Deloitte – State of AI in the Enterprise | Actionable AI Strategies & Insights

Discover Deloitte’s 'State of AI in the Enterprise' report. Learn how industries are adopting AI, explore data-driven insights, and uncover actionable frameworks to drive AI value through culture, tech, and operations alignment.

Deloitte – State of AI in the Enterprise | Actionable AI Strategies & Insights

1.

Deloitte’s State ofGenerative AI in the Enterprise

Quarter four report

January 2025

Now decides next:

Generating a new future

deloitte.com/us/state-of-generative-ai

2.

2

2

Introduction

Key findings

Looking backat 2024

Now: Where we are

Next: Looking ahead

Considerations

Case studies

Authorship & Acknowledgments

About the Deloitte AI Institute

About the Deloitte Center for Integrated Research

About the Deloitte Center for Technology, Media & Telecommunications

Methodology

Table of contents

3.

Introduction

Foreword

It was onlyabout 10 years ago when visionary tech leaders started talking about

a future powered by ubiquitous computing and ambient intelligence. Back then it

sounded like science fiction. Today, it’s real. No where is this future more evident than

in the rapid advancement and adoption of AI technologies. New models and tools are

gaining greater and greater capabilities and performing more complex reasoning. Even

what was state of the art a few years ago pales in comparison to what we have today.

In this AI era, many now believe that Moore’s Law is effectively dead. And we have

every reason to believe that the AI flywheel will continue to accelerate with every week

and year—often referenced as the greatest secular shift of this quarter century.

Despite the technology’s rapid pace, I hear from clients and business leaders who are

wondering when it will meet their transformational expectations—when will business

leaders see the value and innovation that has been promised?

Just like the internet, cloud, or even mobile, the transformational opportunities weren’t

uncovered overnight. But as they became pervasive, they drove significant disruption

to business and technology capabilities, and also triggered many new business

models, new products and services, new partnerships, and new ways of working and

countless other innovations that led to the next wave across industries. As we have

experienced the half-life of these waves continues to be shorter. As such, it requires

enterprises to be a lot more structurally agile to adapt, embrace and innovate to stay

relevant and differentiated.

In the following report, we see that most companies are transforming at the speed

of organizational change, not at the speed of technology. This is not surprising but is

something that will need to be addressed. That said, many are also already using

GenAI to create business value that exceeds their expectations—with compelling new

use cases emerging every day.

So, what do I say to clients who are in the trenches of this transformation? Don’t lose

focus. Stay curious, and challenge the orthodoxies of your organizations. GenAI and

AI broadly is our reality—it’s not going away. While there are more questions than

answers, but to stay in the game, leaders must be willing to try, do unconventional

things, learn and help mature.

State of GenAI in the Enterprise is a snapshot in time of this great transformation. An

opportunity for you to see where and how organizations across industries are finding

their way. I hope it serves to spark new ideas and new approaches that help illuminate

the path to your organization’s AI-fueled future.

–Ranjit Bawa, Principal, US Chief Strategy and Technology Officer

3

4.

Introduction

Generating a newfuture

For the past year, Deloitte has been conducting quarterly global survey reports and

executive interviews focused on Generative AI (GenAI) in the enterprise. We titled

our study Now decides next because we believed in GenAI’s potential to dramatically

transform how businesses operate—and that the actions companies take today will

have a decisive impact on their ability to succeed with GenAI in the future. And that’s

exactly what we found.

As with previous transformational technologies, the initial excitement and hype about

GenAI has gradually given way to a mindset of positive pragmatism. Many companies

are already seeing encouraging returns on their early GenAI investments. However,

those companies and others have learned that creating value with GenAI—and

deploying it at scale—is hard work. Although the technology at times seems like magic,

there is no magic wand when it comes to GenAI adoption, deployment, integration

and value creation.

4

4

5.

There is aspeed limit.

GenAI technology continues to advance at incredible

speed. However, most organizations are moving at the

speed of organizations, not at the speed of technology.

No matter how quickly the technology advances—or

how hard the companies producing GenAI technology

push—organizational change in an enterprise can only

happen so fast.

Barriers are evolving.

Significant barriers to scaling and value creation are still

widespread across key areas. And, over the past year

regulatory uncertainty and risk management have risen in

organizations’ lists of concerns to address. Also, levels of trust

in GenAI are still moderate for the majority of organizations.

Even so, with increased customization and accuracy of

models—combined with a focus on better governance—

adoption of GenAI is becoming more established.

Some uses are outpacing others.

