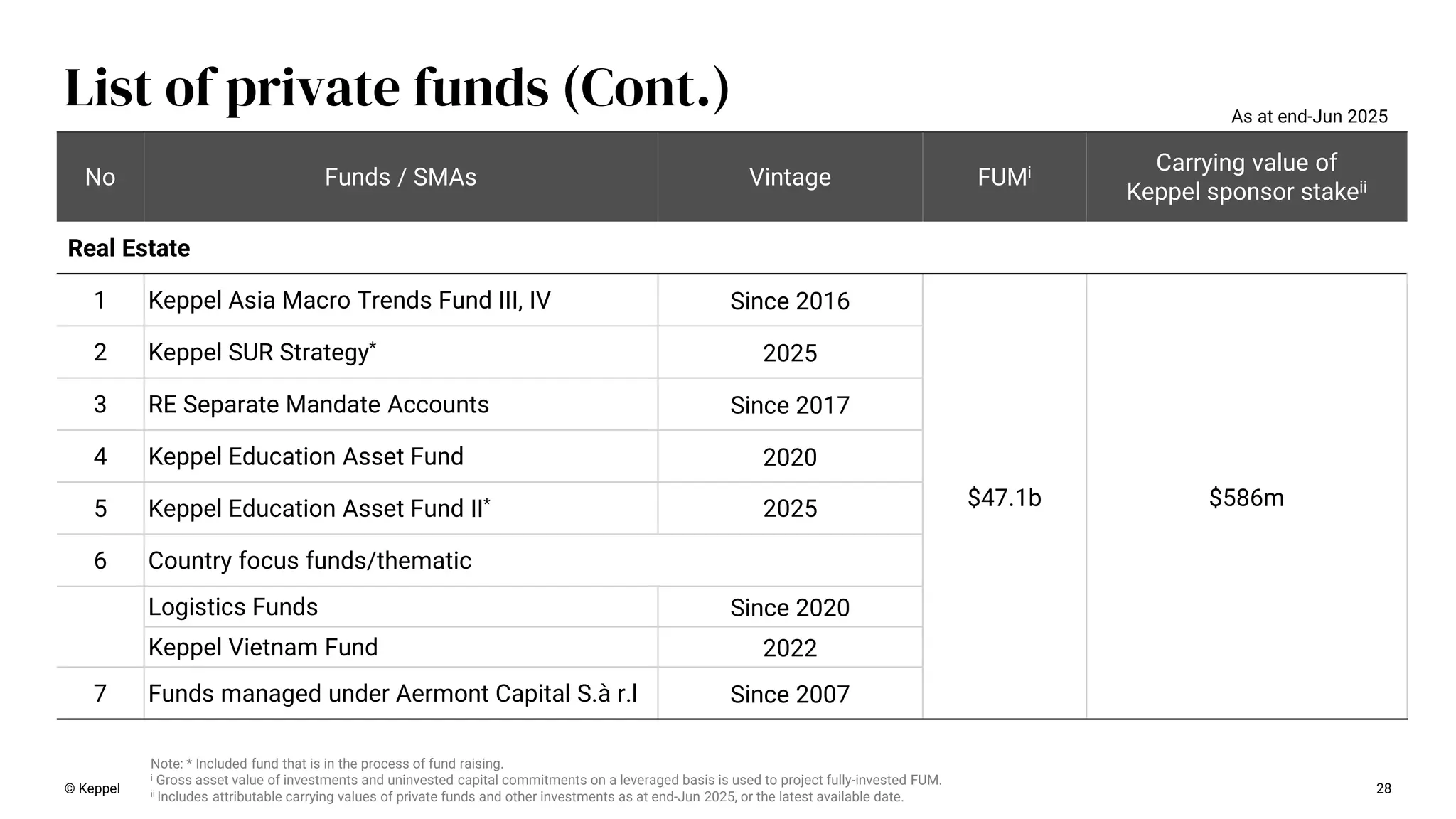

of private funds (Cont.) No Funds / SMAs Vintage FUMi Carrying value of Keppel sponsor stakeii Real Estate 1 Keppel Asia Macro Trends Fund III, IV Since 2016 $47.1b $586m 2 Keppel SUR Strategy* 2025 3 RE Separate Mandate Accounts Since 2017 4 Keppel Education Asset Fund 2020 5 Keppel Education Asset Fund II* 2025 6 Country focus funds/thematic Logistics Funds Since 2020 Keppel Vietnam Fund 2022 7 Funds managed under Aermont Capital S.à r.l Since 2007 Note: * Included fund that is in the process of fund raising. i Gross asset value of investments and uninvested capital commitments on a leveraged basis is used to project fully-invested FUM. ii Includes attributable carrying values of private funds and other investments as at end-Jun 2025, or the latest available date. As at end-Jun 2025

29.

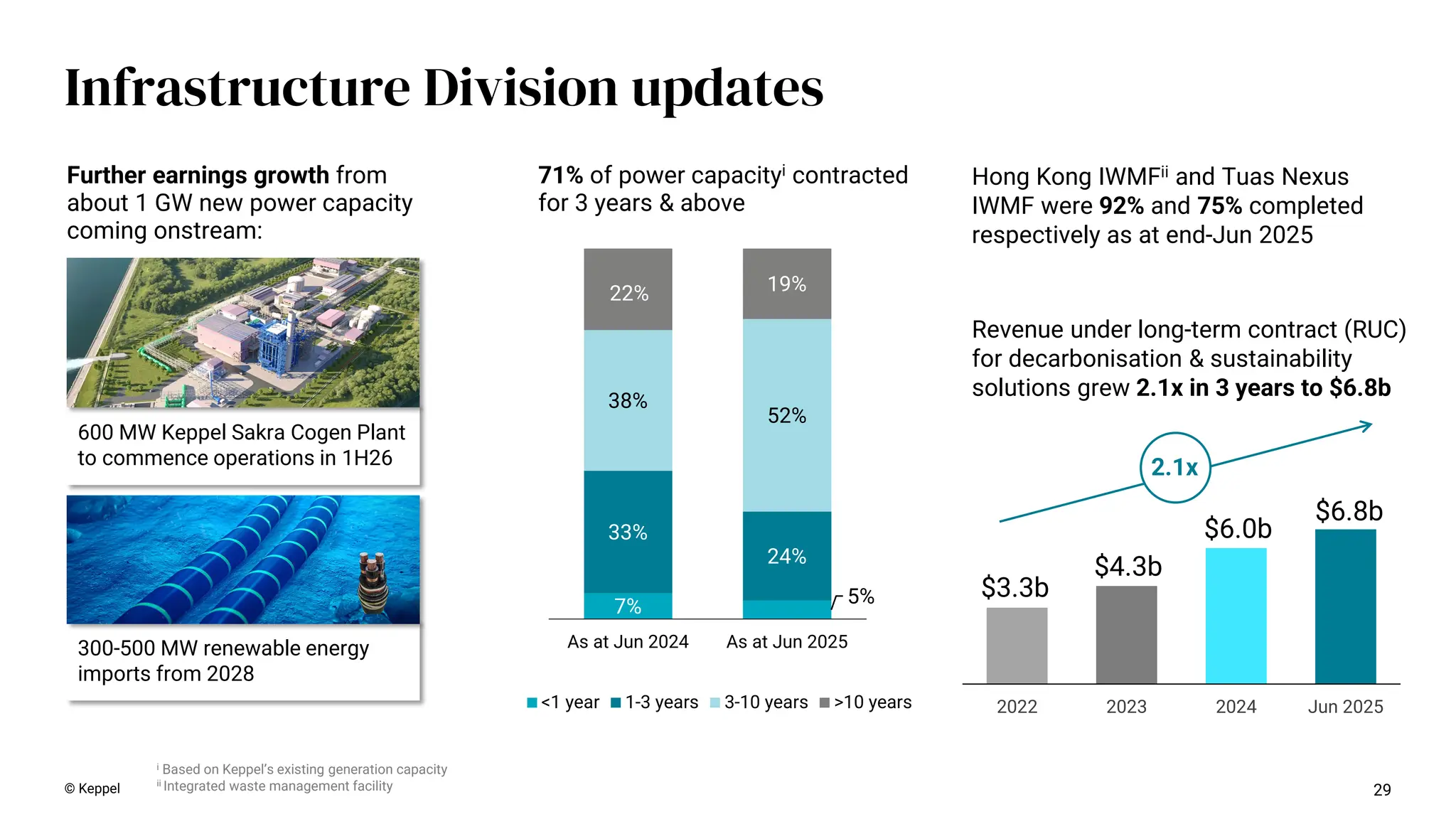

29 Infrastructure Division updates ©

Keppel i Based on Keppel’s existing generation capacity ii Integrated waste management facility Hong Kong IWMFii and Tuas Nexus IWMF were 92% and 75% completed respectively as at end-Jun 2025 Revenue under long-term contract (RUC) for decarbonisation & sustainability solutions grew 2.1x in 3 years to $6.8b 7% 5% 33% 24% 38% 52% 22% 19% As at Jun 2024 As at Jun 2025 <1 year 1-3 years 3-10 years >10 years 71% of power capacityi contracted for 3 years & above 2022 2023 2024 Jun 2025 $6.0b $4.3b $3.3b $6.8b 2.1x Further earnings growth from about 1 GW new power capacity coming onstream: 600 MW Keppel Sakra Cogen Plant to commence operations in 1H26 300-500 MW renewable energy imports from 2028

30.

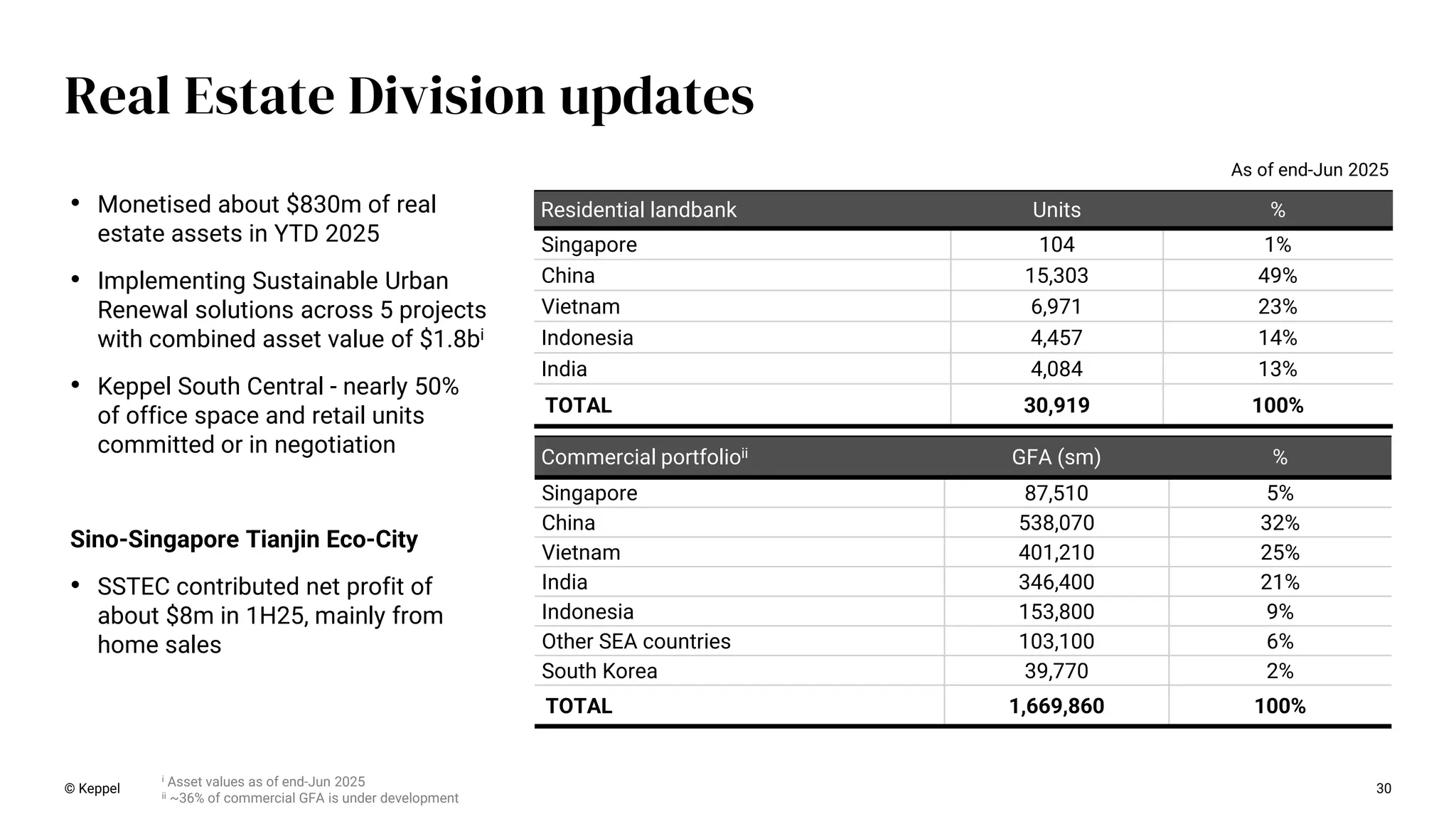

30 Real Estate Division

updates Residential landbank Units % Singapore 104 1% China 15,303 49% Vietnam 6,971 23% Indonesia 4,457 14% India 4,084 13% TOTAL 30,919 100% Commercial portfolioii GFA (sm) % Singapore 87,510 5% China 538,070 32% Vietnam 401,210 25% India 346,400 21% Indonesia 153,800 9% Other SEA countries 103,100 6% South Korea 39,770 2% TOTAL 1,669,860 100% © Keppel • Monetised about $830m of real estate assets in YTD 2025 • Implementing Sustainable Urban Renewal solutions across 5 projects with combined asset value of $1.8bi • Keppel South Central - nearly 50% of office space and retail units committed or in negotiation Sino-Singapore Tianjin Eco-City • SSTEC contributed net profit of about $8m in 1H25, mainly from home sales As of end-Jun 2025 i Asset values as of end-Jun 2025 ii ~36% of commercial GFA is under development

31.

