Dynamic Analysis of Changes to the Supplemental Nutrition Assistance Program (SNAP) in H.R. 1

This slide deck describes the main mechanisms in CBO's dynamic analysis of H.R. 1, explains the changes to SNAP, and explains the macroeconomic effects and budgetary feedback of those changes.

Dynamic Analysis of Changes to the Supplemental Nutrition Assistance Program (SNAP) in H.R. 1

1.

Dynamic Analysis ofChanges to the

Supplemental Nutrition Assistance

Program (SNAP) in H.R. 1

June 2025

Information in this slide deck is based on a presentation given at CBO’s June 2025 meeting of its Panel of Economic Advisers.

2.

1

Notes about thisslide deck: Unless otherwise indicated, all years referred to in describing budget projections are federal fiscal years, which run from October 1 to September 30 and

are designated by the calendar year in which they end. Numbers in the text, tables, and figures may not add up to totals because of rounding.

CBO’s Budget Analysis Division (BAD) estimates that Subtitle A of Title I in H.R. 1 would reduce federal

spending by $287 billion over the 2025–2034 period. (That total excludes the Medicaid budgetary effects of

Section 10009 that are included in the published total.)

The budgetary feedback arising from macroeconomic effects would reduce the federal deficit by an

additional $22 billion over the 2025–2034 period, primarily because lower federal deficits would “crowd in”

private investment and lower interest rates. (This estimate includes only the changes to net interest costs

stemming from changes to interest rates on the baseline projection of federal debt. By long-standing

convention, estimates under House Rule XIII(8) do not include any increases or decreases in interest payments

on the federal debt that would arise from an estimated change in borrowing needs. Consistent with that

approach, the estimate of the budgetary feedback does not include the decreases in interest payments that

would arise from net decreases in borrowing needs that would result from enacting SNAP-related provisions.)

Including budgetary feedback from macroeconomic effects, SNAP-related policies in the bill would reduce the

federal deficit by $309 billion over the 2025–2034 period.

When the budgetary feedback from macroeconomic effects and the decreases in interest payments on lower

federal debt that would arise from the estimated decline in borrowing needs are accounted for, SNAP-related

policies in the bill would reduce the federal deficit by $353 billion over the 2025–2034 period.

Summary

3.

2

This slide deckhas three sections.

▪ The first section describes the main mechanisms in CBO’s dynamic analysis

(see Slides 3 to 9);

▪ The second section explains the changes to SNAP in H.R. 1

(see Slides 10 to 25); and

▪ The third section explains the macroeconomic effects and budgetary feedback

of changes to SNAP in H.R. 1 (see Slides 26 to 32).

Organization of This Slide Deck

4

Conventional estimates ofproposed legislation prepared by CBO and the staff of the

Joint Committee on Taxation (JCT) do account for potential behavioral responses by

households, businesses, and nonfederal governments.

Those conventional estimates do not reflect any changes in the overall size of the

U.S. economy relative to CBO’s baseline macroeconomic projections.

When analyzing proposed major legislation, House Rule XIII(8) requires CBO and JCT to

include the budgetary effects resulting from changes in output, employment, the capital

stock, and other macroeconomic variables, in addition to the behavioral responses in a

conventional estimate.

An analysis of proposed legislation that incorporates such macroeconomic effects is

commonly known as a dynamic analysis.

Conventional Estimates and Dynamic Analysis

6.

5

For more informationabout the framework CBO uses for evaluating the impact of federal policies on output, see Congressional Budget Office, How CBO Analyzes the Effects of

Changes in Federal Fiscal Policies on the Economy (November 2014), www.cbo.gov/publication/49494.

CBO estimates the macroeconomic effects of changes in federal policies in both the

short term and the longer term:

▪ In the short term, policy changes primarily affect the economy by influencing the

demand for goods and services, which leads to changes in output relative to its potential

(maximum sustainable) level.

– CBO uses its multiplier model to estimate how changes in aggregate demand affect

output. Those demand-side effects are combined with estimates of the policies’

effects on the supply of capital and labor.

▪ In the longer term, changes in policies affect the economy primarily by altering public

saving, federal investment, people’s incentives to work and save, and businesses’

incentive to invest, which leads to changes in potential output.

– CBO uses its Solow-type model in which output is determined by the number of

labor hours that workers supply, the size and composition of the capital stock, and

total factor productivity (TFP).

CBO’s Framework for Estimating Macroeconomic Effects

7.

6

CBO’s multiplier modelapplies an output multiplier to each policy (or provision), which is

the product of a policy’s direct and indirect effects on aggregate demand. Output

multipliers vary across policies because the direct effects differ.

▪ Direct effects. A policy’s direct effects on aggregate demand result from changes in

purchases by federal agencies and by the people and organizations that receive federal

payments or pay federal taxes. The direct effect on demand is also referred to as the

marginal propensity to consume (MPC).

▪ Indirect effects. Changes in policy affect output indirectly through demand multipliers,

which depend on the response of monetary policy. When output is projected to remain

above its potential and inflation is projected to remain above, or near, the Federal

Reserve’s long-run goal of 2 percent, CBO uses demand multipliers that have a

cumulative effect on output that range from:

– 0.4 to 1.9 over four quarters (central estimate of 1.2), and

– 0.2 to 0.8 over eight quarters (central estimate of 0.5).

CBO’s Multiplier Model and Short-Term Effects on Output

8.

7

For additional detailsabout CBO’s Solow-type model, see Congressional Budget Office, CBO's Policy Growth Model (April 2021), www.cbo.gov/publication/57017.

The nation’s potential to produce goods and services is the key determinant of output over

the long term, so the longer-term effects of changes in policies rely on CBO’s models of

potential output.

CBO’s Solow-type model, or policy growth model, is calibrated to reproduce the agency’s

baseline projection of potential output using an economywide Cobb-Douglas production

function, which depends on the following:

▪ Labor supply defined in terms of economywide potential hours,

▪ Capital services from nonfarm business capital and owner-occupied residential

housing, and

▪ Economywide potential TFP (the average real output per unit of combined labor and

capital services).

CBO’s Solow-Type Model and Longer-Term Effects on Output

9.

8

Crowding out: Deficits“crowd out” private investment in the longer term, and less

investment leads to a smaller stock of productive capital and lower potential output.

The conventional estimates’ effects across the income distribution and the estimated

effects on spending for each income group are combined to determine the degree of

crowding out.

Labor supply effects: Policies affect potential output by altering incentives to work,

reflected in earnings-weighted hours.

Private investment effects: In addition to the crowding-out channel, private investment is

also affected by changes in the user cost of capital.

Productivity effects: Other factors that affect output but are not attributable to labor or

private capital, such as public investment in infrastructure or research and development,

raise TFP because those investments enhance private activity.

Factors Affecting Potential Output in CBO’s Solow-Type Model

10.

9

Distributional tables: Conventionalestimates prepared by BAD and JCT are transformed by CBO’s

Tax Analysis Division (TAD) and Labor, Income Security, and Long-Term Analysis Division (LISL) into

distributional tables showing the net effect on households’ income after taxes and transfers, sorted by cash

income deciles (or tenths).

Income-based MPCs: MPCs are higher for lower-income households than they are for higher-income

households. In addition, one-time or temporary changes in households’ income after taxes and transfers

generally boost spending less than a persistent change does.

Labor supply effects: Policies affect labor supply by altering incentives to work, reflected in earnings-weighted

hours. In the short term, the effect depends on the state of the labor market; effects are larger when there is

less labor market slack. Labor supply effects are prepared by LISL and TAD and, for health-related policies,

CBO’s Health Analysis Division (HAD).

Investment and productivity effects: Increases in investment boost aggregate demand in the short term and

potential output in the longer term. Investment effects arising from changes in the user cost of capital are

prepared by TAD. Other investment and productivity effects, such as those arising from regulatory changes,

public investment, or federal leases, are prepared by CBO’s Financial Analysis Division (FAD) and

Microeconomic Studies Division (MSD).

Key Inputs for Estimating the Macroeconomic Effects

11

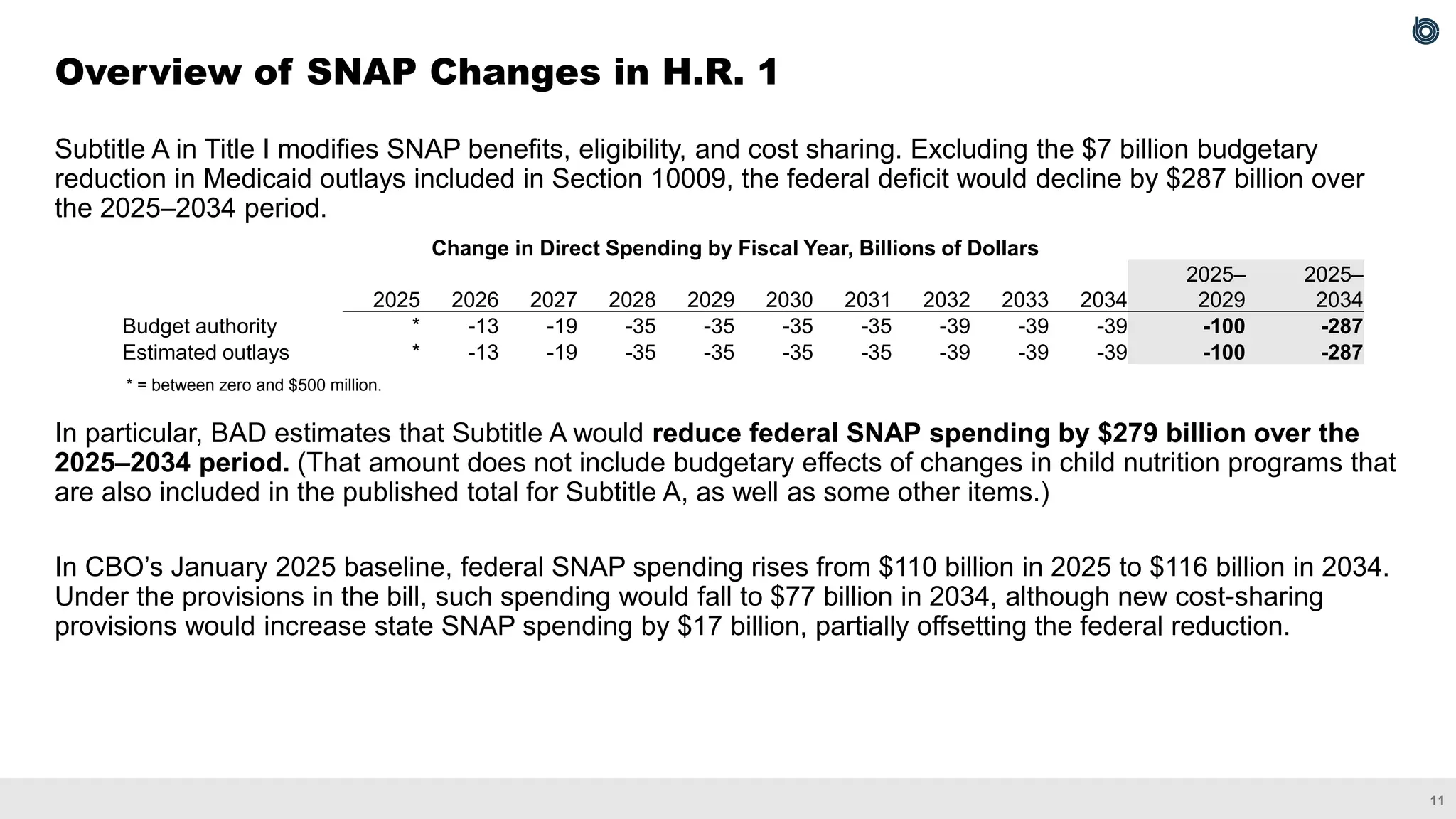

Subtitle A inTitle I modifies SNAP benefits, eligibility, and cost sharing. Excluding the $7 billion budgetary

reduction in Medicaid outlays included in Section 10009, the federal deficit would decline by $287 billion over

the 2025–2034 period.

In particular, BAD estimates that Subtitle A would reduce federal SNAP spending by $279 billion over the

2025–2034 period. (That amount does not include budgetary effects of changes in child nutrition programs that

are also included in the published total for Subtitle A, as well as some other items.)

In CBO’s January 2025 baseline, federal SNAP spending rises from $110 billion in 2025 to $116 billion in 2034.

Under the provisions in the bill, such spending would fall to $77 billion in 2034, although new cost-sharing

provisions would increase state SNAP spending by $17 billion, partially offsetting the federal reduction.