Application of GenAI is further along in some business

areas than in others in terms of integration, return on

investment (ROI) and expectations. The IT function is

most mature; cybersecurity, operations, marketing and

customer service are also showing strong adoption and

results. Organizations reporting higher ROI for their

most scaled initiatives are broadly further along in their

GenAI journeys.

Introduction

Key findings

All statistics noted in this report and its graphics are derived from Deloitte’s fourth quarterly survey, conducted July – September 2024; The

State of Generative AI in the Enterprise: Now decides next, a report series. N (Total leader survey responses) = 2,773. Percentages in this report

and its charts may not add up to 100, due to rounding.

Generative AI is an evolving area of artificial intelligence and refers to AI that in response to a query—a prompt—can create new text,

images, video and other assets. Generative AI systems can interact with humans and are built—or “trained”—on datasets that range in

size and quality from small language models (SLMs) to large language models (LLMs). Generative AI is also referred to as “GenAI.”

Evolving upon GenAI technologies, emerging AI agents are software systems that can complete complex tasks and meet objectives with little

or no human intervention. They are called “agents” because they have the agency to act independently, planning and executing actions to

achieve a specified goal. Related, the vision for agentic AI is that autonomous AI agents will be able to execute assigned tasks consistently and

reliably by acquiring and processing multimodal data, using various tools to complete tasks, and coordinating with other AI agents—all while

remembering what they’ve done in the past and learning from their experience.

5

6.

The focus ison core business value.

A strategic shift is emerging, from technology catch-up

to competitive differentiation with GenAI. Beyond the

IT function, organizations tend to focus their deepest

GenAI deployments on parts of the business uniquely

critical to success in their industries.

The C-suite sees things differently.

Relative to leaders outside of the C-suite, CxOs tend

to express a rosier view of their organization’s GenAI

investments—and how easily and quickly GenAI’s

barriers will be addressed and value achieved. It’s critical

that CxOs move on from being cheerleaders to being

champions for achieving organizational efficiency and

market competitiveness.

Agentic AI is here.

Agentic AI is gaining interest as a breakthrough

innovation that could unlock the full potential of GenAI,

with GenAI-powered systems having the “agency”

to orchestrate complex workflows, coordinate tasks

with other agents, and execute tasks without human

involvement. However, agentic AI is not a silver bullet and

all the broad challenges currently facing GenAI still apply.

Introduction

Key findings

6

7.

Our previous quarterlyreport said the clock was ticking

to prove value—and this remains true today. Senior

decision-makers might not be demanding tangible value

and financial results from GenAI yet, but they soon will be.

More and more organizations are moving from GenAI

experimentation to deployment and scaling—with

proven use cases emerging and significant ROI being

achieved through the most advanced GenAI initiatives.

What’s more, despite some feelings of disillusionment

and unmet expectations, the vast majority of

organizations we surveyed are taking a realistic

perspective and showing sustained commitment in their

quest for value from GenAI, and they seem willing to

do the hard work that needs to be done. Foundation

model improvements—including domain and industry

customization—and the promise of AI agents could

help overcome inherent challenges and accelerate

the creation of business value. However, it might be a

multiyear journey for some organizations to reach full-scale

deployment and achieve the ROI they are looking for.

With GenAI, some level of uncertainty is unavoidable

and the technology will likely continue to advance at

a rapid pace. Business and technology leaders, for

their part, should focus on what they can control—

namely, organizational readiness, particularly in areas

such as data, risk management, governance, regulatory

compliance and workforce / talent. Addressing issues

in these key areas will help position organizations for

success with GenAI no matter how the future unfolds.

Introduction

Key findings

About the State of Generative

AI in the Enterprise:

Wave four survey results

The wave four survey covered in this report was fielded

to 2,773 director- to C-suite-level respondents across six

industries and 14 countries between July and September

2024. Industries included: consumer; energy, resources and

industrials; financial services; life sciences and health care;

technology, media and telecom; and government and public

services. The survey data was augmented by additional

insights from 15 interviews with C-suite executives and AI and

data science leaders at large organizations across a range of

industries. For details on methodology, please see p. 45.

This quarterly report is part of an ongoing series by the

Deloitte AI InstituteTM

to help leaders in business, technology

and the public sector track the rapid pace of Generative AI

change and adoption. The series is based on Deloitte’s

State of AI in the Enterprise reports, which have been

released annually the past five years. Learn more at

deloitte.com/us/state-of-generative-ai.

7

8.

The case studiesfeatured in this report are a small subset of the insights from our ongoing

in-depth interviews with business and AI leaders from a wide range of industries. The goal is

to build on the quantitative findings from our quarterly surveys by capturing practical, real-

world insights directly from leaders and organizations on the front lines of GenAI adoption.