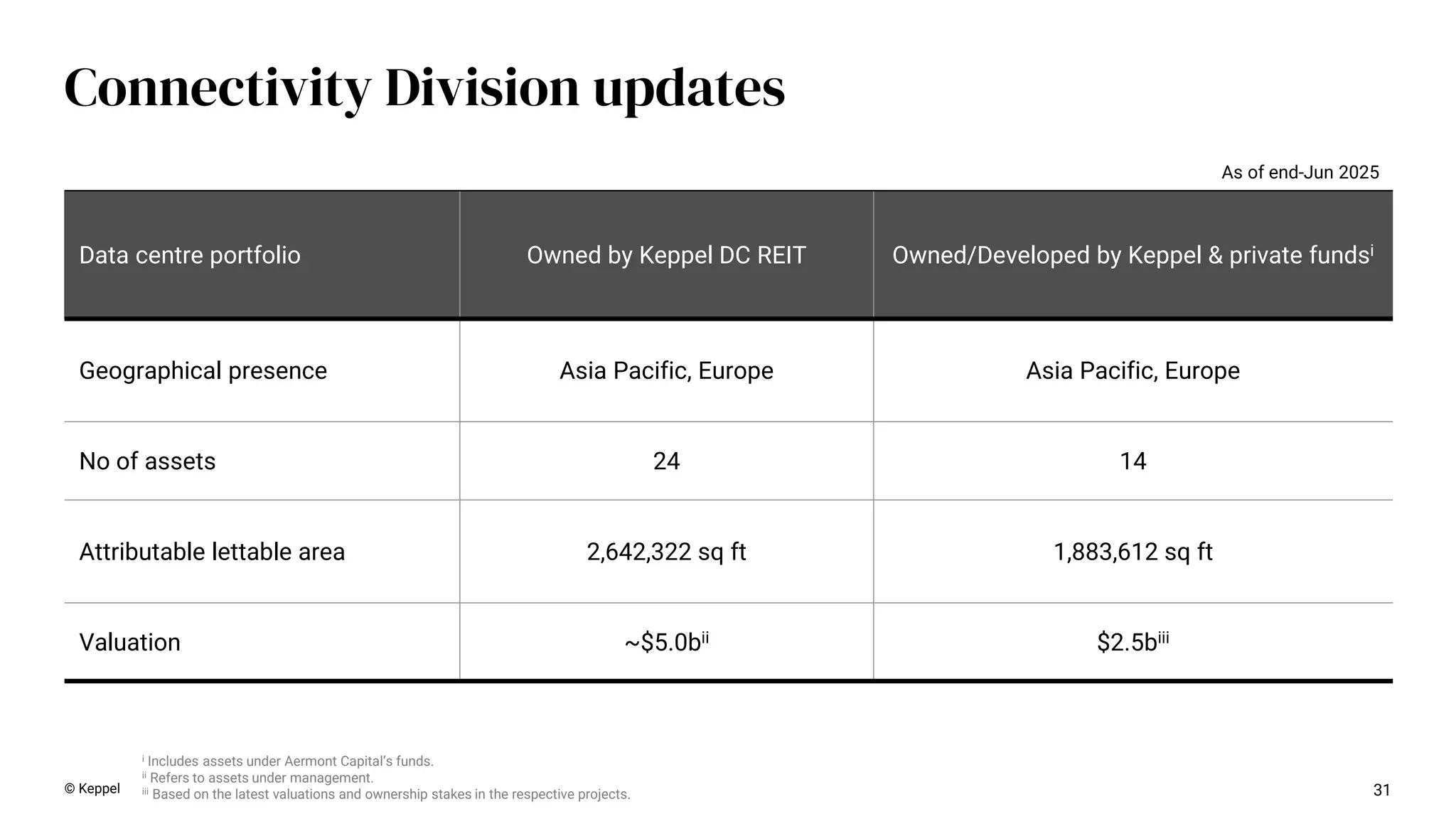

Data centre portfolio

Owned by Keppel DC REIT Owned/Developed by Keppel & private fundsi Geographical presence Asia Pacific, Europe Asia Pacific, Europe No of assets 24 14 Attributable lettable area 2,642,322 sq ft 1,883,612 sq ft Valuation ~$5.0bii $2.5biii As of end-Jun 2025 i Includes assets under Aermont Capital’s funds. ii Refers to assets under management. iii Based on the latest valuations and ownership stakes in the respective projects. 31 Connectivity Division updates © Keppel

32.

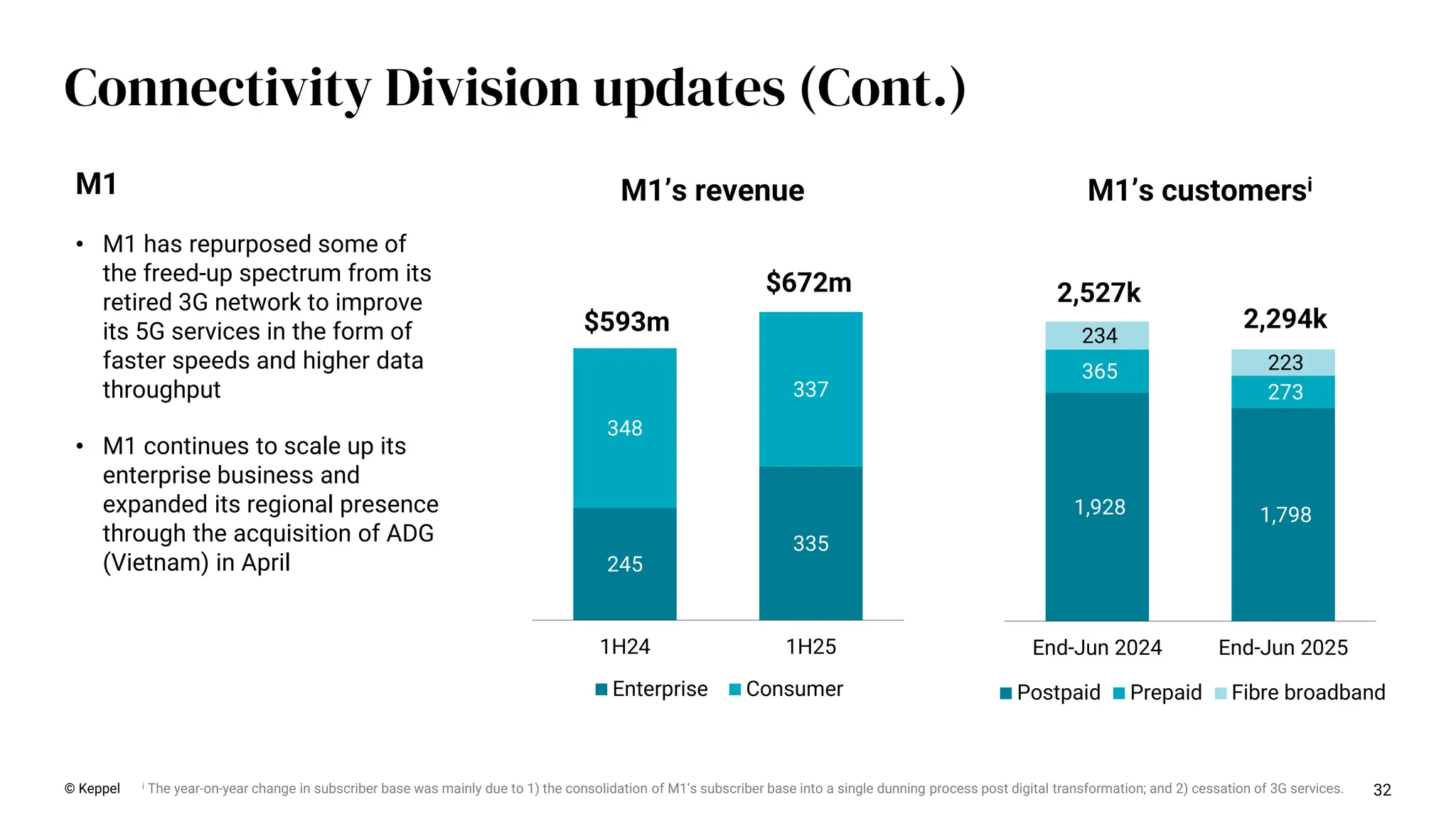

32 Connectivity Division updates

(Cont.) © Keppel 1,928 1,798 365 273 234 223 End-Jun 2024 End-Jun 2025 Postpaid Prepaid Fibre broadband 2,527k 2,294k 245 335 348 337 1H24 1H25 Enterprise Consumer $593m $672m M1’s customersi M1’s revenue M1 • M1 has repurposed some of the freed-up spectrum from its retired 3G network to improve its 5G services in the form of faster speeds and higher data throughput • M1 continues to scale up its enterprise business and expanded its regional presence through the acquisition of ADG (Vietnam) in April i The year-on-year change in subscriber base was mainly due to 1) the consolidation of M1‘s subscriber base into a single dunning process post digital transformation; and 2) cessation of 3G services.

33.

© Keppel 33 Period

Value ($m) 2020 1,238 2021 1,666 2022 1,515 2023 947 2024 1,525 YTD 2025 915 TOTAL 7,806 Asset Country Value ($m) 22.6% stake in Saigon Centre Phase 3 Vietnam 98 42% stake in Palm City Vietnam 141 29.52% stake in Keppel Philippines Holdings Inc Philippines 11 30% stake in Tianjin Fulong China 93 20.5% stake in Computer Generated Solutions, Inc 75.8% stake in Wanjiang Logistics Park US China 80 One Paramounti India 379 Nam Long shares Vietnam 58 30% stake in residential project in Ho Chi Minh Cityi Vietnam 25 2.5% stake in Smartworks India 15 Othersii - 15 YTD 2025 915 Announced since the start of asset monetisation programme in Oct 2020 Vision 2030 asset monetisation i Proposed divestment is subject to completion/relevant approvals. ii Includes other non-core assets in Australia, Thailand, China and Singapore.

34.

Appendices -Additional financial information 03 34

35.

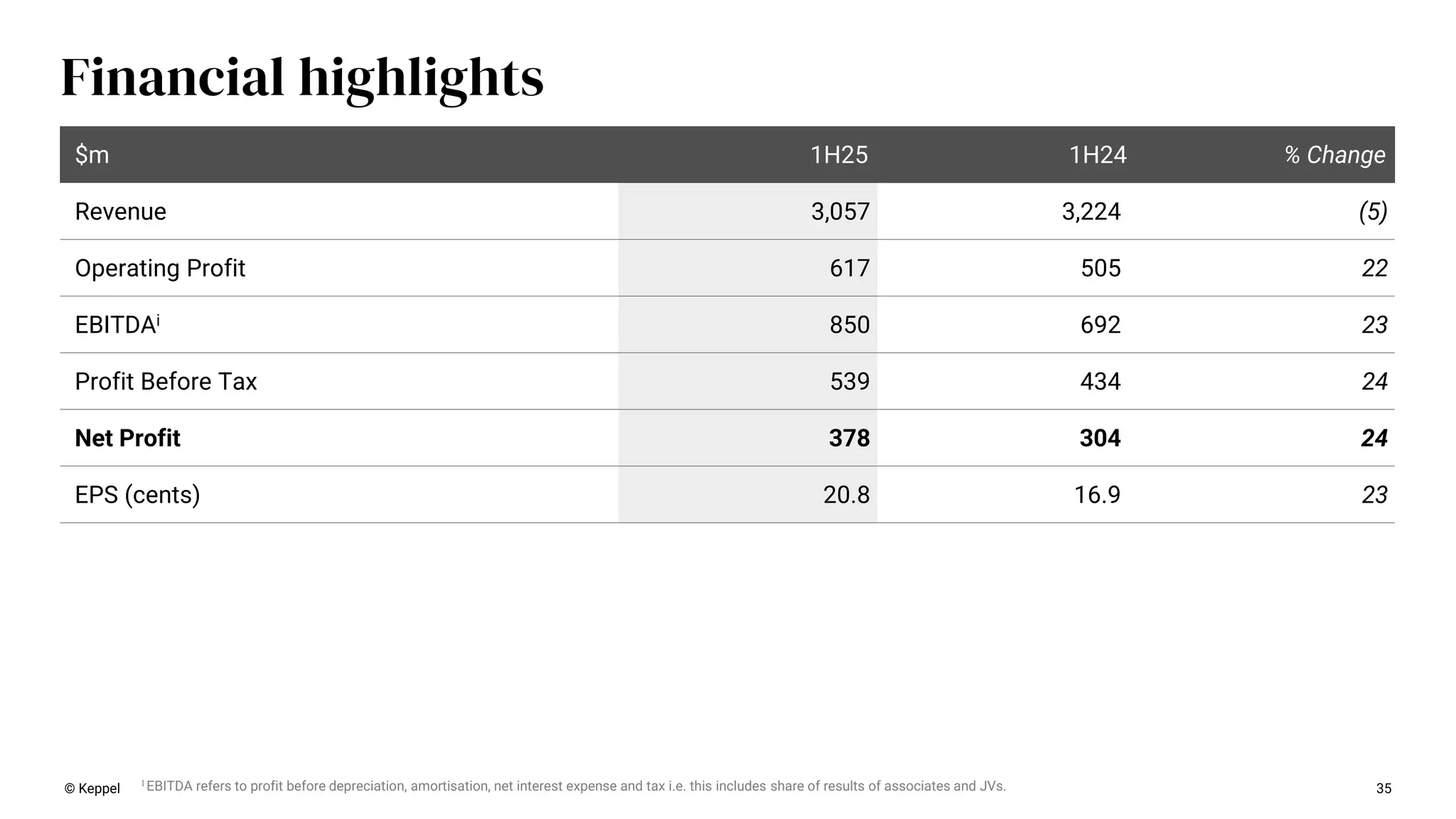

$m 1H25 1H24

% Change Revenue 3,057 3,224 (5) Operating Profit 617 505 22 EBITDAi 850 692 23 Profit Before Tax 539 434 24 Net Profit 378 304 24 EPS (cents) 20.8 16.9 23 Financial highlights © Keppel 35 I EBITDA refers to profit before depreciation, amortisation, net interest expense and tax i.e. this includes share of results of associates and JVs.

36.

