Page | 0

The24 Hour Economy and Accelerated Export Development Programme

Ghana’s National Agenda for Productivity,

Competitiveness, and Inclusive Growth

Transforming Production, Markets, and Human Capital

Prepared by the 24H+ Secretariat

April 2025

Accra, Ghana

Page | 3

ThisProgramme document is also available as a series of standalone booklets.

Each booklet focuses on a specific section or sub-programme of the 24H+ programme.

Page | 6

TABLEOF CONTENTS

Preface _______________________________________________________ 4

EXECUTIVE SUMMARY______________________________________________ 11

1.0 Our Vision _______________________________________________ 12

2.0 The Challenge ____________________________________________ 14

3.0 24H+ Programme: An Integrated Solution ___________________________ 17

PART ONE - CONTEXT ______________________________________________ 37

1.0 Context for a 24H+ _________________________________________38

2.0 Institutional Arrangements ____________________________________49

PART TWO - Programme Components and Strategies __________________________59

3.0 The Strategy _____________________________________________60

4.0 GROW24 – Agriculture Transformation Sub-Programme __________________ 76

5.0 MAKE24 – Manufacturing Growth Sub-Programme ____________________ 106

6.0 BUILD24 – Construction Industry Transformation Sub-Programme __________ 134

7.0 SHOW24 – Culture, Arts, and Tourism Sub-Programme __________________ 154

8.0 CONNECT24 - Supply Chain and Markets Efficiency ____________________ 174

9.0 FUND24 – Mobilising Capital for Inclusive Transformation ________________ 188

10.0 ASPIRE24 – Human Capital Development __________________________ 204

11.0 GO24 – Driving Civic Commitment and Public Alignment _________________ 214

ANNEXES_____________________________________________________ 225

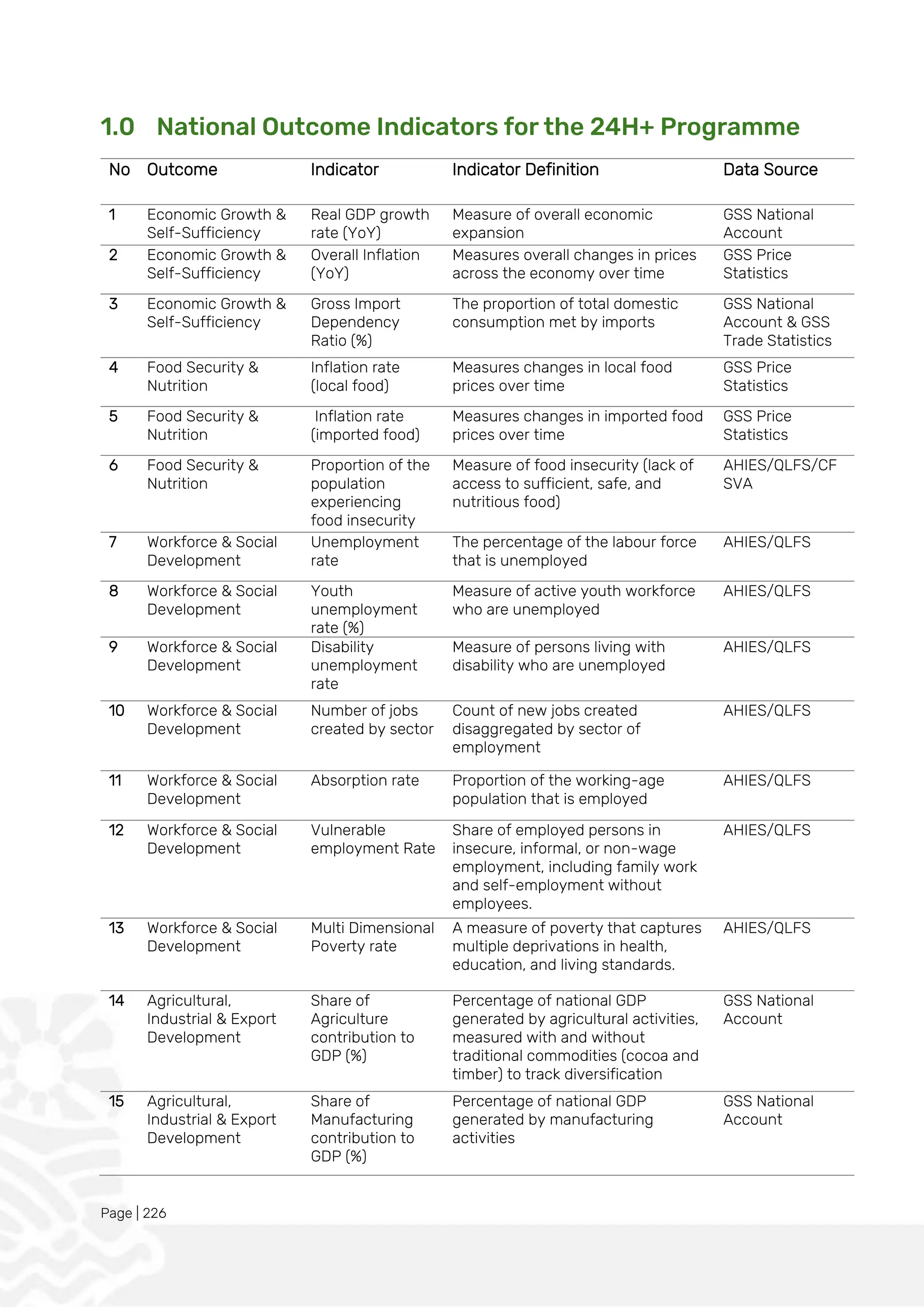