Our interviews explore how leading organizations in diverse industries are

using GenAI to create value. Most notably, we are seeing initiatives focused

on applying GenAI to business-specific challenges in areas critical to success

in that organization’s industry. Examples include using GenAI for:

•

Brand promotion and integrated business planning in the consumer products industry

• Predictive maintenance for physical assets in the energy industry

• Drug discovery and clinical trial tracking in the pharmaceutical industry

• Cybersecurity and portfolio management in the financial services industry

•

Sales enablement, chip development and improved search in the technology industry

•

Archive management and music source separation in the media and entertainment industry

This focus on mission-critical activities suggests a broad strategic shift in the GenAI

landscape, from technology catch-up to competitive differentiation.

Real-world case studies

Go to case studies

8

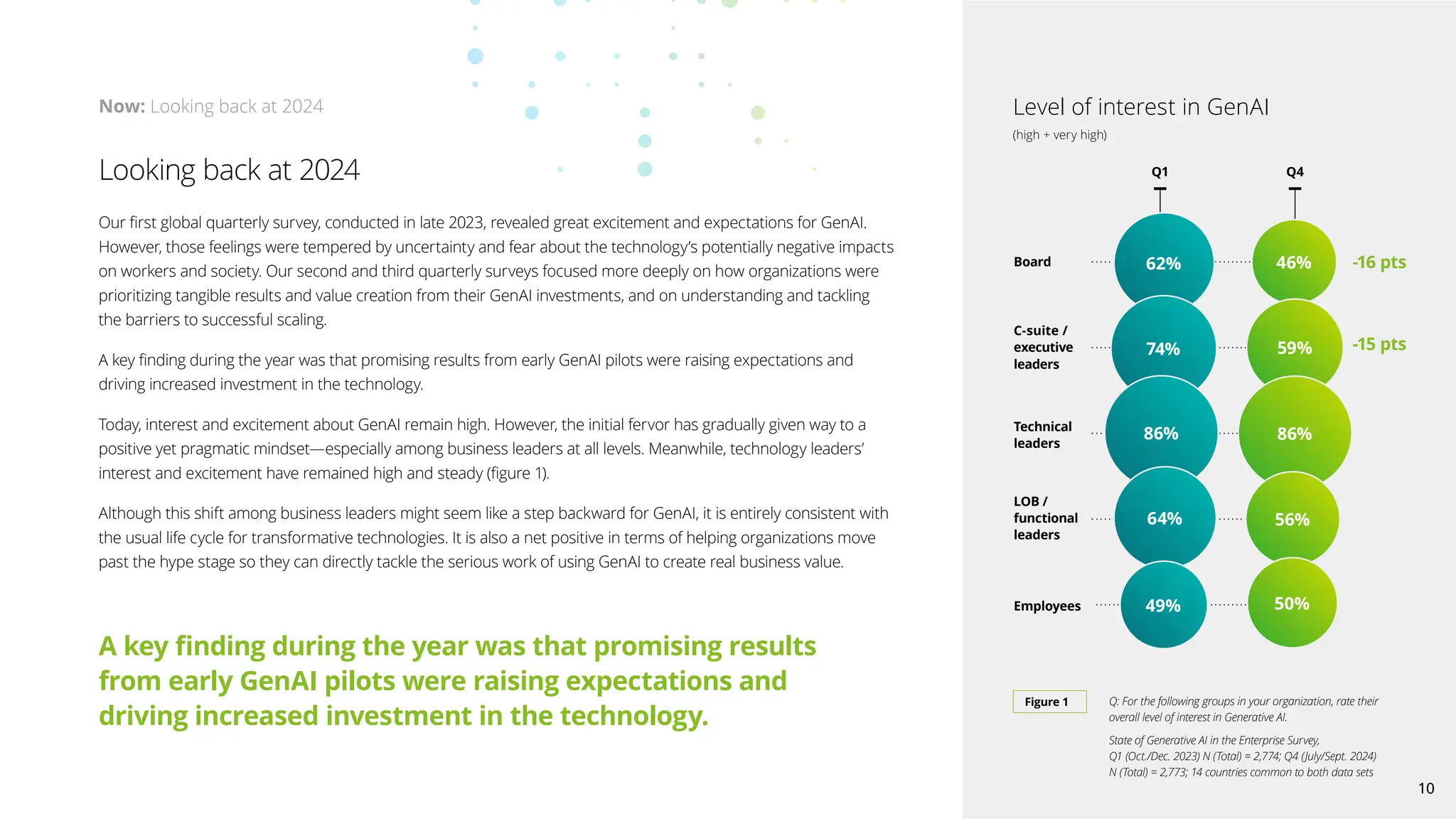

Our first globalquarterly survey, conducted in late 2023, revealed great excitement and expectations for GenAI.