75 71 339 373 1H24

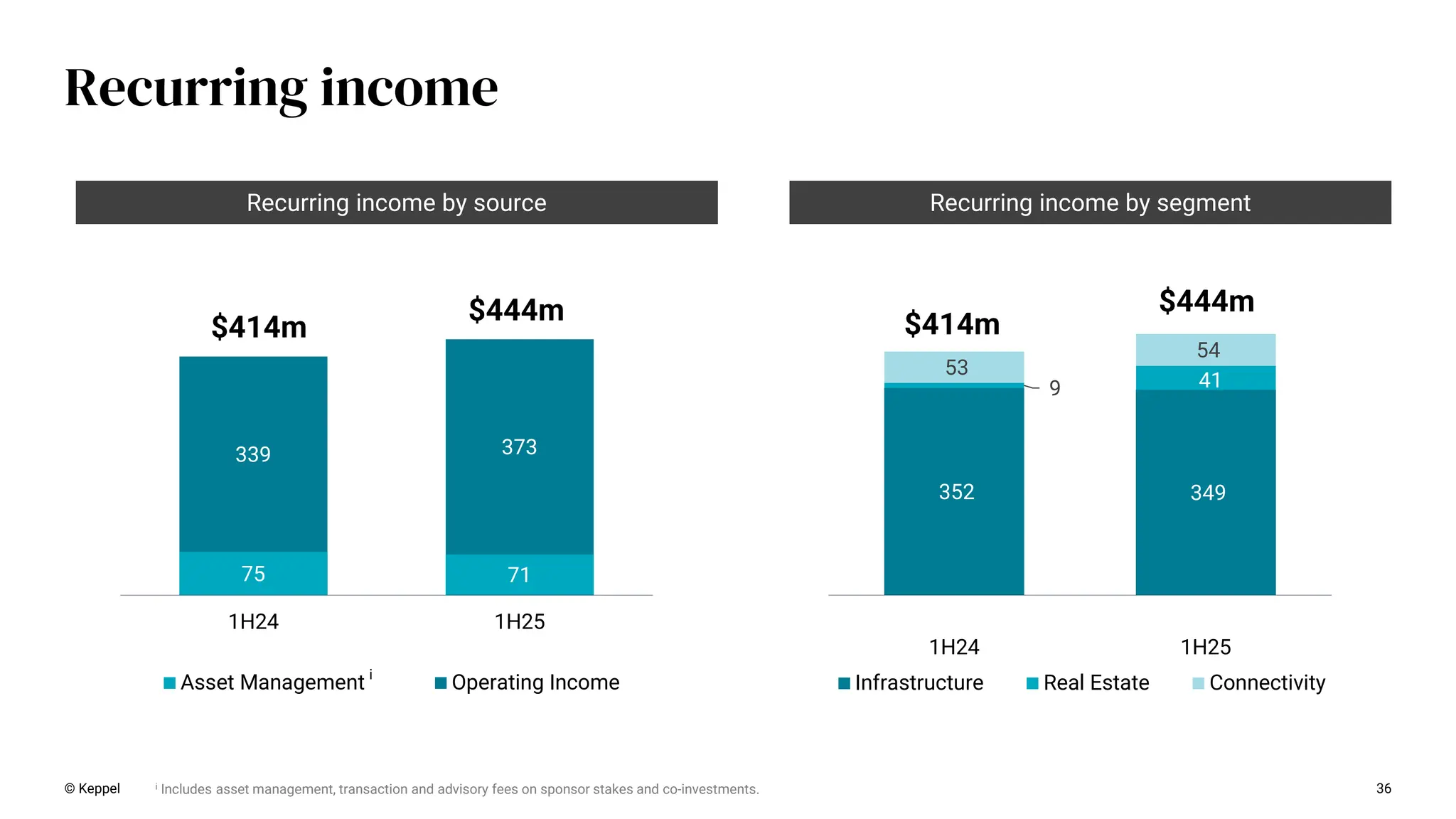

1H25 Asset Management Operating Income $414m $444m 352 349 9 41 53 54 1H24 1H25 Infrastructure Real Estate Connectivity $444m $414m Recurring income by segment Recurring income by source 36 © Keppel Recurring income i Includes asset management, transaction and advisory fees on sponsor stakes and co-investments. i

37.

Infrastructure Segment 37 $m 1H25

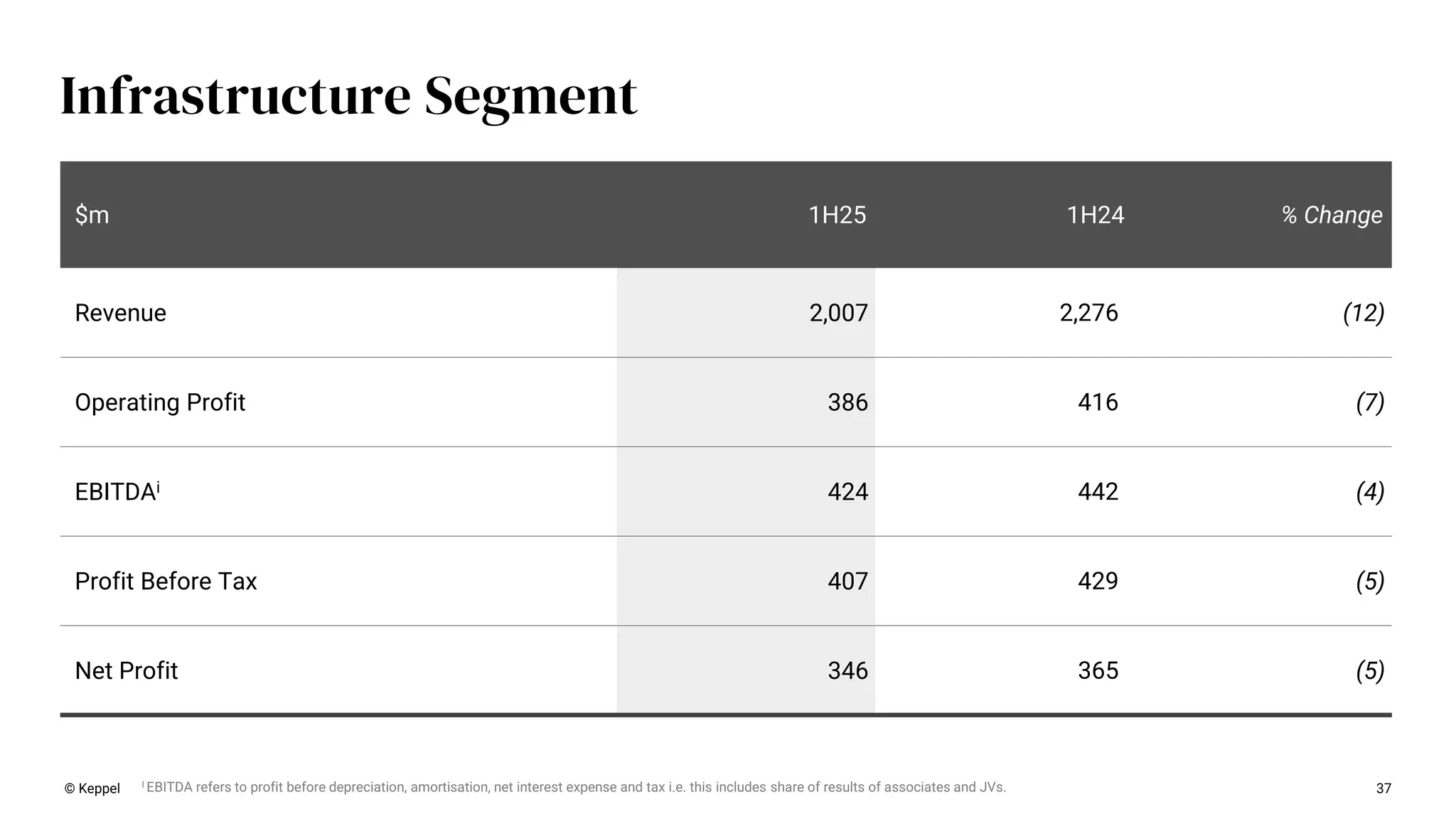

1H24 % Change Revenue 2,007 2,276 (12) Operating Profit 386 416 (7) EBITDAi 424 442 (4) Profit Before Tax 407 429 (5) Net Profit 346 365 (5) © Keppel I EBITDA refers to profit before depreciation, amortisation, net interest expense and tax i.e. this includes share of results of associates and JVs.

38.

38 Real Estate Segment $m

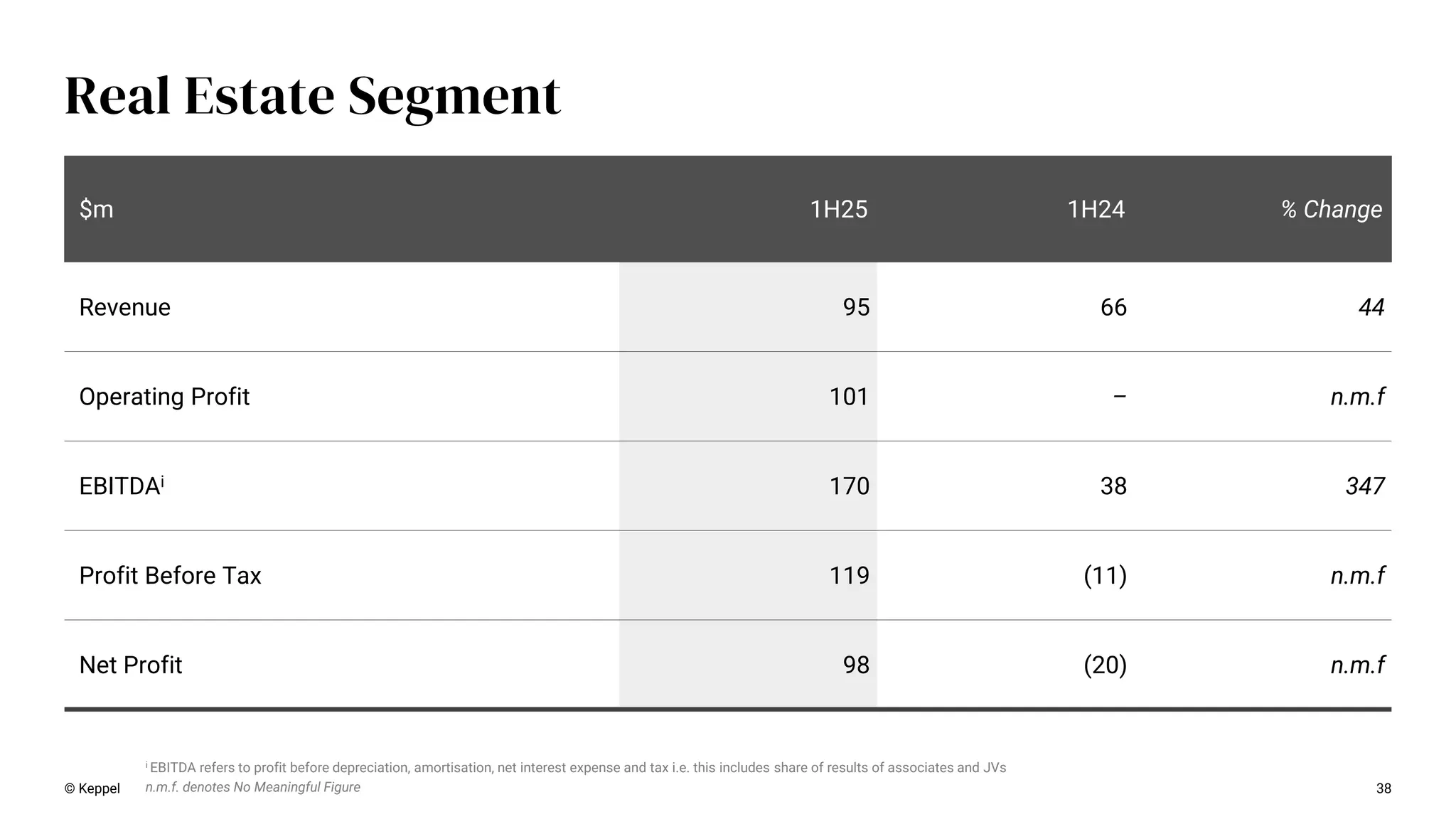

1H25 1H24 % Change Revenue 95 66 44 Operating Profit 101 – n.m.f EBITDAi 170 38 347 Profit Before Tax 119 (11) n.m.f Net Profit 98 (20) n.m.f © Keppel n.m.f. denotes No Meaningful Figure i EBITDA refers to profit before depreciation, amortisation, net interest expense and tax i.e. this includes share of results of associates and JVs

39.

39 Connectivity Segment $m 1H25

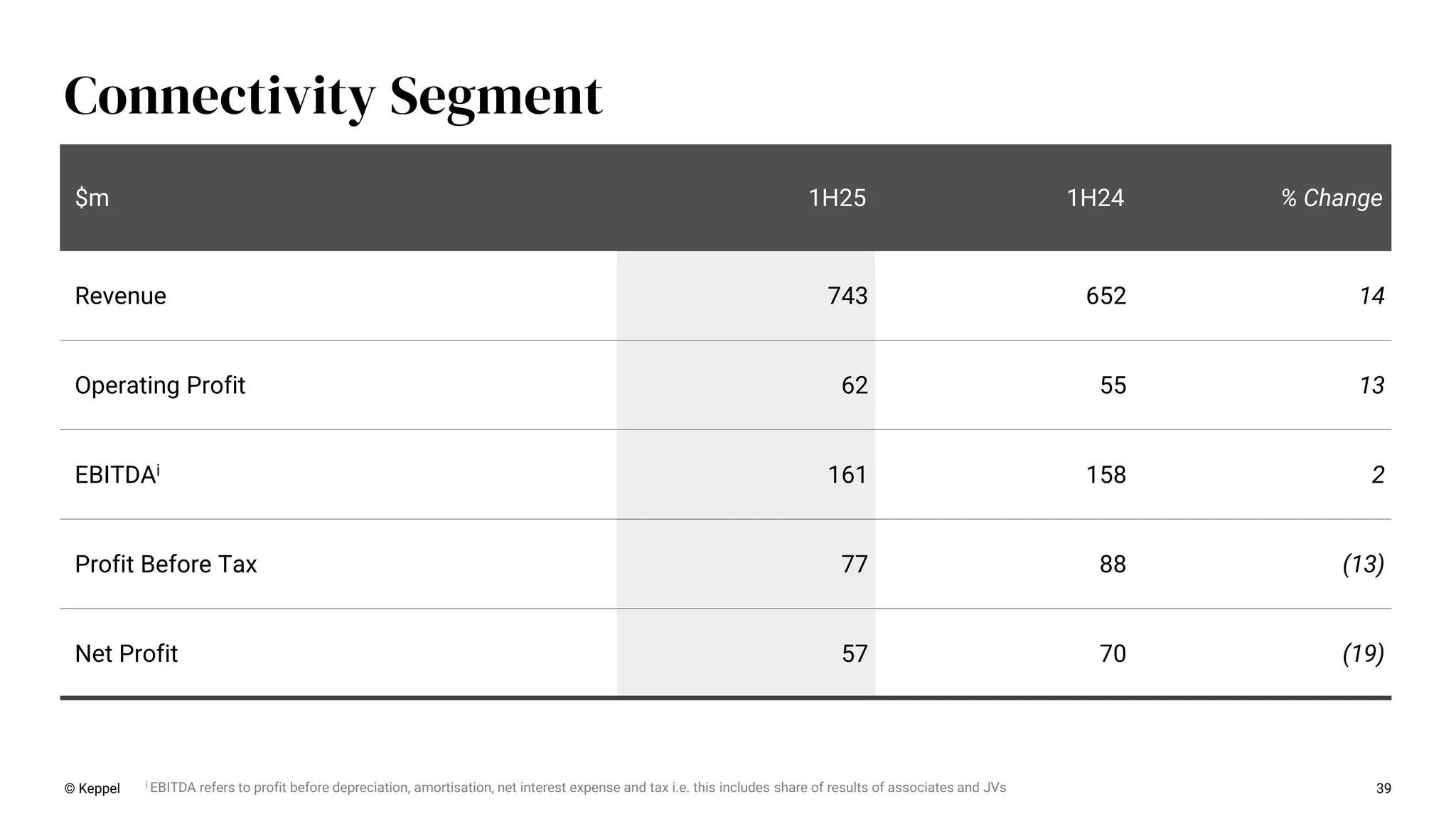

1H24 % Change Revenue 743 652 14 Operating Profit 62 55 13 EBITDAi 161 158 2 Profit Before Tax 77 88 (13) Net Profit 57 70 (19) © Keppel i EBITDA refers to profit before depreciation, amortisation, net interest expense and tax i.e. this includes share of results of associates and JVs

40.