Overview of SNAP Changes in H.R. 1

Change in Direct Spending by Fiscal Year, Billions of Dollars

2025 2026 2027 2028 2029 2030 2031 2032 2033 2034

2025–

2029

2025–

2034

Budget authority * -13 -19 -35 -35 -35 -35 -39 -39 -39 -100 -287

Estimated outlays * -13 -19 -35 -35 -35 -35 -39 -39 -39 -100 -287

* = between zero and $500 million.

13.

12

For additional detailsabout each of those provisions, see Congressional Budget Office, letter to the Honorable Amy Klobuchar and the Honorable Angie Craig about the potential

effects on the Supplemental Nutrition Assistance Program of reconciliation recommendations pursuant to H. Con Res. 14 (May 22, 2025), www.cbo.gov/publication/61426.

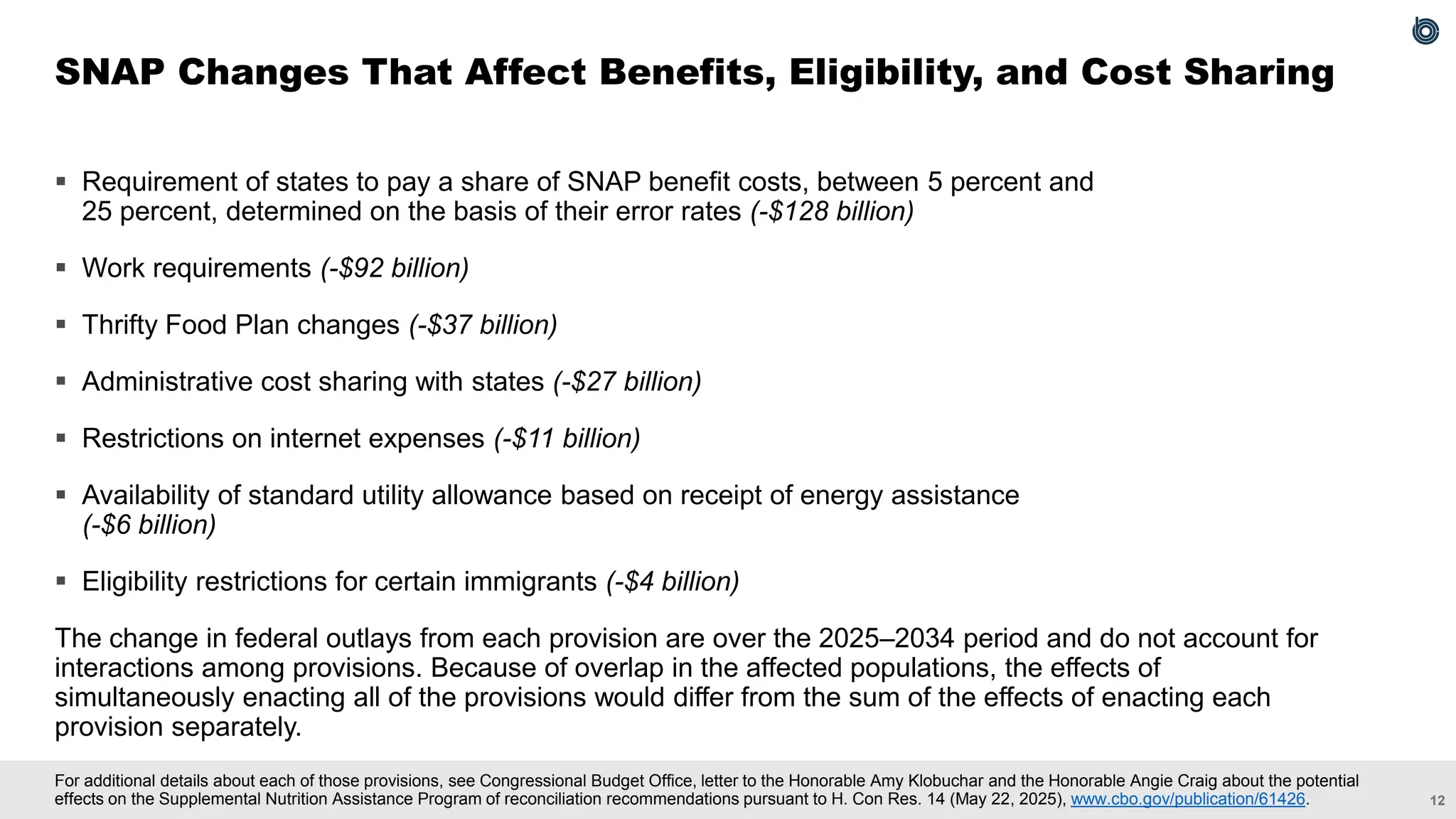

▪ Requirement of states to pay a share of SNAP benefit costs, between 5 percent and

25 percent, determined on the basis of their error rates (-$128 billion)

▪ Work requirements (-$92 billion)

▪ Thrifty Food Plan changes (-$37 billion)

▪ Administrative cost sharing with states (-$27 billion)

▪ Restrictions on internet expenses (-$11 billion)

▪ Availability of standard utility allowance based on receipt of energy assistance

(-$6 billion)

▪ Eligibility restrictions for certain immigrants (-$4 billion)

The change in federal outlays from each provision are over the 2025–2034 period and do not account for

interactions among provisions. Because of overlap in the affected populations, the effects of

simultaneously enacting all of the provisions would differ from the sum of the effects of enacting each

provision separately.

SNAP Changes That Affect Benefits, Eligibility, and Cost Sharing

14.

13

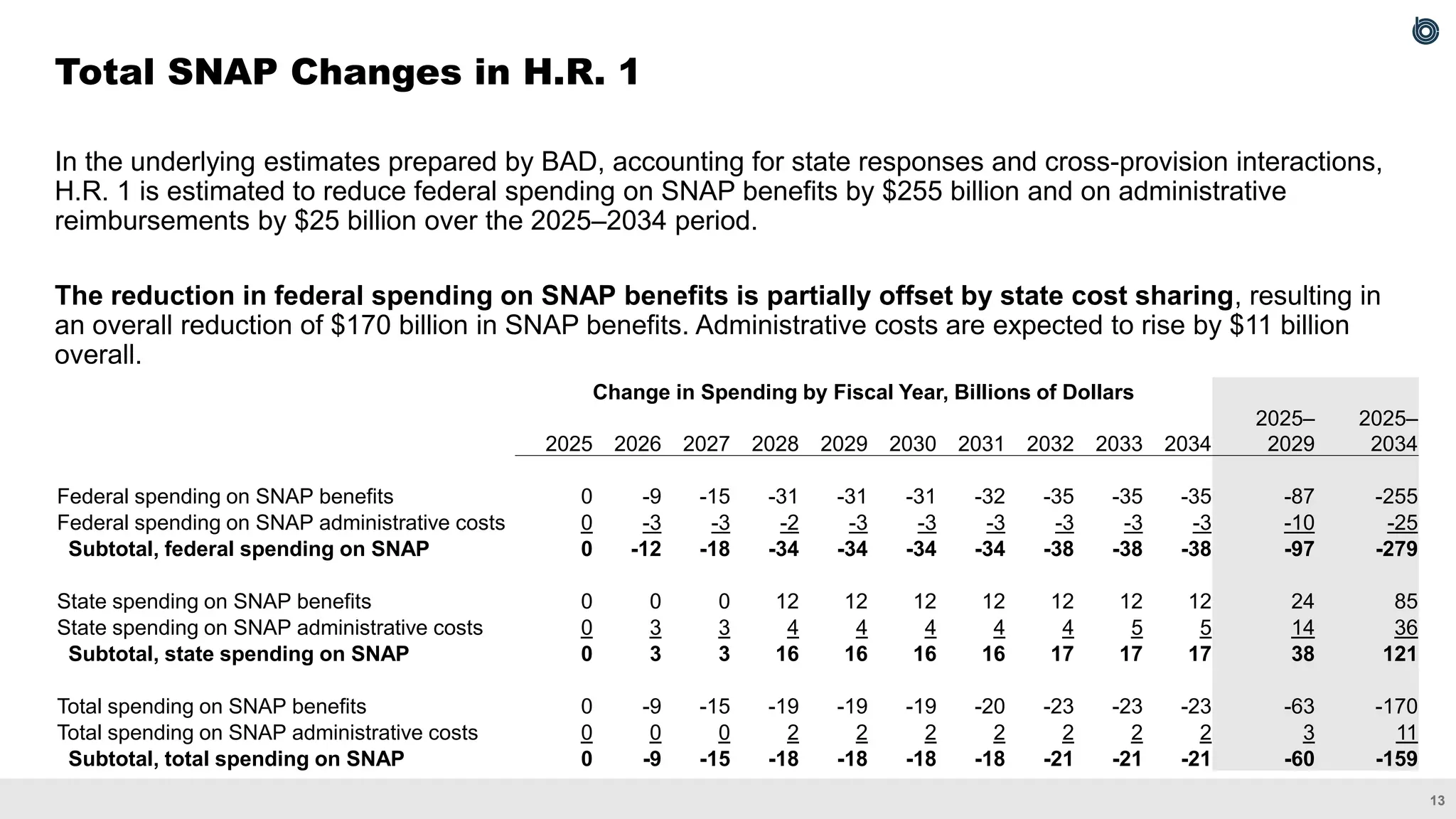

In the underlyingestimates prepared by BAD, accounting for state responses and cross-provision interactions,

H.R. 1 is estimated to reduce federal spending on SNAP benefits by $255 billion and on administrative

reimbursements by $25 billion over the 2025–2034 period.

The reduction in federal spending on SNAP benefits is partially offset by state cost sharing, resulting in

an overall reduction of $170 billion in SNAP benefits. Administrative costs are expected to rise by $11 billion

overall.

Total SNAP Changes in H.R. 1

Change in Spending by Fiscal Year, Billions of Dollars

2025 2026 2027 2028 2029 2030 2031 2032 2033 2034

2025–

2029

2025–

2034

Federal spending on SNAP benefits 0 -9 -15 -31 -31 -31 -32 -35 -35 -35 -87 -255

Federal spending on SNAP administrative costs 0 -3 -3 -2 -3 -3 -3 -3 -3 -3 -10 -25

Subtotal, federal spending on SNAP 0 -12 -18 -34 -34 -34 -34 -38 -38 -38 -97 -279

State spending on SNAP benefits 0 0 0 12 12 12 12 12 12 12 24 85

State spending on SNAP administrative costs 0 3 3 4 4 4 4 4 5 5 14 36

Subtotal, state spending on SNAP 0 3 3 16 16 16 16 17 17 17 38 121

Total spending on SNAP benefits 0 -9 -15 -19 -19 -19 -20 -23 -23 -23 -63 -170

Total spending on SNAP administrative costs 0 0 0 2 2 2 2 2 2 2 3 11

Subtotal, total spending on SNAP 0 -9 -15 -18 -18 -18 -18 -21 -21 -21 -60 -159

15.

14

BAD’s conventional estimatesalready reflect state responses within programs, but the net

change in states’ fiscal positions, beyond the directly affected programs, is generally not

accounted for.

For example, CBO expects that some states would maintain current SNAP benefits and eligibility

and that others would modify benefits or eligibility or possibly leave the program altogether. The

agency estimated state responses in the aggregate using a probabilistic approach to account for

a range of possible outcomes.

If a change in federal policy resulted in a change to a state’s fiscal position relative to what would

occur under current law, how states reacted to that change would depend on whether the federal

policy generated a surplus or a deficit. It could also depend on the time horizon, with states

shifting from an initial short-term response (such as relying on rainy day funds until they can fully

adjust) to a longer-term source of financing.

States would certainly vary how they respond to a change in their fiscal position. CBO typically

estimates state responses in the aggregate, accounting for a range of possible outcomes.

How State Responses Were Prepared

16.