1.0 National Outcome Indicators for the 24H+ Programme __________________ 226

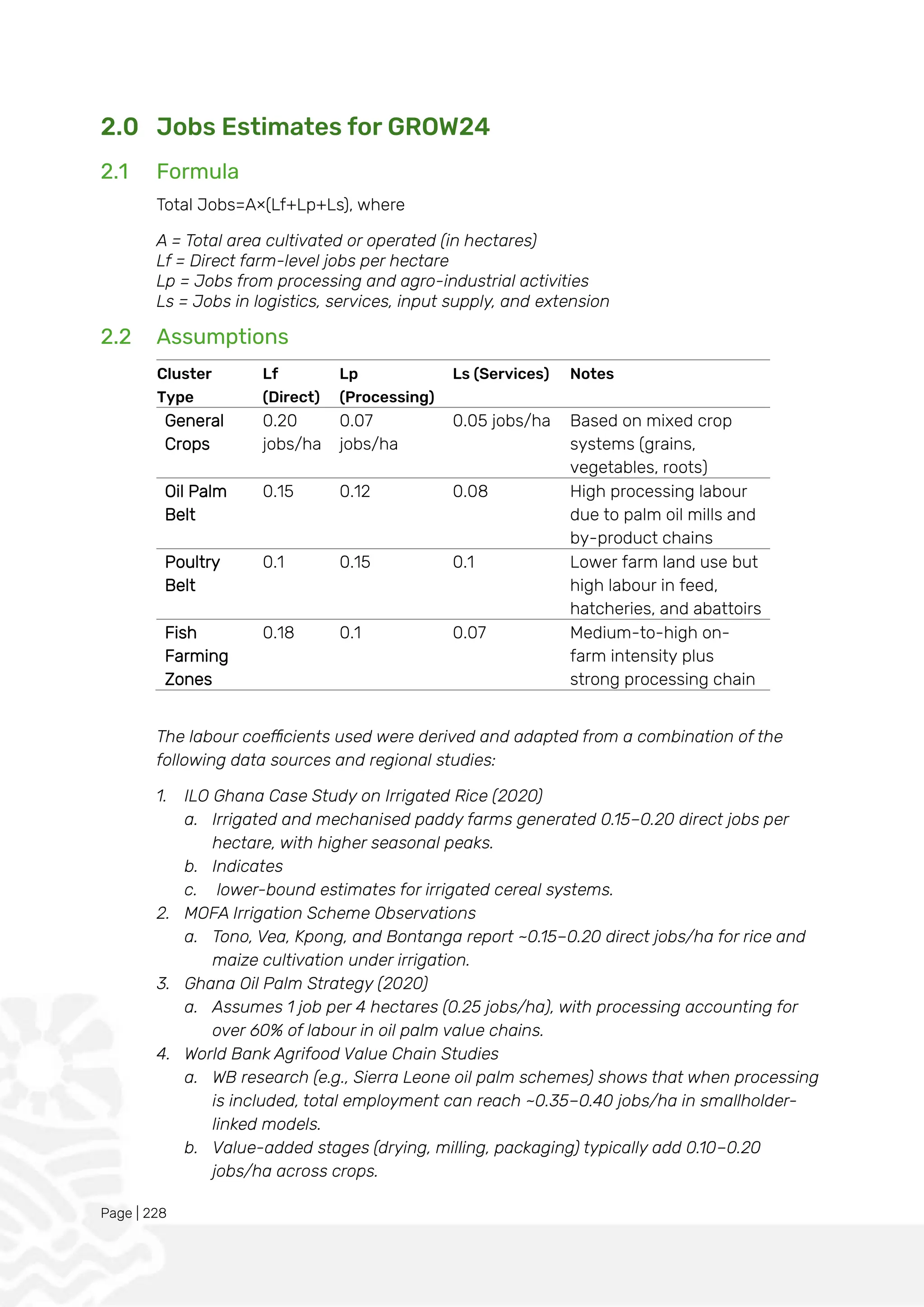

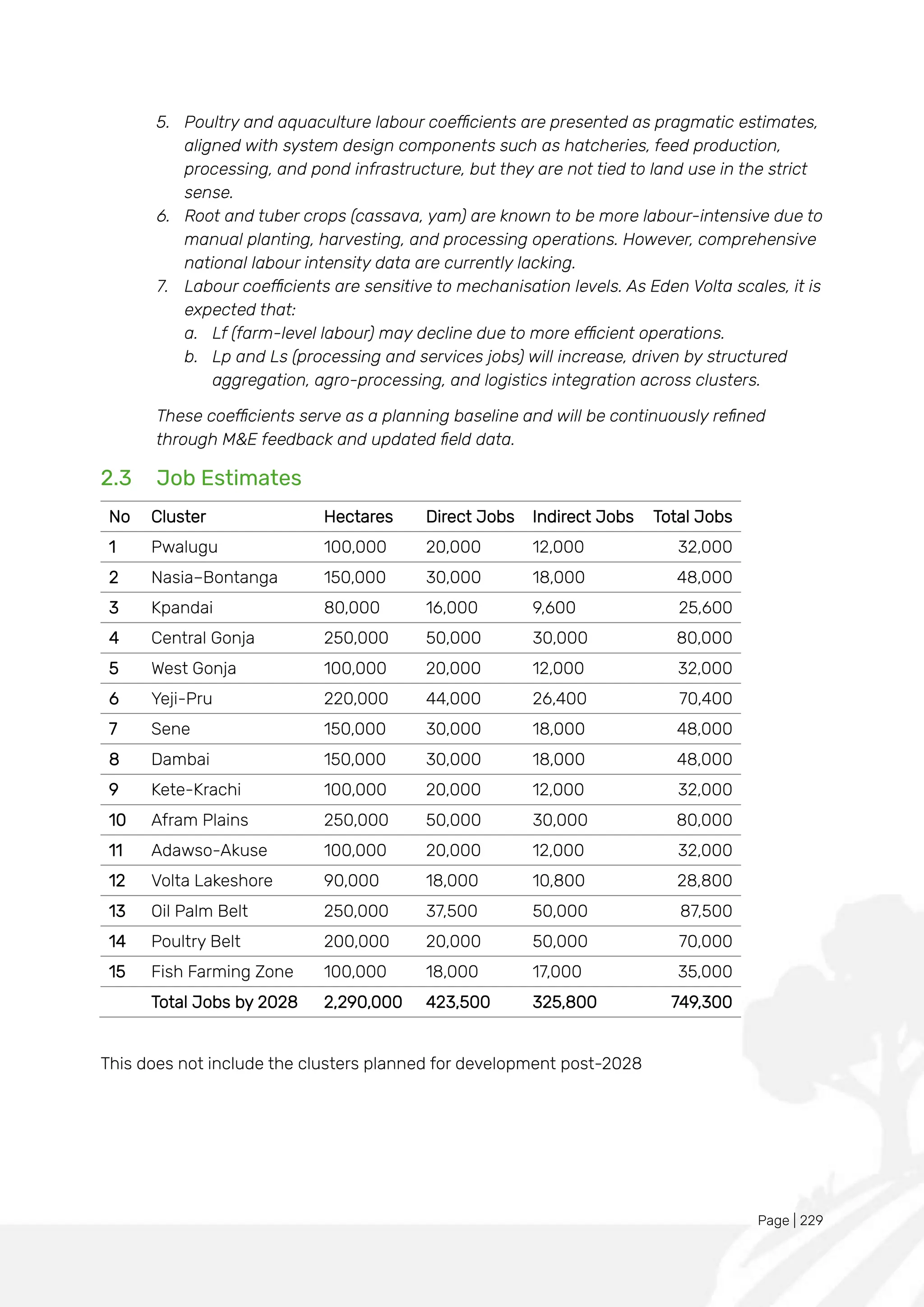

2.0 Jobs Estimates for GROW24 __________________________________ 228

3.0 Acknowledgements ________________________________________ 230

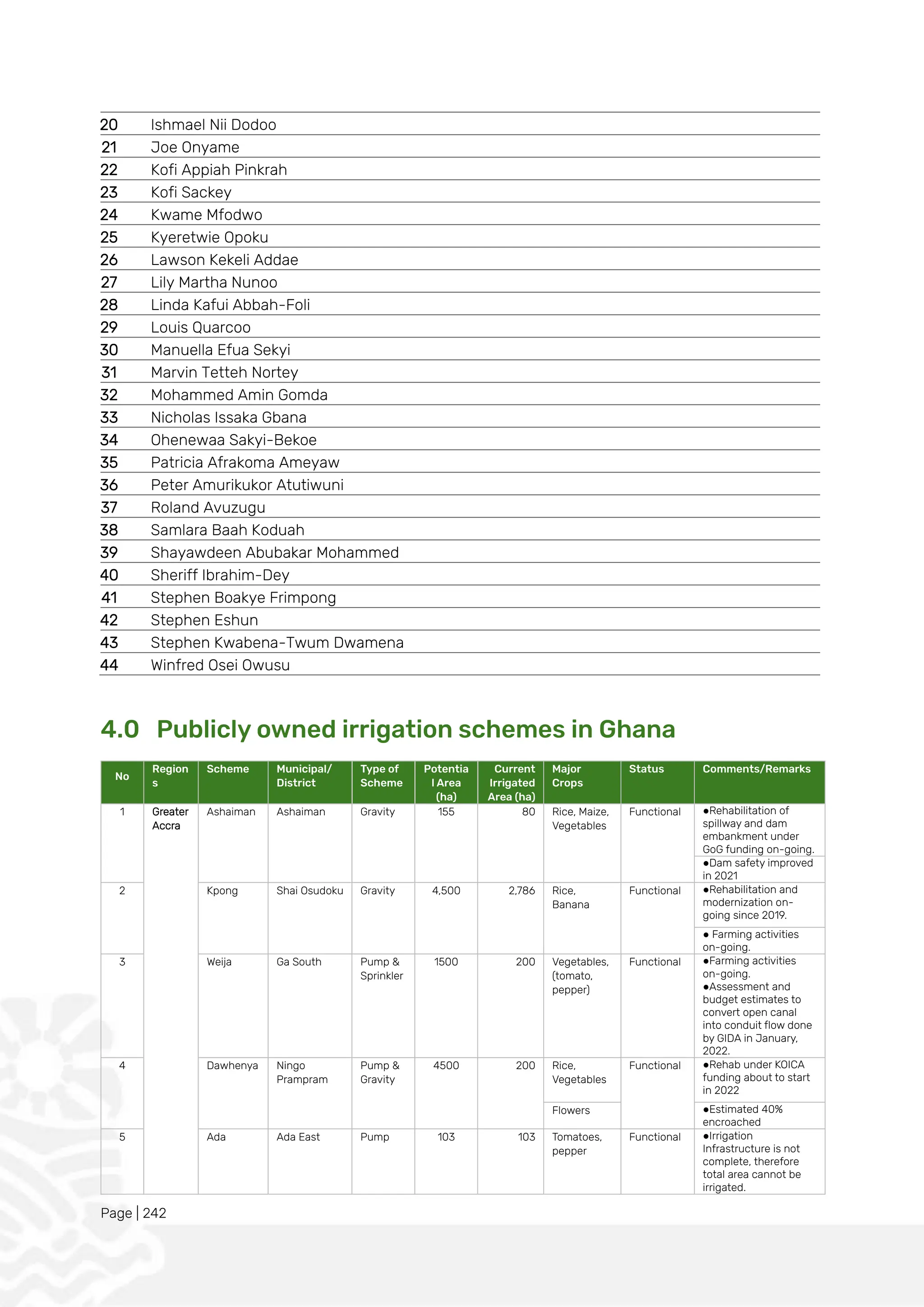

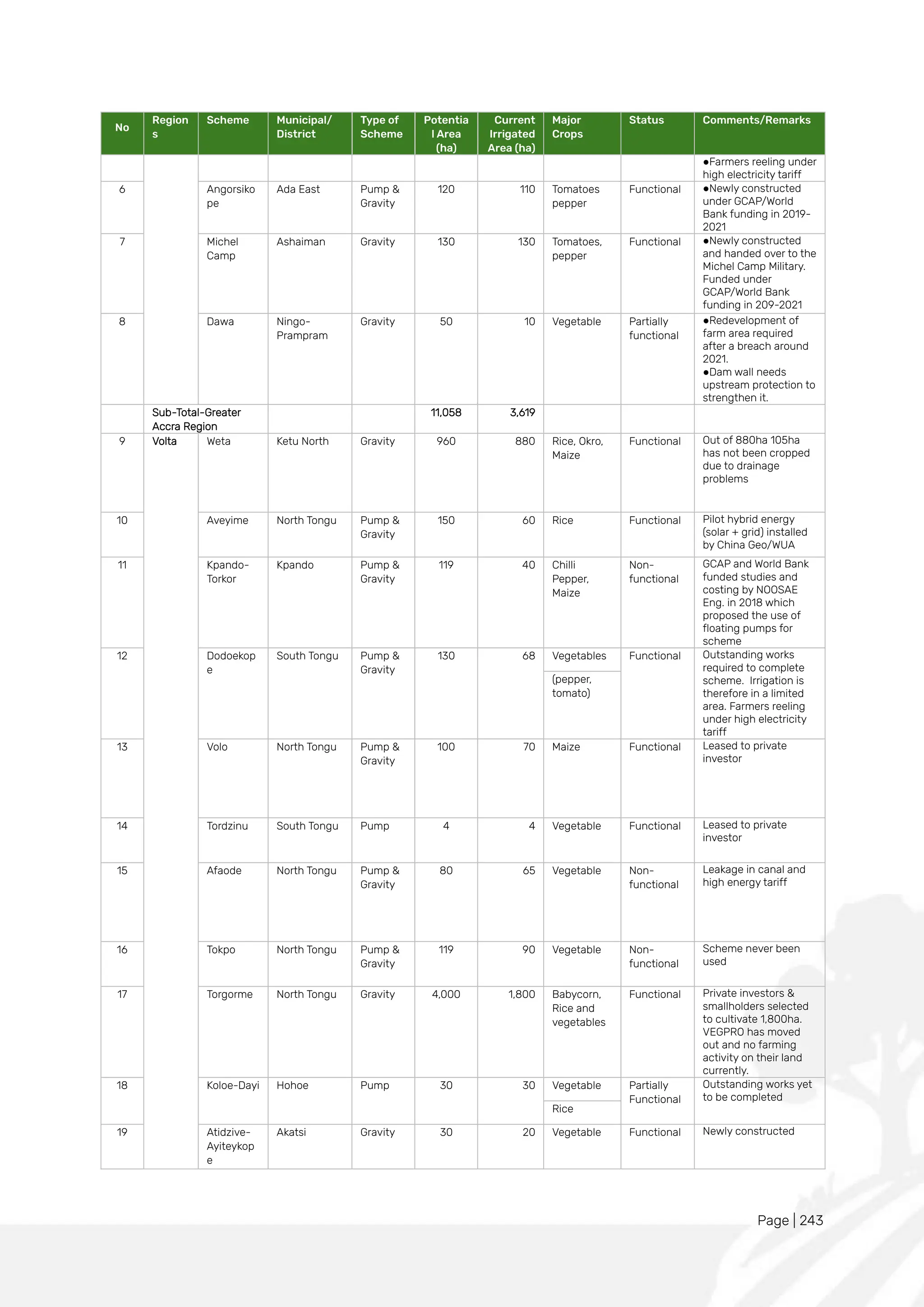

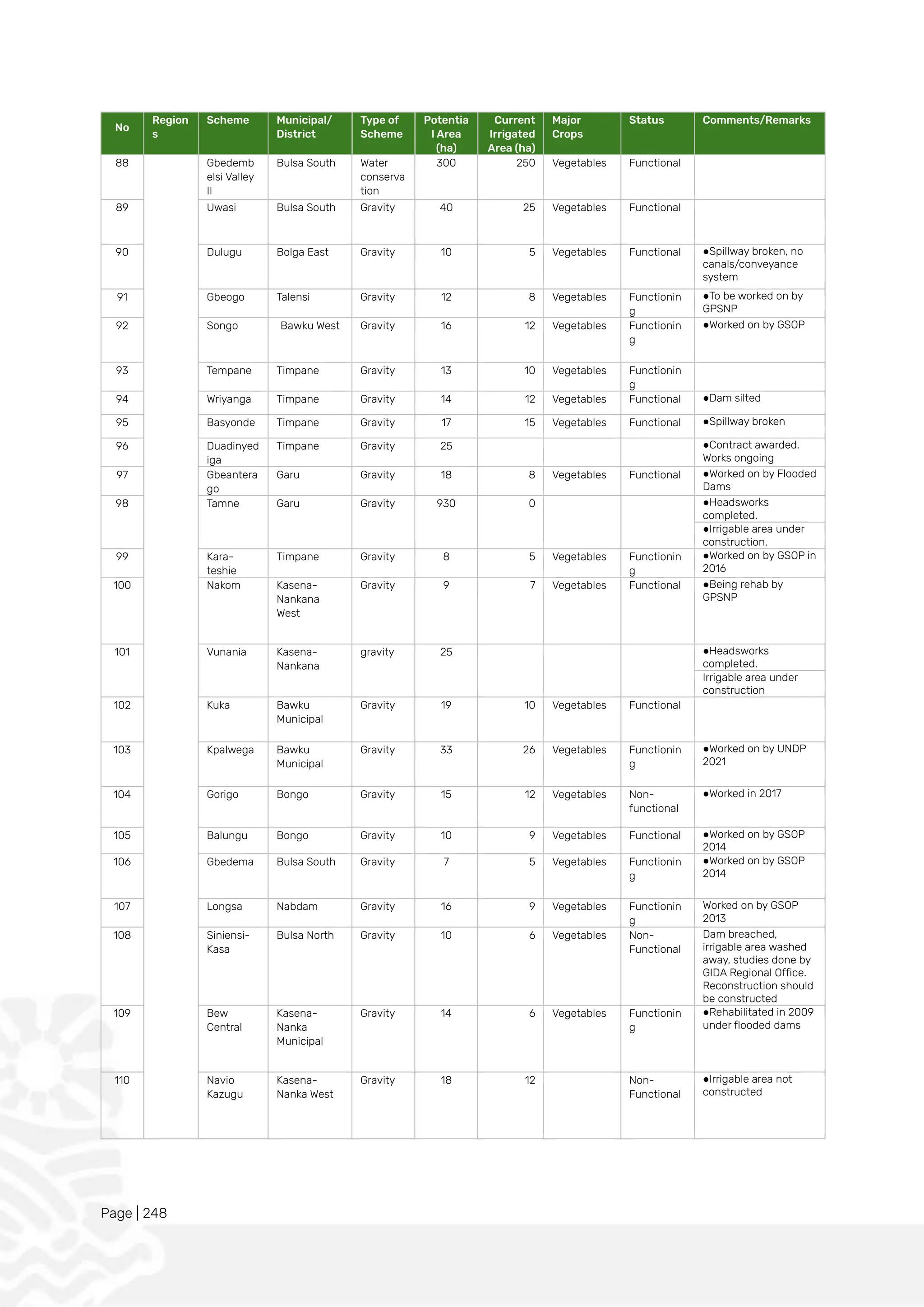

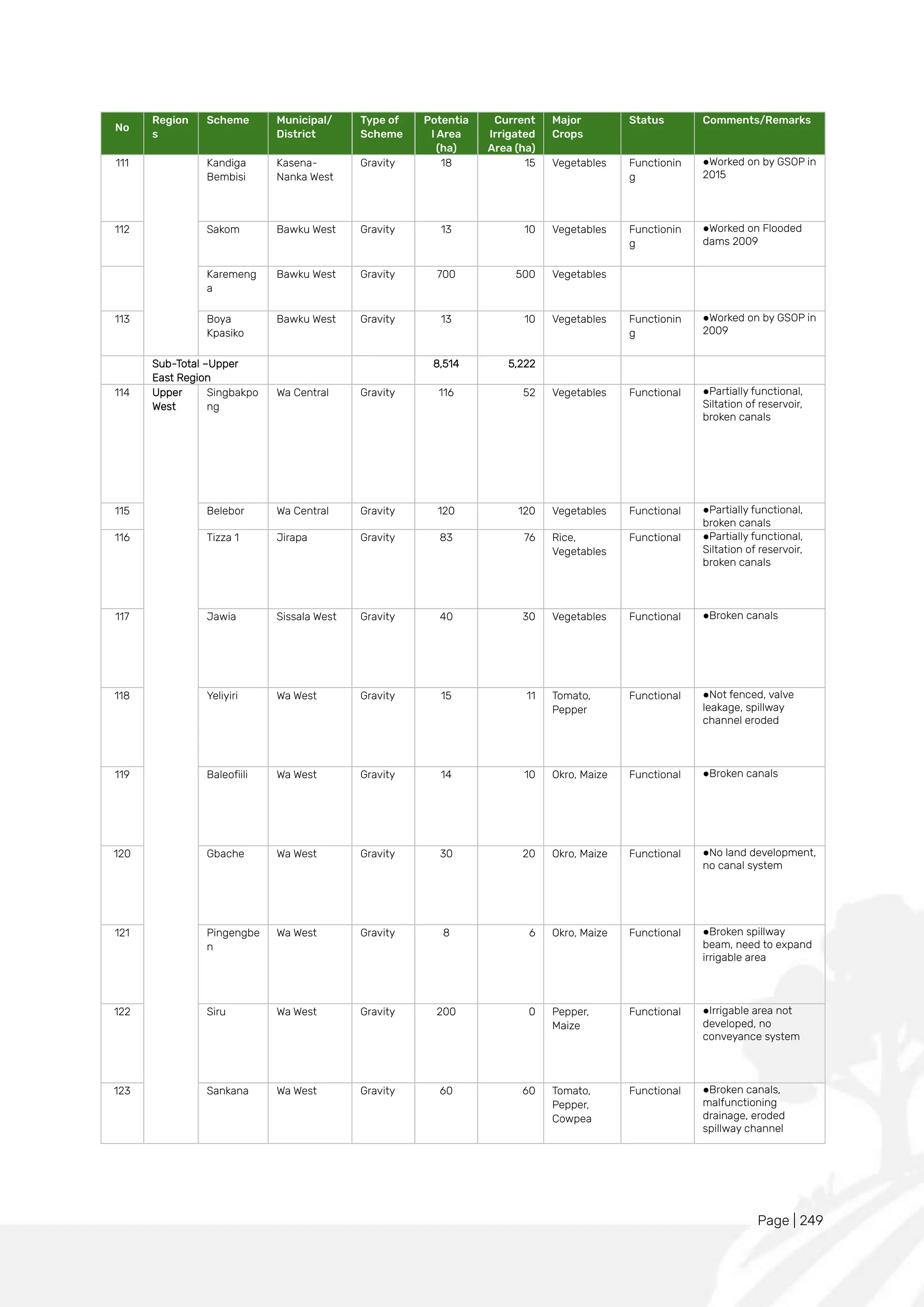

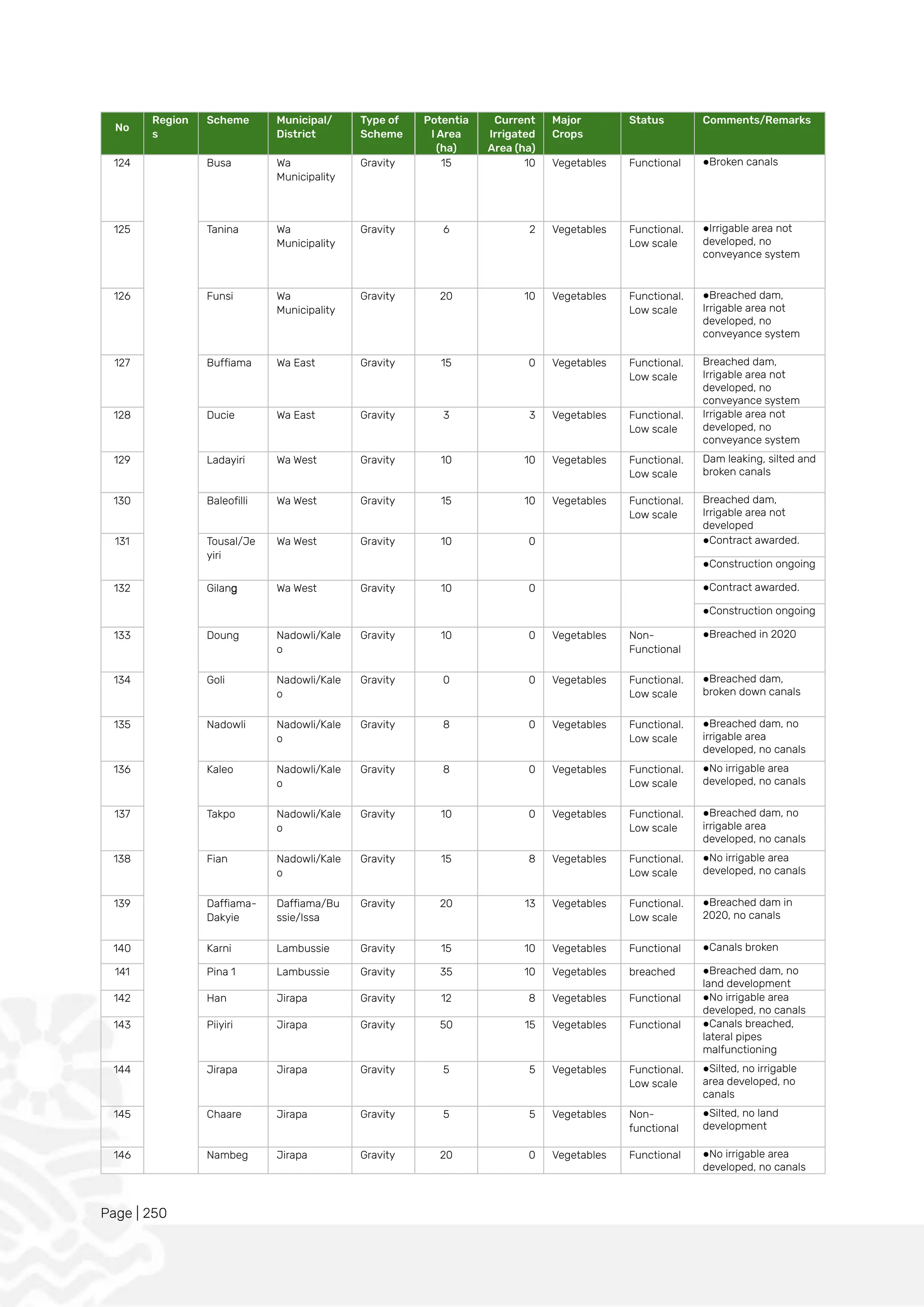

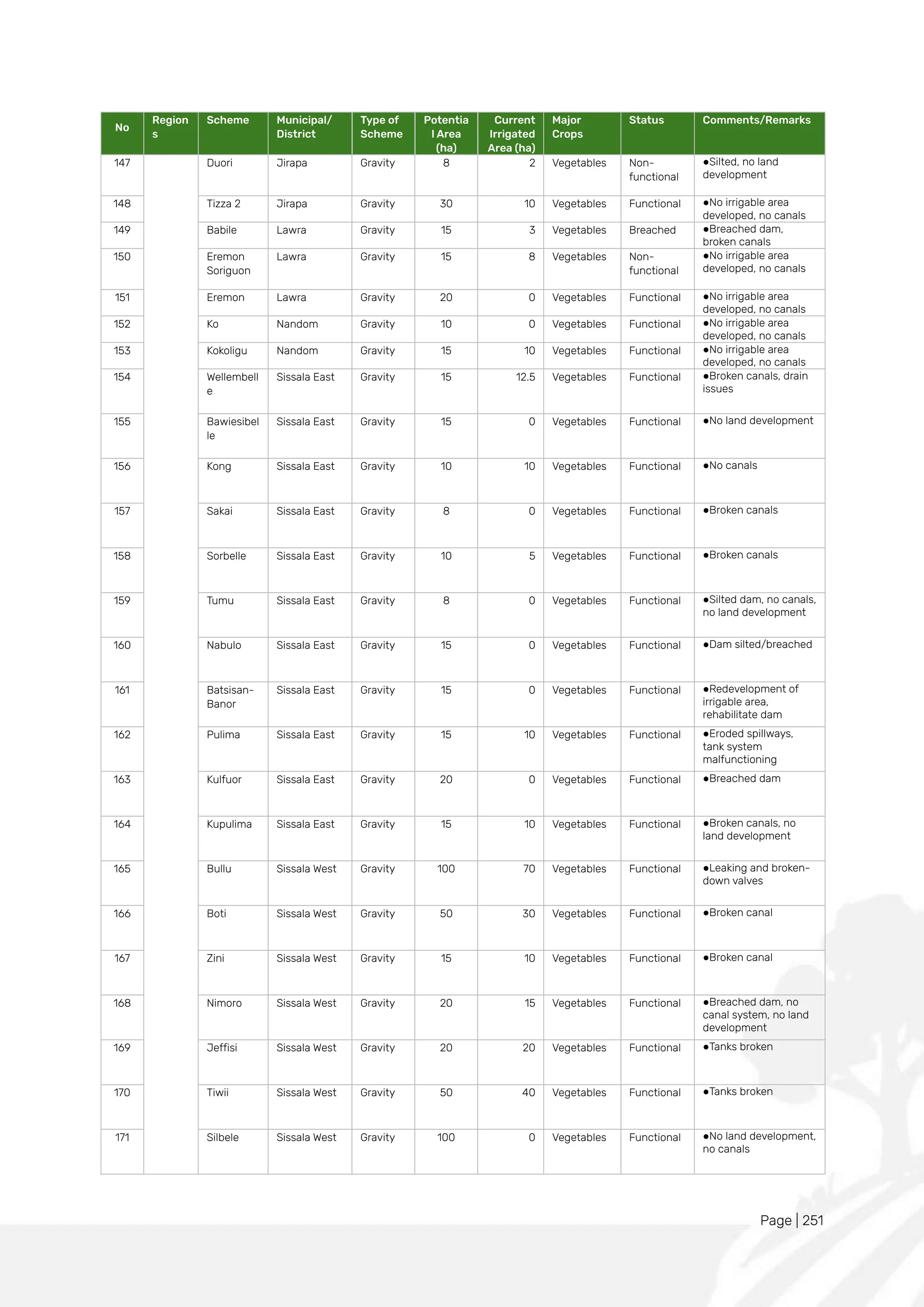

4.0 Publicly owned irrigation schemes in Ghana ________________________ 242

5.0 List of Major Poultry Farms in Ghana _____________________________ 253

6.0 List of Active GIDA Rice Growing Schemes__________________________ 254

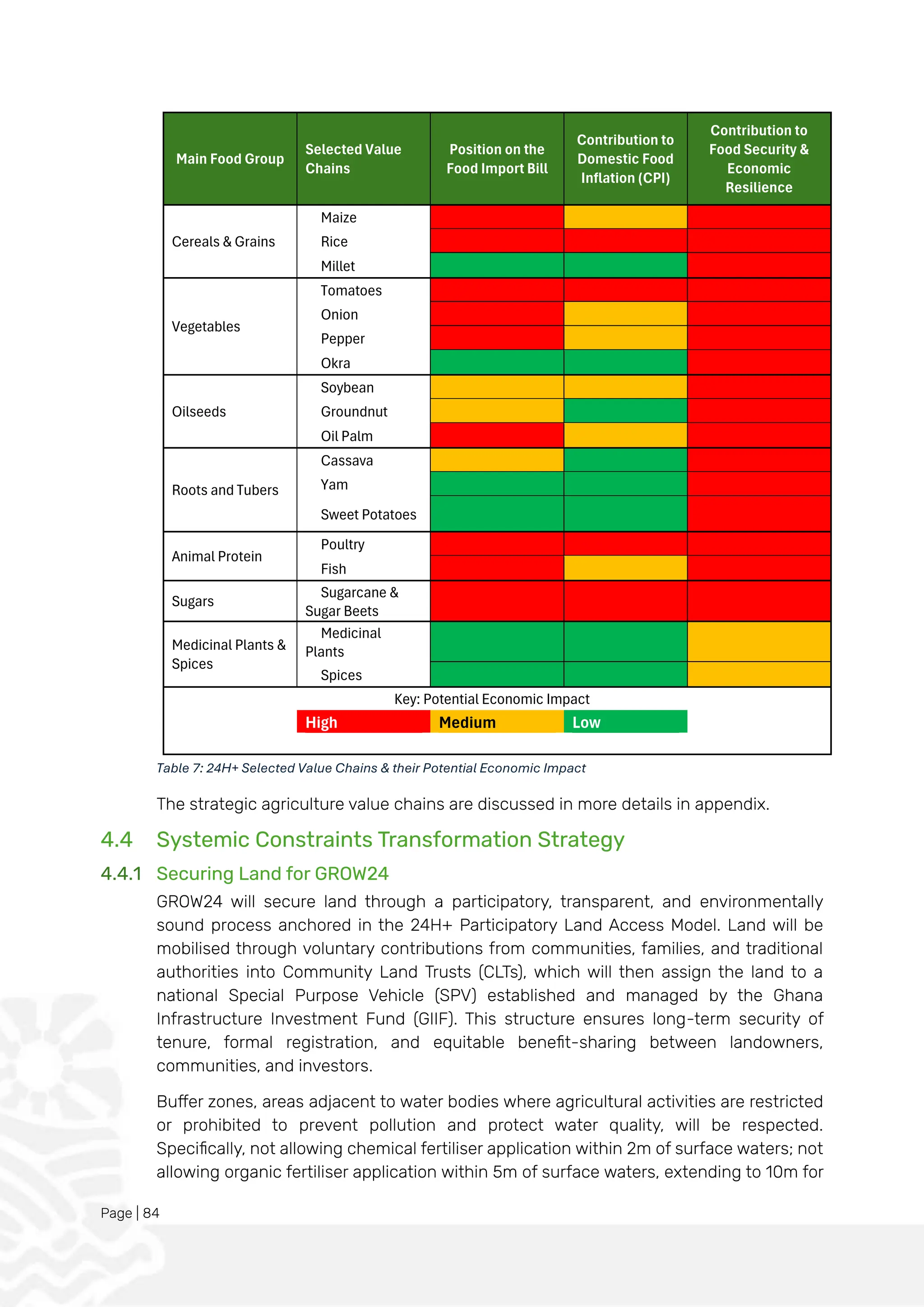

7.0 Strategic Agriculture Value Chains ______________________________ 254

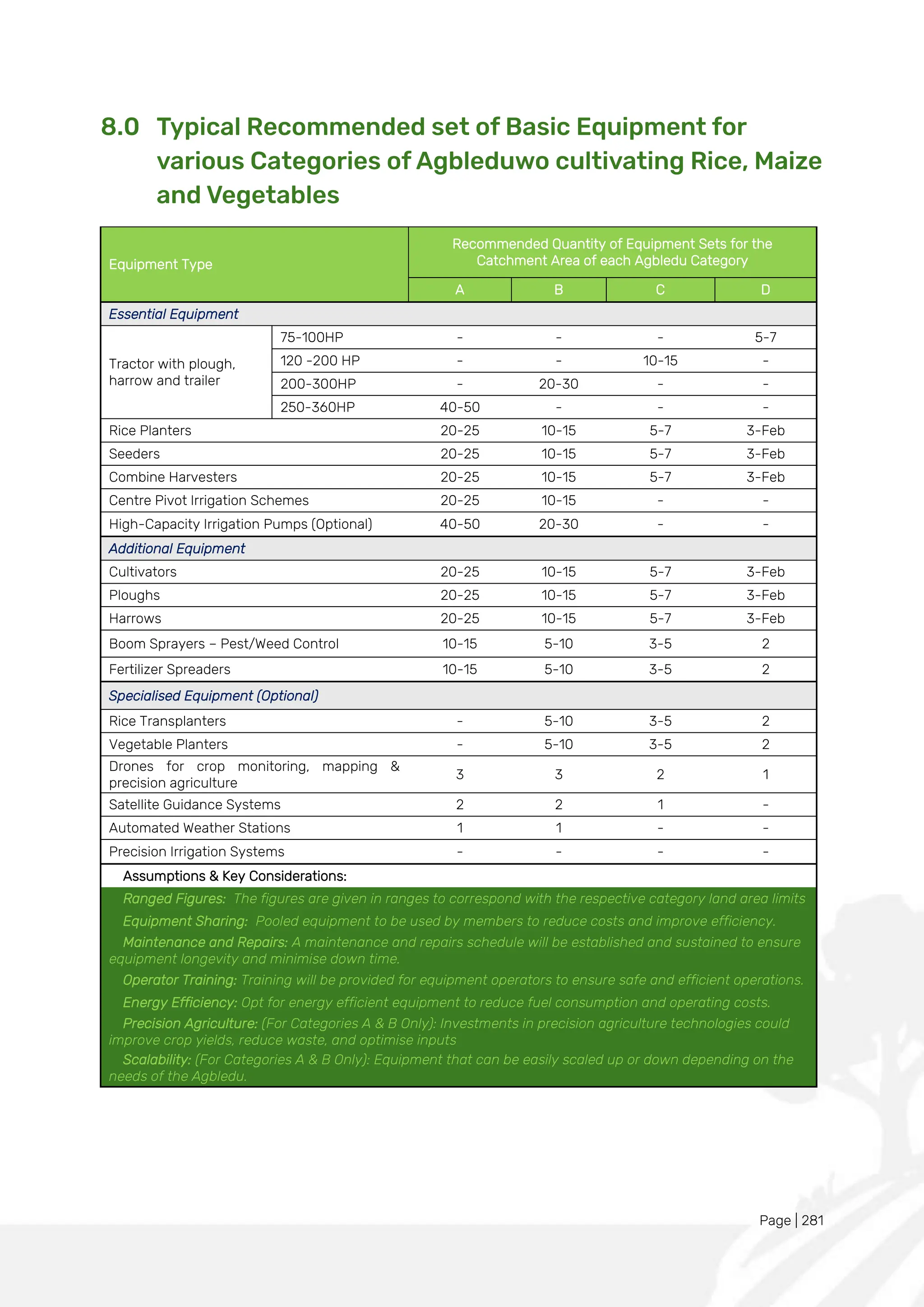

8.0 Typical Recommended set of Basic Equipment for various Categories of Agbleduwo

cultivating Rice, Maize and Vegetables_________________________________ 281

8.

Page | 7

FIGURESAND TABLES

Figure 1: Made in Ghana, Once Upon a Time............................................................................................................ 16

Figure 2: Typical Layout of an Agbledu FSC on a 4-acre land (courtesy Trotro Tractor Limited .................23

Figure 3: Composition of exports............................................................................................................................... 38

Figure 4: Sectoral contributions to GDP .................................................................................................................. 40

Figure 5: Sectoral contribution to GDP growth ...................................................................................................... 40