40 Non-Core Portfolio for

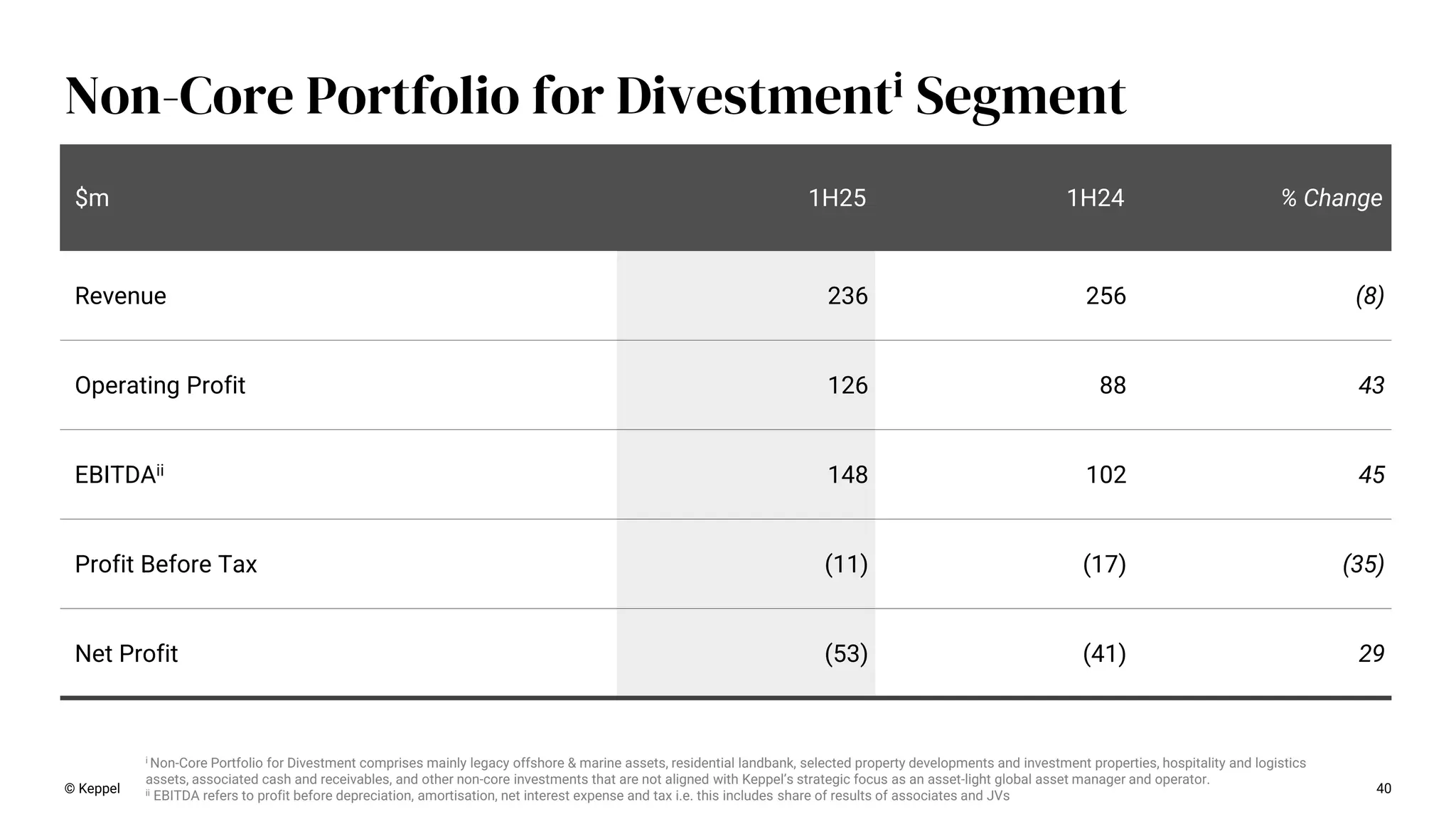

Divestmenti Segment $m 1H25 1H24 % Change Revenue 236 256 (8) Operating Profit 126 88 43 EBITDAii 148 102 45 Profit Before Tax (11) (17) (35) Net Profit (53) (41) 29 © Keppel i Non-Core Portfolio for Divestment comprises mainly legacy offshore & marine assets, residential landbank, selected property developments and investment properties, hospitality and logistics assets, associated cash and receivables, and other non-core investments that are not aligned with Keppel’s strategic focus as an asset-light global asset manager and operator. ii EBITDA refers to profit before depreciation, amortisation, net interest expense and tax i.e. this includes share of results of associates and JVs

41.

• Non-Core Portfolio

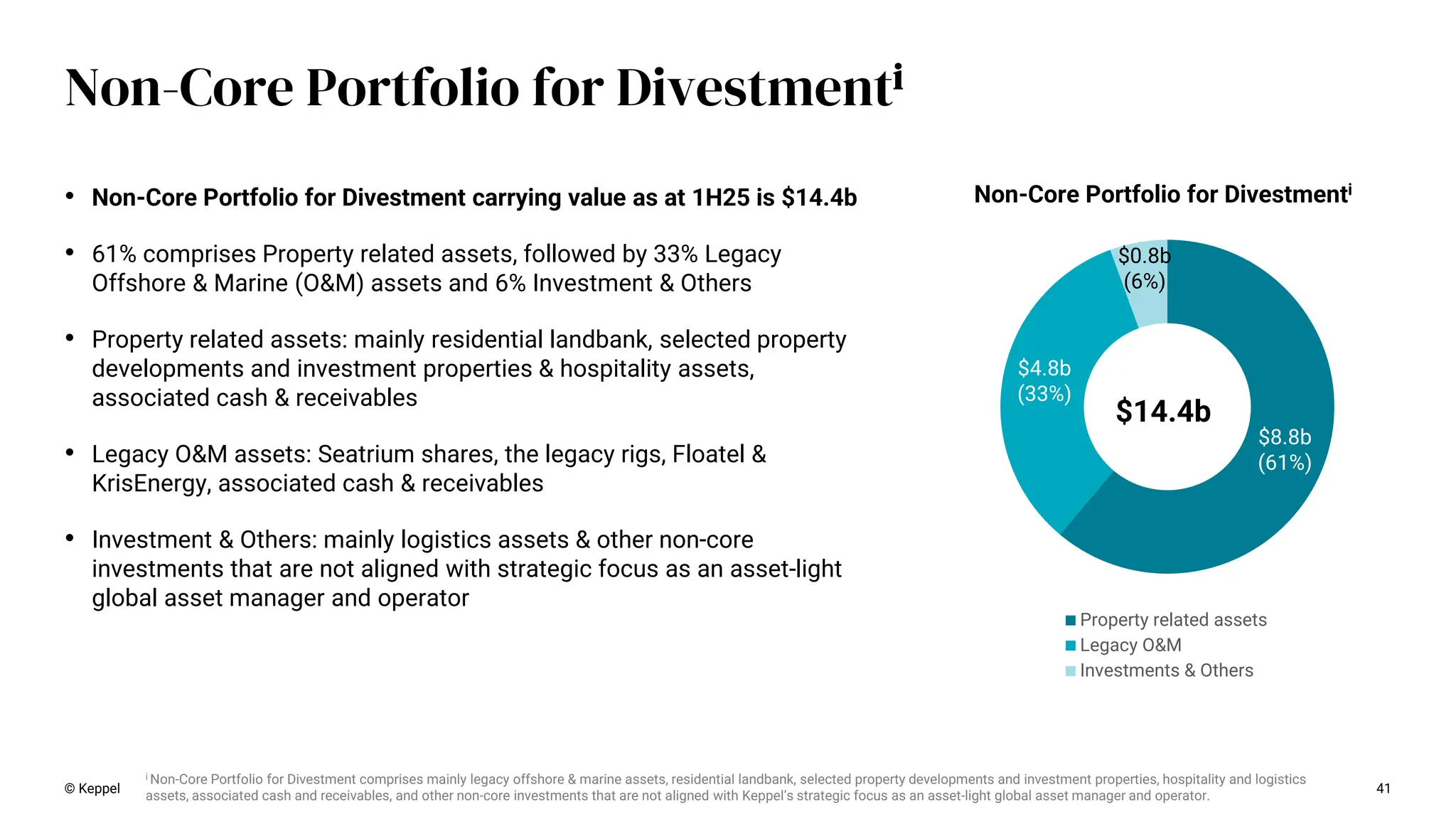

for Divestment carrying value as at 1H25 is $14.4b • 61% comprises Property related assets, followed by 33% Legacy Offshore & Marine (O&M) assets and 6% Investment & Others • Property related assets: mainly residential landbank, selected property developments and investment properties & hospitality assets, associated cash & receivables • Legacy O&M assets: Seatrium shares, the legacy rigs, Floatel & KrisEnergy, associated cash & receivables • Investment & Others: mainly logistics assets & other non-core investments that are not aligned with strategic focus as an asset-light global asset manager and operator © Keppel 41 Non-Core Portfolio for Divestmenti $8.8b (61%) $4.8b (33%) $0.8b (6%) Property related assets Legacy O&M Investments & Others $14.4b i Non-Core Portfolio for Divestment comprises mainly legacy offshore & marine assets, residential landbank, selected property developments and investment properties, hospitality and logistics assets, associated cash and receivables, and other non-core investments that are not aligned with Keppel’s strategic focus as an asset-light global asset manager and operator. Non-Core Portfolio for Divestmenti

42.

42 Net profit by

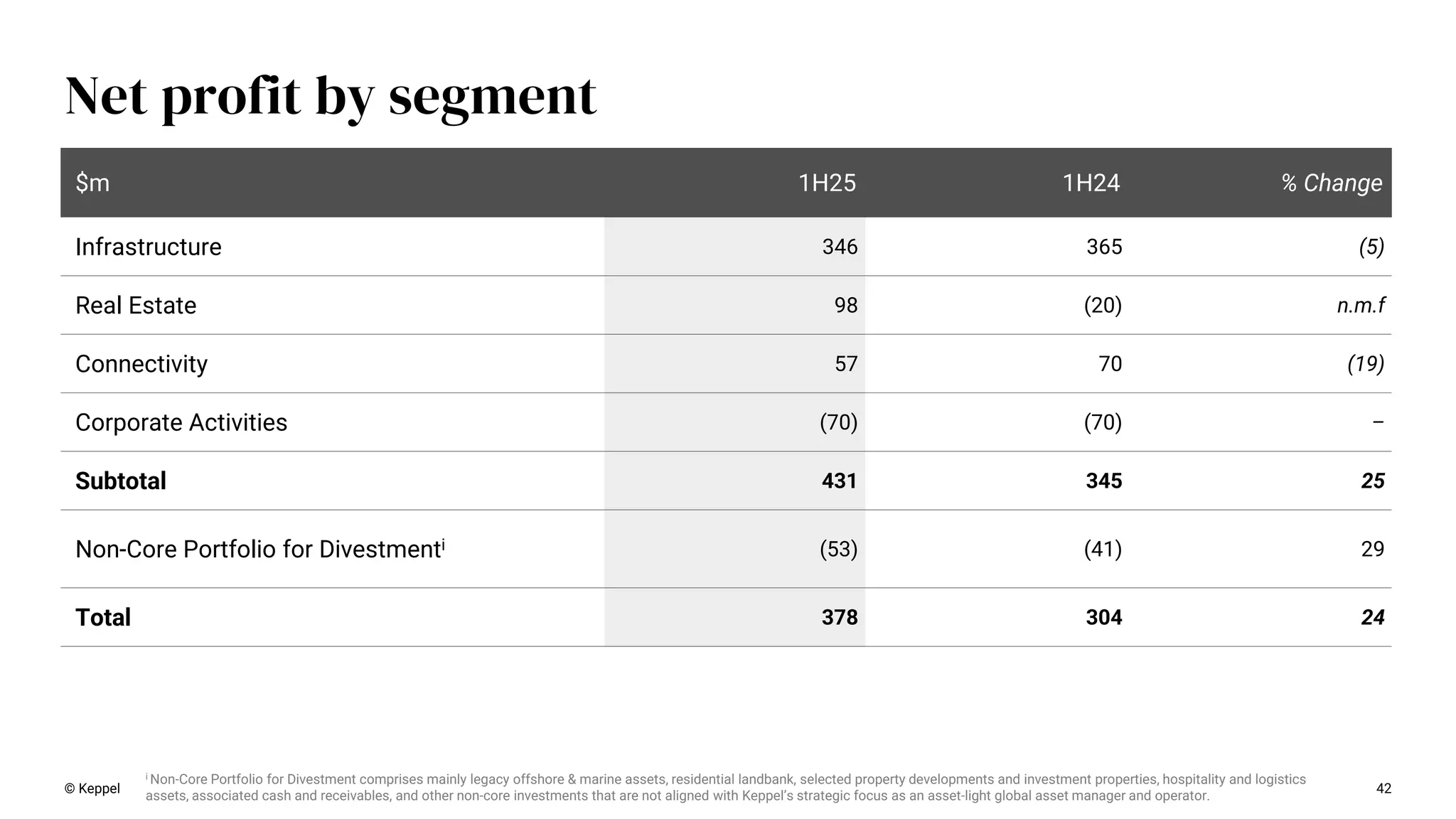

segment $m 1H25 1H24 % Change Infrastructure 346 365 (5) Real Estate 98 (20) n.m.f Connectivity 57 70 (19) Corporate Activities (70) (70) – Subtotal 431 345 25 Non-Core Portfolio for Divestmenti (53) (41) 29 Total 378 304 24 © Keppel i Non-Core Portfolio for Divestment comprises mainly legacy offshore & marine assets, residential landbank, selected property developments and investment properties, hospitality and logistics assets, associated cash and receivables, and other non-core investments that are not aligned with Keppel’s strategic focus as an asset-light global asset manager and operator.