15

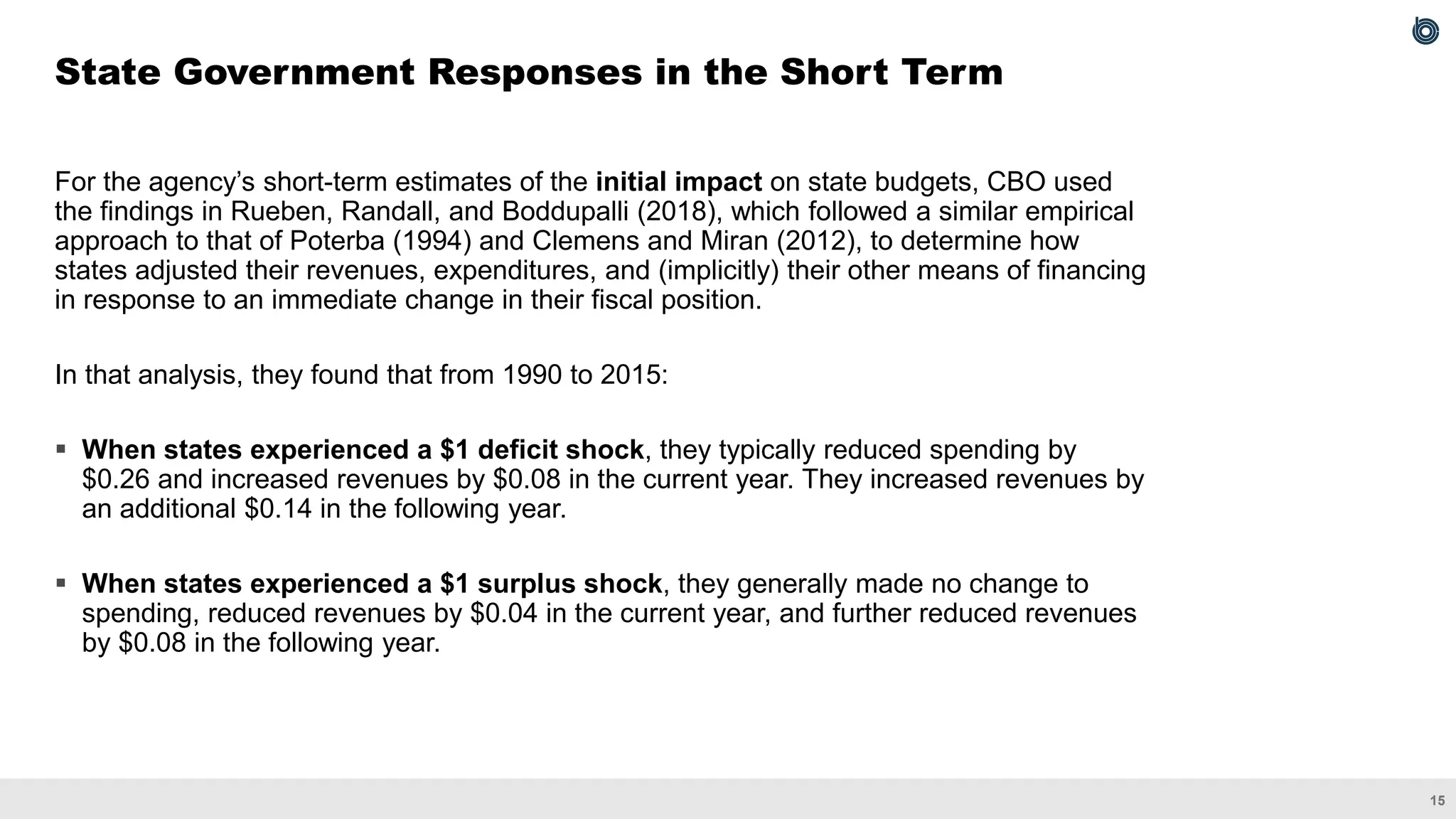

For the agency’sshort-term estimates of the initial impact on state budgets, CBO used

the findings in Rueben, Randall, and Boddupalli (2018), which followed a similar empirical

approach to that of Poterba (1994) and Clemens and Miran (2012), to determine how

states adjusted their revenues, expenditures, and (implicitly) their other means of financing

in response to an immediate change in their fiscal position.

In that analysis, they found that from 1990 to 2015:

▪ When states experienced a $1 deficit shock, they typically reduced spending by

$0.26 and increased revenues by $0.08 in the current year. They increased revenues by

an additional $0.14 in the following year.

▪ When states experienced a $1 surplus shock, they generally made no change to

spending, reduced revenues by $0.04 in the current year, and further reduced revenues

by $0.08 in the following year.

State Government Responses in the Short Term

17.

16

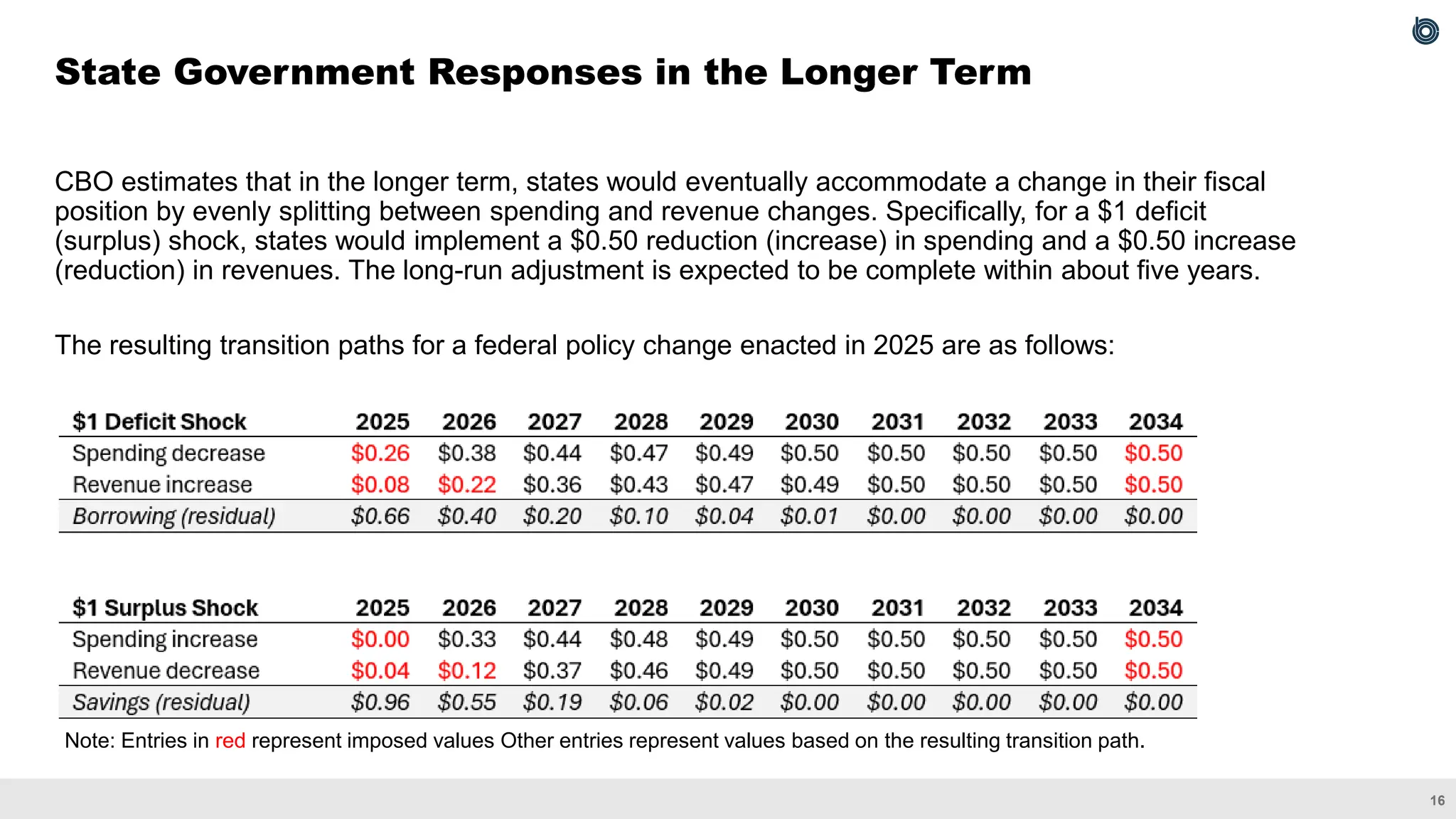

CBO estimates thatin the longer term, states would eventually accommodate a change in their fiscal

position by evenly splitting between spending and revenue changes. Specifically, for a $1 deficit

(surplus) shock, states would implement a $0.50 reduction (increase) in spending and a $0.50 increase

(reduction) in revenues. The long-run adjustment is expected to be complete within about five years.

The resulting transition paths for a federal policy change enacted in 2025 are as follows:

State Government Responses in the Longer Term

Note: Entries in red represent imposed values Other entries represent values based on the resulting transition path.

18.

17

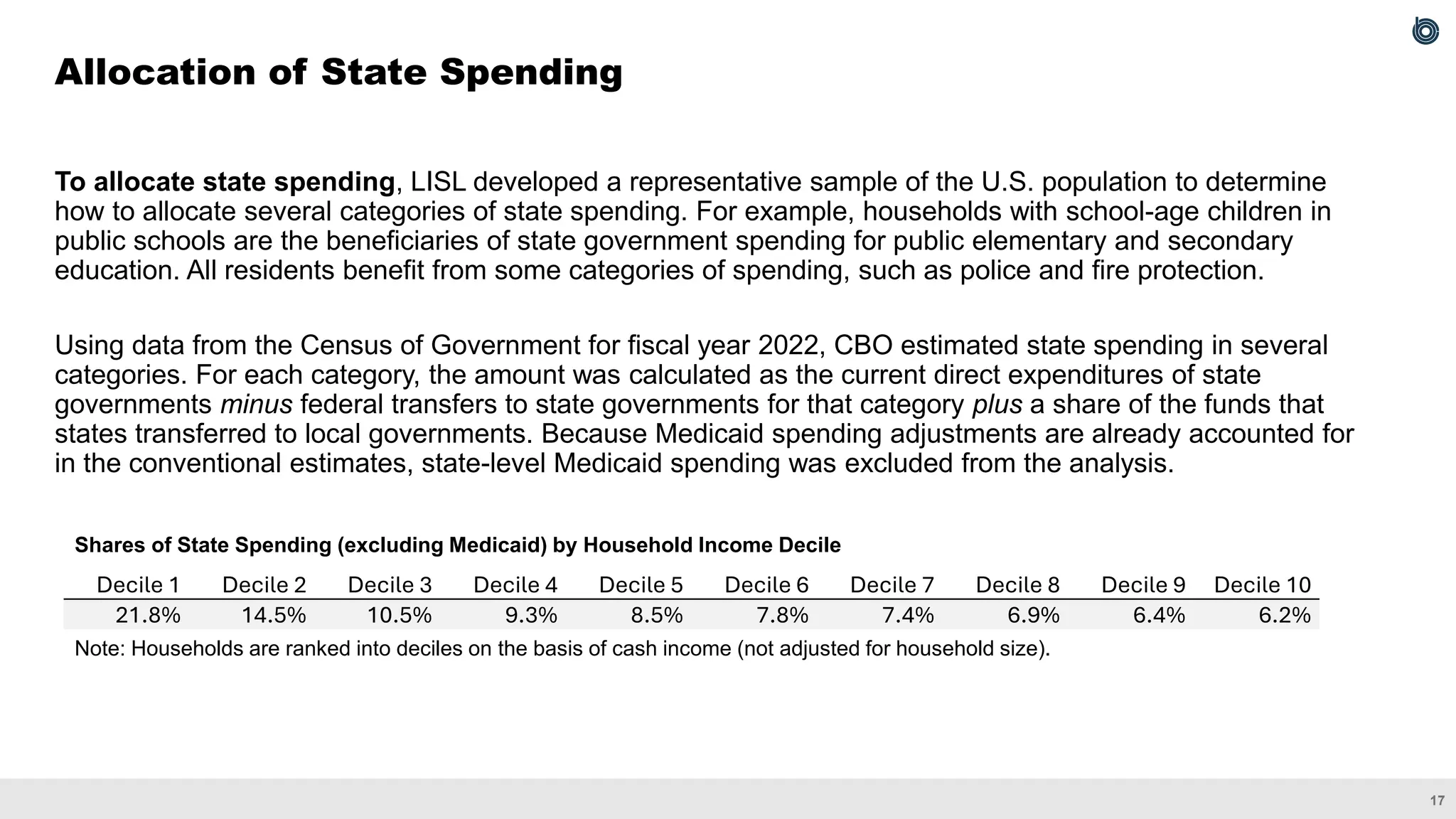

To allocate statespending, LISL developed a representative sample of the U.S. population to determine

how to allocate several categories of state spending. For example, households with school-age children in

public schools are the beneficiaries of state government spending for public elementary and secondary

education. All residents benefit from some categories of spending, such as police and fire protection.

Using data from the Census of Government for fiscal year 2022, CBO estimated state spending in several

categories. For each category, the amount was calculated as the current direct expenditures of state

governments minus federal transfers to state governments for that category plus a share of the funds that

states transferred to local governments. Because Medicaid spending adjustments are already accounted for

in the conventional estimates, state-level Medicaid spending was excluded from the analysis.