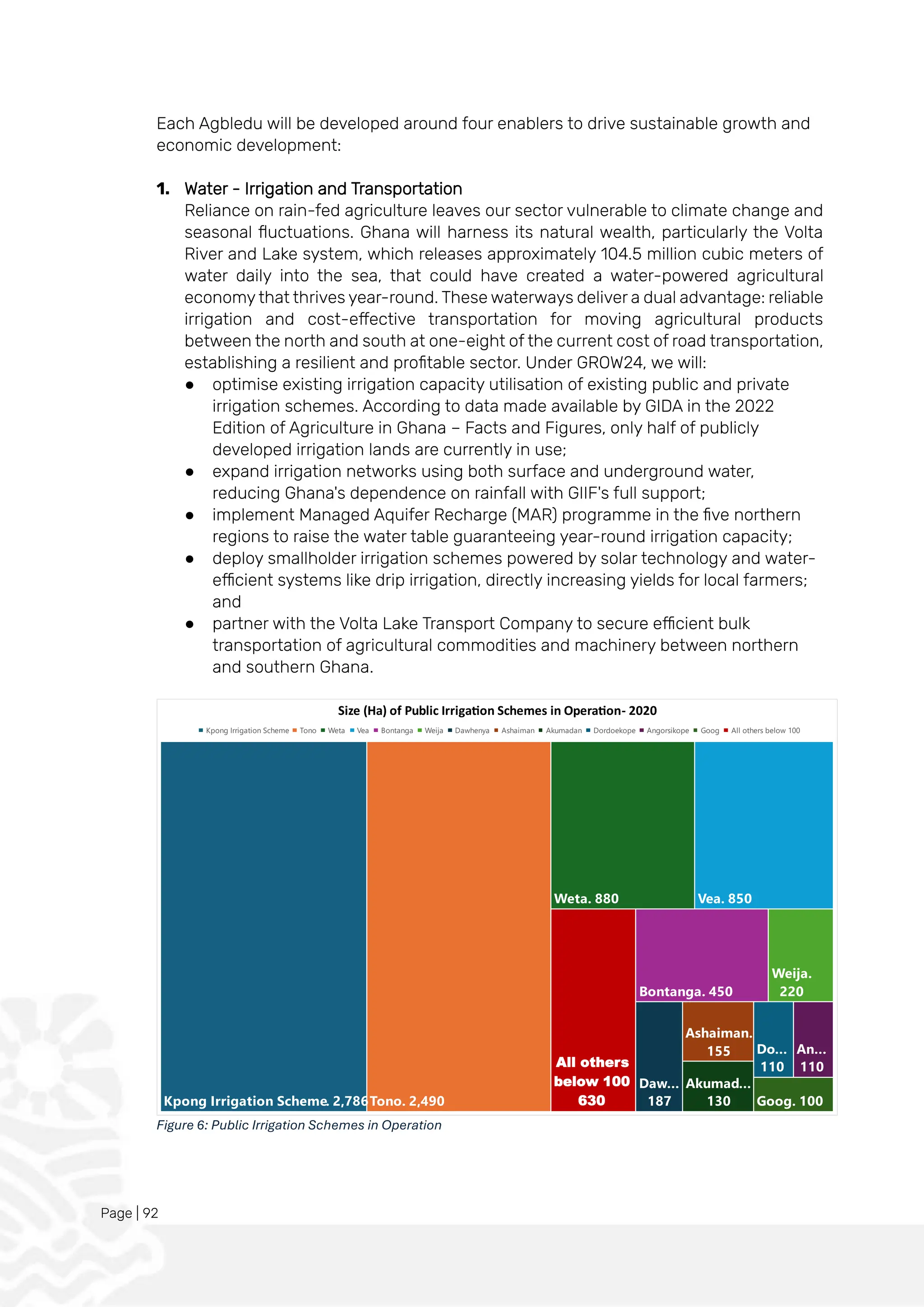

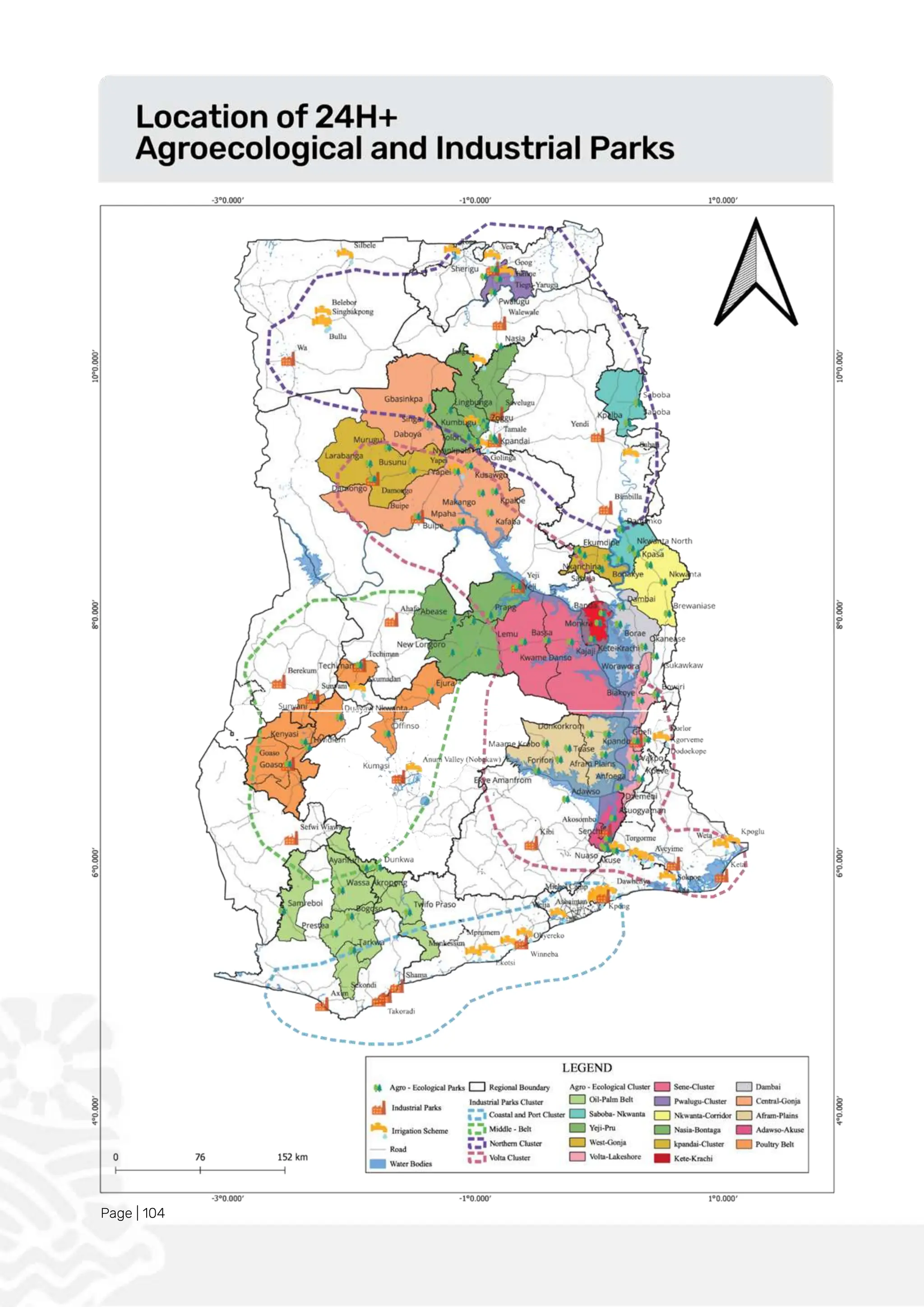

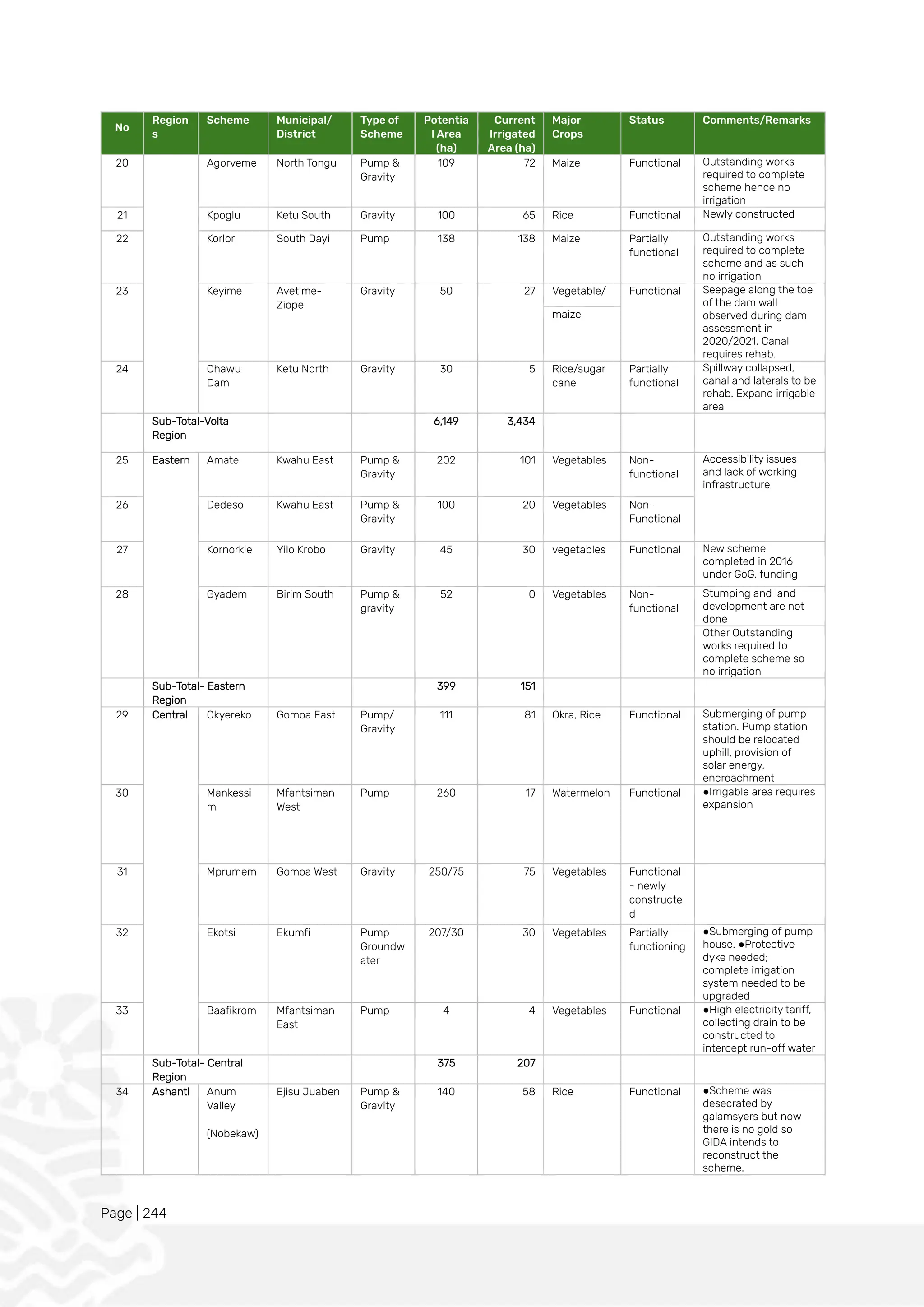

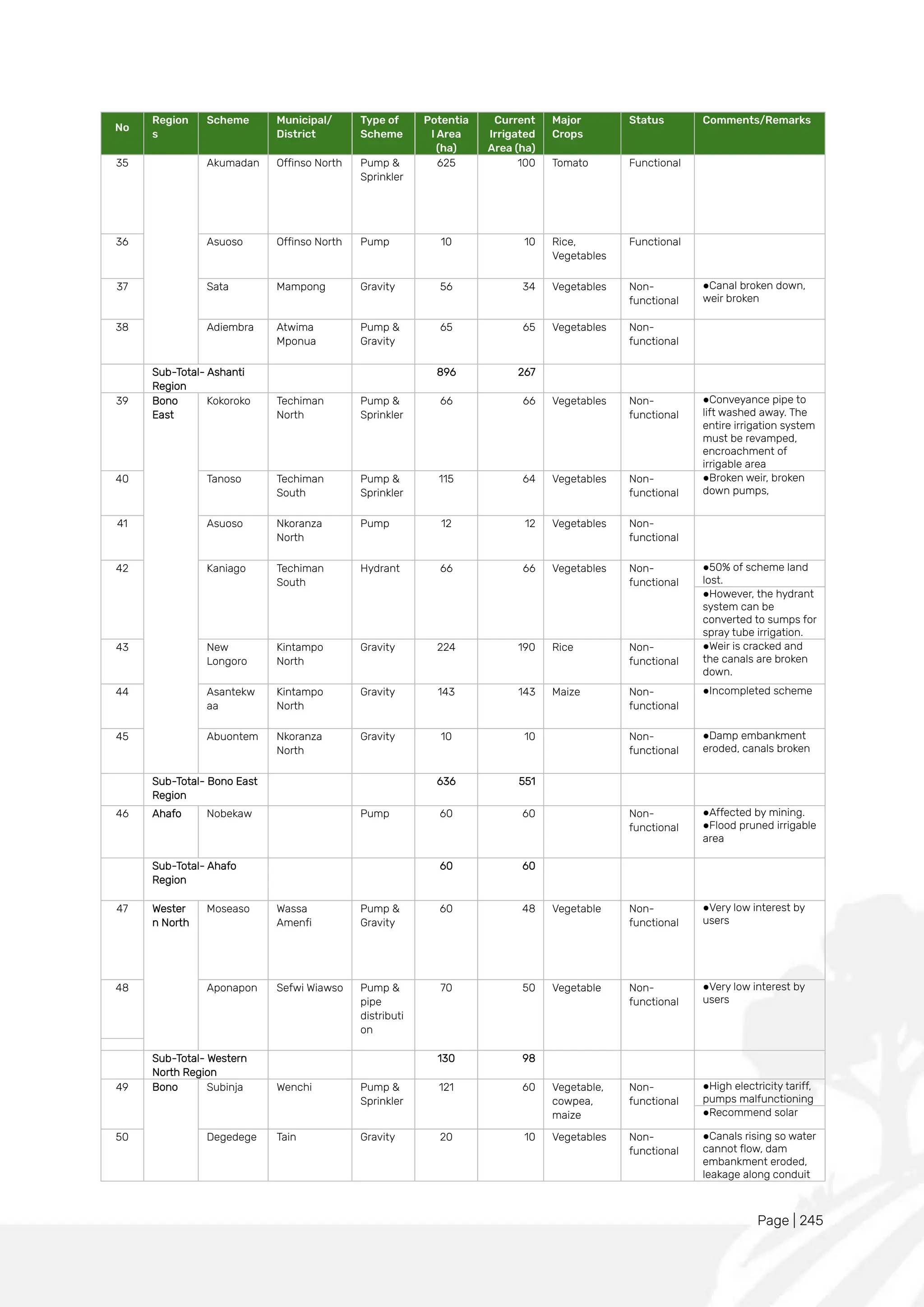

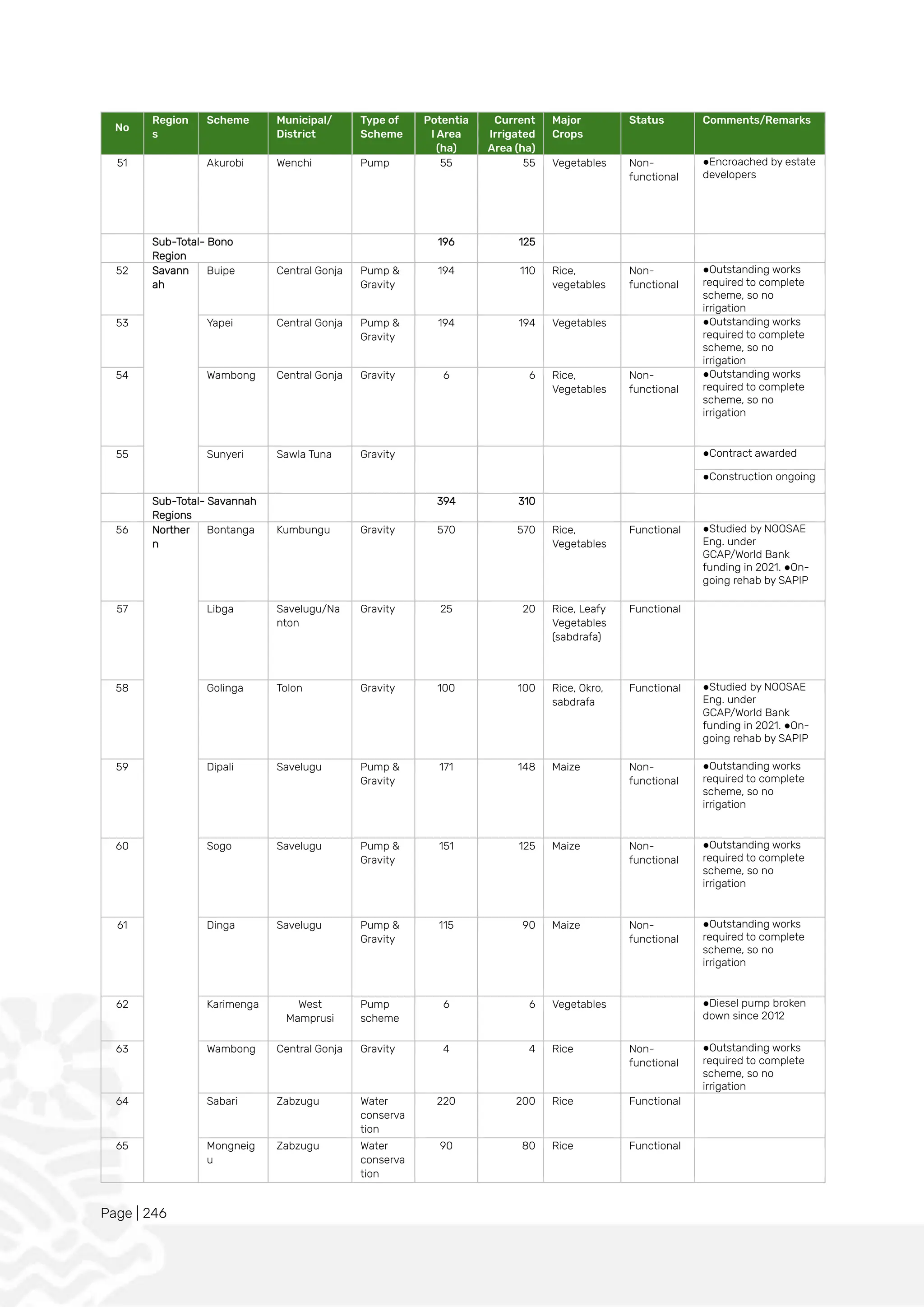

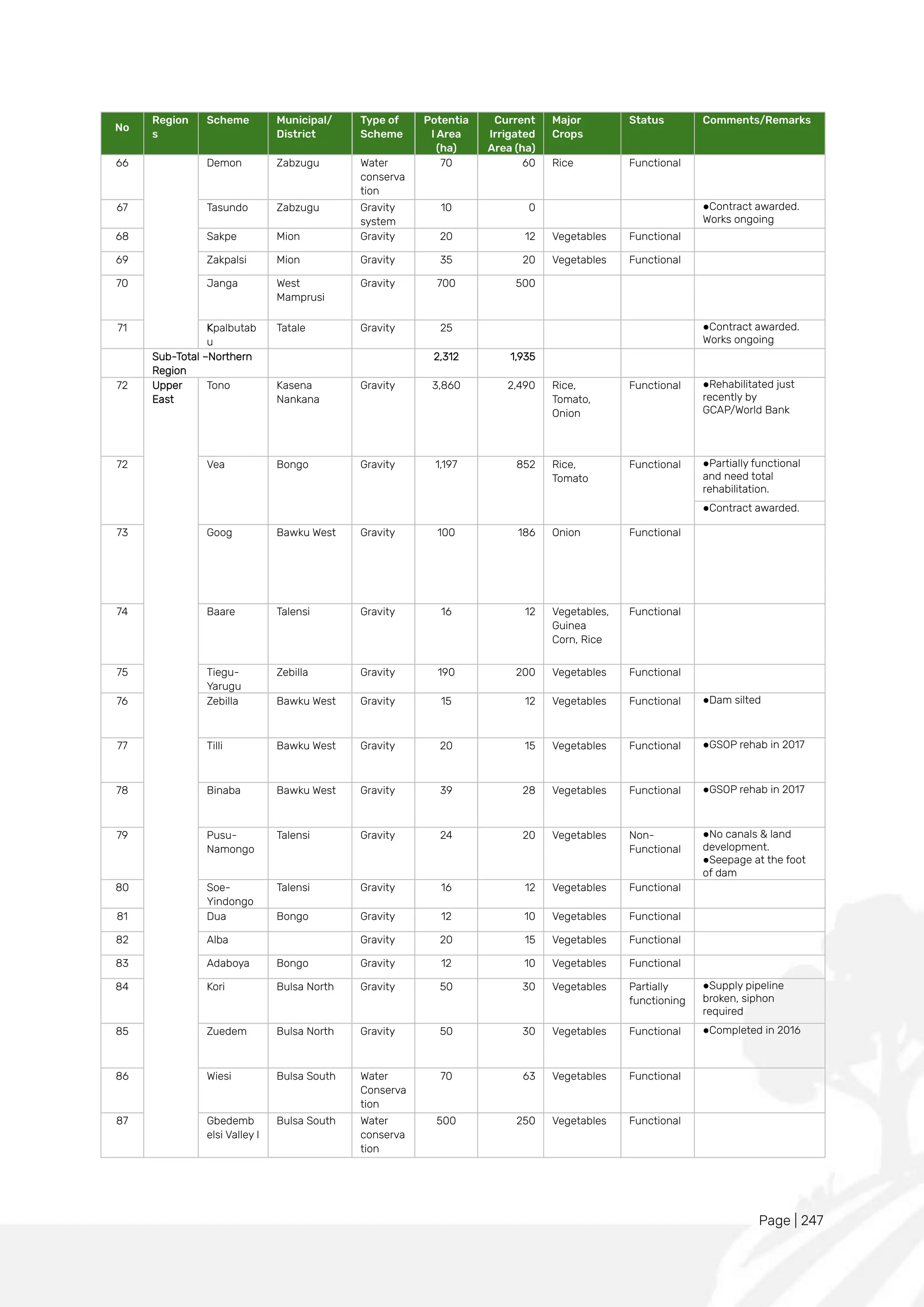

Figure 6: Public Irrigation Schemes in Operation...................................................................................................92

Table 1: Sectoral vs Integrated Approaches .............................................................................................................18

Table 2: Projected impact of the proposed economic transformation on employment ...............................35

Table 3: Food product imports in 2024 .....................................................................................................................39

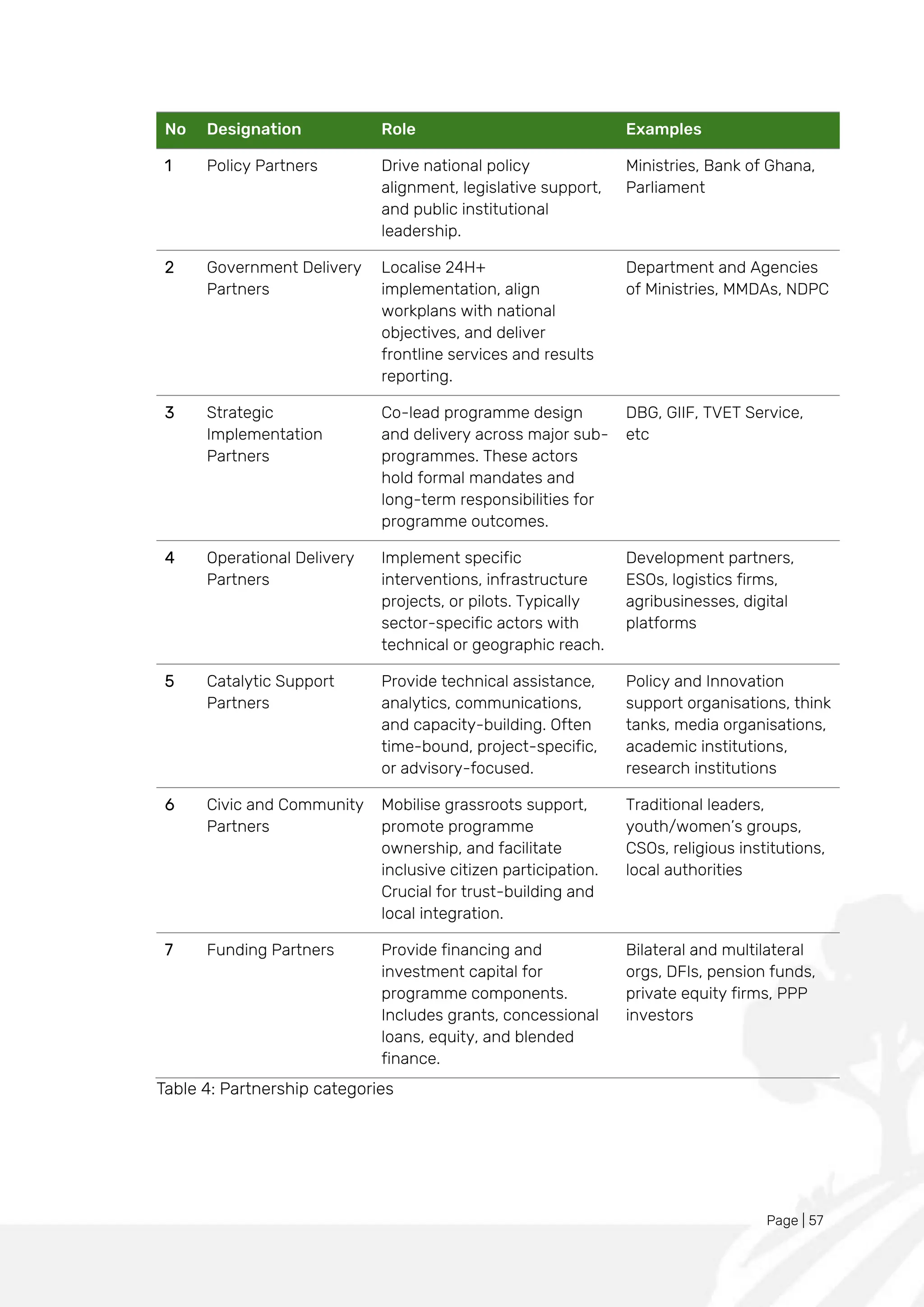

Table 4: Partnership categories...................................................................................................................................57

Table 5: Key Statistics on Systemic Challenges in Ghana’s Agriculture Sector...............................................78

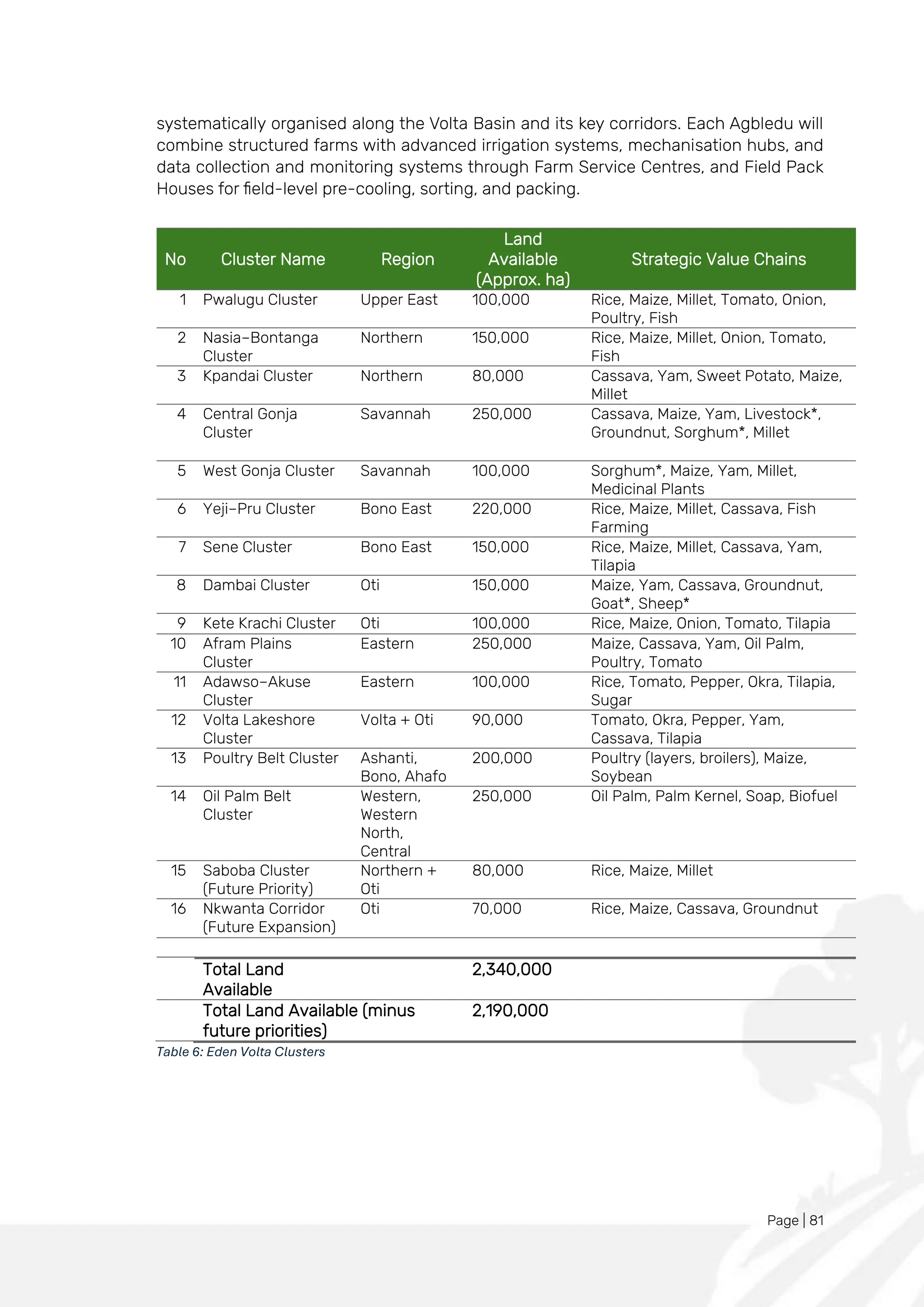

Table 6: Eden Volta Clusters.........................................................................................................................................81

Table 7: 24H+ Selected Value Chains & their Potential Economic Impact....................................................... 84

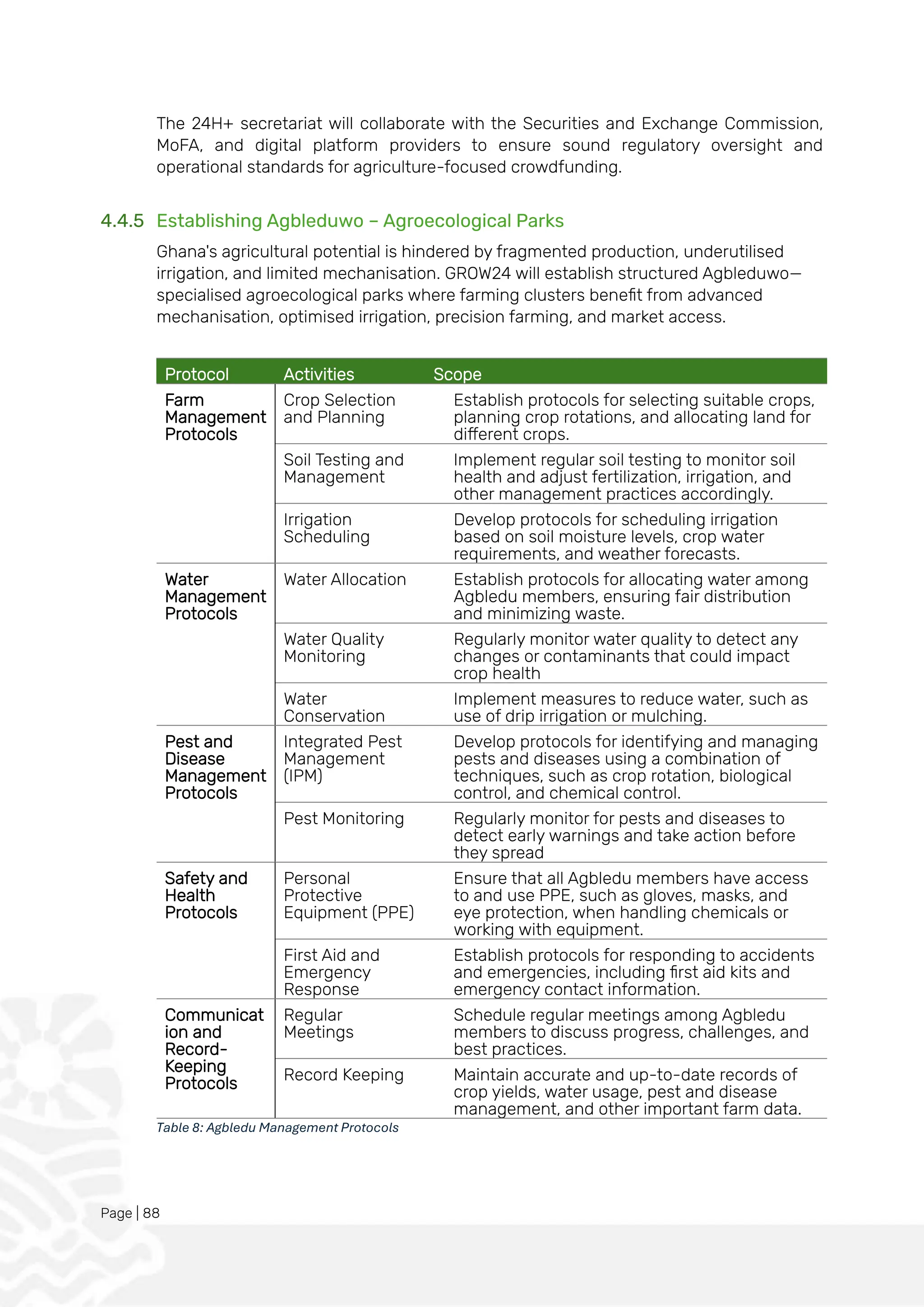

Table 8: Agbledu Management Protocols................................................................................................................ 88