43.

© Keppel 43 1H

2024 net profit (horizontal reporting) i Includes asset management, transaction and advisory fees on sponsor stakes and co-investments. ii Includes returns (net of financing costs attributable to such stakes) from equity accounted stakes in listed and private funds – Infrastructure [$8m from listed funds and -$4m from private funds]; Real Estate [$4m from listed funds and -$3m from private funds], and Connectivity [$11m from listed funds and -$3m from private funds]. iii Includes overheads and financing costs which have not been attributed to segments. iv Non-Core Portfolio for Divestment comprises mainly legacy offshore & marine assets, residential landbank, selected property developments and investment properties, hospitality and logistics assets, associated cash and receivables, and other non-core investments that are not aligned with Keppel’s strategic focus as an asset-light global asset manager and operator. ($’m) Asset Managementi Operatingii Valuation Capital recycling Net profit Infrastructure 44 308 12 1 365 106% Real Estate 19 (10) (29) – (20) (6%) Connectivity 12 41 12 5 70 20% Corporate activitiesiii (70) (20%) New Keppel 75 339 (5) 6 345 100% Non-Core Portfolio for Divestmentiv (41) Net profit 75 339 (5) 6 304

44.

© Keppel 44 Free

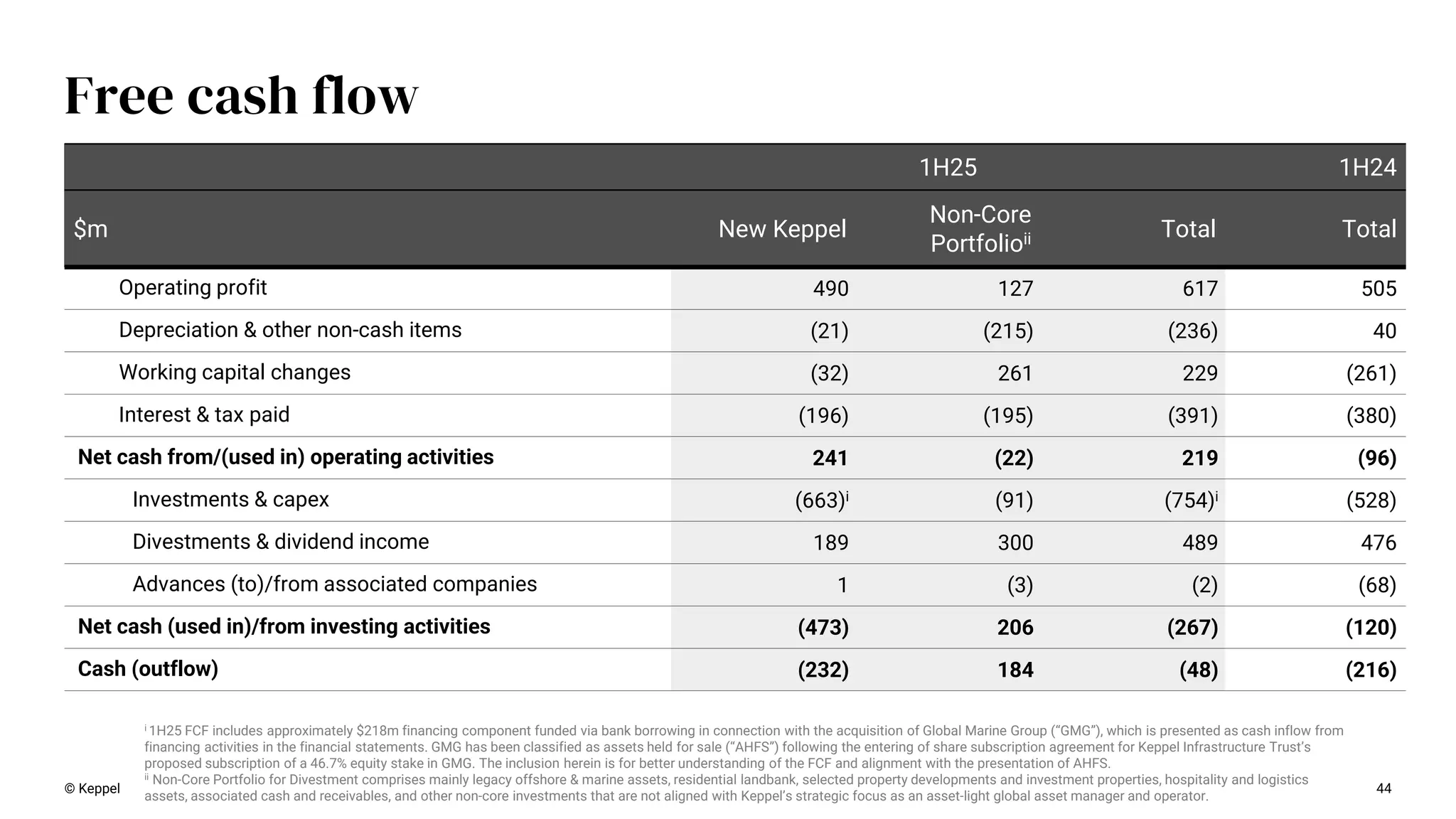

cash flow 1H25 1H24 $m New Keppel Non-Core Portfolioii Total Total Operating profit 490 127 617 505 Depreciation & other non-cash items (21) (215) (236) 40 Working capital changes (32) 261 229 (261) Interest & tax paid (196) (195) (391) (380) Net cash from/(used in) operating activities 241 (22) 219 (96) Investments & capex (663)i (91) (754)i (528) Divestments & dividend income 189 300 489 476 Advances (to)/from associated companies 1 (3) (2) (68) Net cash (used in)/from investing activities (473) 206 (267) (120) Cash (outflow) (232) 184 (48) (216) i 1H25 FCF includes approximately $218m financing component funded via bank borrowing in connection with the acquisition of Global Marine Group (“GMG”), which is presented as cash inflow from financing activities in the financial statements. GMG has been classified as assets held for sale (“AHFS”) following the entering of share subscription agreement for Keppel Infrastructure Trust’s proposed subscription of a 46.7% equity stake in GMG. The inclusion herein is for better understanding of the FCF and alignment with the presentation of AHFS. ii Non-Core Portfolio for Divestment comprises mainly legacy offshore & marine assets, residential landbank, selected property developments and investment properties, hospitality and logistics assets, associated cash and receivables, and other non-core investments that are not aligned with Keppel’s strategic focus as an asset-light global asset manager and operator.

45.

Appendices -Additional Real Estate information 03 45

46.

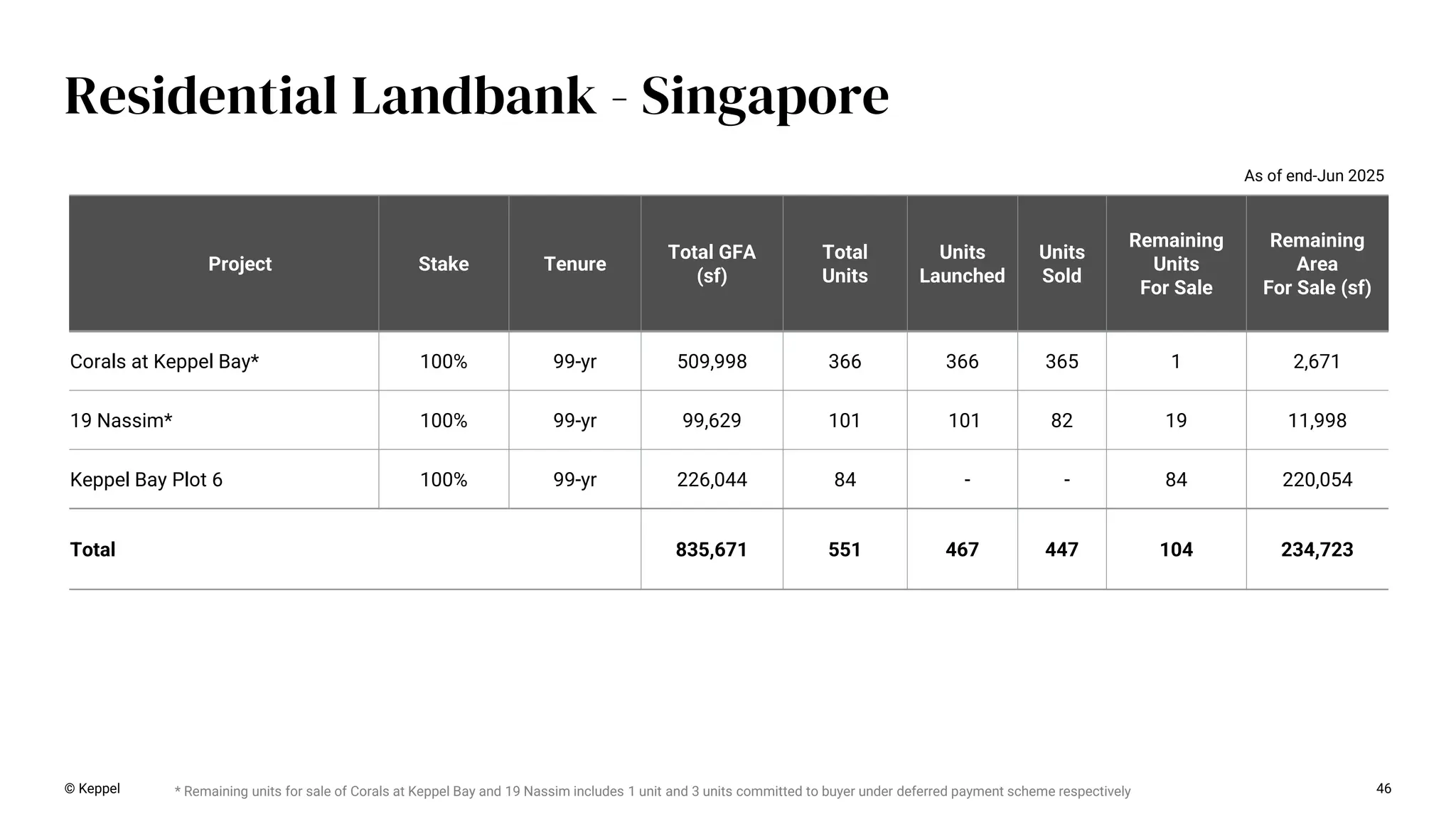

46 Residential Landbank -

Singapore Project Stake Tenure Total GFA (sf) Total Units Units Launched Units Sold Remaining Units For Sale Remaining Area For Sale (sf) Corals at Keppel Bay* 100% 99-yr 509,998 366 366 365 1 2,671 19 Nassim* 100% 99-yr 99,629 101 101 82 19 11,998 Keppel Bay Plot 6 100% 99-yr 226,044 84 - - 84 220,054 Total 835,671 551 467 447 104 234,723 * Remaining units for sale of Corals at Keppel Bay and 19 Nassim includes 1 unit and 3 units committed to buyer under deferred payment scheme respectively As of end-Jun 2025 © Keppel

47.

47 Residential Landbank -

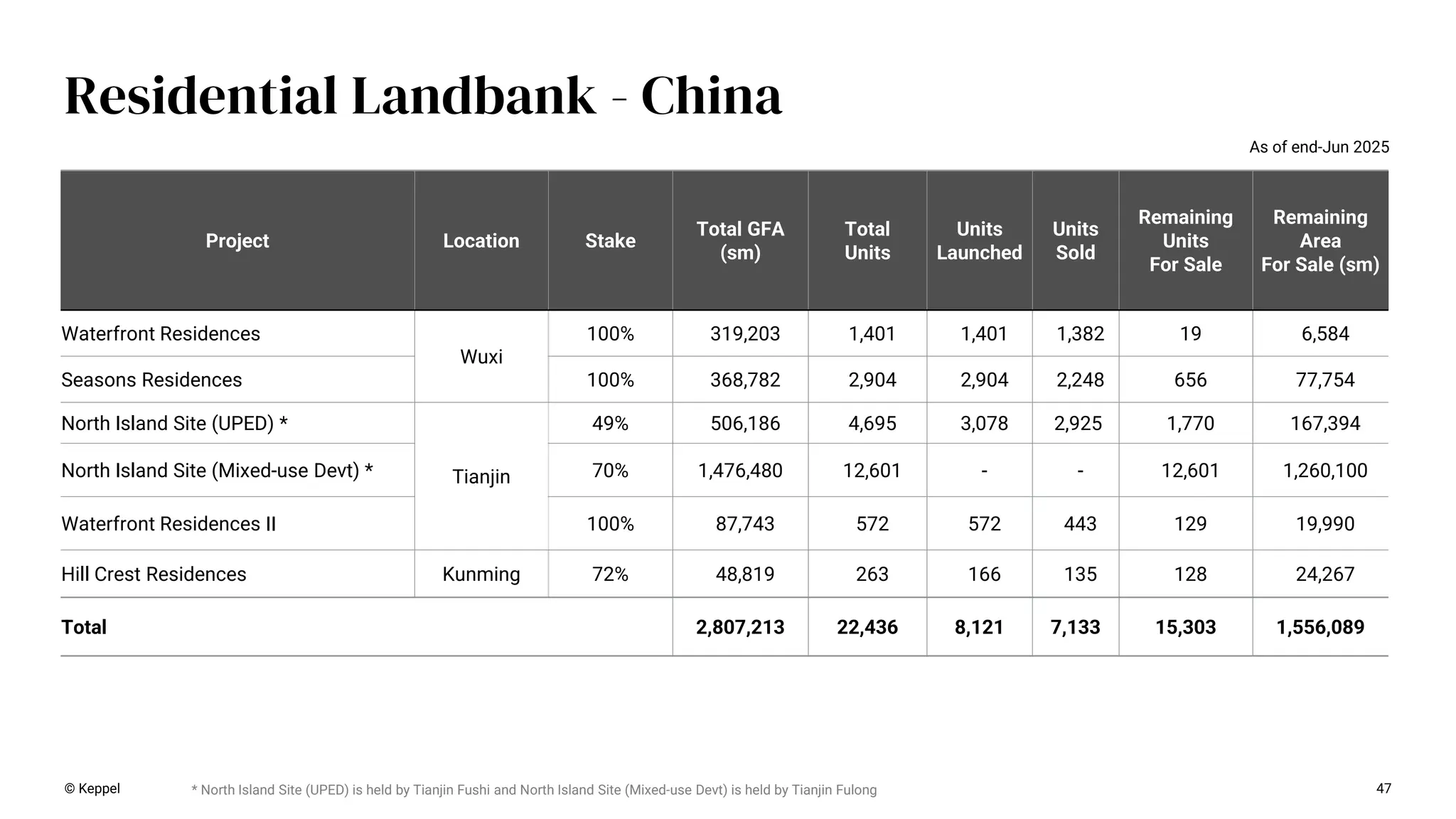

China Project Location Stake Total GFA (sm) Total Units Units Launched Units Sold Remaining Units For Sale Remaining Area For Sale (sm) Waterfront Residences Wuxi 100% 319,203 1,401 1,401 1,382 19 6,584 Seasons Residences 100% 368,782 2,904 2,904 2,248 656 77,754 North Island Site (UPED) * Tianjin 49% 506,186 4,695 3,078 2,925 1,770 167,394 North Island Site (Mixed-use Devt) * 70% 1,476,480 12,601 - - 12,601 1,260,100 Waterfront Residences II 100% 87,743 572 572 443 129 19,990 Hill Crest Residences Kunming 72% 48,819 263 166 135 128 24,267 Total 2,807,213 22,436 8,121 7,133 15,303 1,556,089 As of end-Jun 2025 © Keppel * North Island Site (UPED) is held by Tianjin Fushi and North Island Site (Mixed-use Devt) is held by Tianjin Fulong

48.