Allocation of State Spending

Decile 1 Decile 2 Decile 3 Decile 4 Decile 5 Decile 6 Decile 7 Decile 8 Decile 9 Decile 10

21.8% 14.5% 10.5% 9.3% 8.5% 7.8% 7.4% 6.9% 6.4% 6.2%

Shares of State Spending (excluding Medicaid) by Household Income Decile

Note: Households are ranked into deciles on the basis of cash income (not adjusted for household size).

19.

18

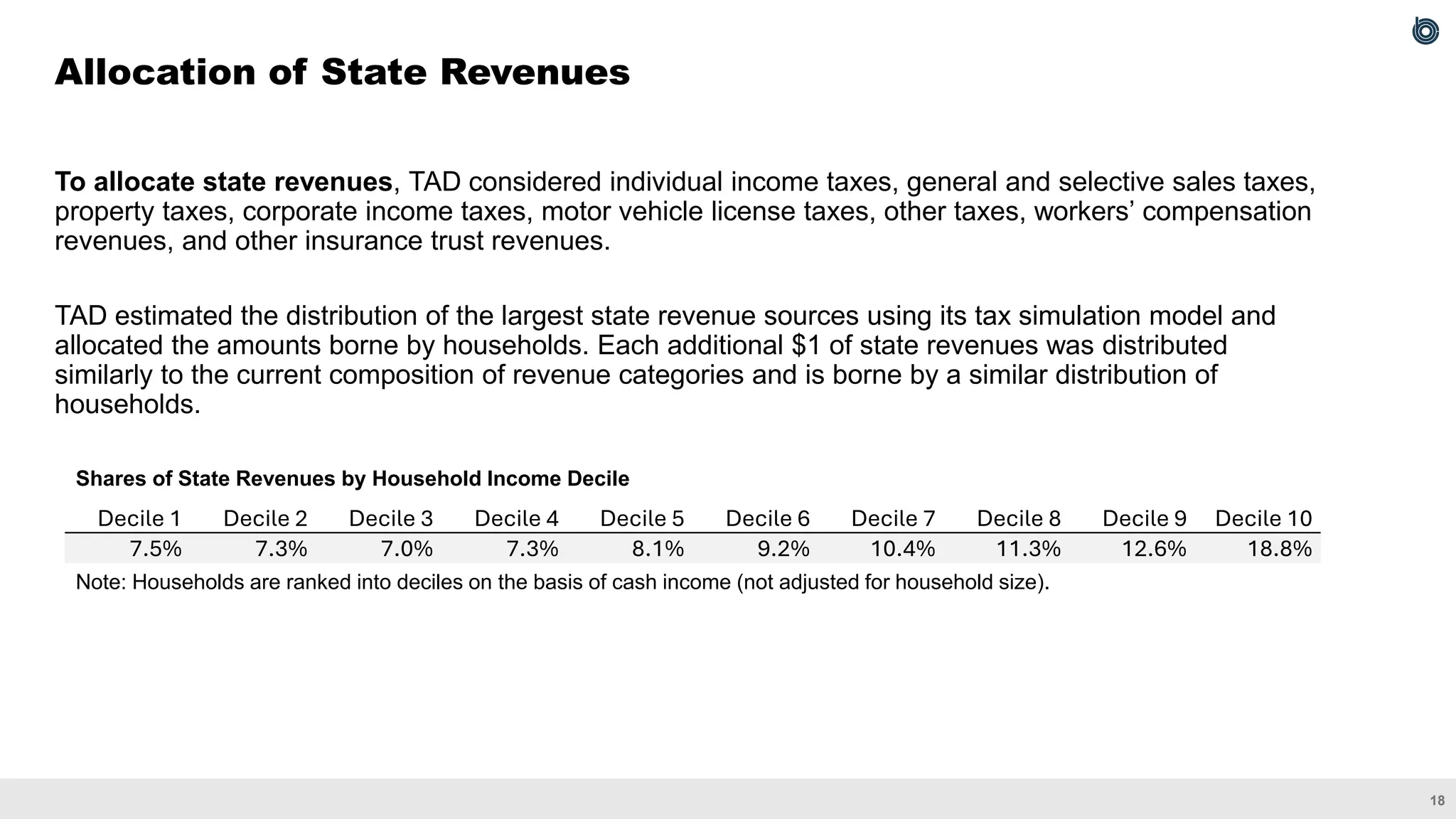

To allocate staterevenues, TAD considered individual income taxes, general and selective sales taxes,

property taxes, corporate income taxes, motor vehicle license taxes, other taxes, workers’ compensation

revenues, and other insurance trust revenues.

TAD estimated the distribution of the largest state revenue sources using its tax simulation model and

allocated the amounts borne by households. Each additional $1 of state revenues was distributed

similarly to the current composition of revenue categories and is borne by a similar distribution of

households.

Allocation of State Revenues

Decile 1 Decile 2 Decile 3 Decile 4 Decile 5 Decile 6 Decile 7 Decile 8 Decile 9 Decile 10

7.5% 7.3% 7.0% 7.3% 8.1% 9.2% 10.4% 11.3% 12.6% 18.8%

Shares of State Revenues by Household Income Decile

Note: Households are ranked into deciles on the basis of cash income (not adjusted for household size).

20.

19

For more detailsabout how the agency projects that states would respond to changes in Medicaid policies, see Congressional Budget Office, letter to the Honorable Ron Wyden and

the Honorable Frank Pallone, Jr. providing estimates for Medicaid policy options and state responses (May 7, 2025), www.cbo.gov/publication/61377.

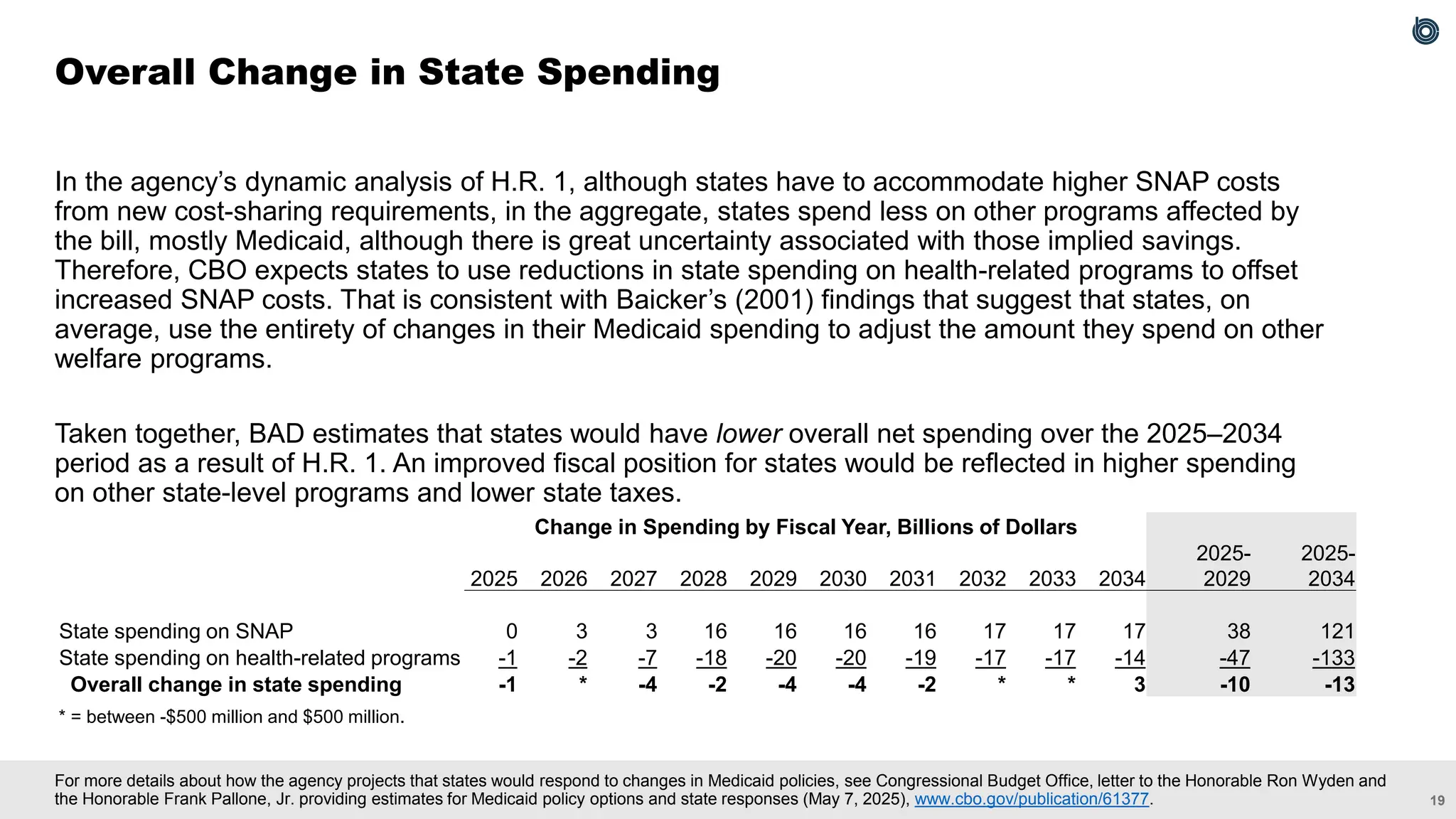

In the agency’s dynamic analysis of H.R. 1, although states have to accommodate higher SNAP costs

from new cost-sharing requirements, in the aggregate, states spend less on other programs affected by

the bill, mostly Medicaid, although there is great uncertainty associated with those implied savings.

Therefore, CBO expects states to use reductions in state spending on health-related programs to offset

increased SNAP costs. That is consistent with Baicker’s (2001) findings that suggest that states, on

average, use the entirety of changes in their Medicaid spending to adjust the amount they spend on other

welfare programs.

Taken together, BAD estimates that states would have lower overall net spending over the 2025–2034

period as a result of H.R. 1. An improved fiscal position for states would be reflected in higher spending

on other state-level programs and lower state taxes.

Overall Change in State Spending

Change in Spending by Fiscal Year, Billions of Dollars

2025 2026 2027 2028 2029 2030 2031 2032 2033 2034

2025-

2029

2025-

2034

State spending on SNAP 0 3 3 16 16 16 16 17 17 17 38 121

State spending on health-related programs -1 -2 -7 -18 -20 -20 -19 -17 -17 -14 -47 -133

Overall change in state spending -1 * -4 -2 -4 -4 -2 * * 3 -10 -13

* = between -$500 million and $500 million.

21.

20

Aggregate demand effects

▪The distributional table includes the total (federal + state) change in SNAP benefits as well states’

fiscal responses. Changes in administrative costs are treated as government consumption.

Labor supply effects

▪ SNAP recipients would adjust their labor supply in response to the change in benefit amounts and

changes in eligibility, such as work requirements.

▪ Workers would adjust their labor supply in response to changes in state labor income taxes.

Although the labor supply effects could have been attributed to the Medicaid provisions in H.R. 1,

they were attributed to the SNAP provisions for illustrative purposes to demonstrate how states’

responses influence labor supply in CBO’s dynamic analysis.

Investment effects

▪ SNAP provisions in H.R. 1 would reduce the federal deficit and would crowd in private investment.

States might also respond by changing capital income taxes, which would impact the user cost of

capital and, in turn, private investment.

Estimating the Macroeconomic Effects of SNAP Changes in H.R. 1

22.