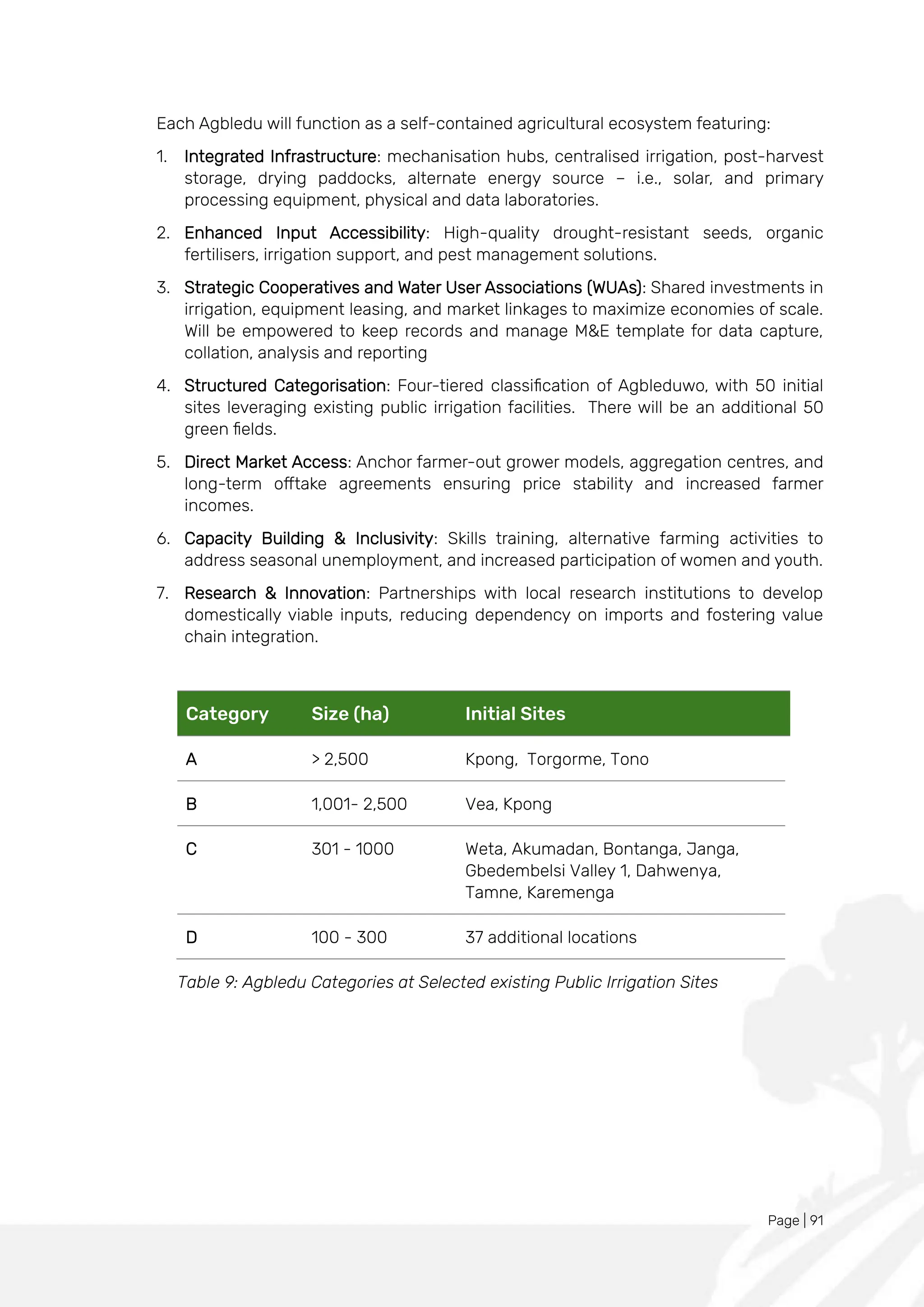

Table 9: Agbledu Categories at Selected existing Public Irrigation Sites.......................................................... 91

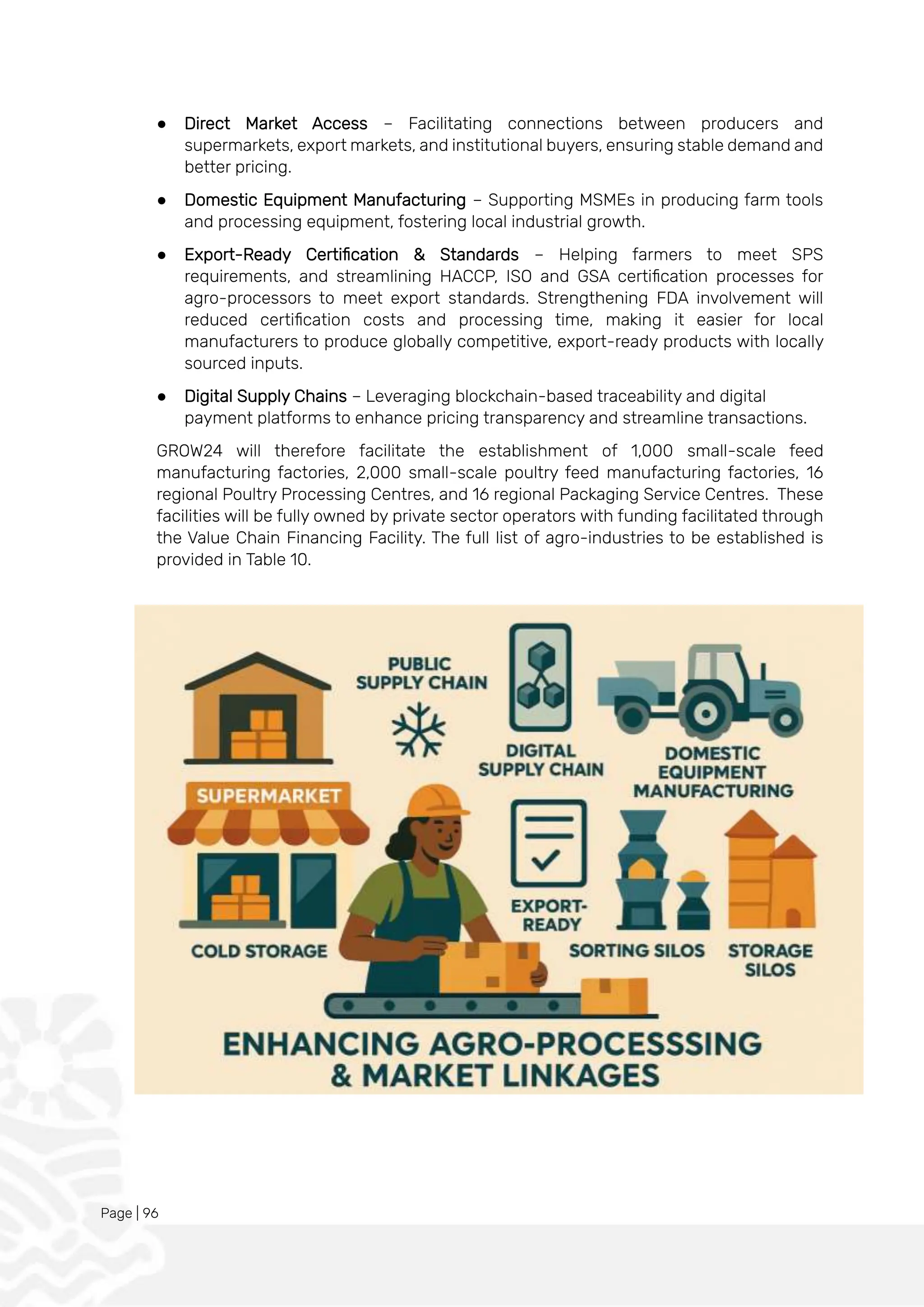

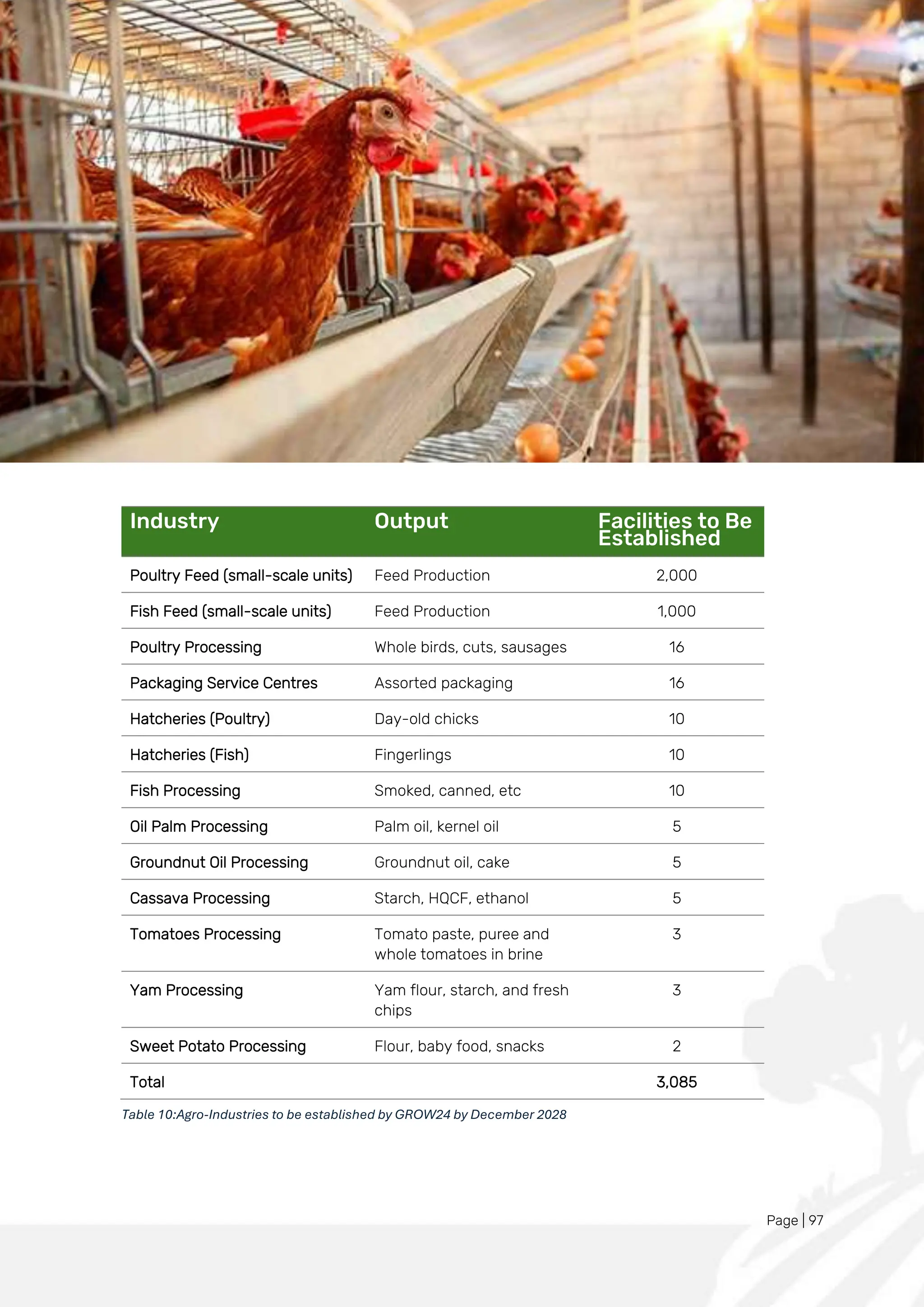

Table 10:Agro-Industries to be established by GROW24 by December 2028 ..................................................97

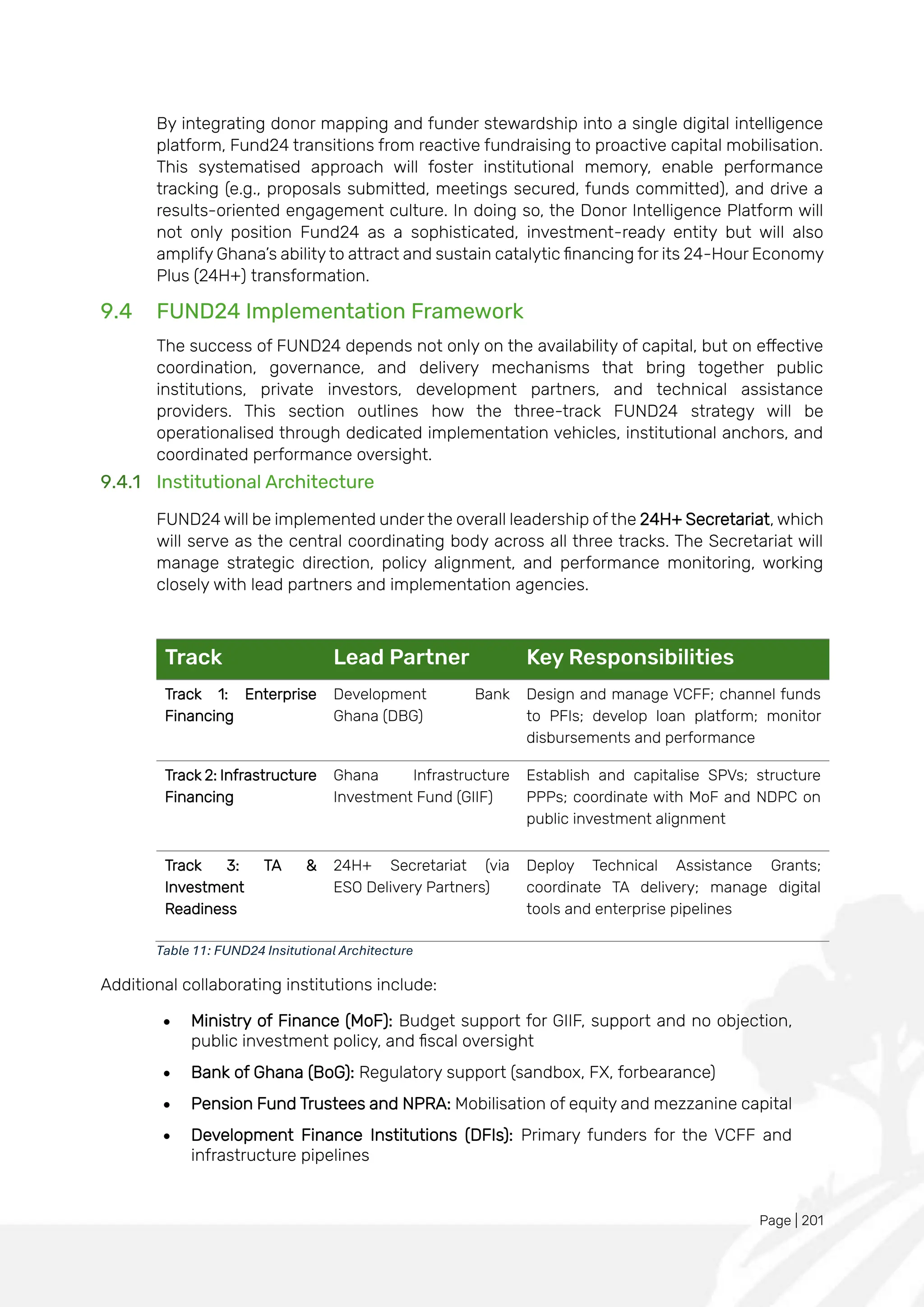

Table 11: FUND24 Insitutional Architecture ............................................................................................................201

Table 12: Geographical Zones of Focus for Oil Palm.............................................................................................267

9.

Page | 8

LISTOF ACRONYMS AND ABBREVIATIONS

Term/ Acronym/

Abbreviation

Full Meaning / Definition

24H+ 24-Hour Economy and Accelerated Export Development

AfCFTA African Continental Free Trade Area

AfDB Africa Development Bank

AGAM Association of Ghana Apparel Manufacturers

Agbledu (Agbleduwo–

plural) (Ewe)

Agroecological Park

FSC Farmer Services Centre

AGI Association of Ghana Industries

AGRA Alliance for Green Revolution in Africa

AI Artificial Intelligence

AR/VR Augmented Reality/Virtual Reality

ASPIRE24 Human Capital Development Sub-Programme of 24H+

ATL Akosombo Textiles Limited

AU African Union

BADEA Arab Bank for Economic Development in Africa

BoG Bank of Ghana

BUILD24 Construction Sub-programme of 24H+

CAT Culture, Arts, and Tourism

CIR Community Improvement and Revitalisation

CLT Community Land Trust

COCOBOD The Ghana Cocoa Board

CONNECT24 The supply chain and market efficiency programme of 24H+

CSIR Council for Scientific and Industrial Research

CTVET Commission for Technical and Vocational Educational and

Training

DBG Development Bank Ghana

DCEs Digital Centres of Excellence

DFIs Development Finance Institutions

DOC Department of Cooperatives

DRM Digital Rights Management

ECG Electricity Company of Ghana

ECOWAS Economic Community of West African States

Eden Volta Transformation of Volta Basin into Breadbasket of Africa

ESO Enterprise Support Organisation

EU European Union

FAO Food and Agriculture Organization of the United Nations

FBO Farmer-Based Organization

FDA Food and Drug Authority

10.

Page | 9

Term/Acronym/

Abbreviation

Full Meaning / Definition

FSC Farmer Services Centre

FUND24 The capital mobilisation arm of 24H+

GCX Ghana Commodity Exchange

GDP Gross Domestic Product

GEA Ghana Enterprise Agency

GIADEC Ghana Integrated Aluminium Development Corporation

GIDA Ghana Irrigation Development Authority

GIIF Ghana Infrastructure Investment Fund

GINI Gini Coefficient (Income Inequality Measure)

GIPC Ghana Investment Promotion Centre

GIRSAL Ghana Incentive-Based Risk-Sharing System for Agricultural

Lending

GNATD Ghana National Association of Tailors and Dressmakers

GO24 The civic and institutional mobilisation component of 24H+

GPHA Ghana Ports & Harbours Authority

GRA Ghana Revenue Authority

GRATIS Ghana Regional Appropriate Technology Industrial Service

GROW24 Agriculture Sub-Programme of 24H+

GSA Ghana Standards Authority

GSS Ghana Statistical Service

GUTA Ghana Union of Traders’ Associations

HACCP Hazard Analysis and Critical Control Point

ICT Information and Communication Technology

ICUMS Integrated Customs Management System

IFAD International Fund for Agricultural Development

IFC International Finance Corporation

IMF International Monetary Fund

IP Intellectual Property

IPM Integrated Pest Management

ISO International Organization for Standardization

IT Information Technology

IWT Inland Waterway Transport

KNUST Kwame Nkrumah University of Science and Technology

MAKE24 The manufacturing and industrialisation sub-programme

MDAs Ministries, Departments and Agencies

MiDA Millennium Development Authority

MMDAs Metropolitan, Municipal and District Assemblies

MoFA Ministry of Food and Agriculture

11.

Page | 10

Term/Acronym/

Abbreviation

Full Meaning / Definition

MSMEs Micro, Small and Medium Enterprises

NCCC National Cultural Convention Centre

NDPC National Development Planning Commission

NEIP National Entrepreneurship and Innovation Programme

NWPM National Water Policy Mechanism

PA24H+ Presidential Advisor, 24-Hour Economy and Accelerated Export

Development

PPP Public-Private Partnership

RTA Rehabilitation Through Agriculture

SAVs Strategic Agricultural Value Chains

SDG Sustainable Development Goal

SEZ Special Economic Zones

Shikpon (Ga) Urban and peri-urban vegetable farming zones

SHOW24 Culture, Arts, and Tourism Sub-Programme of 24H+

SMEs Small and Medium Enterprises

SMVs Strategic Manufacturing Value Chains

SPS Sanitary and Phytosanitary

SPV Special Purpose Vehicle

STP Strategic Transformation Pillar

TVET Technical and Vocational Education and Training

UNCTAD United Nations Conference on Trade and Development

UNDP United Nations Development Programme

VAT Value Added Tax

VCFF Value Chain Financing Facility

VLTC Volta Lake Transport Company

VRA Volta River Authority

WAEMU West African Economic and Monetary Union

WHO World Health Organisation

WTO World Trade Organisation

Wumbei (Gonja) The name given to Industrial Parks in the 24H+ programme

Page | 12

1.0Our Vision

driven Ghanaian economy with optimally integrated value chains, a globally

competitive workforce, and strong regional and global trade integration, delivering

sustainable, inclusive growth, decent jobs, and increased resilience to external

shocks.

Page | 14

2.0The Challenge

2.1 Colonial Economic Structure

Ghana's fundamental economic structure is deformed. It is still structured like a

colonial economy – meaning it is just a cog in a larger global economy where it is

organised around the interests of others, not its citizens. The economy is largely

structured to function as a peripheral supplier in the global economic system, geared

towards the extraction of raw materials for external markets.

We continue to export primary commodities such as cocoa beans, gold dorê, crude

oil - at prices set by international buyers – capturing only a small fraction of the value

generated along global value chains we participate in. At the same time, we import

almost all our finished goods and a significant proportion of our production inputs –

usually at premium prices also determined by the international producers and

traders.

The result is a persistent value drain: we export wealth in raw form and re-import it

as expensive goods and services, reinforcing dependency, trade deficits, and

underdevelopment.

We illustrate further below.

2.2 Import Dependency

Ghanaian manufacturers depend heavily on imported raw materials and machinery.

They sell 90% of their products in Ghana (only 25% of our manufacturers export

products). This structure means that every production cycle involves a net loss of

foreign exchange1

. It means that even if industries grow, the drain on our foreign

exchange reserves grows. Critical agricultural subsectors (e.g., poultry) share this

structural weakness.

To illustrate, when a local manufacturing firm secures a $5 million investment to

expand production, a significant portion is often spent on importing machinery, raw

materials, and even skilled labour. It does not circulate locally and multiply. It does

not create jobs. It increases our need for foreign currency, forcing the Cedi to

depreciate and making imported goods more expensive, fuelling inflation, and

undermining economic stability. Producers find themselves compelled to maintain

large inventories that tie up working capital that could otherwise be invested in

expansion or innovation.

Ghana also imports huge quantities of food - US$ 2 billion worth in 2024 alone2

. The

top ten food imports last year included rice, guts, bladders and stomachs of animals,

frozen cut and offal of fowl, sugar, and cereals, accounting for half of our food import

bill. These are products that we can produce competitively if we invest scientifically

and holistically in local value chains and especially post-harvest logistics.

The issue is not just foreign exchange prices, important as this is. Dependency on

imported food and industrial inputs exposes the country to undue external supply

1

See Graphic Online, “Overreliance on Imported Raw Materials Crippling Production – AGI,” Graphic Online, January 23, 2024. Available

at: https://www.graphic.com.gh/news/general-news/ghana-news-overreliance-on-imported-raw-materials-crippling-production-

agi.html; Ghanaian Times, “Ghana Records GH¢4.5bn Trade Deficits in 2022 – GSS Report,” Ghanaian Times, March 15, 2023. Available

at: https://ghanaiantimes.com.gh/ghana-records-gh%C2%A2-4-5bn-trade-deficits-in-2022-gss-report

2

Ghana Statistical Service, “Over Half of Ghana’s Food Supply in 2024 Came from Imports,” The High Street Journal, March 1, 2025.

Available at: https://thehighstreetjournal.com/over-half-of-ghanas-food-supply-in-2024-came-from-imports/

16.

Page | 15

shockssuch as global price volatility, global exchange rate fluctuations, and supply

chain disruptions. It means we import foreign inflation.

No amount of macroeconomic dexterity will solve this structural crisis. No amount

of hard work by producers or by State agencies will deliver the development our

people so badly need. Macroeconomic fixes like IMF stabilisation programmes that

are not accompanied by structural reform in the production system can only be

temporary and often appear to worsen the situation. We must address the structural

problems.

2.3 Structural Misalignments Within the Domestic Economy

This structural challenge is exacerbated by perverse domestic arrangements that

often reflect ad hoc, uncoordinated and piecemeal efforts to deal with the

symptoms of our structural problems over the years, and the failure of the State to

guide private players to do more. We cannot effectively promote industrialisation

without an alignment between foundational systems—energy, logistics, and

financing on the one hand, and the dynamics of the production process on the other.

These misalignments ensure that Ghana’s productive capacity remains chronically

underutilised. In 2024, Myjoyonline reported a decline in capacity utilisation in the

cement industry, from 48% in 2022 to just 38% in 20233

.

This misalignment is especially evident in Ghana’s energy system. Electricity

outages account for an average of 9.3% in lost annual sales for Ghanaian firms,

according to the World Bank Enterprise Surveys. To mitigate this, companies self-

generate approximately 16.9% of their electricity needs. Energy expenditure

accounts for between 6.6% and 8.7% of total sales4

. This makes locally produced

goods expensive and uncompetitive, especially in energy-intensive sectors like

manufacturing. In contrast, firms in Vietnam and Kenya, for example, benefit from

more stable energy supply and more affordable industrial tariffs, strengthening their

export competitiveness.

The financial system also reflects this structural disconnect. Ghana’s banking sector

has not developed to provide the kind of patient, long-term capital that industrial

development requires. Our banking sector constrains industrial growth through the

high cost and short tenor of credit. According to the Bank of Ghana and the IMF

Financial Sector Assessment reports, the average lending rate in Ghana exceeds

25% p.a, with loan tenors rarely exceeding 24 months. Moreover, collateral

requirements remain prohibitively high, often exceeding 200% of the loan value,

effectively locking out a large proportion of small and medium-sized enterprises. In

comparison, Vietnam and Kenya provide development bank support and offer

industrial credit at average rates of 8–12%, with more flexible repayment periods and

sector-specific facilities for agriculture and manufacturing.