48 Residential Landbank -

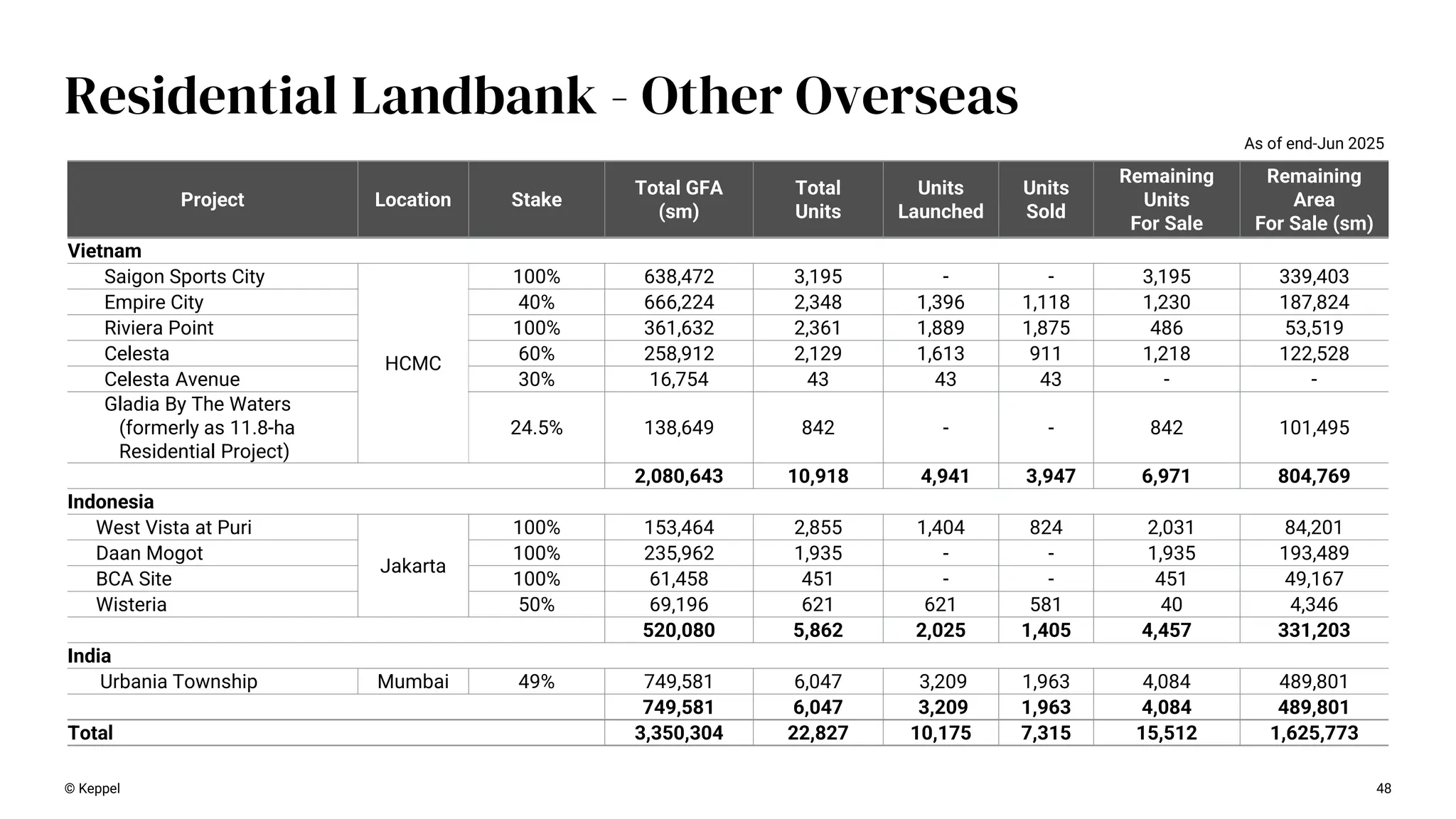

Other Overseas Project Location Stake Total GFA (sm) Total Units Units Launched Units Sold Remaining Units For Sale Remaining Area For Sale (sm) Vietnam Saigon Sports City HCMC 100% 638,472 3,195 - - 3,195 339,403 Empire City 40% 666,224 2,348 1,396 1,118 1,230 187,824 Riviera Point 100% 361,632 2,361 1,889 1,875 486 53,519 Celesta 60% 258,912 2,129 1,613 911 1,218 122,528 Celesta Avenue 30% 16,754 43 43 43 - - Gladia By The Waters (formerly as 11.8-ha Residential Project) 24.5% 138,649 842 - - 842 101,495 2,080,643 10,918 4,941 3,947 6,971 804,769 Indonesia West Vista at Puri Jakarta 100% 153,464 2,855 1,404 824 2,031 84,201 Daan Mogot 100% 235,962 1,935 - - 1,935 193,489 BCA Site 100% 61,458 451 - - 451 49,167 Wisteria 50% 69,196 621 621 581 40 4,346 520,080 5,862 2,025 1,405 4,457 331,203 India Urbania Township Mumbai 49% 749,581 6,047 3,209 1,963 4,084 489,801 749,581 6,047 3,209 1,963 4,084 489,801 Total 3,350,304 22,827 10,175 7,315 15,512 1,625,773 As of end-Jun 2025 © Keppel

49.

49 Residential Launch Readiness

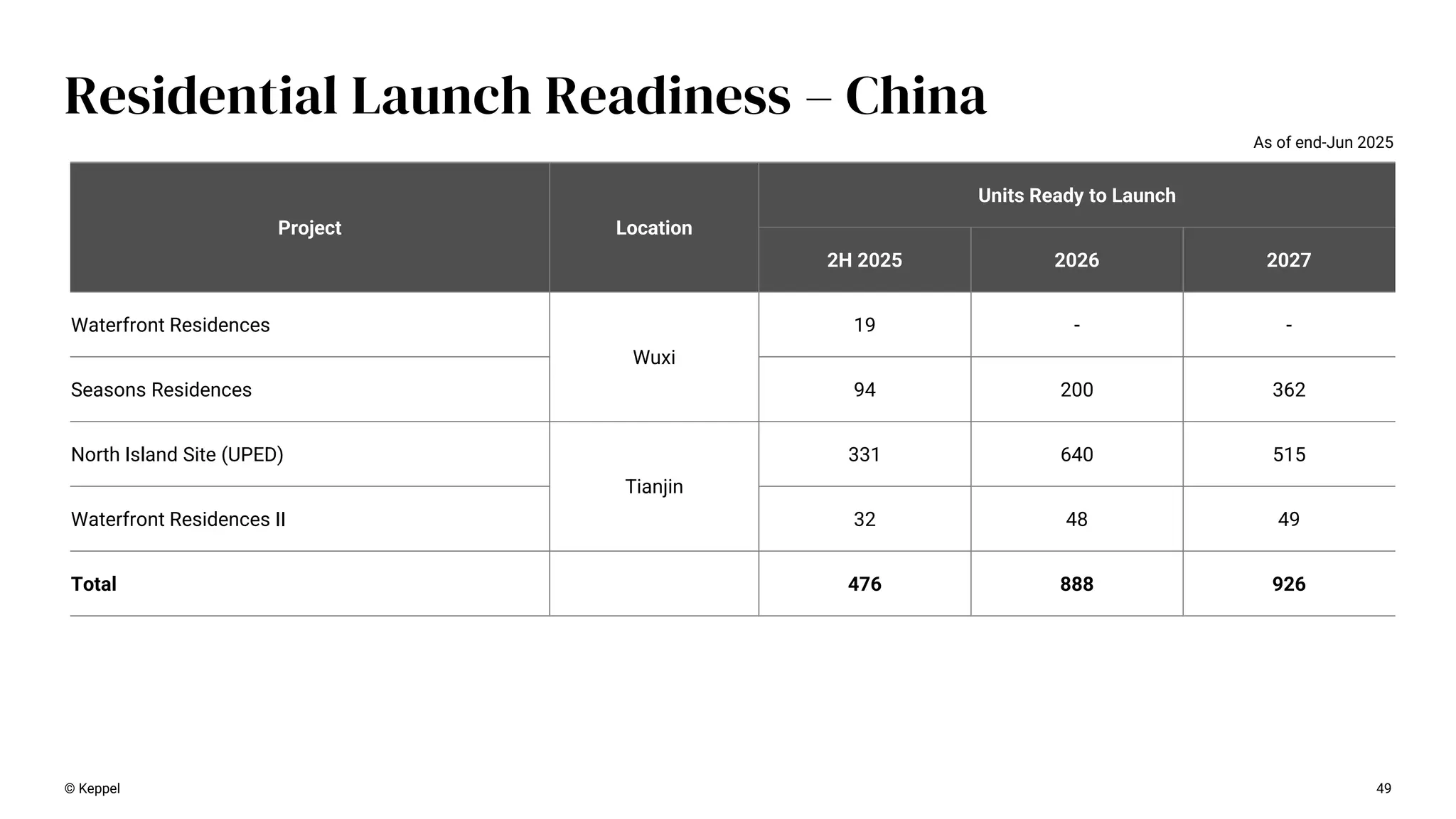

– China As of end-Jun 2025 Project Location Units Ready to Launch 2H 2025 2026 2027 Waterfront Residences Wuxi 19 - - Seasons Residences 94 200 362 North Island Site (UPED) Tianjin 331 640 515 Waterfront Residences II 32 48 49 Total 476 888 926 © Keppel

50.

50 Residential Launch Readiness

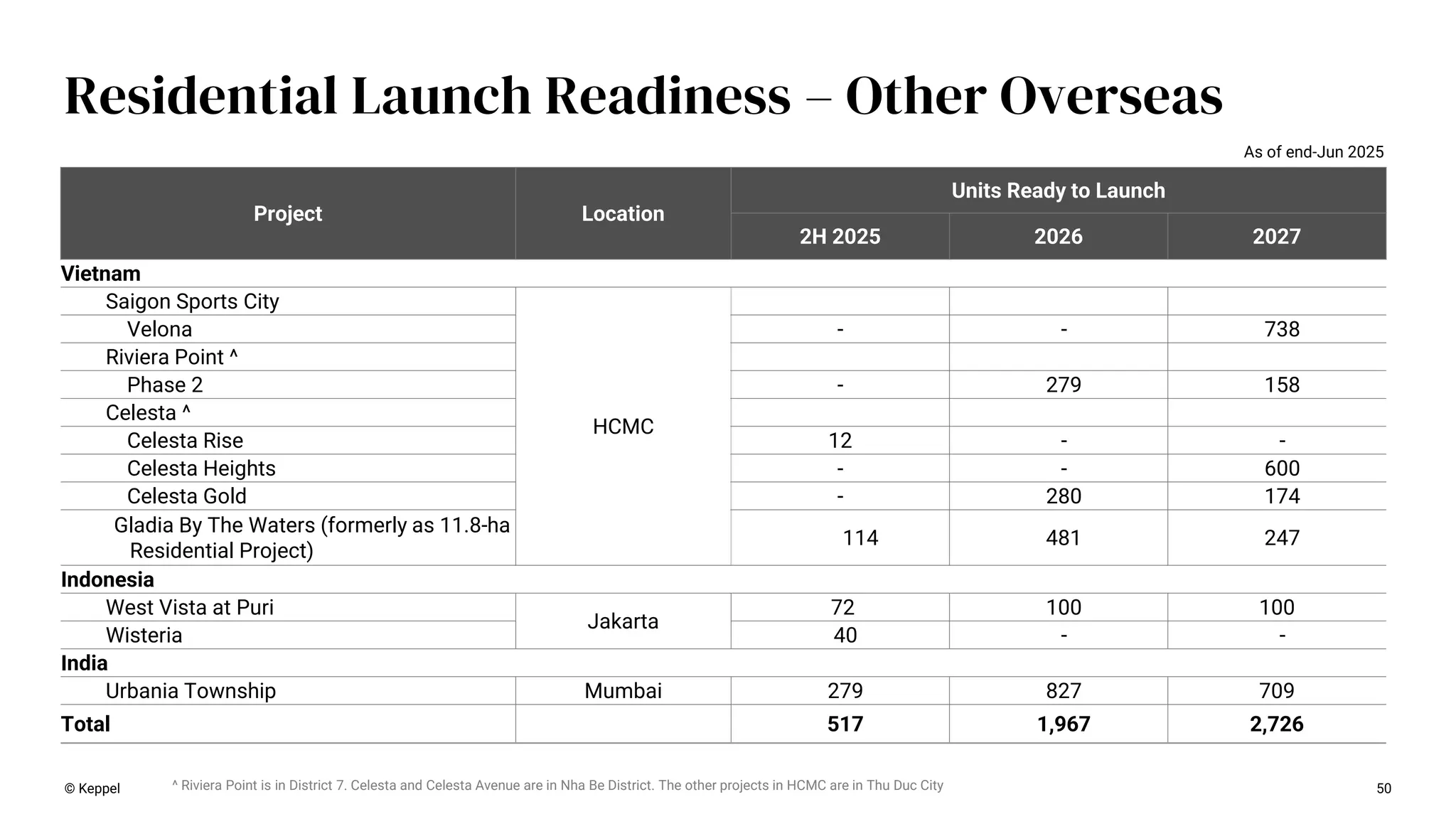

– Other Overseas Project Location Units Ready to Launch 2H 2025 2026 2027 Vietnam Saigon Sports City HCMC Velona - - 738 Riviera Point ^ Phase 2 - 279 158 Celesta ^ Celesta Rise 12 - - Celesta Heights - - 600 Celesta Gold - 280 174 Gladia By The Waters (formerly as 11.8-ha Residential Project) 114 481 247 Indonesia West Vista at Puri Jakarta 72 100 100 Wisteria 40 - - India Urbania Township Mumbai 279 827 709 Total 517 1,967 2,726 As of end-Jun 2025 ^ Riviera Point is in District 7. Celesta and Celesta Avenue are in Nha Be District. The other projects in HCMC are in Thu Duc City © Keppel

51.