21

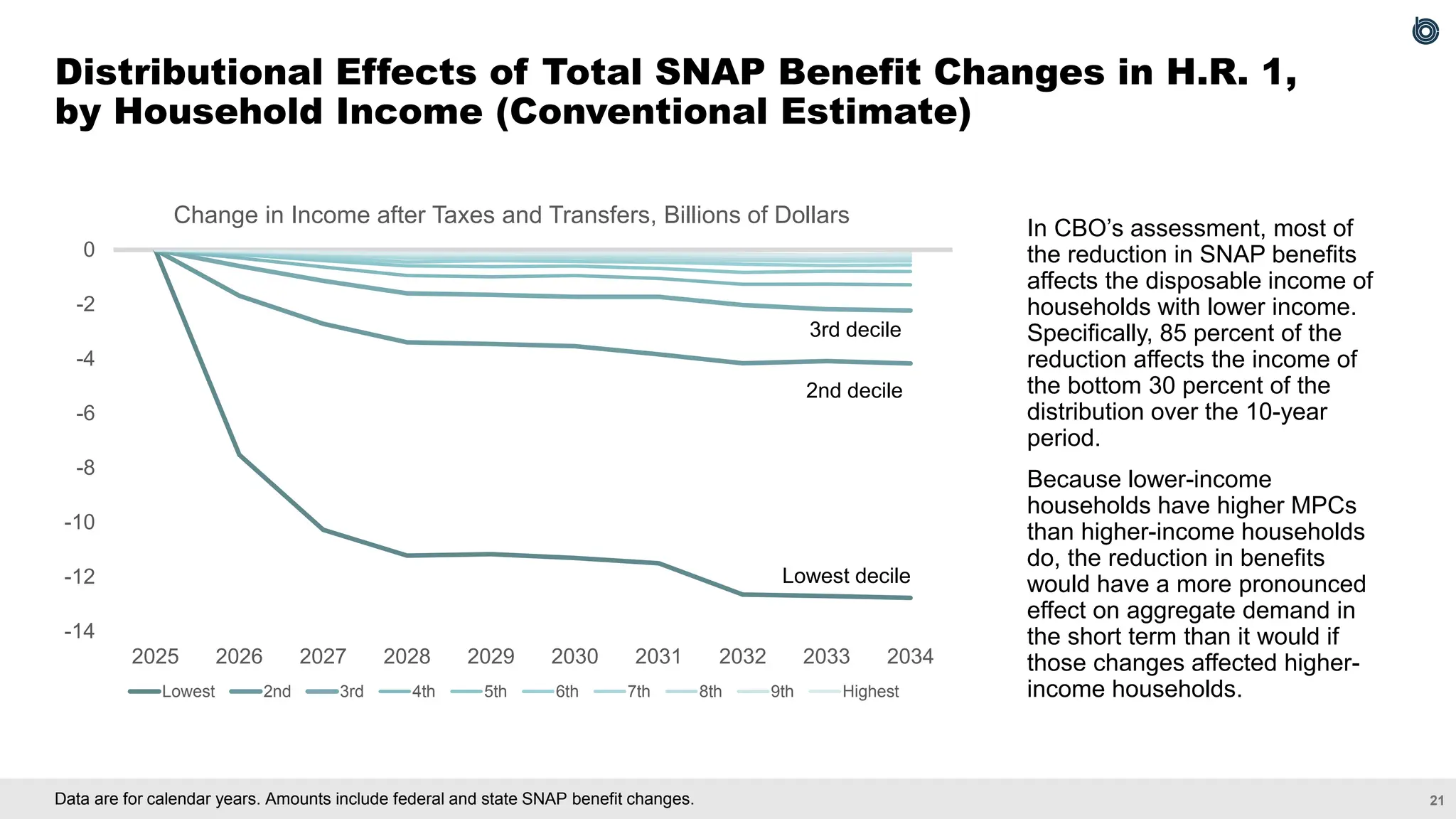

Data are forcalendar years. Amounts include federal and state SNAP benefit changes.

Distributional Effects of Total SNAP Benefit Changes in H.R. 1,

by Household Income (Conventional Estimate)

-14

-12

-10

-8

-6

-4

-2

0

2025 2026 2027 2028 2029 2030 2031 2032 2033 2034

Change in Income after Taxes and Transfers, Billions of Dollars

Lowest 2nd 3rd 4th 5th 6th 7th 8th 9th Highest

Lowest decile

2nd decile

3rd decile

In CBO’s assessment, most of

the reduction in SNAP benefits

affects the disposable income of

households with lower income.

Specifically, 85 percent of the

reduction affects the income of

the bottom 30 percent of the

distribution over the 10-year

period.

Because lower-income

households have higher MPCs

than higher-income households

do, the reduction in benefits

would have a more pronounced

effect on aggregate demand in

the short term than it would if

those changes affected higher-

income households.

23.

22

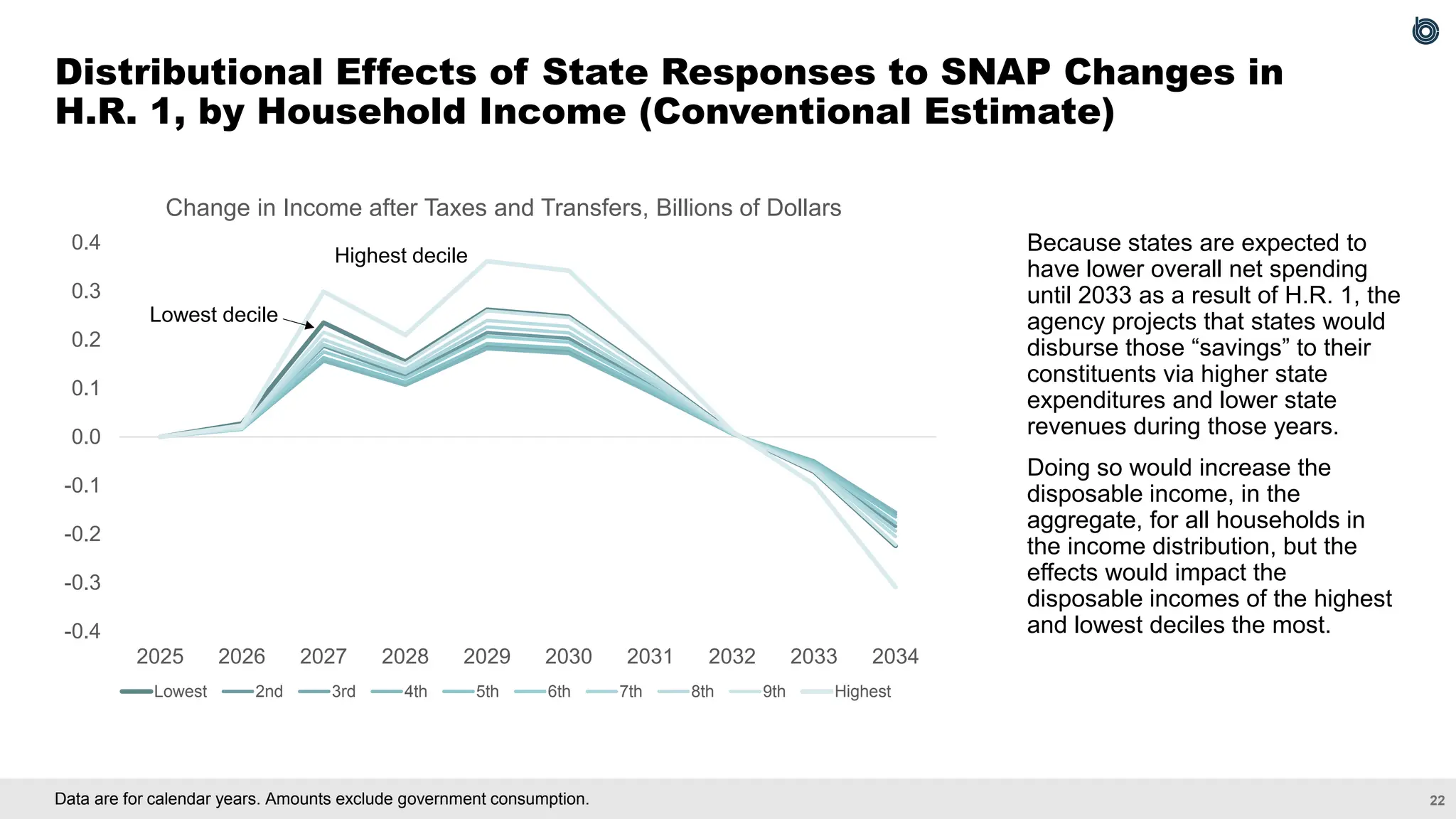

Data are forcalendar years. Amounts exclude government consumption.

Distributional Effects of State Responses to SNAP Changes in

H.R. 1, by Household Income (Conventional Estimate)

Because states are expected to

have lower overall net spending

until 2033 as a result of H.R. 1, the

agency projects that states would

disburse those “savings” to their

constituents via higher state

expenditures and lower state

revenues during those years.

Doing so would increase the

disposable income, in the

aggregate, for all households in

the income distribution, but the

effects would impact the

disposable incomes of the highest

and lowest deciles the most.

-0.4

-0.3

-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

2025 2026 2027 2028 2029 2030 2031 2032 2033 2034

Change in Income after Taxes and Transfers, Billions of Dollars

Lowest 2nd 3rd 4th 5th 6th 7th 8th 9th Highest

Highest decile

Lowest decile

24.