Ghana’s export competitiveness is limited not only by high production costs but also

by weak supply chain integration and low value-addition. While manufacturing

exports account for over 40% and 85% of total exports in places like Kenya and

3

Ibrahim, A. (2024, July 18). Cement manufacturers’ capacity utilisation falls from 48% to 38% in one year, says Ishmael

Yamson. MyJoyOnline. Retrieved from https://www.myjoyonline.com/cement-manufacturers-capacity-utilisation-falls-from-48-to-38-

in-one-year-says-ishmael-yamson/

4

MiDA 2024 Constraints Analysis

17.

Page | 16

Vietnam5

,respectively, Ghana’s figure lags below 15%, and as highlighted by

UNCTAD, Ghana’s export base remains narrow, overly reliant on primary

commodities, and underperforming in value-added goods. This disparity is even

more pronounced in specific sectors. For instance, in textiles and apparel, Vietnam

has leveraged integration into global value chains to export over $40 billion

annually6

, while Ghana's entire manufacturing export base across all sectors is under

$2 billion. Similarly, Kenya exports processed agricultural products to over 90

countries, while Ghana's processed agricultural exports reach fewer than 30

markets. Even in areas where Ghana possesses natural resource advantages, such

as cocoa processing, the country exports primarily raw or semi-processed cocoa,

while competitors increasingly capture value through finished chocolate products

and specialised derivatives.

The problem is not that Ghana imports - it’s that our society is structurally

conditioned to import as a first resort - and not just commodities but ideas and

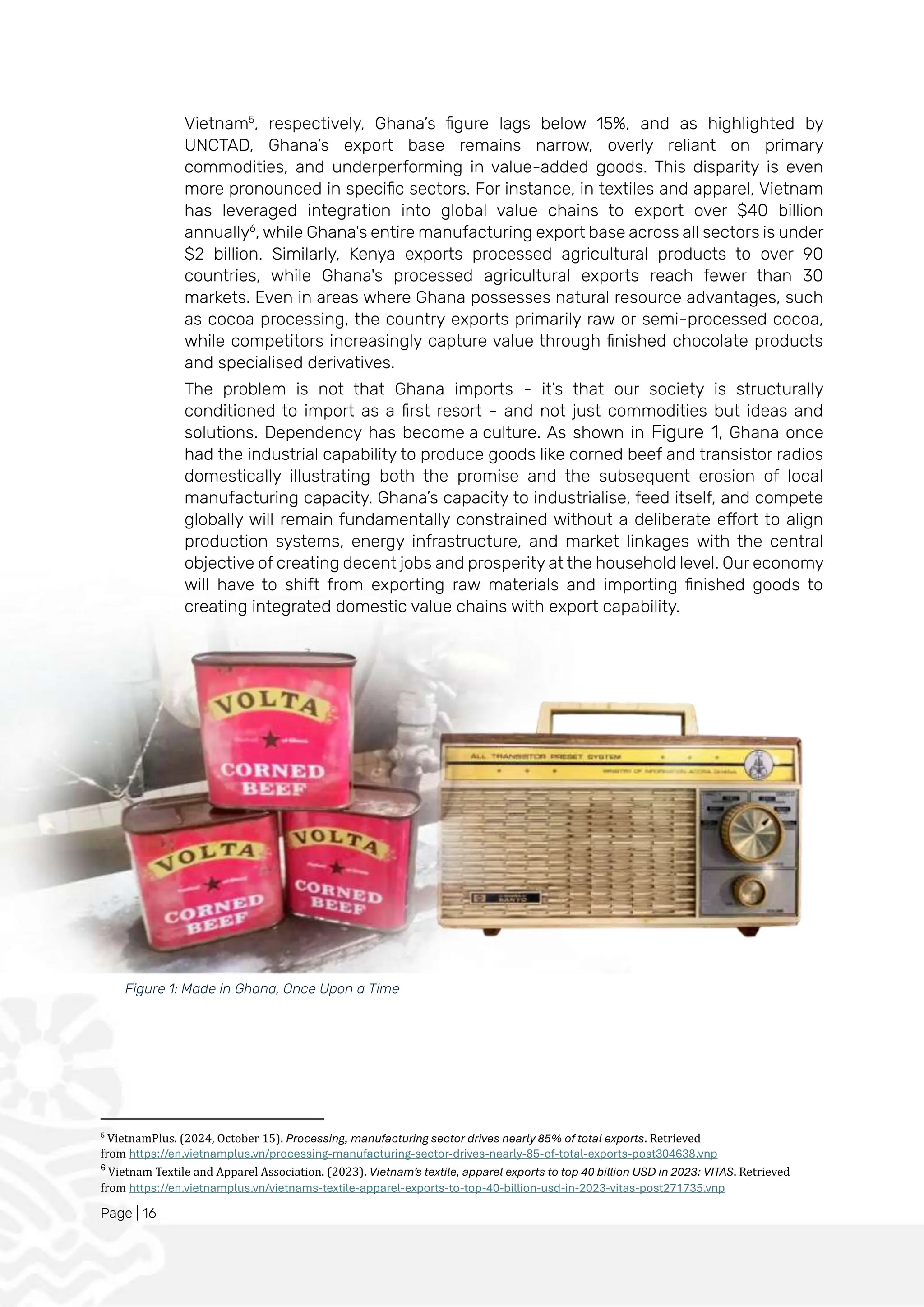

solutions. Dependency has become a culture. As shown in Figure 1, Ghana once

had the industrial capability to produce goods like corned beef and transistor radios

domestically illustrating both the promise and the subsequent erosion of local

manufacturing capacity. Ghana’s capacity to industrialise, feed itself, and compete

globally will remain fundamentally constrained without a deliberate effort to align

production systems, energy infrastructure, and market linkages with the central

objective of creating decent jobs and prosperity at the household level. Our economy

will have to shift from exporting raw materials and importing finished goods to

creating integrated domestic value chains with export capability.

5

VietnamPlus. (2024, October 15). Processing, manufacturing sector drives nearly 85% of total exports. Retrieved

from https://en.vietnamplus.vn/processing-manufacturing-sector-drives-nearly-85-of-total-exports-post304638.vnp

6

Vietnam Textile and Apparel Association. (2023). Vietnam’s textile, apparel exports to top 40 billion USD in 2023: VITAS. Retrieved

from https://en.vietnamplus.vn/vietnams-textile-apparel-exports-to-top-40-billion-usd-in-2023-vitas-post271735.vnp

Figure 1: Made in Ghana, Once Upon a Time

18.

Page | 17

3.024H+ Programme: An Integrated Solution

The structural problems of Ghana’s economy cannot be successfully addressed

piecemeal. We need a holistic programme of systemic transformation that

simultaneously delivers:

a. reduced dependence on imported food and production inputs;

b. lower post-harvest losses due to improved logistics, especially in transporting

produce between northern and southern Ghana;

c. expanded domestic manufacturing;

d. affordable patient capital that unlocks MSME growth;

e. a highly skilled, Pan-Africanist, ethically grounded, digitally fluent workforce;

f. a vibrant cultural, artistic, and tourist industry that creates decent

employment and builds a positive African identity; and

g. citizen engagement, accountability, both at the private and state level, and

whole-of-government alignment.

This is the orientation of 24H+.

Achieving these outcomes requires more than isolated interventions in individual

sectors. Ghana’s past experience has shown that progress in one area, such as

agriculture or manufacturing, often fails to translate into broader economic gains.

Improvements are frequently undercut by bottlenecks in logistics, finance, or skills,

and more importantly, by the absence of deliberate linkages that allow success in

one part of the economy to trigger growth in others.

To overcome this, 24H+ deliberately breaks with the traditional sectoral approaches

that address challenges in isolation. It adopts an integrated value chain approach.

This means interventions are not designed or delivered in silos. Agriculture,

manufacturing, culture, logistics, finance, skills development, and market access are

treated as interconnected components of a single economic system. This ensures

that progress in one area reinforces and multiplies gains across others, rather than

being constrained by gaps elsewhere.

19.

Page | 18

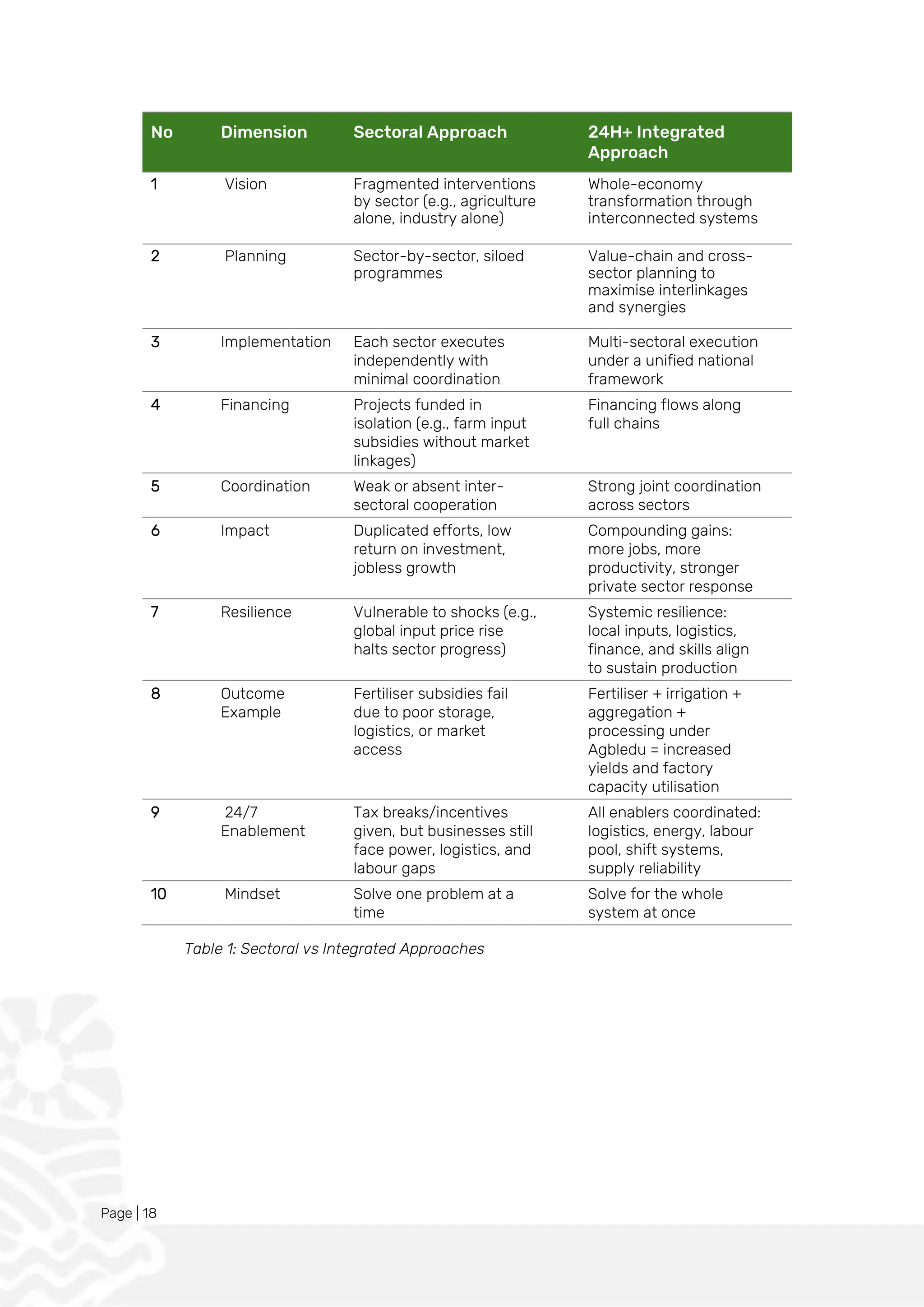

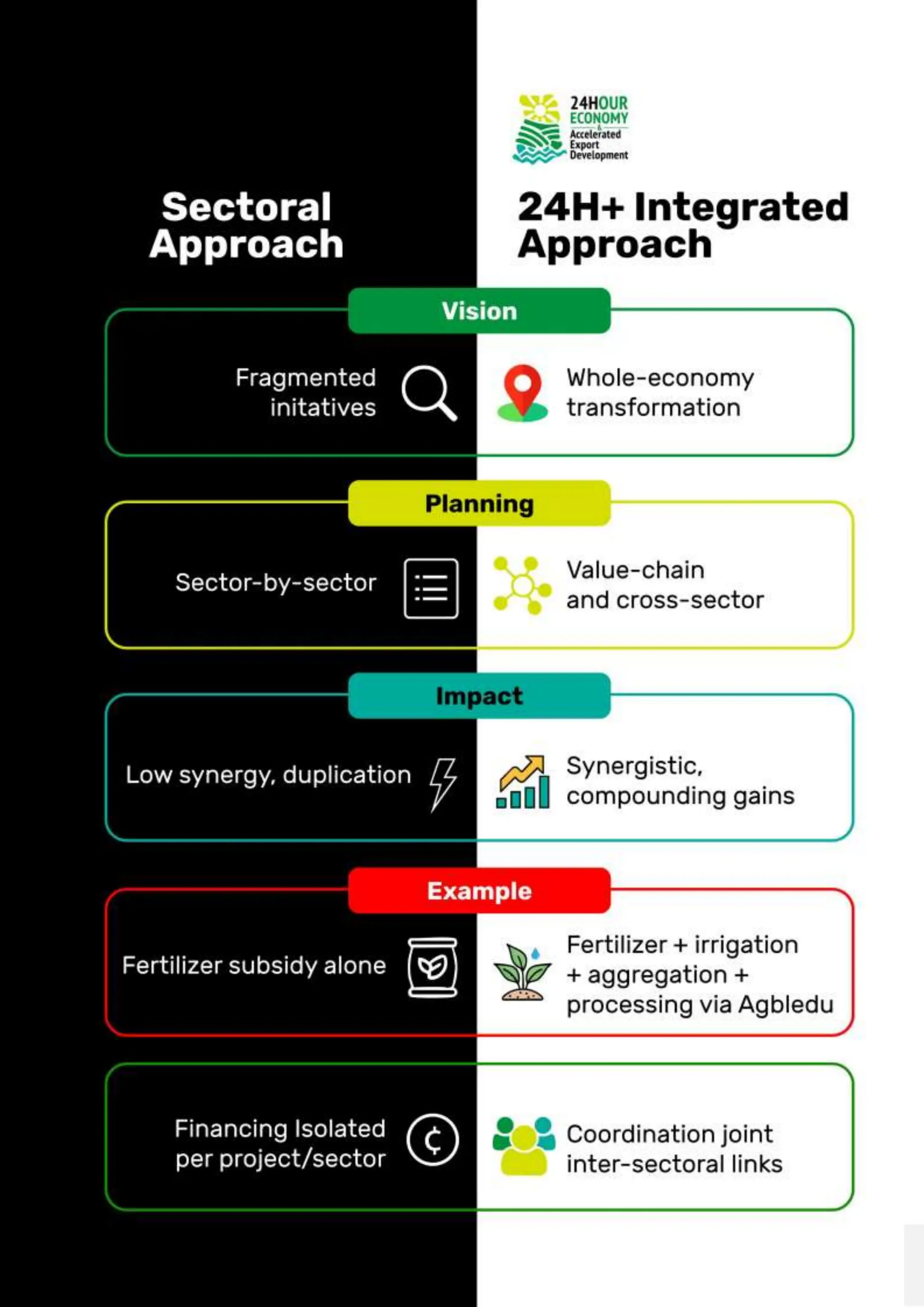

NoDimension Sectoral Approach 24H+ Integrated

Approach

1 Vision Fragmented interventions

by sector (e.g., agriculture

alone, industry alone)

Whole-economy

transformation through

interconnected systems

2 Planning Sector-by-sector, siloed

programmes

Value-chain and cross-

sector planning to

maximise interlinkages

and synergies

3 Implementation Each sector executes

independently with

minimal coordination

Multi-sectoral execution

under a unified national

framework

4 Financing Projects funded in

isolation (e.g., farm input

subsidies without market

linkages)

Financing flows along

full chains

5 Coordination Weak or absent inter-

sectoral cooperation

Strong joint coordination

across sectors

6 Impact Duplicated efforts, low

return on investment,

jobless growth

Compounding gains:

more jobs, more

productivity, stronger

private sector response

7 Resilience Vulnerable to shocks (e.g.,

global input price rise

halts sector progress)

Systemic resilience:

local inputs, logistics,

finance, and skills align

to sustain production

8 Outcome

Example

Fertiliser subsidies fail

due to poor storage,

logistics, or market

access

Fertiliser + irrigation +

aggregation +

processing under

Agbledu = increased

yields and factory

capacity utilisation

9 24/7

Enablement

Tax breaks/incentives

given, but businesses still

face power, logistics, and

labour gaps

All enablers coordinated:

logistics, energy, labour

pool, shift systems,

supply reliability

10 Mindset Solve one problem at a

time

Solve for the whole

system at once

Table 1: Sectoral vs Integrated Approaches

20.

Page | 19

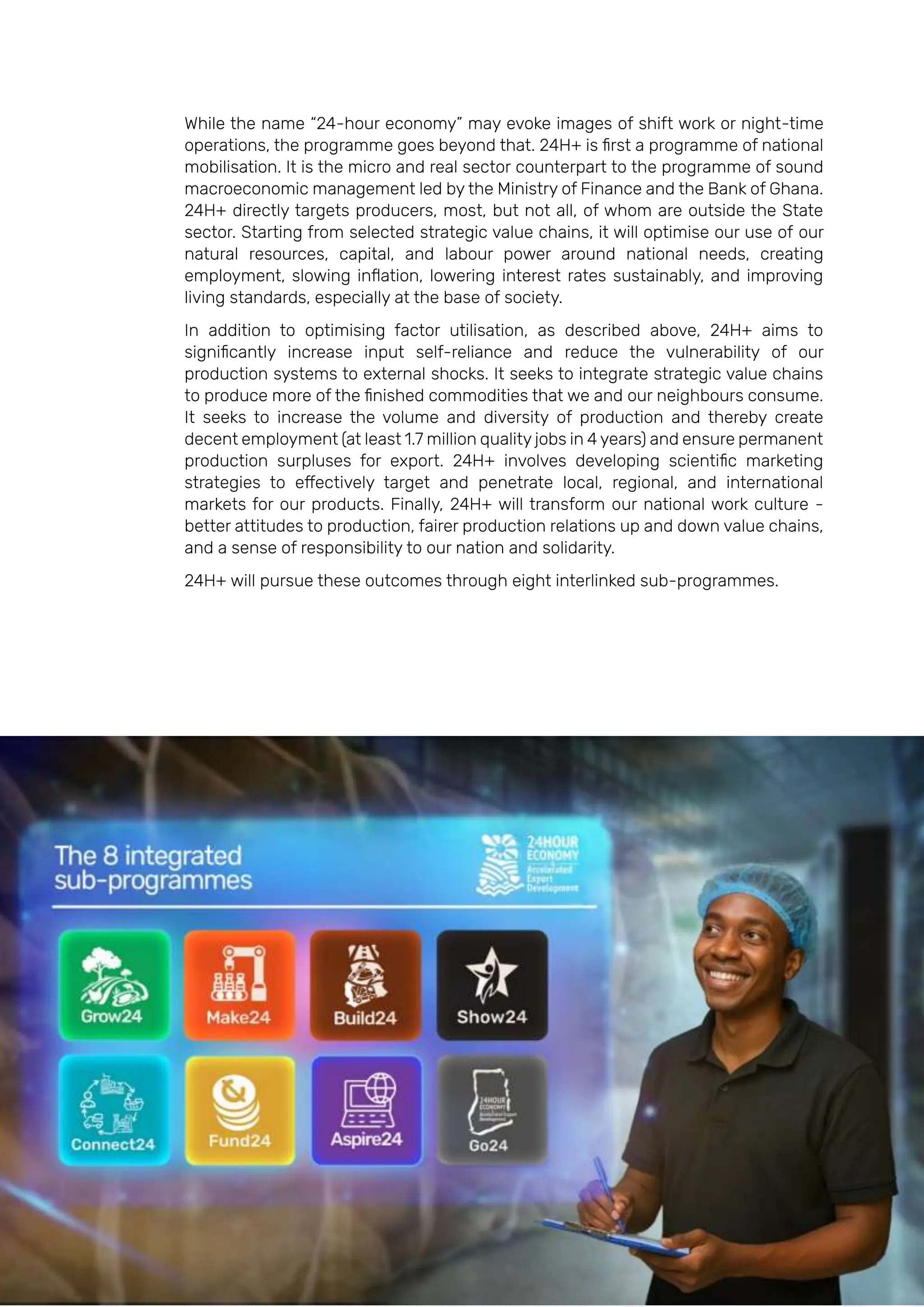

Whilethe name “24-hour economy” may evoke images of shift work or night-time

operations, the programme goes beyond that. 24H+ is first a programme of national

mobilisation. It is the micro and real sector counterpart to the programme of sound

macroeconomic management led by the Ministry of Finance and the Bank of Ghana.

24H+ directly targets producers, most, but not all, of whom are outside the State

sector. Starting from selected strategic value chains, it will optimise our use of our

natural resources, capital, and labour power around national needs, creating

employment, slowing inflation, lowering interest rates sustainably, and improving

living standards, especially at the base of society.

In addition to optimising factor utilisation, as described above, 24H+ aims to

significantly increase input self-reliance and reduce the vulnerability of our

production systems to external shocks. It seeks to integrate strategic value chains

to produce more of the finished commodities that we and our neighbours consume.

It seeks to increase the volume and diversity of production and thereby create

decent employment (at least 1.7 million quality jobs in 4 years) and ensure permanent

production surpluses for export. 24H+ involves developing scientific marketing

strategies to effectively target and penetrate local, regional, and international

markets for our products. Finally, 24H+ will transform our national work culture -

better attitudes to production, fairer production relations up and down value chains,

and a sense of responsibility to our nation and solidarity.

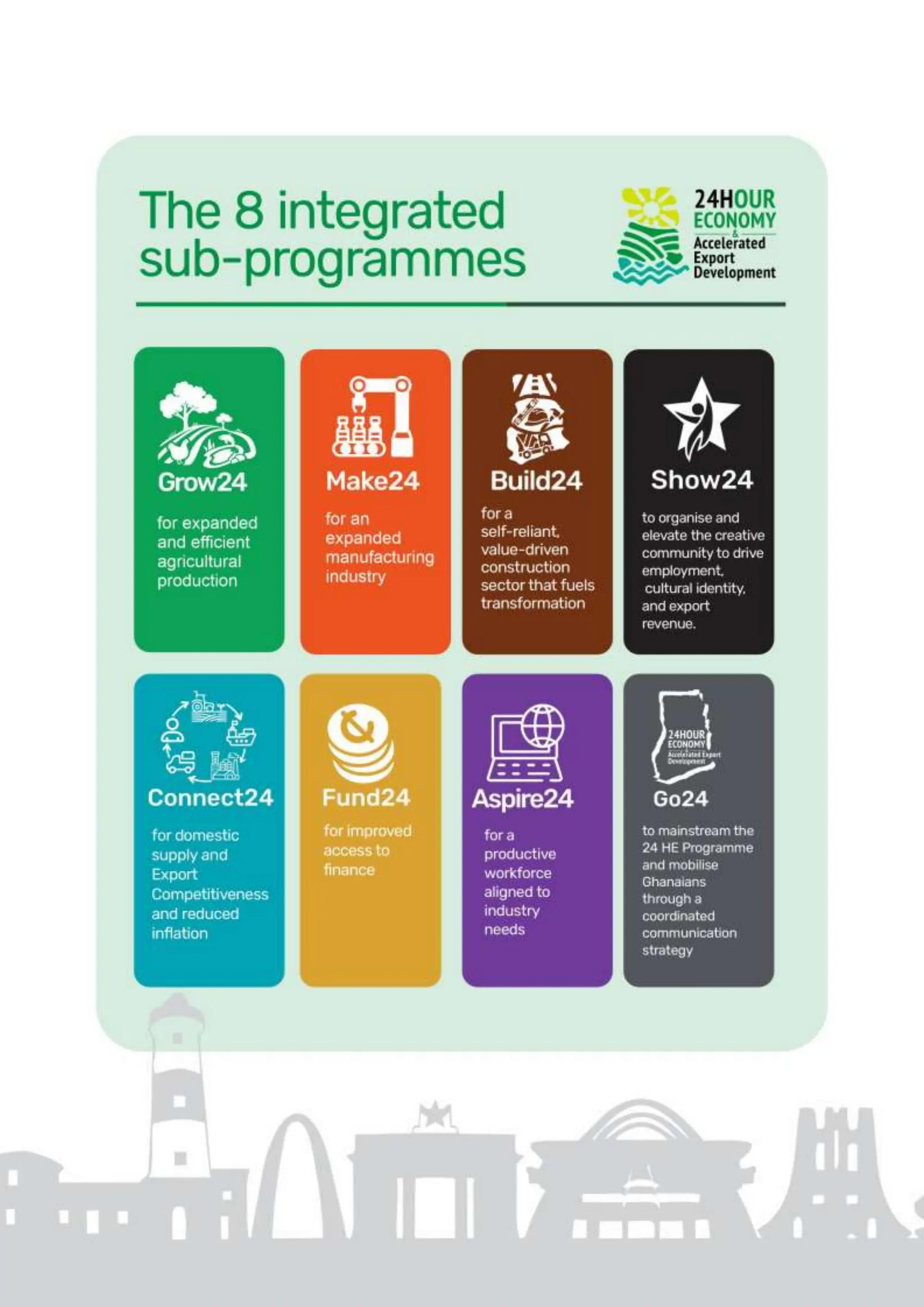

24H+ will pursue these outcomes through eight interlinked sub-programmes.

Page | 21

3.1Agriculture

In the agricultural sector, the GROW24 Sub-Programme will revitalise critical

strategic agricultural value chains (SAVs) that are important for food and feed self-

sufficiency and security, manufacturing input self-reliance, sustainable job creation,

and climate resilience.

This will be driven through two flagship transformation engines:

1. Eden Volta Breadbasket Project – an initiative to transform the Volta Basin into

the Breadbasket of West Africa by cultivating over 2 million hectares of arable

land under structured irrigation and climate-smart systems. This will be achieved

through the development of integrated agroecological parks ("Agbleduwo")

along the Volta Lake and its tributaries, each equipped with mechanisation hubs,

renewable energy, logistics, and primary processing facilities to drive scale and

resilience. Anchor farmers will serve as key drivers of this transformation,

coordinating production, aggregation, and value addition within each Agbledu.