51 Expected Completion for

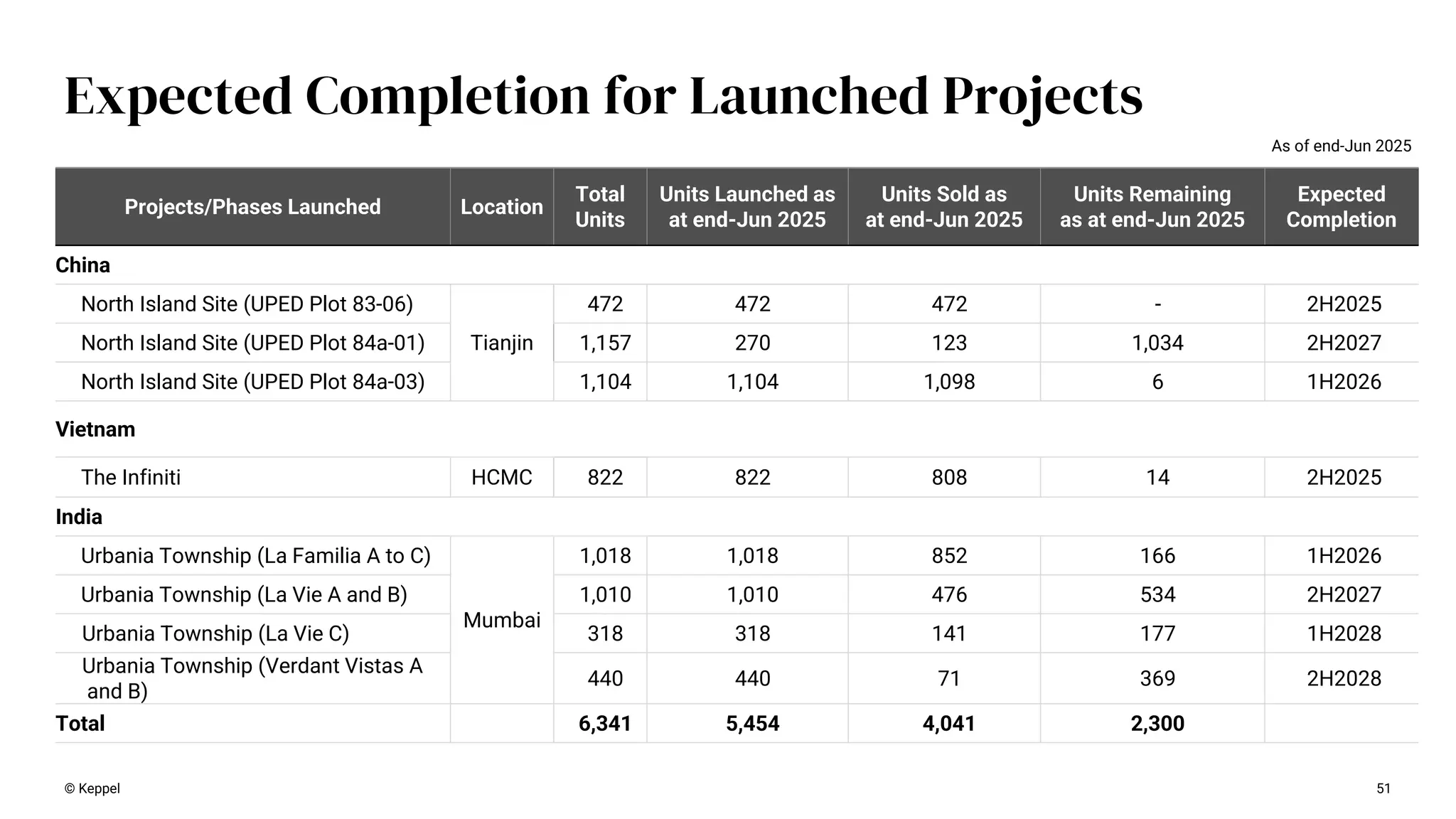

Launched Projects Projects/Phases Launched Location Total Units Units Launched as at end-Jun 2025 Units Sold as at end-Jun 2025 Units Remaining as at end-Jun 2025 Expected Completion China North Island Site (UPED Plot 83-06) Tianjin 472 472 472 - 2H2025 North Island Site (UPED Plot 84a-01) 1,157 270 123 1,034 2H2027 North Island Site (UPED Plot 84a-03) 1,104 1,104 1,098 6 1H2026 Vietnam The Infiniti HCMC 822 822 808 14 2H2025 India Urbania Township (La Familia A to C) Mumbai 1,018 1,018 852 166 1H2026 Urbania Township (La Vie A and B) 1,010 1,010 476 534 2H2027 Urbania Township (La Vie C) 318 318 141 177 1H2028 Urbania Township (Verdant Vistas A and B) 440 440 71 369 2H2028 Total 6,341 5,454 4,041 2,300 © Keppel As of end-Jun 2025

52.

52 Expected Completion for

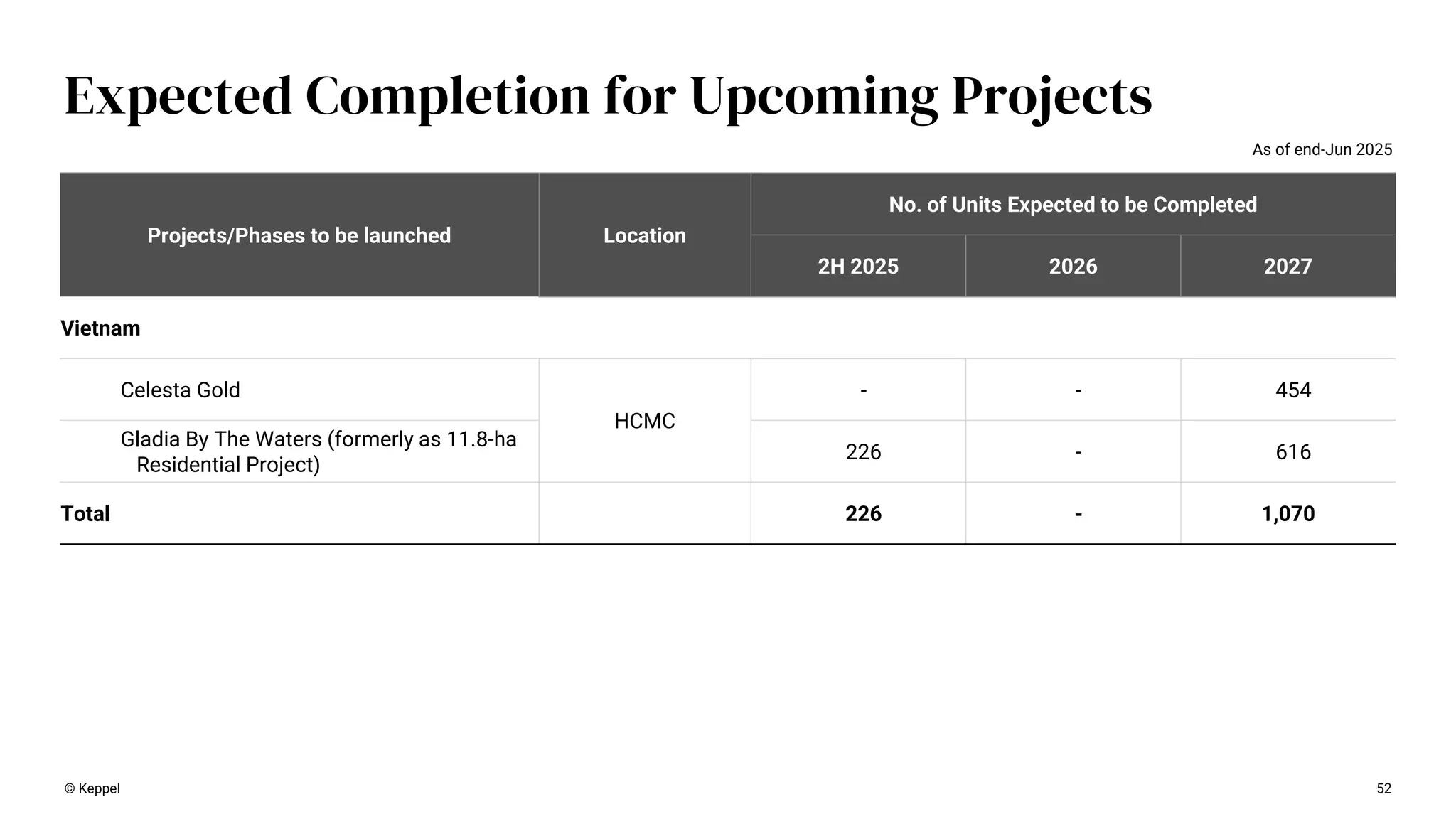

Upcoming Projects Projects/Phases to be launched Location No. of Units Expected to be Completed 2H 2025 2026 2027 Vietnam Celesta Gold HCMC - - 454 Gladia By The Waters (formerly as 11.8-ha Residential Project) 226 - 616 Total 226 - 1,070 © Keppel As of end-Jun 2025

53.

TBC: To be

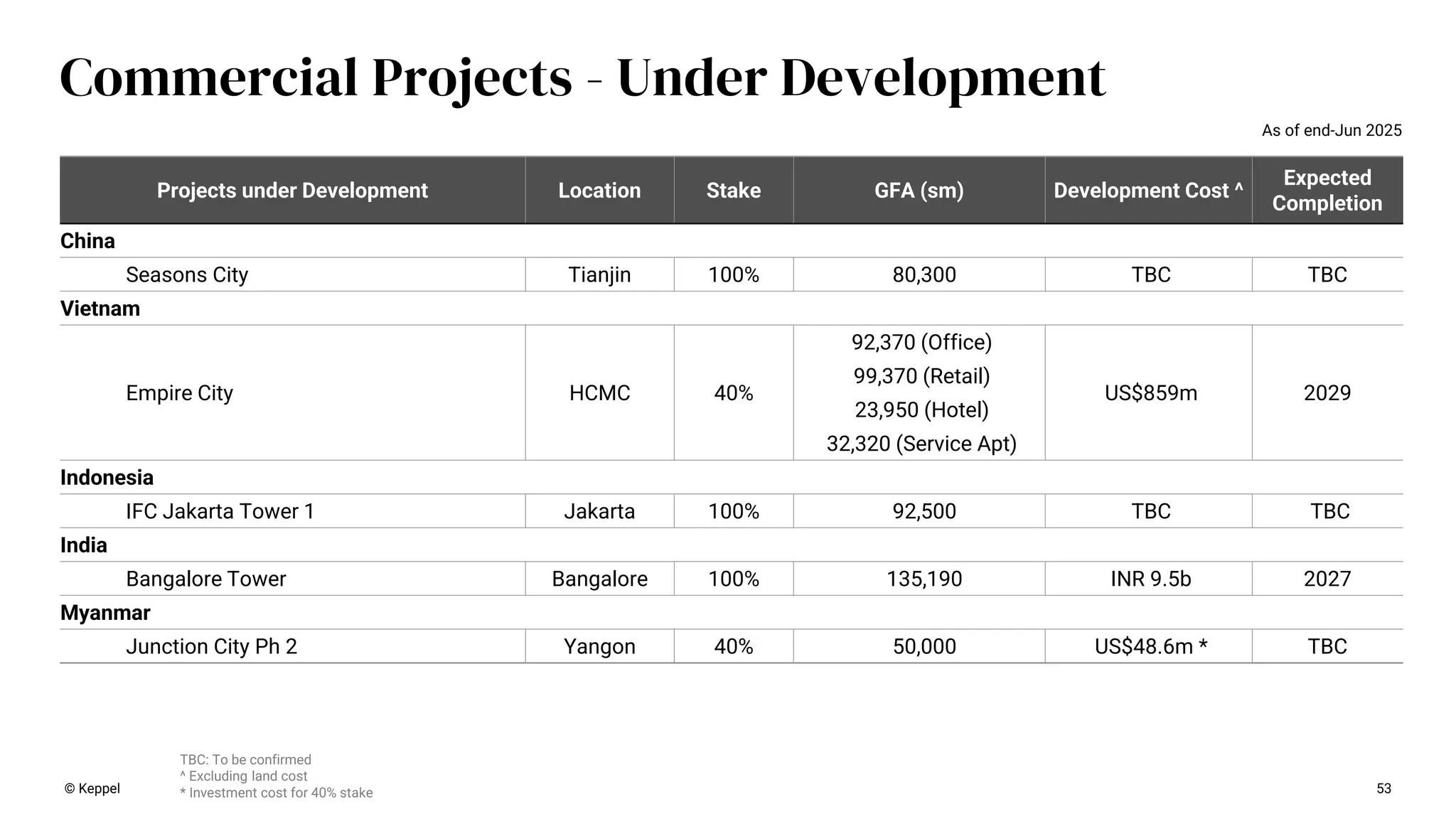

confirmed ^ Excluding land cost * Investment cost for 40% stake Commercial Projects - Under Development Projects under Development Location Stake GFA (sm) Development Cost ^ Expected Completion China Seasons City Tianjin 100% 80,300 TBC TBC Vietnam Empire City HCMC 40% 92,370 (Office) US$859m 2029 99,370 (Retail) 23,950 (Hotel) 32,320 (Service Apt) Indonesia IFC Jakarta Tower 1 Jakarta 100% 92,500 TBC TBC India Bangalore Tower Bangalore 100% 135,190 INR 9.5b 2027 Myanmar Junction City Ph 2 Yangon 40% 50,000 US$48.6m * TBC 53 © Keppel As of end-Jun 2025

54.