23

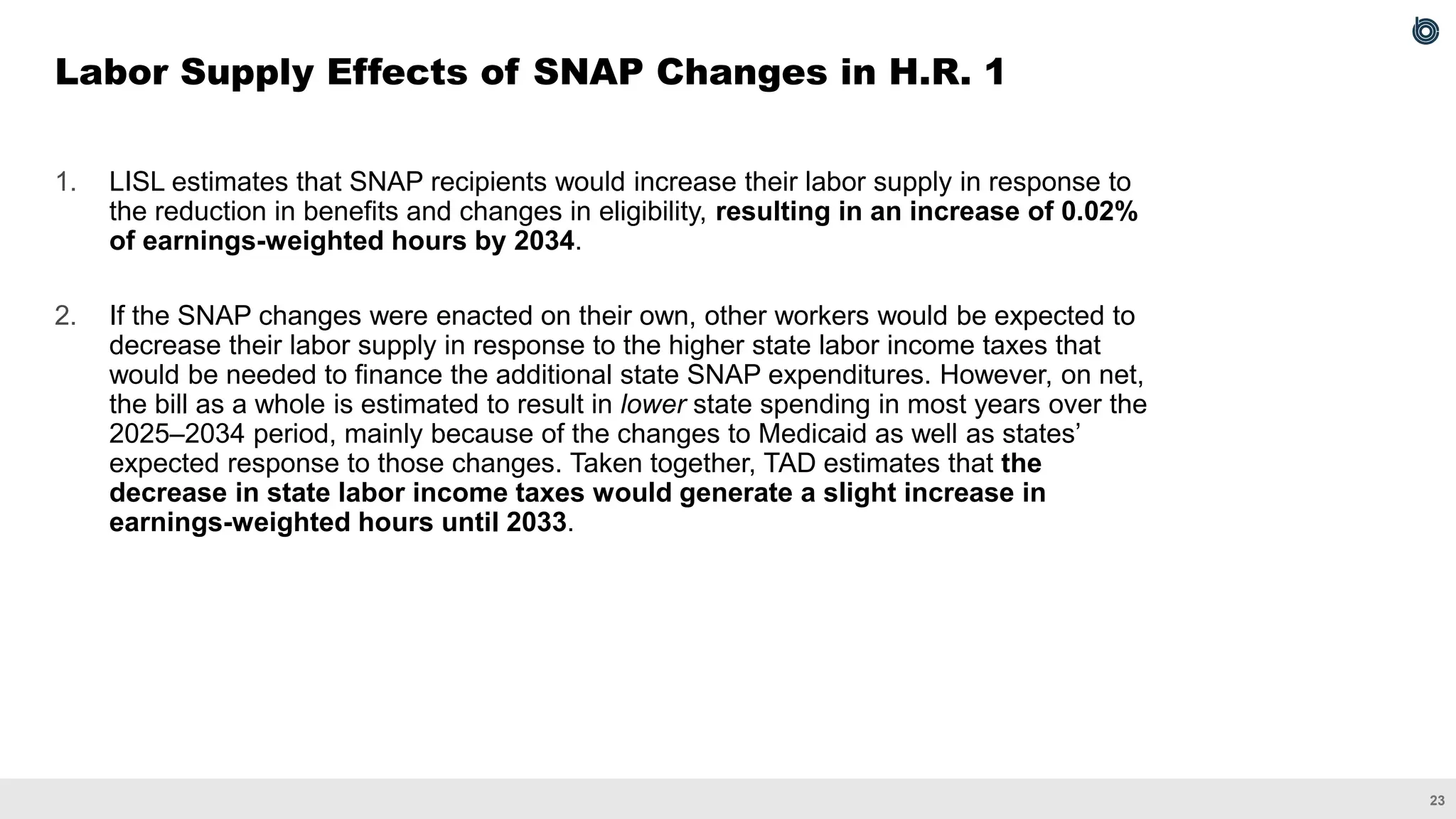

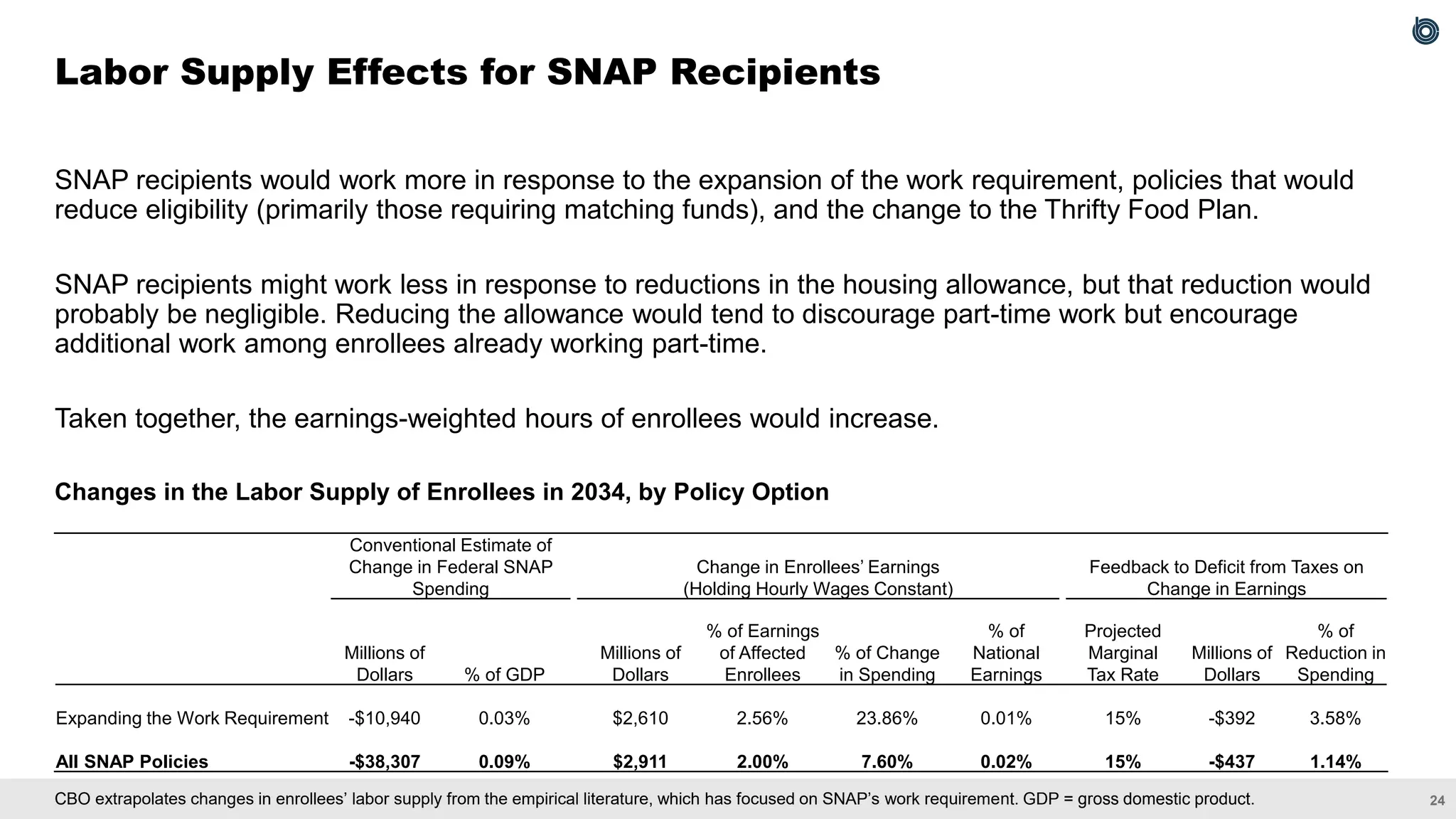

Labor Supply Effectsof SNAP Changes in H.R. 1

1. LISL estimates that SNAP recipients would increase their labor supply in response to

the reduction in benefits and changes in eligibility, resulting in an increase of 0.02%

of earnings-weighted hours by 2034.

2. If the SNAP changes were enacted on their own, other workers would be expected to

decrease their labor supply in response to the higher state labor income taxes that

would be needed to finance the additional state SNAP expenditures. However, on net,

the bill as a whole is estimated to result in lower state spending in most years over the

2025–2034 period, mainly because of the changes to Medicaid as well as states’

expected response to those changes. Taken together, TAD estimates that the

decrease in state labor income taxes would generate a slight increase in

earnings-weighted hours until 2033.

25.

24

CBO extrapolates changesin enrollees’ labor supply from the empirical literature, which has focused on SNAP’s work requirement. GDP = gross domestic product.

SNAP recipients would work more in response to the expansion of the work requirement, policies that would

reduce eligibility (primarily those requiring matching funds), and the change to the Thrifty Food Plan.

SNAP recipients might work less in response to reductions in the housing allowance, but that reduction would

probably be negligible. Reducing the allowance would tend to discourage part-time work but encourage

additional work among enrollees already working part-time.

Taken together, the earnings-weighted hours of enrollees would increase.

Changes in the Labor Supply of Enrollees in 2034, by Policy Option

Labor Supply Effects for SNAP Recipients

Conventional Estimate of

Change in Federal SNAP

Spending

Change in Enrollees’ Earnings

(Holding Hourly Wages Constant)

Feedback to Deficit from Taxes on

Change in Earnings

Millions of

Dollars % of GDP

Millions of

Dollars

% of Earnings

of Affected

Enrollees

% of Change

in Spending

% of

National

Earnings

Projected

Marginal

Tax Rate

Millions of

Dollars

% of

Reduction in

Spending

Expanding the Work Requirement -$10,940 0.03% $2,610 2.56% 23.86% 0.01% 15% -$392 3.58%

All SNAP Policies -$38,307 0.09% $2,911 2.00% 7.60% 0.02% 15% -$437 1.14%

26.

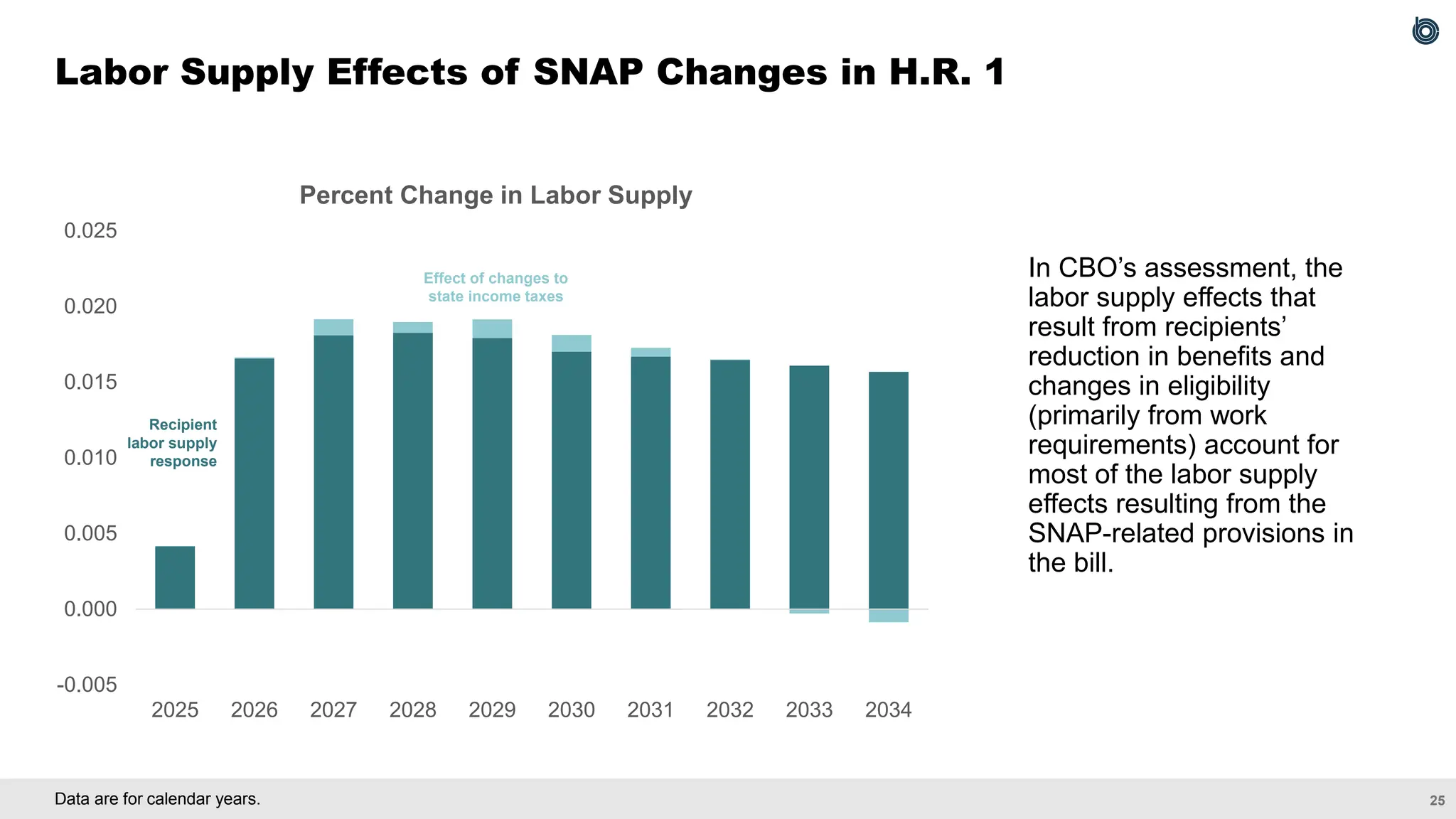

25

Data are forcalendar years.

Labor Supply Effects of SNAP Changes in H.R. 1

In CBO’s assessment, the

labor supply effects that

result from recipients’

reduction in benefits and

changes in eligibility

(primarily from work

requirements) account for

most of the labor supply

effects resulting from the

SNAP-related provisions in

the bill.

-0.005

0.000

0.005

0.010

0.015

0.020

0.025

2025 2026 2027 2028 2029 2030 2031 2032 2033 2034

Percent Change in Labor Supply

Effect of changes to

state income taxes

Recipient

labor supply

response

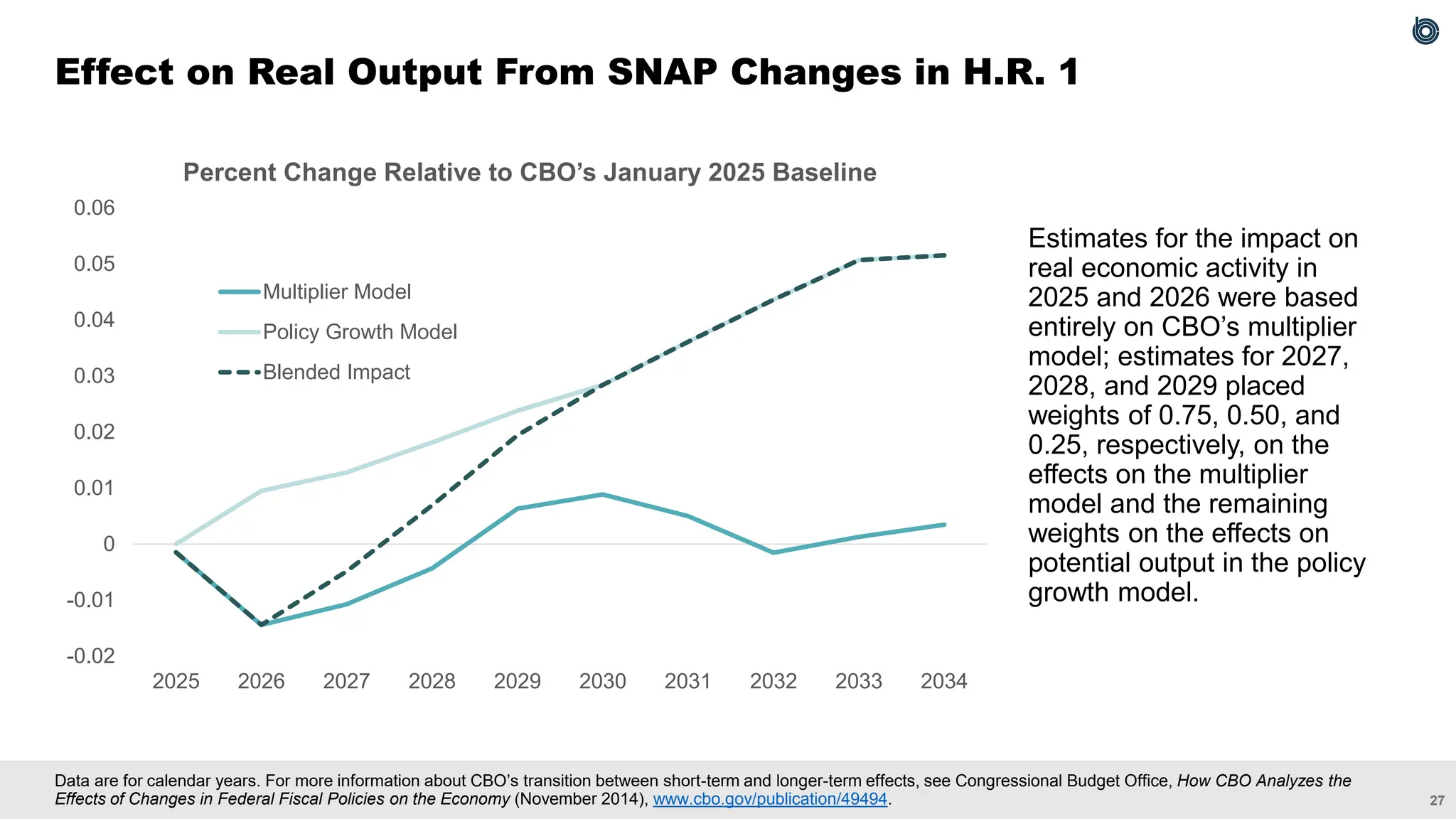

27

Data are forcalendar years. For more information about CBO’s transition between short-term and longer-term effects, see Congressional Budget Office, How CBO Analyzes the

Effects of Changes in Federal Fiscal Policies on the Economy (November 2014), www.cbo.gov/publication/49494.