Productivity in keyvalue chains is expected to increase by up to 130%, depending

on the commodity and farming system;

2. Shikpon Urban and Peri-Urban Farming Revolution – structured peri-urban

vegetable and fruit farming clusters around Ghana’s major cities, designed to

guarantee an affordable, year-round fresh food supply. These urban farms will

be built around 3–5 hectare plots per metro area and will deploy greenhouse

systems, micro-irrigation, and rainwater harvesting. The initiative will focus on

short-cycle, high-demand vegetables (lettuce, tomatoes, peppers, okra, onions)

and will be operated by youth-led cooperatives and agripreneurs. These clusters

will be integrated with cold chain logistics, urban aggregation points, and digital

marketplaces, enabling real-time pricing, efficient distribution, and stronger

farm-to-market linkages.

These will be designed to:

1. create agroecological parks (“Agbleduwo”) with integrated infrastructure,

mechanisation, and market access that transform fragmented smallholder

farming into productive agricultural clusters;

2. support farmers to build strong cooperatives to improve productivity, strengthen

market power, and enhance access to finance, technology, and extension

services;

3. develop Strategic Agricultural Value Chains - high-potential value chains across

seven food groups - to reduce Ghana's $2 billion food import bill;

4. cut post-harvest losses from 30%+7

to 15% through modern logistics (storage,

preservation, transportation) technologies, and processing facilities; and

5. strengthen the application of research and indigenous knowledge, including

accessible seed banks, for high-yielding climate-smart agriculture.

7

Ehrlich, D. (2025, March 17). Post-harvest food loss in Ghana’s fruit and vegetable supply chains: Evidence from the field. International

Growth Centre. Retrieved from https://www.theigc.org/publications/post-harvest-food-loss-ghanas-fruit-and-vegetable-supply-chains-

evidence-field

23.

Page | 22

Inline with the broader transformation agenda, GROW24 integrates the principles of

agroecology—not just as a set of ecological practices, but as a strategic framework

for equitable, sustainable, and locally grounded agricultural development. This

includes promoting biodiversity, supporting smallholder farmers as key economic

actors, incorporating local and traditional knowledge systems, and ensuring that

farming systems are resilient, regenerative, and socially just.

The Agbleduwo will therefore be both productive hubs and demonstration zones for

inclusive and sustainable agroecological transformation. Each park will be supported

by a Farmer Services Centre (FSC) with staff trained in agroecological values and

equipped to deliver technical support, cooperative development, value chain

literacy, and community-based services.

24.

Page | 23

Figure2: Typical Layout of an Agbledu FSC on a 4-acre land (courtesy Trotro Tractor Limited

25.

Page | 24

3.2Manufacturing

The MAKE24 Sub-Programme is Ghana’s strategy for manufacturing transformation

under the 24H+ programme. It aims to transition Ghana from an import-dependent

economy into a productive, export-oriented industrial country by leveraging

competitive advantages in five Strategic Manufacturing Value Chains (SMVs): agro-

processing, pharmaceuticals, textiles and garments, construction materials, and

machinery/technology.

MAKE24 goes beyond simply building factories. It focuses on creating inclusive and

productive industrial ecosystems that strengthen backward and forward linkages,

support formalisation and clustering, and drive long-term industrial competitiveness

under AfCFTA.

Critical to MAKE24 is the development of a national network of modern industrial

parks—the Wumbei Industrial Parks—designed to resolve the foundational constraints

holding back Ghanaian manufacturers: inaccessible land, unreliable utilities, and high

logistics and setup costs.

By 2028, 10 Wumbei Parks will be developed, with a total of 50 parks targeted within

the next decade. Each park will average 50 acres or more, and will be equipped with

shared, serviced infrastructure including:

• Reliable, renewable and/or embedded power systems;

• Piped water supply and waste treatment systems;

• Road access, internal circulation routes, and digital connectivity;

• Pre-zoned land and flexible layouts for firm expansion and clustering.

The priority for MAKE24 is unlocking land access in partnership with traditional

authorities and repurposing public lands for productive use. The Ghana Infrastructure

Investment Fund (GIIF) will establish a Special Purpose Vehicle (SPV) to acquire,

service, and manage these parks under a blended finance model supported by FUND24.

To drive spatial equity and competitiveness, most Wumbei Parks will be co-located with

agroecological production zones under GROW24 and integrated into the Volta Lake

Industrial Corridor—Ghana’s most underutilised logistics asset. This corridor will reduce

logistics costs by up to 80%, connect the north and south, and support balanced

regional industrialisation.

MAKE24 will also:

1. Unlock the five priority SMVs by coordinating infrastructure investment, workforce

development under ASPIRE24, and access to affordable, long-term capital under

FUND24.

2. Increase average capacity utilisation in Ghanaian manufacturing from 46% to 85%

by providing targeted support to firms, structured input supply chains, and

guaranteed market access.

3. Formalise informal manufacturers and support their transition into structured

production clusters, cooperatives, and trade associations to reduce transaction

costs, enforce quality standards, and support collective market access.

26.

Page | 25

Throughits tight integration with other sub-programmes—GROW24 (raw materials

supply), CONNECT24 (logistics), ASPIRE24 (skills), and FUND24 (finance)—MAKE24

will catalyse structural change in Ghana’s industrial landscape and position the

country as a leading manufacturing base under the African Continental Free Trade

Area.

Page | 27

3.3Built environment and Infrastructure

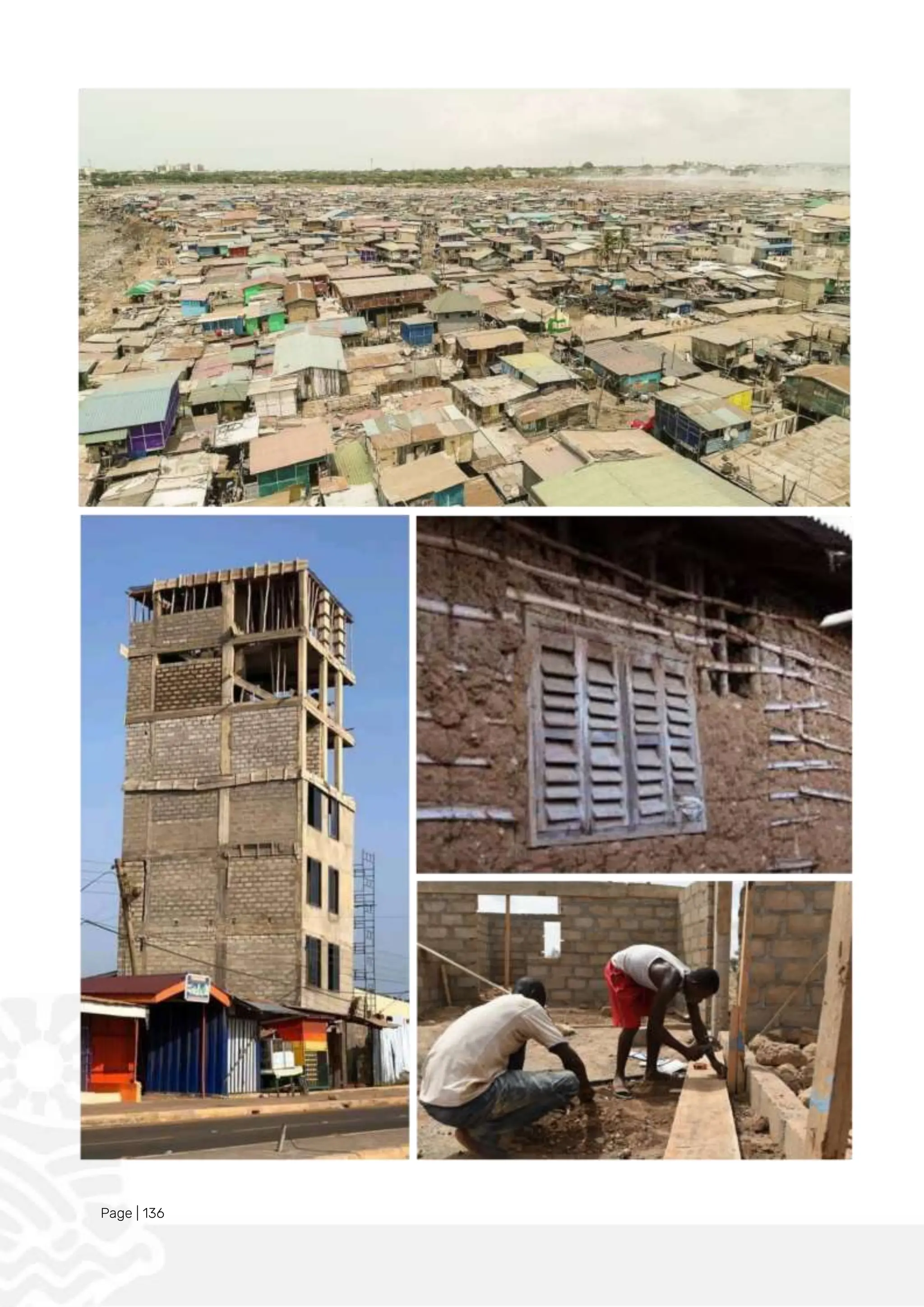

The BUILD24 Sub-Programme addresses one of the most foundational yet

underperforming sectors of Ghana’s economy: construction and the broader built

environment. The construction industry currently suffers from low productivity,

limited innovation, fragmented regulation, and a heavy reliance on imports for basic

materials and technologies. BUILD24 will transform this sector into a dynamic driver

of Ghana’s industrialisation, job creation, and economic resilience. It will do this by

pursuing a bold strategy to localise production, formalise construction services, and

modernise sector governance.

At its core, BUILD24 seeks to restructure the construction value chain to boost local

content across all major infrastructure and housing projects. It will prioritise the

development and standardisation of locally sourced construction inputs such as

bricks, tiles, cement, insulation, roofing, doors, and prefabricated components—

thereby reducing import dependency, enhancing self-reliance, and building the

foundation for a circular economy in construction. Through targeted investment and

enterprise support, BUILD24 will nurture fabrication clusters and construction input

hubs across the country, linked to the Wumbei Industrial Parks under MAKE24.

BUILD24 will also establish the Construction Industry Development Authority (CIDA)

to serve as a central coordinating body, harmonising regulations, enforcing quality

standards, driving skills certification, and overseeing a national construction

innovation strategy. This authority will work closely with public agencies such as the

Public Works Department (PWD), Architectural and Engineering Services Limited

(AESL), and industry associations to ensure effective implementation and sector-

wide transformation.

Strategic interventions under BUILD24 include:

1. Establishing a National Materials Catalogue and Standards System in

collaboration with GSA and CSIR-BRRI to support localisation and enforce

quality;

2. Rolling out a National Construction Skills Corps (linked to ASPIRE24) to upskill

artisans, technicians, and professionals in modern methods, including green

building, prefabrication, and digital site management;

3. Leveraging public procurement to stimulate demand for Made-in-Ghana

construction inputs across roads, schools, clinics, housing, and industrial parks;

4. Digitising permitting, land use planning, and construction oversight through a

National E-Build System for transparency, efficiency, and reduced costs.

BUILD24 will ensure that Ghana builds faster, better, and smarter—delivering the

infrastructure backbone needed to scale up production across agriculture,

manufacturing, logistics, and digital services. It anchors Ghana’s transformation in

strong foundations, while creating thousands of skilled jobs and a construction

sector that is inclusive, future-facing, and globally competitive.

29.

Page | 28

3.4Culture, Arts and Tourism as Engines of Identity and Income

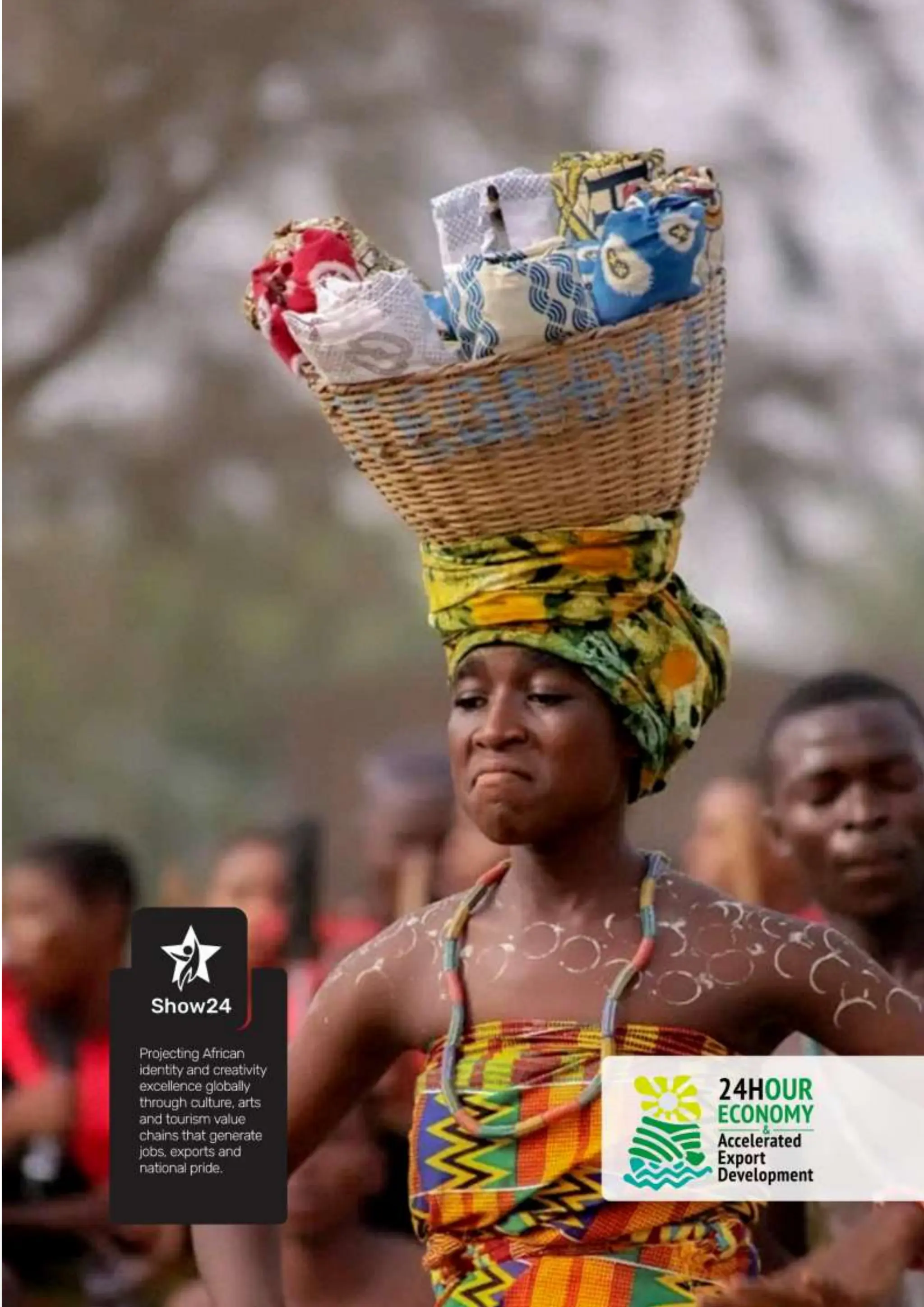

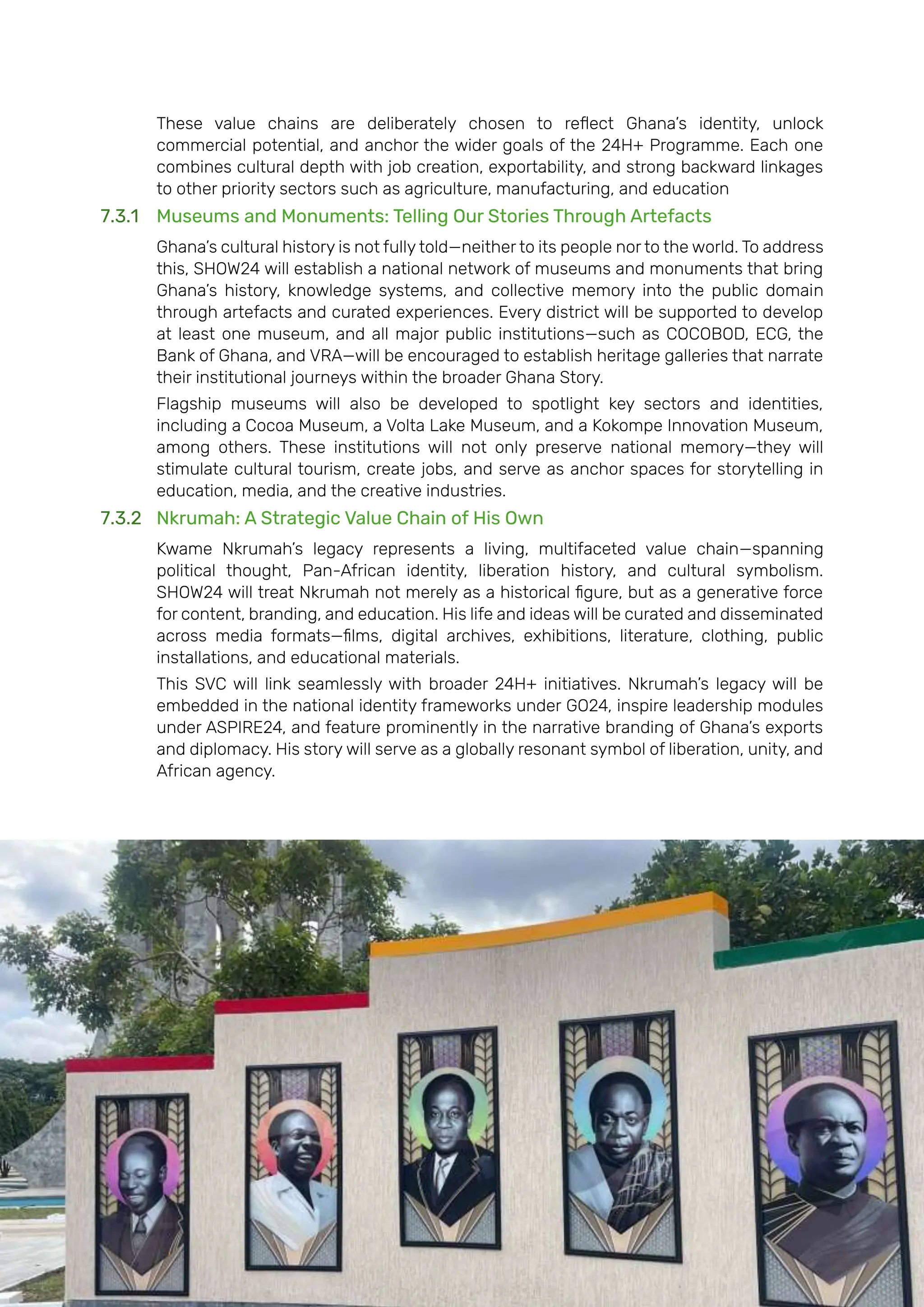

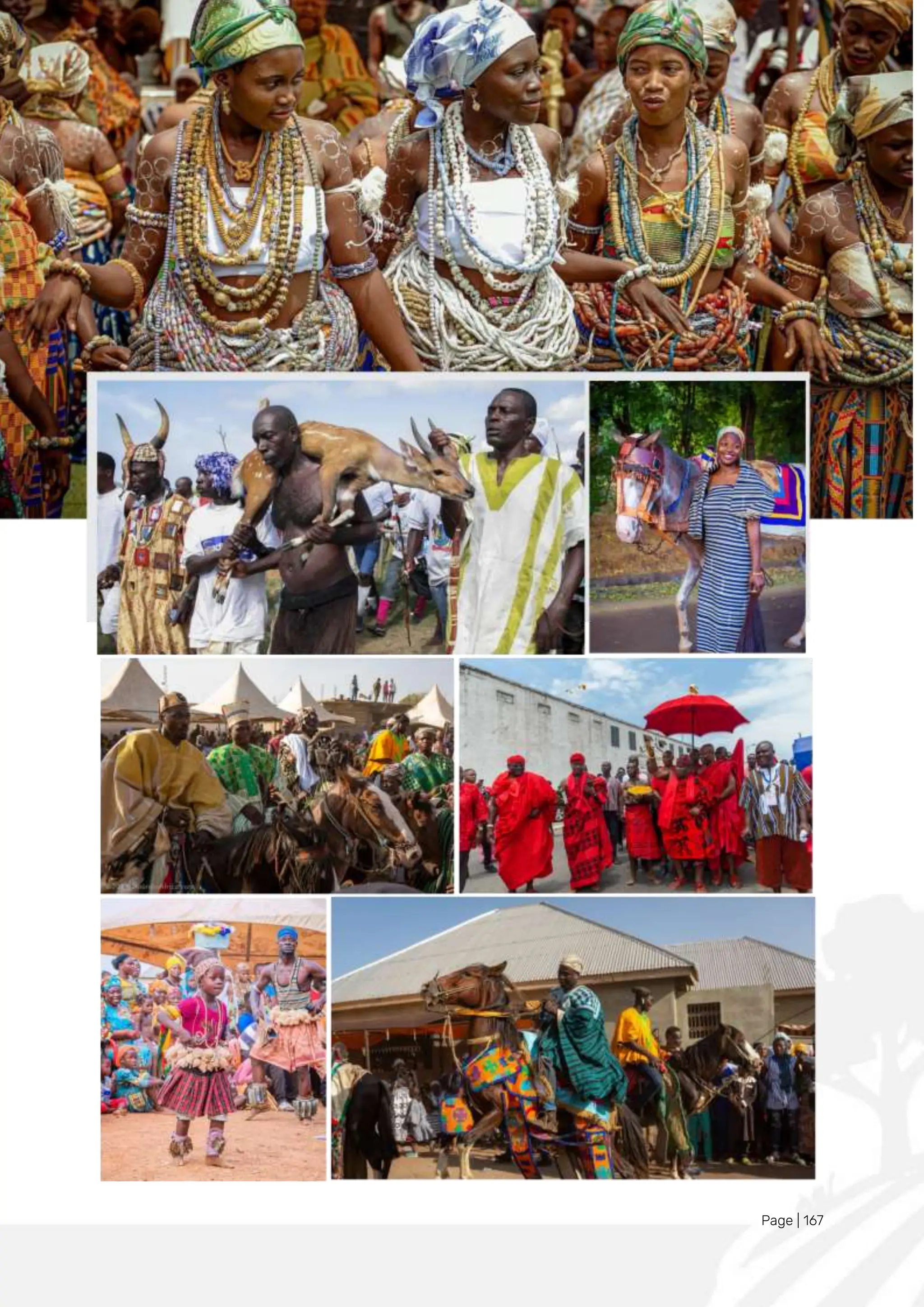

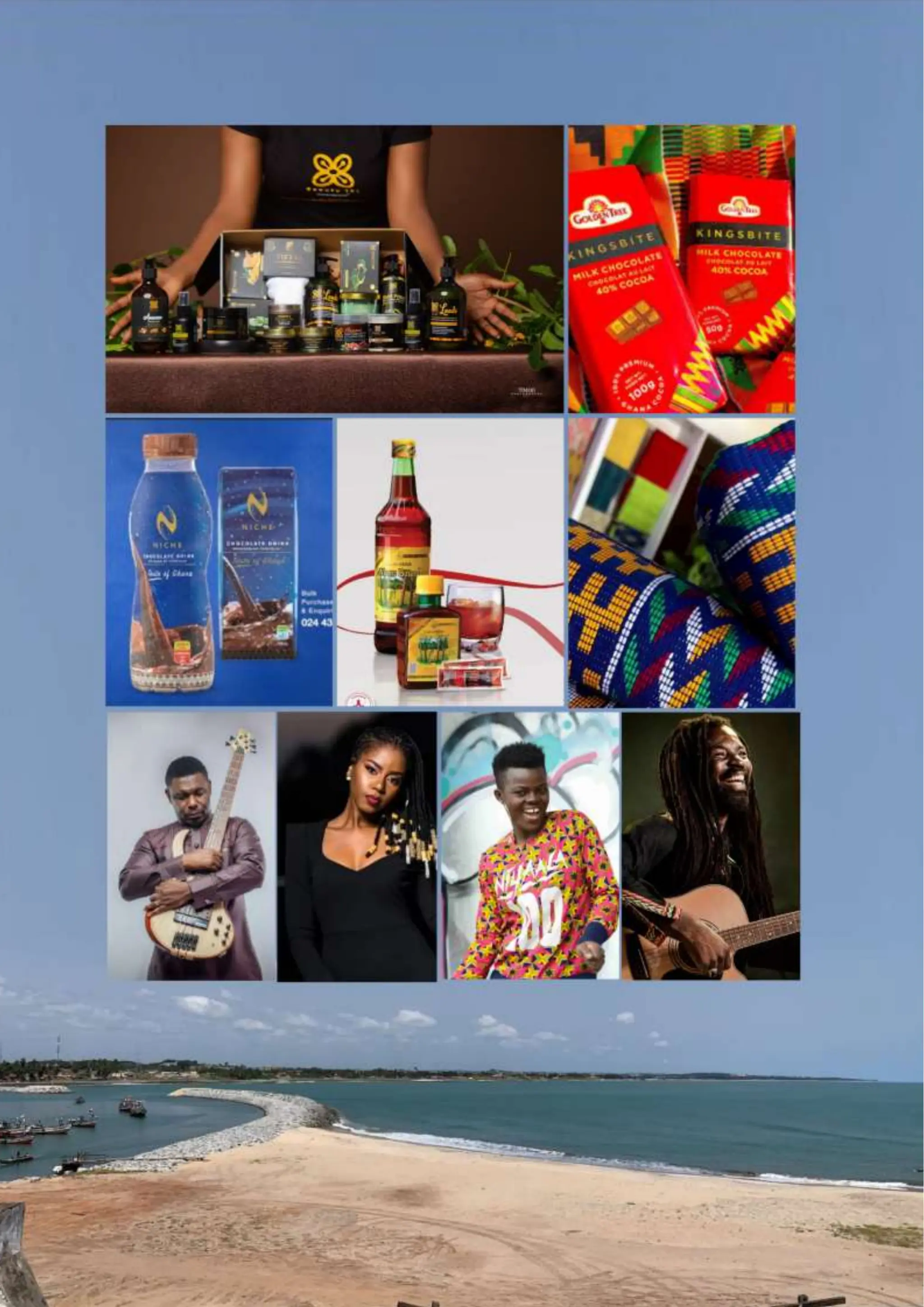

The SHOW24 Sub-Programme repositions Ghana’s culture, arts, and tourism (CAT)

sectors as dynamic engines of job creation, national pride, and export growth. It

recognises that culture is not just heritage—it is a system of production, meaning-

making, and influence. Ghana’s long history—from ancient West African civilisations

and anti-colonial struggles to Pan-African leadership and diasporic connections—

offers rich material for world-class storytelling and creative enterprise. Yet, as in

agriculture and industry, these assets have long been undervalued, fragmented, and

often appropriated by others. SHOW24 shifts the narrative and the structure,

reclaiming culture as both a strategic value chain and a unifying force for national

development.