* AEI completed

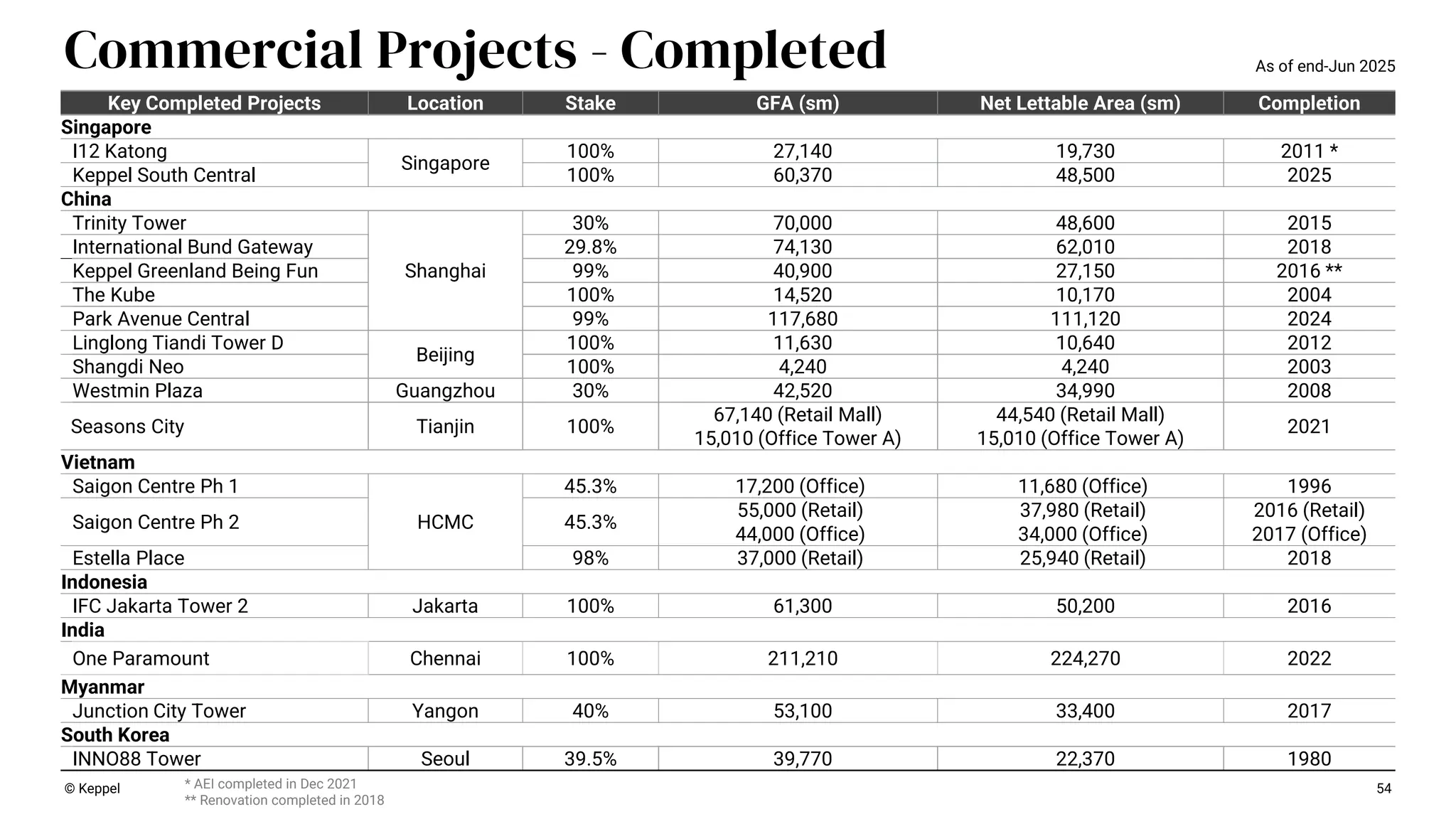

in Dec 2021 ** Renovation completed in 2018 54 Commercial Projects - Completed Key Completed Projects Location Stake GFA (sm) Net Lettable Area (sm) Completion Singapore I12 Katong Singapore 100% 27,140 19,730 2011 * Keppel South Central 100% 60,370 48,500 2025 China Trinity Tower Shanghai 30% 70,000 48,600 2015 International Bund Gateway 29.8% 74,130 62,010 2018 Keppel Greenland Being Fun 99% 40,900 27,150 2016 ** The Kube 100% 14,520 10,170 2004 Park Avenue Central 99% 117,680 111,120 2024 Linglong Tiandi Tower D Beijing 100% 11,630 10,640 2012 Shangdi Neo 100% 4,240 4,240 2003 Westmin Plaza Guangzhou 30% 42,520 34,990 2008 Seasons City Tianjin 100% 67,140 (Retail Mall) 15,010 (Office Tower A) 44,540 (Retail Mall) 15,010 (Office Tower A) 2021 Vietnam Saigon Centre Ph 1 HCMC 45.3% 17,200 (Office) 11,680 (Office) 1996 Saigon Centre Ph 2 45.3% 55,000 (Retail) 37,980 (Retail) 2016 (Retail) 44,000 (Office) 34,000 (Office) 2017 (Office) Estella Place 98% 37,000 (Retail) 25,940 (Retail) 2018 Indonesia IFC Jakarta Tower 2 Jakarta 100% 61,300 50,200 2016 India One Paramount Chennai 100% 211,210 224,270 2022 Myanmar Junction City Tower Yangon 40% 53,100 33,400 2017 South Korea INNO88 Tower Seoul 39.5% 39,770 22,370 1980 © Keppel As of end-Jun 2025

55.

Plot Date Sales Value (RMB’m) Land

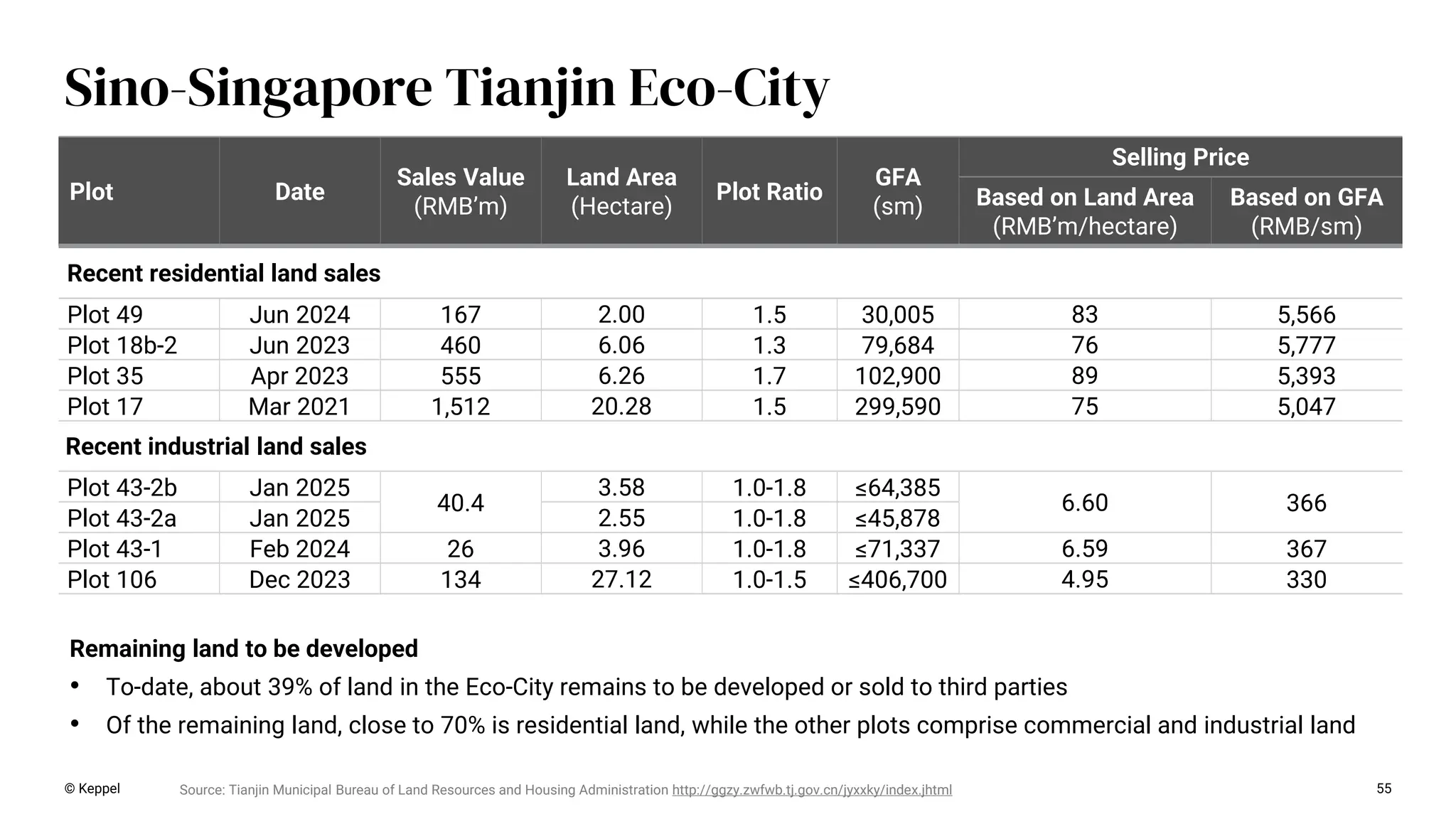

Area (Hectare) Plot Ratio GFA (sm) Selling Price Based on Land Area (RMB’m/hectare) Based on GFA (RMB/sm) Recent residential land sales Plot 49 Jun 2024 167 2.00 1.5 30,005 83 5,566 Plot 18b-2 Jun 2023 460 6.06 1.3 79,684 76 5,777 Plot 35 Apr 2023 555 6.26 1.7 102,900 89 5,393 Plot 17 Mar 2021 1,512 20.28 1.5 299,590 75 5,047 Recent industrial land sales Plot 43-2b Jan 2025 40.4 3.58 1.0-1.8 ≤64,385 6.60 366 Plot 43-2a Jan 2025 2.55 1.0-1.8 ≤45,878 Plot 43-1 Feb 2024 26 3.96 1.0-1.8 ≤71,337 6.59 367 Plot 106 Dec 2023 134 27.12 1.0-1.5 ≤406,700 4.95 330 Source: Tianjin Municipal Bureau of Land Resources and Housing Administration http://ggzy.zwfwb.tj.gov.cn/jyxxky/index.jhtml Remaining land to be developed • To-date, about 39% of land in the Eco-City remains to be developed or sold to third parties • Of the remaining land, close to 70% is residential land, while the other plots comprise commercial and industrial land © Keppel 55 Sino-Singapore Tianjin Eco-City

56.

© Keppel 56 Disclaimer NOT

FOR RELEASE, PUBLICATION OR DISTRIBUTION, IN WHOLE OR IN PART, IN, INTO OR FROM ANY JURISDICTION WHERE TO DO SO WOULD CONSTITUTE A VIOLATION OF THE RELEVANT LAWS OF THAT JURISDICTION. THIS PRESENTATION SHALL NOT CONSTITUTE AN OFFER TO SELL OR A SOLICITATION OF AN OFFER TO SELL, SUBSCRIBE FOR OR BUY SECURITIES IN ANY JURISDICTION, INCLUDING IN THE UNITED STATES. This presentation is for information purposes only and does not have regard to your specific investment objectives, financial situation or your particular needs. Any information in this presentation is not to be construed as investment or financial advice and does not constitute an invitation, offer or solicitation of any offer to acquire, purchase or subscribe for securities or other financial instruments in Keppel Ltd. (“Keppel”). The past performance of Keppel is not indicative of the future performance of Keppel. You should exercise judgment in your own financial decisions. If in doubt, please consult with your professional advisers. Unless explicitly indicated otherwise, all monetary values denoted as ‘$’ within this presentation are to be interpreted as referring to Singapore dollars.

Download

![© Keppel 19

1H 2025 net profit (horizontal reporting)

i Includes asset management, transaction and advisory fees on sponsor stakes and co-investments.

ii Includes returns (net of financing costs attributable to such stakes) from equity accounted stakes in listed and private funds – Infrastructure [$6m from listed funds]; Real Estate [$15m from listed

funds], and Connectivity [$16m from listed funds].

iii Includes overheads and financing costs which have not been attributed to segments.

iv Non-Core Portfolio for Divestment comprises mainly legacy offshore & marine assets, residential landbank, selected property developments and investment properties, hospitality and logistics

assets, associated cash and receivables, and other non-core investments that are not aligned with Keppel’s strategic focus as an asset-light global asset manager and operator.

($’m) Asset

Managementi Operatingii Valuation

Capital

recycling Net profit

Infrastructure 16 333 (3) – 346 80%

Real Estate 41 - 27 30 98 23%

Connectivity 14 40 1 2 57 13%

Corporate activitiesiii (70) (16%)

New Keppel 71 373 25 32 431 100%

Non-Core Portfolio for

Divestmentiv (53)

Net profit 71 373 25 32 378](https://image.slidesharecdn.com/keppelltd-250731003357-cabdb749/75/Keppel-Ltd-1H-2025-Results-Presentation-Slides-19-2048.jpg)

![© Keppel 43

1H 2024 net profit (horizontal reporting)

i Includes asset management, transaction and advisory fees on sponsor stakes and co-investments.

ii Includes returns (net of financing costs attributable to such stakes) from equity accounted stakes in listed and private funds – Infrastructure [$8m from listed funds and -$4m from private funds];

Real Estate [$4m from listed funds and -$3m from private funds], and Connectivity [$11m from listed funds and -$3m from private funds].

iii Includes overheads and financing costs which have not been attributed to segments.

iv Non-Core Portfolio for Divestment comprises mainly legacy offshore & marine assets, residential landbank, selected property developments and investment properties, hospitality and logistics

assets, associated cash and receivables, and other non-core investments that are not aligned with Keppel’s strategic focus as an asset-light global asset manager and operator.

($’m) Asset

Managementi Operatingii Valuation

Capital

recycling Net profit

Infrastructure 44 308 12 1 365 106%

Real Estate 19 (10) (29) – (20) (6%)

Connectivity 12 41 12 5 70 20%

Corporate activitiesiii (70) (20%)

New Keppel 75 339 (5) 6 345 100%

Non-Core Portfolio for

Divestmentiv (41)

Net profit 75 339 (5) 6 304](https://image.slidesharecdn.com/keppelltd-250731003357-cabdb749/75/Keppel-Ltd-1H-2025-Results-Presentation-Slides-43-2048.jpg)

![Where to Buy LinkedIn Accounts_ [12 Best Sites] (3).pdf](https://cdn.slidesharecdn.com/ss_thumbnails/wheretobuylinkedinaccounts12bestsites3-251124162550-95b6ddfa-thumbnail.jpg?width=640&height=640&fit=bounds)

![Where to Buy LinkedIn Accounts_ [12 Best Sites] (2).pdf](https://cdn.slidesharecdn.com/ss_thumbnails/wheretobuylinkedinaccounts12bestsites2-251124191348-c246988b-thumbnail.jpg?width=640&height=640&fit=bounds)