Effect on Real Output From SNAP Changes in H.R. 1

Estimates for the impact on

real economic activity in

2025 and 2026 were based

entirely on CBO’s multiplier

model; estimates for 2027,

2028, and 2029 placed

weights of 0.75, 0.50, and

0.25, respectively, on the

effects on the multiplier

model and the remaining

weights on the effects on

potential output in the policy

growth model.

-0.02

-0.01

0

0.01

0.02

0.03

0.04

0.05

0.06

2025 2026 2027 2028 2029 2030 2031 2032 2033 2034

Percent Change Relative to CBO’s January 2025 Baseline

Multiplier Model

Policy Growth Model

Blended Impact

29.

28

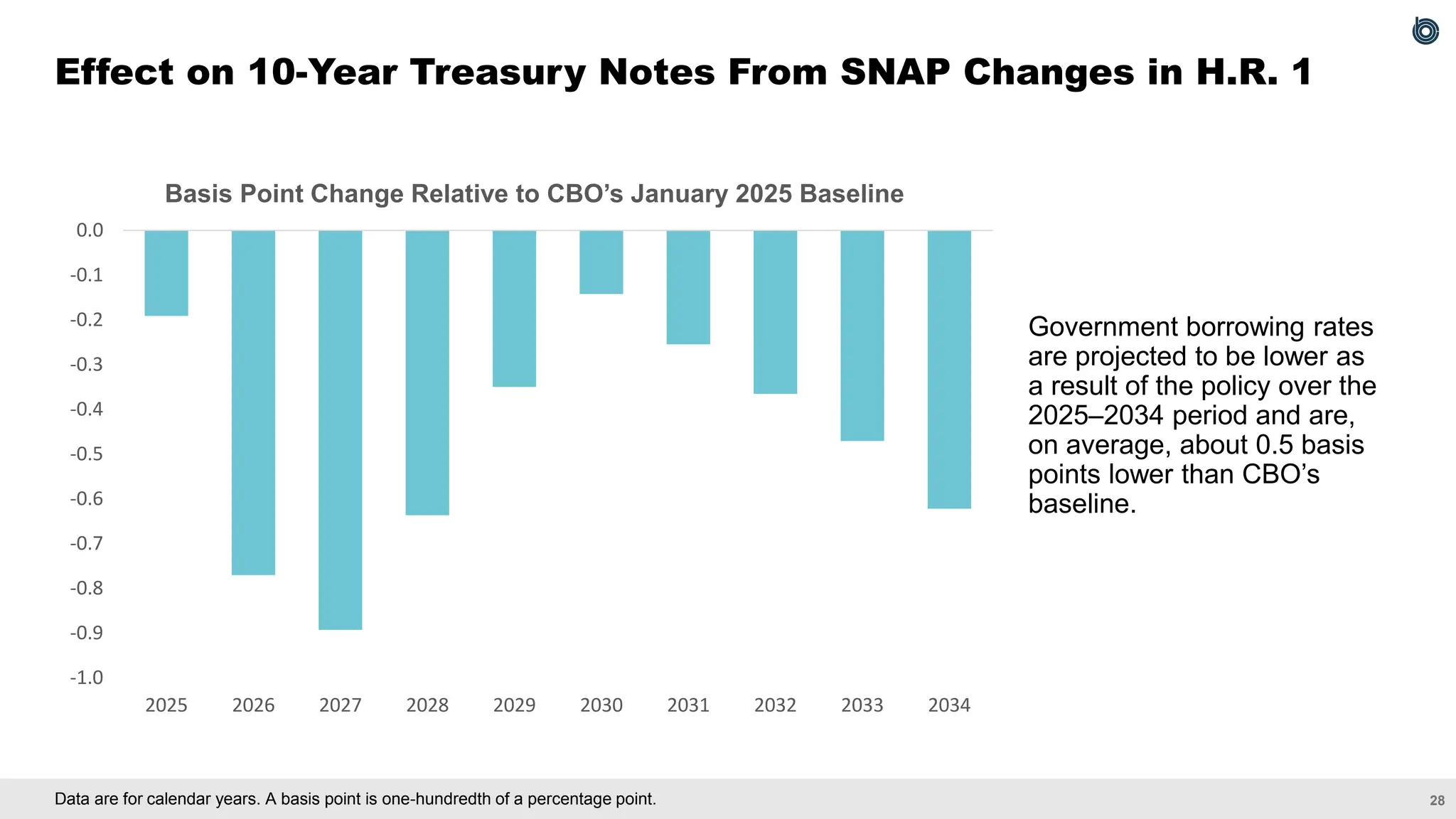

Data are forcalendar years. A basis point is one-hundredth of a percentage point.

Effect on 10-Year Treasury Notes From SNAP Changes in H.R. 1

Government borrowing rates

are projected to be lower as

a result of the policy over the

2025–2034 period and are,

on average, about 0.5 basis

points lower than CBO’s

baseline.

-1.0

-0.9

-0.8

-0.7

-0.6

-0.5

-0.4

-0.3

-0.2

-0.1

0.0

2025 2026 2027 2028 2029 2030 2031 2032 2033 2034

Basis Point Change Relative to CBO’s January 2025 Baseline

30.

29

For more detailson CBO’s dynamic analysis of all the provisions in H.R. 1, see Congressional Budget Office, H.R. 1, One Big Beautiful Bill Act (Dynamic Estimate) (June 17, 2025),

www.cbo.gov/publication/61486.

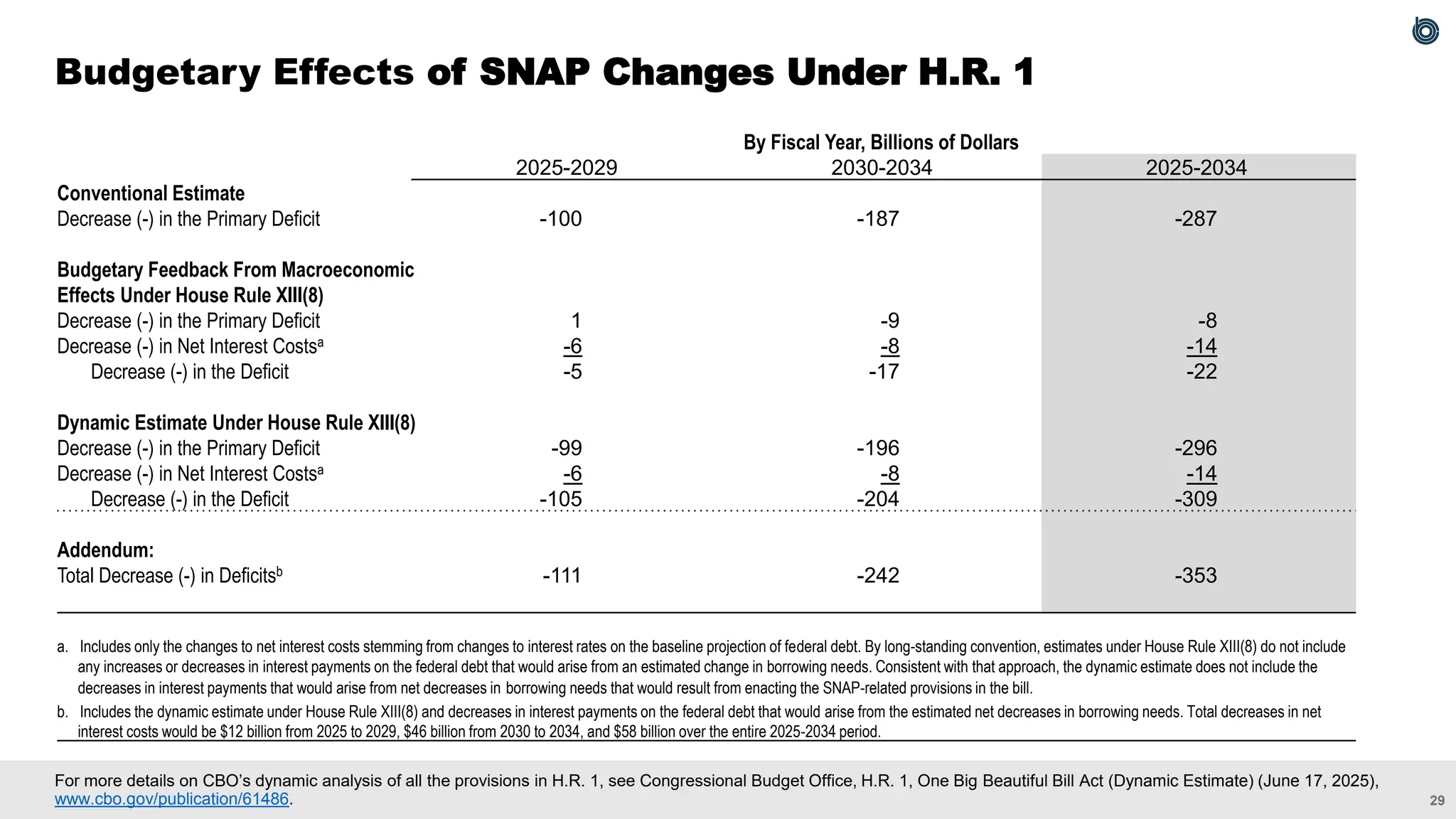

Budgetary Effects of SNAP Changes Under H.R. 1

By Fiscal Year, Billions of Dollars

2025-2029 2030-2034 2025-2034

Conventional Estimate

Decrease (-) in the Primary Deficit -100 -187 -287

Budgetary Feedback From Macroeconomic

Effects Under House Rule XIII(8)

Decrease (-) in the Primary Deficit 1 -9 -8

Decrease (-) in Net Interest Costsa -6 -8 -14

Decrease (-) in the Deficit -5 -17 -22

Dynamic Estimate Under House Rule XIII(8)

Decrease (-) in the Primary Deficit -99 -196 -296

Decrease (-) in Net Interest Costsa -6 -8 -14

Decrease (-) in the Deficit -105 -204 -309

Addendum:

Total Decrease (-) in Deficitsb -111 -242 -353

a. Includes only the changes to net interest costs stemming from changes to interest rates on the baseline projection of federal debt. By long-standing convention, estimates under House Rule XIII(8) do not include

any increases or decreases in interest payments on the federal debt that would arise from an estimated change in borrowing needs. Consistent with that approach, the dynamic estimate does not include the

decreases in interest payments that would arise from net decreases in borrowing needs that would result from enacting the SNAP-related provisions in the bill.

b. Includes the dynamic estimate under House Rule XIII(8) and decreases in interest payments on the federal debt that would arise from the estimated net decreases in borrowing needs. Total decreases in net

interest costs would be $12 billion from 2025 to 2029, $46 billion from 2030 to 2034, and $58 billion over the entire 2025-2034 period.

31.