SHOW24 identifies six catalytic Cultural, Arts, and Tourism (CAT) value chains:

museums and monuments, the legacy of Nkrumah, culinary heritage, textiles and

fashion, re-engineered festivals, and popular music and dance. These value chains

combine cultural authenticity, commercial potential, and wide employment reach,

especially for young people and women. Ghana’s hundreds of festivals, for example,

will be revitalised and rebranded as compelling cultural experiences, capable of

attracting both domestic and international tourism, supporting creative livelihoods,

and serving as platforms for storytelling, commerce, and national identity.

To unlock this potential, SHOW24 pursues a five-part strategy: (1) developing content

and talent through a National Creators Academy and community-based arts hubs;

(2) activating infrastructure—including the revitalisation of 250 community centres

into CAT hubs; (3) scaling market access and exports through licensing platforms,

diaspora networks, and festival tourism; (4) financing CAT enterprises through the

24H+ Value Chain Financing Facility; and (5) embedding cultural identity and

inclusion into the nation’s development journey through “The Ghana Story”

framework.

SHOW24 reframes creativity as a national asset and identity as infrastructure. It

brings coherence to fragmented sectors, delivers dignified jobs, and builds a globally

competitive creative economy. With every festival scaled, museum launched, fabric

exported, or story told, Ghana becomes not only a producer of goods but a producer

of meaning, pride, and value on the global stage.

3.5 Supply Chains, Logistics and Market Systems

The CONNECT24 Sub-Programme is Ghana’s strategic blueprint for fixing the broken

links between production and prosperity. It tackles one of the most persistent

barriers to national competitiveness: inefficient, high-cost supply chains and

fragmented market systems. From post-harvest losses and rural isolation to

congested ports and informal markets, these bottlenecks drain value from every

stage of production. CONNECT24 transforms this reality by building an integrated,

multimodal logistics and market ecosystem—designed to move goods faster,

cheaper, and smarter across the country and beyond.

At the heart of CONNECT24 is the full-scale activation of the Volta Lake as Ghana’s

inland freight corridor. With dedicated investment in port terminals at Buipe, Yeji,

Akosombo, and Mpakadan, and intermodal links to farms, factories, and rail, the lake

will become the spine of a low-cost, high-capacity logistics network connecting

30.

Page | 29

northernproduction zones to southern markets and ports. This will reduce logistics

costs from over 40% of product value to below 20%, unlocking national and regional

trade flows.

CONNECT24 also invests in cold chain and warehouse infrastructure, modernises

port and customs systems, expands structured aggregation and digital

marketplaces, and develops Tamale Airport into a regional air cargo hub for high-

value exports. These interventions will reduce post-harvest losses by half, enable

real-time price access for 500,000 producers, and ensure reliable input and product

flows for GROW24 and MAKE24.

CONNECT24 strengthens Ghana’s ability to compete from the farm gate to the

market to export. It ensures that goods move efficiently, reducing waste, lowering

costs, and connecting producers to structured markets and buyers across Ghana,

the region, and the world. With Volta Lake serving as a national logistics spine and

modern systems enabling reliable, 24/7 operations, Ghana will not only feed itself

and supply its industries—it will compete confidently in regional and global markets.

This is the infrastructure of a connected, productive, and export-ready economy.

3.6 Production and Infrastructure Financing

The FUND24 Sub-Programme facilitates value-chain & Infrastructure Financing to

address two key structural bottlenecks—limited access to affordable finance for

enterprises and insufficient long-term capital for productive infrastructure. The sub-

programme will unlock patient, appropriately priced capital to enable Ghanaian

producers, processors, and service providers across strategic value chains to invest,

grow, and compete.

FUND24 will

1. Unlock $1 billion+ in enterprise financing for MSMEs in strategic value chains

through a Value Chain Financing Facility, delivered by DBG through rural banks,

microfinance institutions, Savings and Loans institutions and commercial banks.

Loans will be concessional (below 12%) and tied to membership in cooperatives

or trade and industry associations to enhance credit discipline, monitoring, and

access.

2. De-risk MSME lending through a Technical Assistance Grant Fund and Credit

Insurance Scheme, supporting borrower readiness, cooperative development,

market access facilitation, credit scoring, and real-time loan tracking. This will be

implemented through Enterprise Support Organisations (ESOs) and risk-sharing

facilities in partnership with institutions like GIRSAL.

3. Support infrastructure financing through the creation of three Special Purpose

Vehicles (SPVs) under the Ghana Infrastructure Investment Fund (GIIF), focused

on Agroecological Parks, Industrial Parks, and Multimodal Logistics Systems.

These SPVs will be seeded with public capital and structured to attract blended

finance, sovereign wealth funds, and private investment through PPPs.

Infrastructure such as inland water transport along the Volta Lake corridor will be

prioritised to reduce logistics costs and enhance regional trade connectivity.

Land will be leased to investors free for the first 10 years to catalyse private

investment in farms and factories, which will be supported through the Value

Chain Financing Facility.

31.

Page | 30

FUND24will be implemented with support from the Bank of Ghana and will deploy

targeted financial solutions to reduce investment risks and costs across the 24H+

strategic value chains, enabling both large-scale infrastructure delivery and wide-

reaching MSME participation. It ensures Ghana’s transformation is not constrained

by capital access, while building a resilient, inclusive financial architecture for long-

term development

32.

Page | 31

3.7Work Culture

Ghana’s productivity challenge is not only technical but also cultural. A resilient,

inclusive, and competitive economy requires a workforce that is skilled, values-

driven, digitally fluent, and globally competitive. The ASPIRE24 Sub-Programme

responds to this imperative by reorienting Ghana’s education-to-employment

ecosystem—linking mindset, skills, and workplace readiness to the real demands of

the productive economy.

The ASPIRE24 Sub-Programme will equip Ghana’s entrepreneurs, youth, and labour

force with the values, ethics, mindset, and tools needed to meet global standards of

productivity and innovation. It will focus on four interlinked areas: transforming work

culture and attitudes to production; strengthening vocational and technical

education; mainstreaming digital intelligence and multilingual capability; and

providing targeted business support services and skills upscaling opportunities.

In the immediate term, ASPIRE24 will focus on mainstreaming digital intelligence

training across Ghana’s national TVET system. Working with industry and education

stakeholders, the programme will develop a comprehensive skills framework and

implementation roadmap and establish Digital Centres of Excellence across

upgraded TVET institutions. These centres will train students in emerging digital

skills and also function as community access points for digital tools, internet

connectivity, and workforce services.

Over time, ASPIRE24 will position Ghana as a leading African talent hub, supplying

the skills and competencies required to drive the digital and industrial transitions

envisioned under the 24H+ programme.

33.

Page | 32

3.8Sustainable Mobilisation

A 24-hour economy cannot be built by policy alone—it requires a shared national

commitment, active citizen engagement, and alignment across all arms of the state.

The GO24 Sub-Programme addresses two critical enablers of transformation: the

need for broad-based public mobilisation and the imperative to embed the 24H+

agenda into the everyday functioning of government and community life. GO24 will

tackle the challenge of low citizen engagement and limited state alignment by

mainstreaming the 24H+ transformation agenda across all levels of government and

mobilising the Ghanaian public around a shared national mission.

GO24 will:

1. Build public awareness and Mobilisation through national campaigns,

storytelling platforms, and education initiatives that drive citizen participation in

the 24H+ vision;

2. mainstream 24H+ across Government, requiring all MDAs and MMDAs to develop

tailored 24H+

strategies, extend essential public services for round-the-clock

productivity, and align internal operations with the programme’s objectives.;

3. revitalise Community Infrastructure by improving lighting, safety, and

beautification in public spaces to support evening and night-time commercial

activity; and

4. reform Enabling Regulations, including labour laws, local government by-laws,

and business licensing, to support expanded hours of operation and innovation

in economic activity.

GO24 will transform passive individual citizens into organised active co-creators of

Ghana’s economic future and ensure that every arm of the State becomes a

proactive partner in national transformation.

34.

Page | 33

3.9Integrated Virtuous Cycle of Growth and Employment

24H+ Programme is integrated in conception and rollout. Each subprogramme

targets a critical node in the economy and interacts with and reinforces others in a

virtuous cycle. As domestic production rises, foreign exchange leakage declines. As

costs fall, firms become competitive. As exports grow, macroeconomic stability

improves. Reduced import dependency preserves foreign exchange, enabling

investment in productive capacity. Increased local value addition creates demand

for domestic inputs, which creates employment. Expanded employment generates

consumer purchasing power, and rising productivity improves export

competitiveness.

Together, they form a unified matrix that:

1 reduces the food and inputs import bill by building self-reliant, climate-resilient

agricultural systems;

2 expands domestic manufacturing capacity, raising industrial output from 12%

to 20% of GDP;

3 streamlines supply chains to cut post-harvest losses and logistics costs,

especially between northern and southern Ghana through inland water

transport.

4 provides patient capital at affordable rates to unlock MSME growth in priority

value chains;

5 develops a highly skilled, ethically grounded, digitally intelligent, culturally

confident workforce;

6 catalyses a revival in our cultural, artistic, and tourism industries and inculcates

a constructive African identity in our citizens; and

7 mainstream citizen engagement, volunteer work, accountability, and whole-of-

government alignment around these goals.

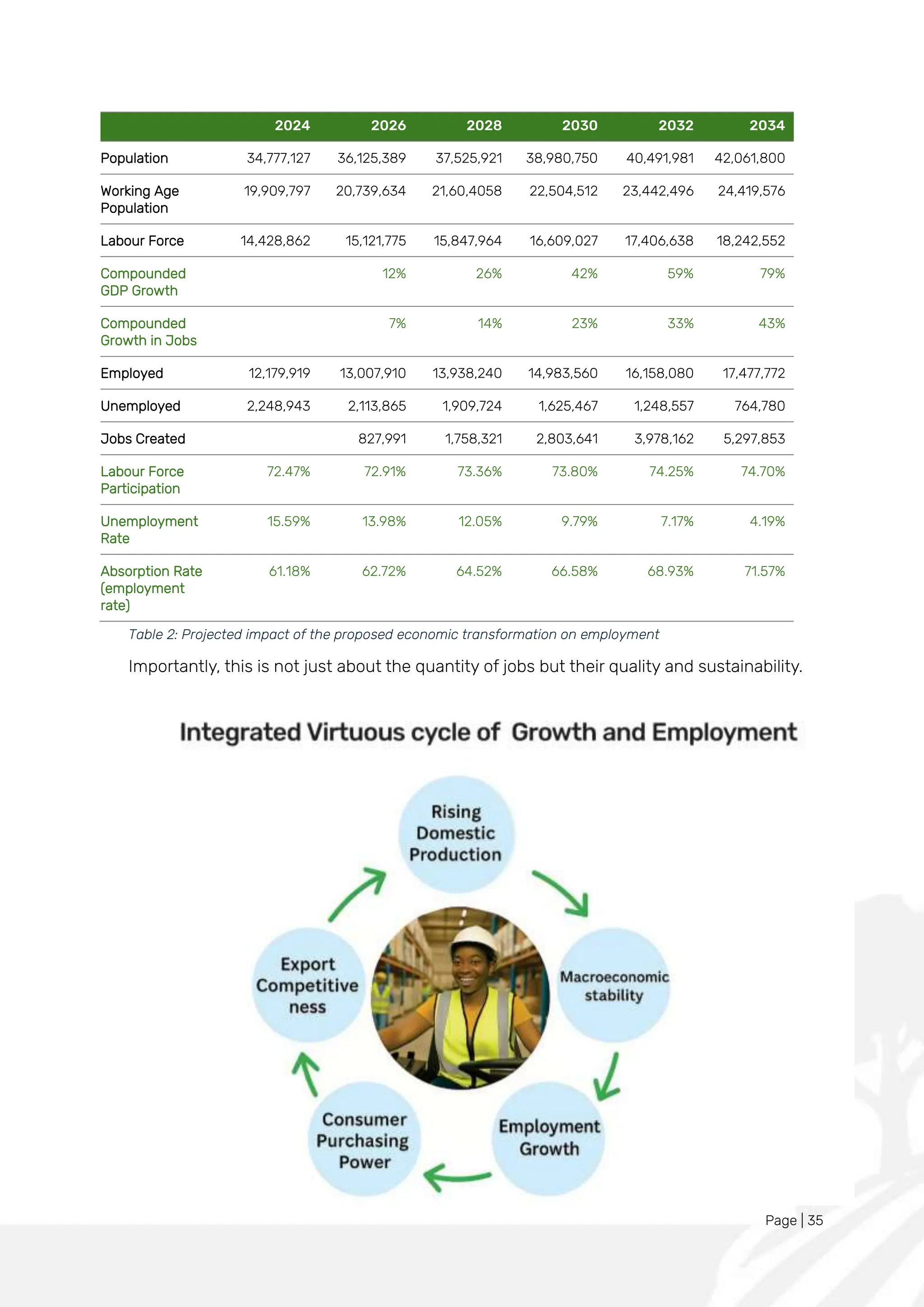

The 24H+ approach offers quantifiable benefits. Internal economic modelling

demonstrates that structural transformation would improve the relationship

between economic growth and job creation (the “employment elasticity of output”)

from the current 0.29 to approximately 0.55. This means that for every percentage

point of GDP growth, employment would expand by 0.55%, nearly double the current

rate. Combined with sustained GDP growth above 6%, the impact on unemployment

would be transformative.

As shown in Table 2, implementing this integrated approach could create more than

827,000 new jobs within the first two years, expanding to over 1.7 million jobs by

2028 and exceeding 5.2 million jobs by 2034. This would progressively reduce

Ghana's unemployment rate to approximately 12% by 2028, under 10% by 2030, and

ultimately to just 4.19% by 2034—a level consistent with full employment when

accounting for frictional unemployment.

Page | 35

20242026 2028 2030 2032 2034

Population 34,777,127 36,125,389 37,525,921 38,980,750 40,491,981 42,061,800

Working Age

Population

19,909,797 20,739,634 21,60,4058 22,504,512 23,442,496 24,419,576

Labour Force 14,428,862 15,121,775 15,847,964 16,609,027 17,406,638 18,242,552

Compounded

GDP Growth

12% 26% 42% 59% 79%

Compounded

Growth in Jobs

7% 14% 23% 33% 43%

Employed 12,179,919 13,007,910 13,938,240 14,983,560 16,158,080 17,477,772

Unemployed 2,248,943 2,113,865 1,909,724 1,625,467 1,248,557 764,780

Jobs Created 827,991 1,758,321 2,803,641 3,978,162 5,297,853

Labour Force

Participation

72.47% 72.91% 73.36% 73.80% 74.25% 74.70%

Unemployment

Rate

15.59% 13.98% 12.05% 9.79% 7.17% 4.19%

Absorption Rate

(employment

rate)

61.18% 62.72% 64.52% 66.58% 68.93% 71.57%

Table 2: Projected impact of the proposed economic transformation on employment

Importantly, this is not just about the quantity of jobs but their quality and sustainability.

37.

Page | 36

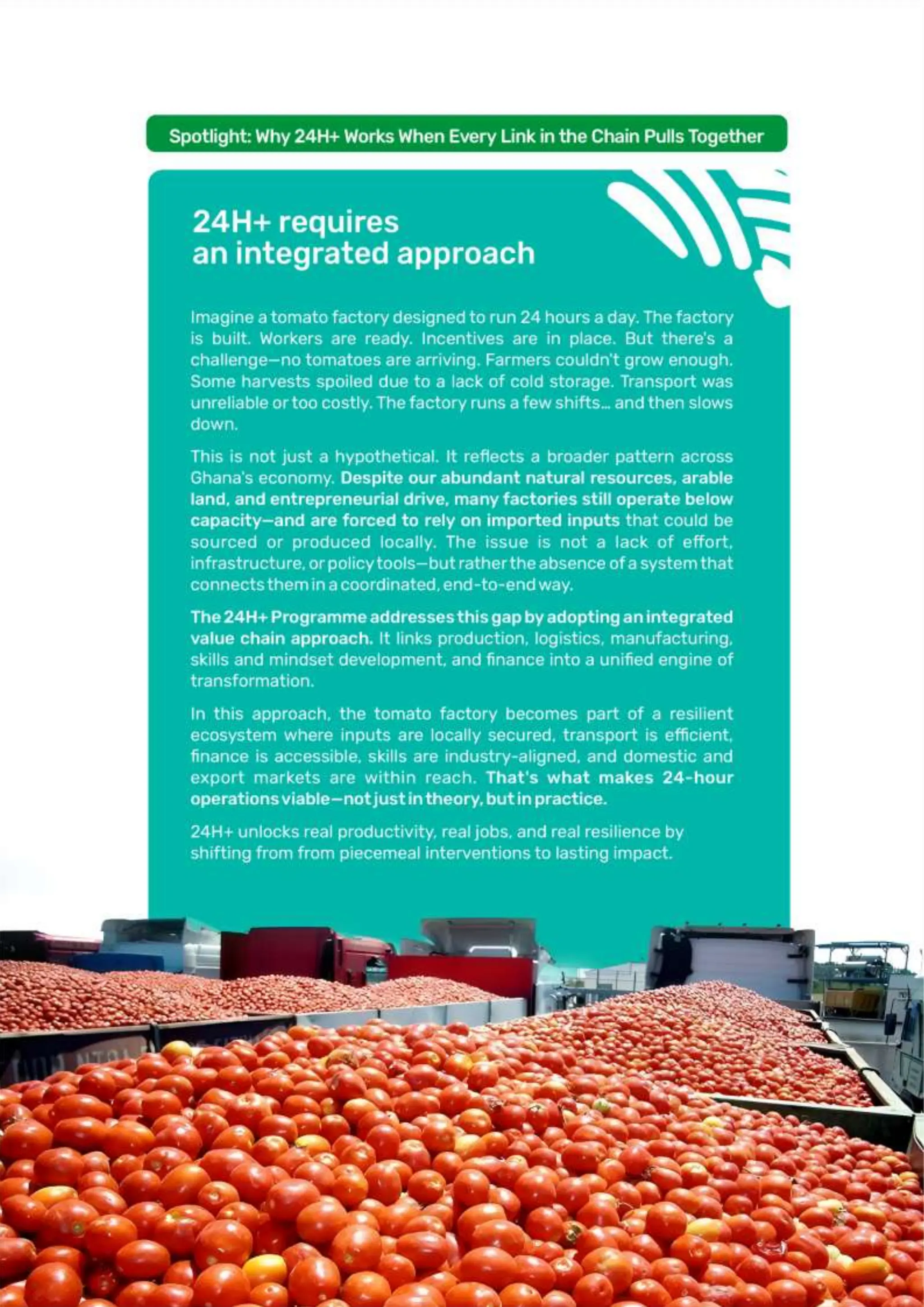

Spotlight:Why 24H+ Works When Every Link in the Chain Pulls Together

24H+ requires an integrated approach

Imagine a tomato factory designed to run 24 hours a day. The factory is built.

Workers are ready. Incentives are in place. But there’s a challenge—no tomatoes are

arriving. Farmers couldn’t grow enough. Some harvests spoiled due to a lack of cold

storage. Transport was unreliable or too costly. The factory runs a few shifts… and

then slows down.

This is not just a hypothetical. It reflects a broader pattern across Ghana’s economy.

Despite our abundant natural resources, arable land, and entrepreneurial drive,

many factories still operate below capacity—and are forced to rely on imported

inputs that could be sourced or produced locally. The issue is not a lack of effort,

infrastructure, or policy tools—but rather the absence of a system that connects

them in a coordinated, end-to-end way

The 24H+ Programme addresses this gap by adopting an integrated value chain

approach. It links production, logistics, manufacturing, skills and mindset

development, and finance into a unified engine of transformation.

In this approach, the tomato factory becomes part of a resilient ecosystem where

inputs are locally secured, transport is efficient, finance is accessible, skills are

industry-aligned, and domestic and export markets are within reach. That’s what

makes 24-hour operations viable—not just in theory, but in practice.

24H+ unlocks real productivity, real jobs, and real resilience by shifting from from piecemeal

interventions to lasting impact.

Page | 38

1.0Context for a 24H+

1.1 The Problem - Structural Deformity

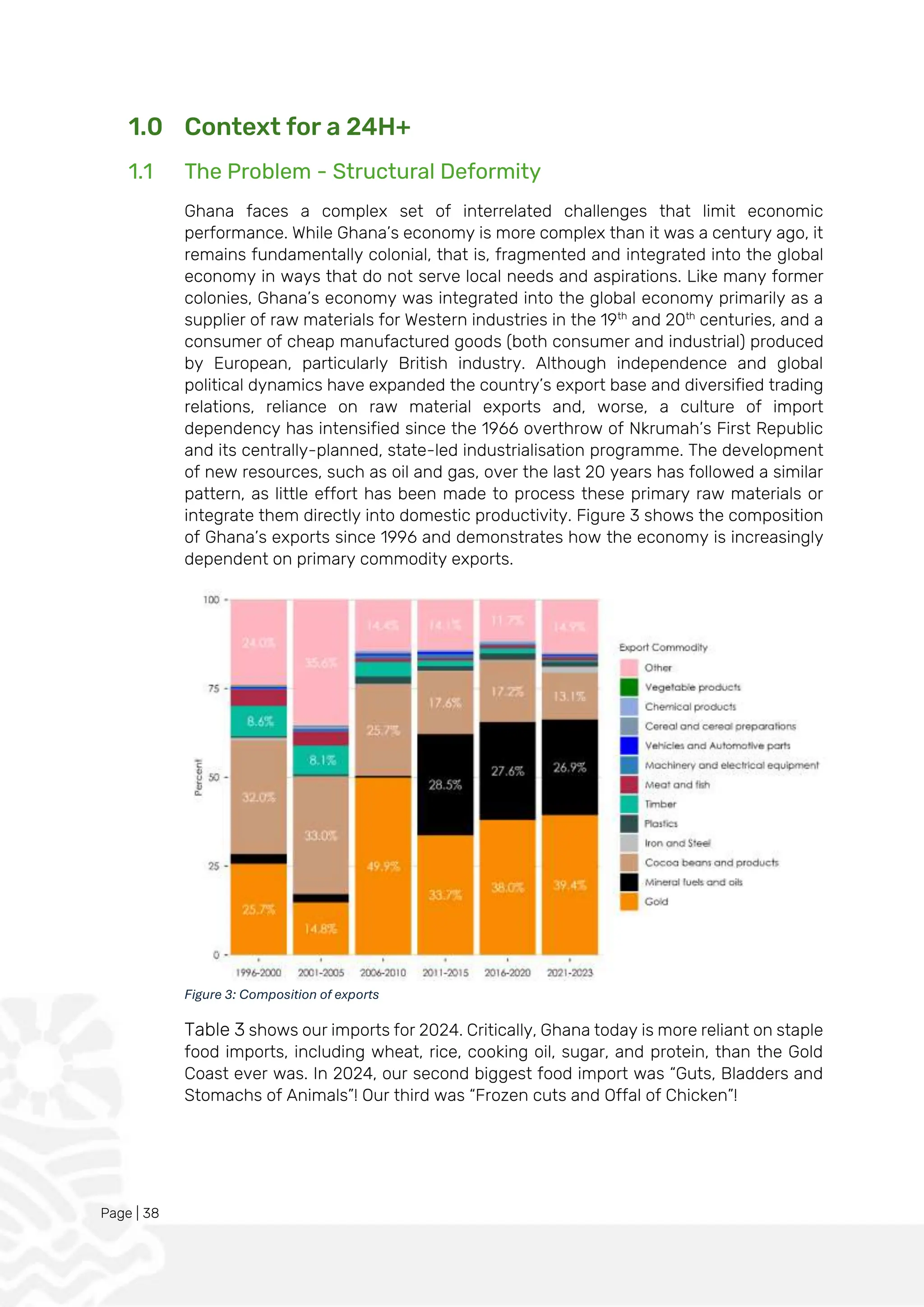

Ghana faces a complex set of interrelated challenges that limit economic

performance. While Ghana’s economy is more complex than it was a century ago, it

remains fundamentally colonial, that is, fragmented and integrated into the global

economy in ways that do not serve local needs and aspirations. Like many former

colonies, Ghana’s economy was integrated into the global economy primarily as a

supplier of raw materials for Western industries in the 19th

and 20th

centuries, and a

consumer of cheap manufactured goods (both consumer and industrial) produced

by European, particularly British industry. Although independence and global

political dynamics have expanded the country’s export base and diversified trading

relations, reliance on raw material exports and, worse, a culture of import

dependency has intensified since the 1966 overthrow of Nkrumah’s First Republic

and its centrally-planned, state-led industrialisation programme. The development

of new resources, such as oil and gas, over the last 20 years has followed a similar

pattern, as little effort has been made to process these primary raw materials or

integrate them directly into domestic productivity. Figure 3 shows the composition

of Ghana’s exports since 1996 and demonstrates how the economy is increasingly

dependent on primary commodity exports.

Figure 3: Composition of exports

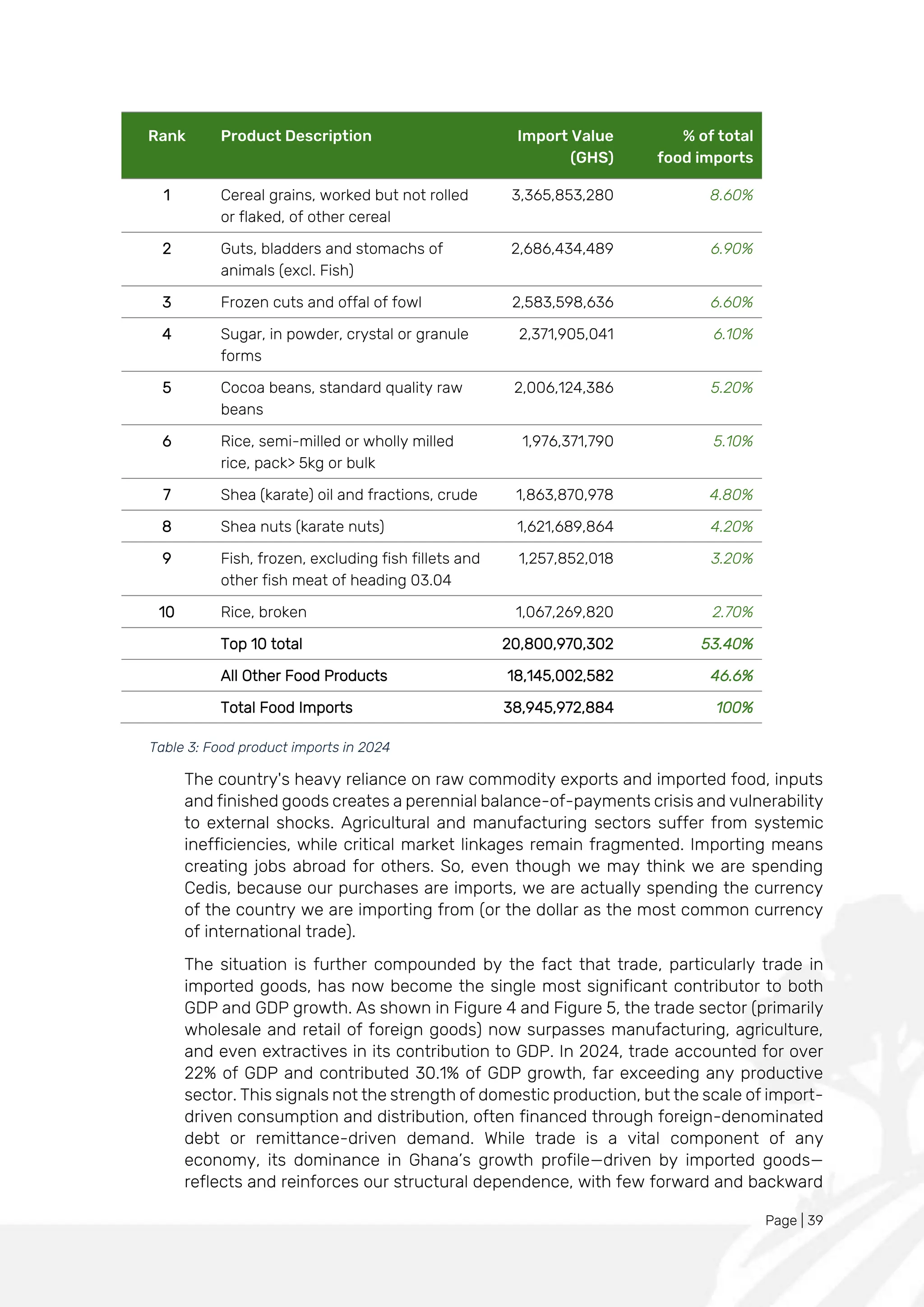

Table 3 shows our imports for 2024. Critically, Ghana today is more reliant on staple

food imports, including wheat, rice, cooking oil, sugar, and protein, than the Gold

Coast ever was. In 2024, our second biggest food import was “Guts, Bladders and

Stomachs of Animals”! Our third was “Frozen cuts and Offal of Chicken”!

40.

Page | 39

RankProduct Description Import Value

(GHS)

% of total

food imports

1 Cereal grains, worked but not rolled

or flaked, of other cereal

3,365,853,280 8.60%

2 Guts, bladders and stomachs of

animals (excl. Fish)

2,686,434,489 6.90%

3 Frozen cuts and offal of fowl 2,583,598,636 6.60%

4 Sugar, in powder, crystal or granule

forms

2,371,905,041 6.10%

5 Cocoa beans, standard quality raw

beans

2,006,124,386 5.20%

6 Rice, semi-milled or wholly milled

rice, pack> 5kg or bulk

1,976,371,790 5.10%

7 Shea (karate) oil and fractions, crude 1,863,870,978 4.80%

8 Shea nuts (karate nuts) 1,621,689,864 4.20%

9 Fish, frozen, excluding fish fillets and

other fish meat of heading 03.04

1,257,852,018 3.20%

10 Rice, broken 1,067,269,820 2.70%

Top 10 total 20,800,970,302 53.40%

All Other Food Products 18,145,002,582 46.6%

Total Food Imports 38,945,972,884 100%

Table 3: Food product imports in 2024

The country's heavy reliance on raw commodity exports and imported food, inputs

and finished goods creates a perennial balance-of-payments crisis and vulnerability

to external shocks. Agricultural and manufacturing sectors suffer from systemic

inefficiencies, while critical market linkages remain fragmented. Importing means

creating jobs abroad for others. So, even though we may think we are spending

Cedis, because our purchases are imports, we are actually spending the currency

of the country we are importing from (or the dollar as the most common currency

of international trade).

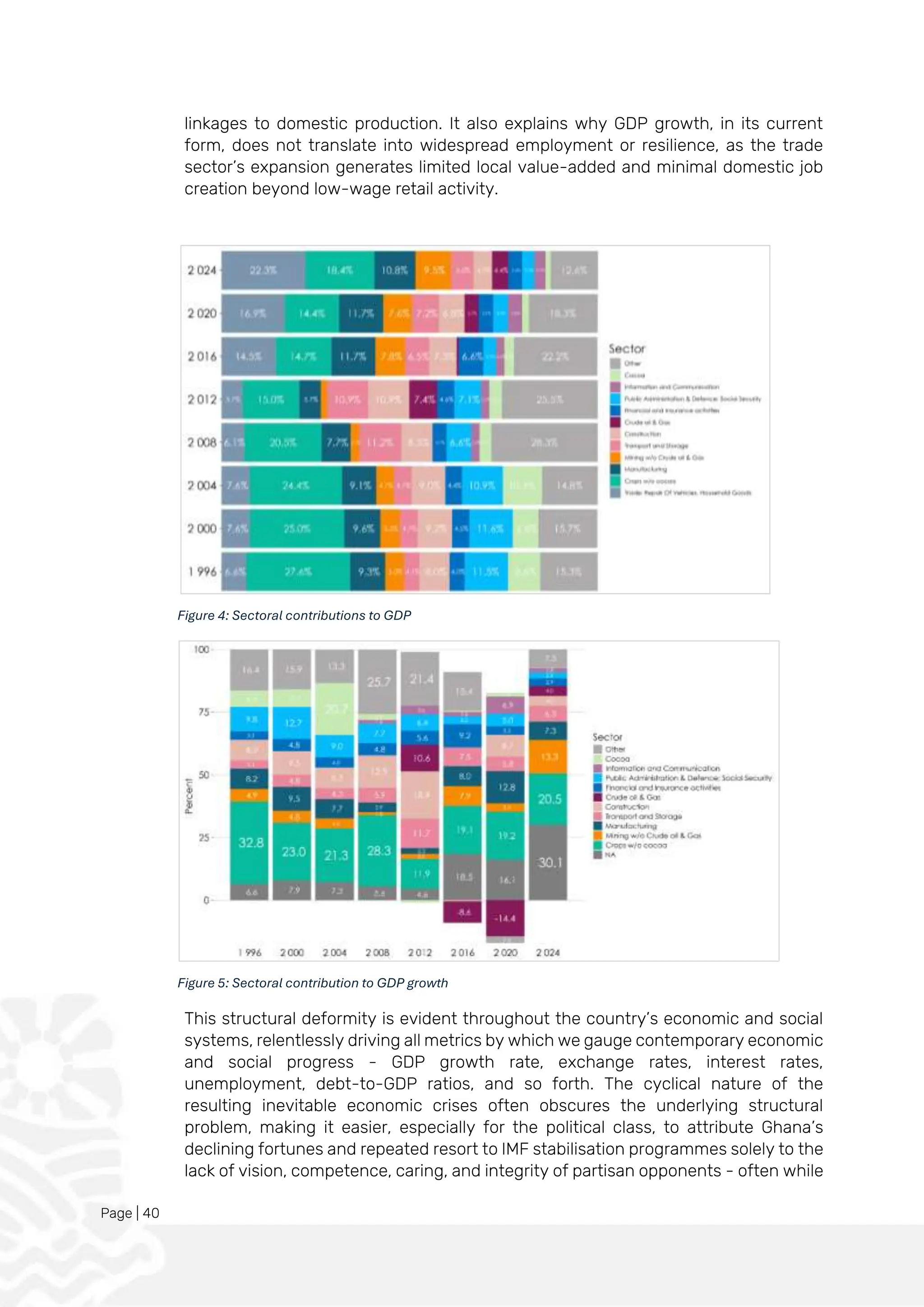

The situation is further compounded by the fact that trade, particularly trade in

imported goods, has now become the single most significant contributor to both

GDP and GDP growth. As shown in Figure 4 and Figure 5, the trade sector (primarily

wholesale and retail of foreign goods) now surpasses manufacturing, agriculture,

and even extractives in its contribution to GDP. In 2024, trade accounted for over

22% of GDP and contributed 30.1% of GDP growth, far exceeding any productive

sector. This signals not the strength of domestic production, but the scale of import-

driven consumption and distribution, often financed through foreign-denominated

debt or remittance-driven demand. While trade is a vital component of any

economy, its dominance in Ghana’s growth profile—driven by imported goods—

reflects and reinforces our structural dependence, with few forward and backward

41.

Page | 40

linkagesto domestic production. It also explains why GDP growth, in its current

form, does not translate into widespread employment or resilience, as the trade

sector’s expansion generates limited local value-added and minimal domestic job

creation beyond low-wage retail activity.

Figure 4: Sectoral contributions to GDP

Figure 5: Sectoral contribution to GDP growth

This structural deformity is evident throughout the country’s economic and social

systems, relentlessly driving all metrics by which we gauge contemporary economic

and social progress - GDP growth rate, exchange rates, interest rates,

unemployment, debt-to-GDP ratios, and so forth. The cyclical nature of the

resulting inevitable economic crises often obscures the underlying structural

problem, making it easier, especially for the political class, to attribute Ghana’s

declining fortunes and repeated resort to IMF stabilisation programmes solely to the

lack of vision, competence, caring, and integrity of partisan opponents - often while

42.

Page | 41

adoptingremedies for economic salvation rooted within the same development

paradigm. Leadership integrity, industriousness, compassion, and competence are

crucial for national development. They are not, however, sufficient. They are not a

substitute for the sound and integrated production structure that Ghana needs.

In addition to this structural deformity, limited access to finance restricts MSME

growth and participation in strategic value chains. Studies show that access to

finance remains the most important obstacle to enterprise growth in Ghana, with

most businesses relying on private savings or internal resources to finance their

operations8

.

Underlying these challenges is a significant human resource gap, with workforce

skills development programmes not aligned with the demands of a modern,

competitive economy. Additionally, weak citizen engagement and inadequate

stakeholder coordination undermine the sustainability and ownership of

development initiatives. These factors collectively constrain Ghana's ability to

generate sustainable livelihoods, achieve food security, develop competitive

industries, and fully participate in regional and global markets.

Taken together, these challenges reinforce a development trap. Without a

coordinated, multi-dimensional strategy that addresses production, market

systems, finance, skills, and public mobilisation as interdependent components,

Ghana risks continued economic vulnerability, limited value capture, and unrealised

national potential in an increasingly competitive global landscape.

1.2 Interconnected Structural Constraints

The deformity in the economy manifests in these seven interconnected structural

constraints that collectively impede transformation.

1.2.1 Agricultural Underperformance and Food Import Dependence

Ghana spends over $2 billion annually on food imports despite possessing vast

agricultural potential9

. This paradox stems from multiple interconnected factors:

only 5% of arable land is irrigated10

, post-harvest losses exceed 30% of production,

and smallholder farmers who produce 80% of Ghana's food11

struggle with limited

mechanisation, an ageing workforce, and restricted access to finance. The 2025

State of the Nation Address acknowledged that Ghana’s agriculture remains below

potential due to low productivity and underinvestment in value-addition

infrastructure, stressing that food inflation is worsened by a failure to achieve food

self-sufficiency12

. This agricultural underperformance directly impacts other sectors

by constraining raw material supply for manufacturing, driving food inflation,

depleting foreign reserves, and limiting rural income growth13

.

8

The Constraints to Inclusive Growth in Ghana, MiDA (2024)

9

Ministry of Food and Agriculture. (2025, April). Feed Ghana Programme rallies Ghanaians to cut $2billion food import. Retrieved

from https://www.modernghana.com/news/1390729/feed-ghana-programme-rallies-ghanaians-to-cut.html

10

Ministry of Food and Agriculture (MoFA). (2021). Agriculture in Ghana: Facts and Figures (2021). Accra: Statistics, Research and

Information Directorate (SRID), MoFA.

11

United Nations Environment Programme. (2021). Supporting smallholder farmers in Ghana through innovative climate adaptation.

Retrieved from https://www.unep.org/ndc/news-and-stories/story/supporting-smallholder-farmers-ghana-through-innovative-climate-

adaptation

12

National Food Buffer Stock Company. (2025, March). Key Agribusiness Highlights from Ghana's 2025 SONA. Retrieved

from https://nafco.gov.gh/uncategorized/key-agribusiness-highlights-from-ghanas-2025-sona/

13

Ghana Statistical Service. (2021). Ghana's Agriculture Sector Report. Retrieved from https://www.gipc.gov.gh/wp-

content/uploads/2023/03/Ghanas-Agriculture-Sector-Report-1.pdf

43.

Page | 42

1.2.2Manufacturing Sector Stagnation and Limited Industrialisation

Ghana’s manufacturing sector has long underperformed relative to its potential. Its

contribution to GDP has stagnated at approximately 12%, and it employs only 10–

12% of the formal labour force—a figure that has remained largely unchanged for over

a decade. This stagnation is driven by a set of interrelated constraints that limit

productivity, discourage investment, and undermine the sector’s ability to anchor

structural transformation.

One of the most critical constraints is infrastructure deficiency, particularly in

transport and energy. Only 27% of roads in Ghana are tarred,14

raising logistics costs

and impeding efficient supply chain integration. Energy access is also unreliable and

costly. According to the World Bank Enterprise Survey (2023), electricity outages

account for 9% of annual sales losses for firms. Businesses often face multiple power

outages per month, and non-residential consumers pay electricity tariffs as high as

$0.15 per kilowatt-hour, among the highest in our sub-region15

.

Access to affordable finance is another major barrier. Interest rates for

manufacturers in Ghana are 15–20 percentage points higher than in competing

countries, making it difficult for firms to expand, upgrade machinery, or compete

globally. Compounding this is the fact that manufacturing capacity utilisation

remains low, averaging only 42–46%16

, a reflection of weak demand, unreliable

inputs, and persistent market fragmentation.

These constraints collectively limit the sector’s ability to create jobs, generate

foreign exchange, and reduce import dependence.

1.2.3 Human Capital Development Gaps and Skills Mismatches

Ghana faces a 22% youth unemployment rate, with almost 70% of employed persons

in vulnerable employment - often lacking job security, formal contracts, or access to

benefits17

. This structural issue limits both economic inclusion and productivity

growth.

Compounding this, access to digital skills remains uneven. According to the Ghana

Poverty Assessment by the World Bank in 2020, only 33.8% of Ghanaian youth

possess ICT skills, and those with such skills are nearly three times more likely to

access wage employment than those without. Gender disparities are also notable:

39% of young men have ICT skills compared to only 22.3% of young women,

contributing to unequal employment outcomes in technology-driven sectors.

Several interlinked factors contribute to this challenge. First, many educational and

training curricula remain outdated and poorly aligned with industry needs.

Graduates often leave school without the technical or practical skills required by

employers, particularly in potential growth industries such as manufacturing, ICT,

14

Ministry of Roads and Highways. (2021). Press Release on Completed Roads at SONA. Retrieved from https://mrh.gov.gh/wp-

content/uploads/2022/03/Press-Release-on-Completed-Roads-at-SONA.pdf

15

Karimu, A., et al. (2024). The welfare implication of reversing Ghana's electricity tariff structure. International Growth Centre. Retrieved

from https://www.theigc.org/sites/default/files/2025-03/Karimu%20et%20al%20Working%20Paper%20April%202024.pdf

16

Association of Ghana Industries. (2022). Industry Perspectives Magazine Vol.5 Qrt 2 2022. Retrieved

from https://www.agighana.org/wp-content/uploads/2022/08/Industry-Perspectives-Magazine-Vol.5-Qrt-2-2022.pdf

17

Ghana Statistical Service. (2024). 2023 Quarter Labour Statistics Report. Retrieved

from https://statsghana.gov.gh/gssmain/fileUpload/pressrelease/2023_Quarter_Labour_Statistics_Bulletin_full_report.pdf

44.

Page | 43

agriculture,and logistics. Second, digital literacy remains low, especially among

informal workers and older segments of the labour force. Despite the rising demand

for digital and data-related competencies, access to training in these areas is still

limited, and many existing workers are unprepared for the digital demands of the

21st

-century economy. Third, opportunities for practical, hands-on training—whether

through apprenticeships, internships, or modernised vocational instruction—are

severely constrained by underinvestment in facilities and weak linkages between

training institutions and employers. The Ghana Employers Association found that

47% of employers identified computer literacy or IT skills as lacking among existing

employees, while only 2% of Ghana's workforce has completed formal Technical and

Vocational Education and Training (TVET) programmes18

.

Only a small proportion of Ghana’s workforce has completed formal Technical and

Vocational Education and Training (TVET), and even fewer workers have received

industry-aligned, work-based experience. This leaves a growing number of young

people caught in a cycle of underemployment or skills mismatches, even as more

than 300,000 people enter the workforce each year.

1.2.4 Supply Chain Inefficiencies and Market System Failures

Ghana’s logistics and market systems remain inefficient, fragmented, and costly,

undermining competitiveness across agriculture, manufacturing, and trade.

Logistics costs account for an estimated 40–50% of product value, far above the

global average of 15%–20%19

. This is largely driven by overreliance on road transport,

which carries 80%–90% of freight and passenger traffic despite underinvestment in

road quality, connectivity, and complementary transport modes such as rail and

inland water transport20

.

These inefficiencies drive post-harvest losses of 30–50%, particularly in perishable

value chains such as fruits, vegetables, and livestock, due to inadequate storage,

preservation, and distribution infrastructure. Smallholder farmers and MSMEs—who

form the backbone of Ghana’s production economy—lack access to reliable

aggregation centres, structured markets, and affordable logistics services. These

barriers restrict their ability to scale, connect to processors, or participate in high-

value trade.

The government has acknowledged that food insecurity, inflation, and industrial

underperformance are all symptoms of weak connective infrastructure between

production and markets. 24H+, therefore, focuses on incentivising private

investment in warehousing, cold chain systems, inland transport services, and

structured market platforms that improve price transparency, shorten distribution

chains, and reward quality.

These supply chain inefficiencies directly reduce the competitiveness of Ghanaian

goods, raise consumer prices, and limit the ability of producers and processors to

18

World Bank. (2023, July 12). Improve Technical and Vocational Education and Training (TVET) to Meet Skills-Labour Mismatch.

Retrieved from https://www.worldbank.org/en/news/press-release/2023/07/12/improve-technical-vocational-education-training-tvet-

meet-skills-labour-mismatch

19

World Bank. (2018). Connecting to Compete 2018: Trade Logistics in the Global Economy. Retrieved

from https://documents1.worldbank.org/curated/en/576061531492034646/pdf/Connecting-to-compete-2018-trade-logistics-in-the-

global-economy-the-logistics-performance-index-and-its-indicators.pdf

20

Ghana Investment Promotion Centre. (2018). Ghanaian government targets improving the country's transport network amid rising

demand. Oxford Business Group. Retrieved from https://oxfordbusinessgroup.com/reports/ghana/2018-report/economy/vehicles-for-

growth-the-government-invests-in-infrastructure-amid-rising-demand

45.

Page | 44

meetdemand reliably or competitively. Addressing them will require a deliberate

shift toward multimodal logistics development, expanded post-harvest

infrastructure, and transparent, technology-enabled market systems that reward

efficiency, coordination, and local value addition.

1.2.5 Financial System Bottlenecks and Value Chain Financing Gaps

Ghana’s financial architecture remains misaligned with the needs of its productive

sectors, especially agriculture, manufacturing, and small, medium and large

enterprise development. While these sectors drive the bulk of employment and

domestic economic activity, they remain underserved by the formal financial system.

According to the International Finance Corporation (IFC) and the World Bank,

Ghanaian micro, small, and medium enterprises (MSMEs) face a financing gap of $6.1

billion, equivalent to 13% of national GDP21

. Only 20–23% of small and medium-sized

businesses access formal credit, and those that do often encounter prohibitively

high borrowing costs. Data from the Bank of Ghana’s February 2024 APR report

shows SME interest rates ranging from 29.58% to 44.24%, significantly higher than

in many peer economies22

.

The agricultural sector, which employs nearly 40% of the national workforce,

receives only about 4% of total commercial bank lending. This discrepancy reflects

deep structural weaknesses. Most available financial products are poorly suited to

the seasonal cash flow cycles typical of agricultural and manufacturing value chains.

Short repayment periods and inflexible terms undermine the viability of long-term

investments, particularly in equipment, processing, and logistics infrastructure.

Fewer than 10% of loans extend beyond a three-year tenor, constraining capital

formation across value chains.

A further constraint is Ghana’s heavily collateralised lending environment, where

most banks require physical collateral valued at 150–250% of the loan amount—most

often land or real estate. This creates a structural barrier for smallholder farmers,

informal producers, and early-stage entrepreneurs who lack titled assets. In effect,

access to credit is determined more by asset ownership than by business viability,

locking out the majority of producers from the financing they need to scale.

These interlinked bottlenecks fragment value chains, perpetuate import

dependency, and limit the productive sector’s contribution to national

transformation.

1.2.6 Limited Citizen Engagement and Civic Participation in Development

Public participation in Ghana's development initiatives remains constrained by

several interconnected factors. A significant issue is the declining trust in local

government institutions. According to Afrobarometer surveys, the proportion of

Ghanaians expressing "a lot" or "somewhat" trust in local government councils

21

World Bank. (2020). Improving Access to Finance for Ghanaian SMEs: Role for a New DFI.

22

Bank of Ghana. (2024). APR for February 2024. Retrieved from https://www.bog.gov.gh/wp-content/uploads/2024/03/APR-For-

February-2024.pdf

46.

Page | 45

decreasedfrom 62% in 2012 to 47% in 2017, indicating a notable erosion of

confidence in local governance structures23

.

This decline in trust is compounded by limited citizen engagement with local

government officials. In 2017, only 28% of Ghanaians reported contacting their local

government councillors at least once in the preceding year, suggesting a disconnect

between citizens and their local representatives.

Furthermore, structural challenges hinder the integration of local economies into

national development frameworks. The lack of structured local markets and

cooperatives, along with inadequate infrastructure and safety concerns, limits

round-the-clock commercial activity. Regulatory constraints also obstruct business

expansion, restricting opportunities for economic growth at the community level.

1.2.7 Structural Economic Dependency and Value Chain Fragmentation

Ghana's economy operates in a dependency loop where we export raw materials at

low value and import finished goods at high cost. In 2024, gold, crude petroleum oils,

and cocoa products together accounted for about 80% of total exports24

. On the

import side, processed consumer and industrial goods dominate. The top 10 import

items made up 33.4% of all imports, led by automotive gas oil (USD 2.4 billion) and

motor spirit (USD 2.0 billion)25

. Other key imports include cement clinker, used motor

vehicles, machinery, cereal grains, frozen meats, and herbicides. Although Ghana

recorded a nominal trade surplus in 2024, adjusted figures suggest a real trade

deficit when inflation and import composition are accounted for, underscoring the

limitations of an extractive, import-dependent growth model.

This economic structure severely limits forward and backwards linkages, meaning

growth in agriculture for example, rarely translates into broader economic activity or

job creation in manufacturing, logistics, or retail. Nearly 50% of Ghana’s total

production inputs are imported, creating vulnerability to global price volatility and

currency shocks.

This structural challenge has led to concentrated wealth creation, with the GINI

coefficient rising from 0.41 to 0.46 over the past decade (Ghana Statistical Service,

2023), indicating that economic growth does not reliably translate into broad-

based prosperity or meaningful development for most Ghanaians.

1.3 The Cascading Effects of Structural Constraints

These seven constraints interact in a self-reinforcing cycle that limits Ghana's

economic transformation:

1. Agricultural underperformance → reduces raw material supply → constrains

agro-processing → increases import dependence → depletes foreign exchange

23

Afrobarometer. (2018). Summary of Results: Afrobarometer Round 7 Survey in Ghana, 2017. Retrieved

from https://www.afrobarometer.org/wp-content/uploads/2022/02/gha_r7_sor_10042019.pdf

24

Ghana Statistical Service. (2025). 2024 Trade Full Year Report. Retrieved

from https://statsghana.gov.gh/gssmain/fileUpload/Trade/2024_Trade_Full_Year_Report-_25-02-2025_Final_Print.pdf

25

Ghana Statistical Service. (2025). Top 10 Imports in 2024. Retrieved from https://www.graphic.com.gh/business/business-news/list-

see-ghanas-top-10-imports-in-2024.html

47.

Page | 46

→limits resources for infrastructure development → reinforces agricultural

challenges

2. Manufacturing stagnation → reduces job creation → limits value addition →

increases import dependence → constrains export earnings → reduces tax

revenue → limits public infrastructure investment → reinforces manufacturing

constraints