30

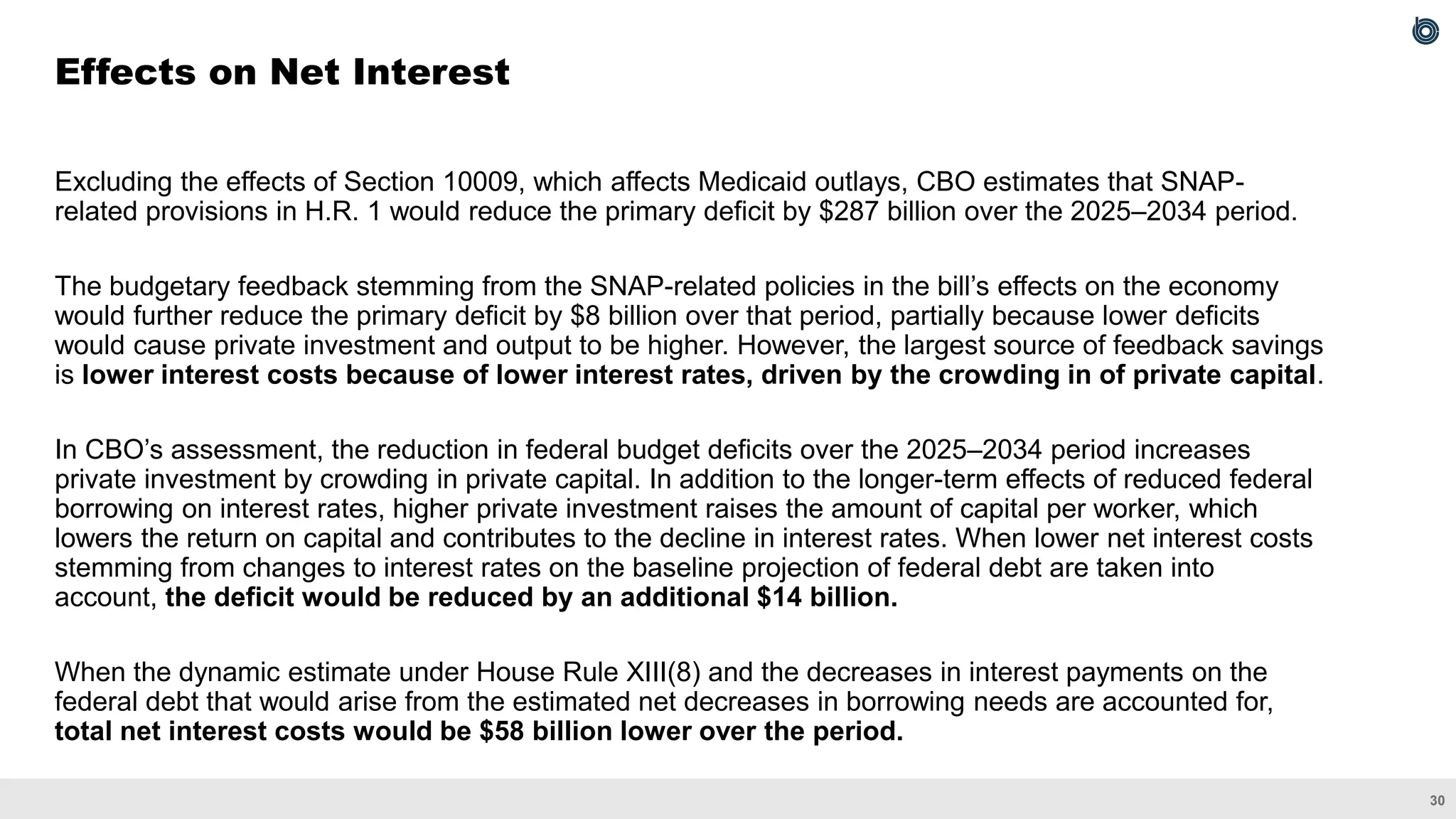

Effects on NetInterest

Excluding the effects of Section 10009, which affects Medicaid outlays, CBO estimates that SNAP-

related provisions in H.R. 1 would reduce the primary deficit by $287 billion over the 2025–2034 period.

The budgetary feedback stemming from the SNAP-related policies in the bill’s effects on the economy

would further reduce the primary deficit by $8 billion over that period, partially because lower deficits

would cause private investment and output to be higher. However, the largest source of feedback savings

is lower interest costs because of lower interest rates, driven by the crowding in of private capital.

In CBO’s assessment, the reduction in federal budget deficits over the 2025–2034 period increases

private investment by crowding in private capital. In addition to the longer-term effects of reduced federal

borrowing on interest rates, higher private investment raises the amount of capital per worker, which

lowers the return on capital and contributes to the decline in interest rates. When lower net interest costs

stemming from changes to interest rates on the baseline projection of federal debt are taken into

account, the deficit would be reduced by an additional $14 billion.

When the dynamic estimate under House Rule XIII(8) and the decreases in interest payments on the

federal debt that would arise from the estimated net decreases in borrowing needs are accounted for,

total net interest costs would be $58 billion lower over the period.

32.

31

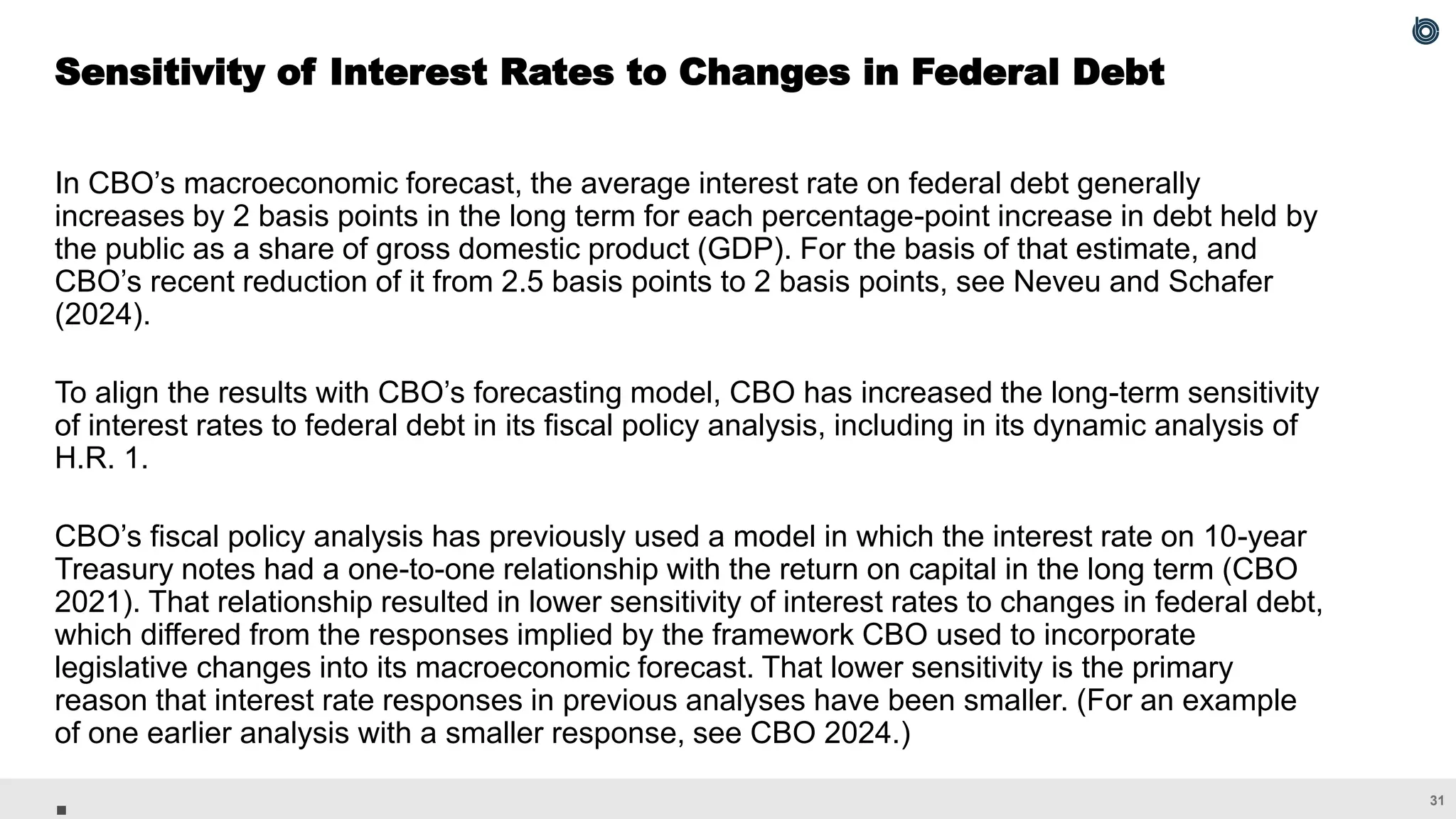

In CBO’s macroeconomicforecast, the average interest rate on federal debt generally

increases by 2 basis points in the long term for each percentage-point increase in debt held by

the public as a share of gross domestic product (GDP). For the basis of that estimate, and

CBO’s recent reduction of it from 2.5 basis points to 2 basis points, see Neveu and Schafer

(2024).

To align the results with CBO’s forecasting model, CBO has increased the long-term sensitivity

of interest rates to federal debt in its fiscal policy analysis, including in its dynamic analysis of

H.R. 1.

CBO’s fiscal policy analysis has previously used a model in which the interest rate on 10-year

Treasury notes had a one-to-one relationship with the return on capital in the long term (CBO

2021). That relationship resulted in lower sensitivity of interest rates to changes in federal debt,

which differed from the responses implied by the framework CBO used to incorporate

legislative changes into its macroeconomic forecast. That lower sensitivity is the primary

reason that interest rate responses in previous analyses have been smaller. (For an example

of one earlier analysis with a smaller response, see CBO 2024.)

Sensitivity of Interest Rates to Changes in Federal Debt

33.

32

SNAP-related provisions inthe bill are expected to lower output in the short term because of benefit

reductions for households with lower income but boost output because the labor supply and private

investment would be larger, on net, in the longer term.

After incorporating macroeconomic feedback and savings from reduced net interest costs from

lower federal debt, SNAP-related policies in H.R. 1 would reduce the federal deficit by a total of

$353 billion over the 2025–2034 period.

Current areas of uncertainty

▪ Because many policies begin to take effect in 2027 and beyond, CBO’s projected transition

between the short term and longer term mitigates the demand-side effects beginning in that year.

However, the change in demand of households and businesses may vary considerably over time.

▪ The self-financing of states is subject to considerable uncertainty. States, on average, may

respond to a lesser or greater extent than CBO currently anticipates. In addition, aggregating state

behavior may mask important differences at the state level.

Dynamic Effects of SNAP Provisions in H.R. 1

34.

33

Katherine Baicker, “GovernmentDecision-Making and the Incidence of Federal Mandates,”

Journal of Public Economics, vol. 82, no. 2 (November 2001), pp. 147–194,

https://doi.org/10.1016/S0047-2727(00)00149-3.

Jeffrey Clemens and Stephen Miran, “Fiscal Policy Multipliers on Subnational Government

Spending,” American Economic Journal: Economic Policy, vol. 4, no. 2 (May 2012), pp. 46–68,

https://doi.org/10.1257/pol.4.2.46.

Congressional Budget Office, “CBO’s Policy Growth Model” (April 2021), Slide 9,

www.cbo.gov/publication/57017.

Congressional Budget Office, “How the Expiring Individual Income Tax Provisions in the 2017

Tax Act Affect CBO’s Economic Forecast” (December 2024) Slide 15,

www.cbo.gov/publication/60986.

References

35.

34

Andre R. Neveuand Jeffrey Schafer, Revisiting the Relationship Between Debt

and Long-Term Interest Rates: Working Paper 2024-05 (Congressional Budget

Office, December 2024), www.cbo.gov/publication/60314.

James M. Poterba, “State Responses to Fiscal Crises: The Effects of Budgetary

Institutions and Politics,” Journal of Political Economy, vol. 102, no. 4 (August

1994), pp. 799–821, https://doi.org/10.1086/261955.

Kim S. Rueben, Megan Randall, and Aravind Boddupalli, Budget Processes and

the Great Recession: How State Fiscal Institutions Shape Tax and Spending

Decisions. (Urban Institute, October 2018), https://tinyurl.com/yurrkfza.

References (Continued)

36.

35

This document wasprepared to enhance the transparency of the work of the

Congressional Budget Office and to encourage external review of that work. In

keeping with CBO’s mandate to provide objective, impartial analysis, it makes no

recommendations.

The document is the result of work by analysts across CBO. It was reviewed by

Devrim Demirel, Mark Hadley, Jeffrey Kling, John McClelland, Sam Papenfuss,

and Julie Topoleski.

CBO seeks feedback to make its work as useful as possible. Please send

comments to communications@cbo.gov.

About This Document