However, those feelings were tempered by uncertainty and fear about the technology’s potentially negative impacts

on workers and society. Our second and third quarterly surveys focused more deeply on how organizations were

prioritizing tangible results and value creation from their GenAI investments, and on understanding and tackling

the barriers to successful scaling.

A key finding during the year was that promising results from early GenAI pilots were raising expectations and

driving increased investment in the technology.

Today, interest and excitement about GenAI remain high. However, the initial fervor has gradually given way to a

positive yet pragmatic mindset—especially among business leaders at all levels. Meanwhile, technology leaders’

interest and excitement have remained high and steady (figure 1).

Although this shift among business leaders might seem like a step backward for GenAI, it is entirely consistent with

the usual life cycle for transformative technologies. It is also a net positive in terms of helping organizations move

past the hype stage so they can directly tackle the serious work of using GenAI to create real business value.

Looking back at 2024

Now: Looking back at 2024

Figure 1 Q: For the following groups in your organization, rate their

overall level of interest in Generative AI.

State of Generative AI in the Enterprise Survey,

Q1 (Oct./Dec. 2023) N (Total) = 2,774; Q4 (July/Sept. 2024)

N (Total) = 2,773; 14 countries common to both data sets

Level of interest in GenAI

(high + very high)

Q1 Q4

Board

C-suite /

executive

leaders

Technical

leaders

LOB /

functional

leaders

Employees

62%

74%

86%

64%

49%

46%

59%

86%

56%

50%

A key finding during the year was that promising results

from early GenAI pilots were raising expectations and

driving increased investment in the technology.

-16 pts

-15 pts

10

10

11.

Over the pastyear, as organizations gained experience with GenAI, they began to better

understand both the rewards and challenges of deploying the technology at scale—

and adjusted their plans and expectations accordingly. Budgets have risen, and the

need for C-suites and boards to spur their organizations into action has diminished.

At the same time, the need for disciplined action has grown. Technical preparedness

has improved, while regulatory uncertainty and risk management have become bigger

barriers to progress. Talent and workforce issues remain important; however, access to

specialized technical talent no longer seems to be the dire emergency it once was, at least

in comparison to other priorities. There has been one constant, however: improved data

management continues to be a top priority, even for companies that live and breathe data.

“Data emerged as the central factor for [our GenAI] success,” said a former software

engineering manager for one of the world’s leading technology companies. “While

the models and computing power existed, accessing the right data proved to be the

biggest bottleneck. To address this, the company implemented a centralized data

strategy, managed by a single data leader, to streamline data acquisition and minimize

redundancy—enabling faster model development.”

Now: Looking back at 2024

“Data emerged as the central

factor for [our GenAI] success …”

— Former software engineering manager for leading technology company

11

12.

From a technologyperspective, the capabilities of

foundation models and applications have improved

dramatically over the past year. There are smaller, more

efficient models; better latency; bigger access windows;

expanded modalities; greater autonomy; and increased

model specialization.

Reliability and trust have improved as well, although both

still have a long way to go. Meanwhile, the adoption rate

for customized, open-source and/or proprietary large

language models (LLMs) remains limited at 20%–25% of

those surveyed.

Over the past year, respondents reported they

believe their organizations have most improved their

GenAI preparedness in the critical areas of technology

infrastructure (+7 points) and strategy (+5 points). However,

preparedness has seemingly not improved in the other

critical areas of risk and governance and talent.

The vast majority of respondents (78%) reported they

expect to increase their overall AI spending in the next

fiscal year, with GenAI mostly expanding its share of

the overall AI budget relative to our first-quarter survey

results. In particular, the percentage of organizations

investing 20%–39% of their overall AI budget on

GenAI climbed by 12 points, while the percentage of

organizations investing less than 20% of their AI budget

on GenAI fell by 6 points.

“The way we do business has not changed,” said the VP of

artificial intelligence at a major media and entertainment

company. “For every project, our objective is always to do

something that has a positive impact on the business. This

has not changed and is not going to change because it’s

what makes sense. However, a large proportion of project

proposals now have a [GenAI] component to them.”

Now: Looking back at 2024

78% of respondents expect to increase their overall AI spending

in the next fiscal year.

12

13.

Relative to otherrespondents, the C-suite leaders (CxOs) in our survey generally demonstrated higher levels

of excitement and optimism about their organizations’ GenAI implementations. For example, 21% of C-suite

survey respondents reported they feel GenAI is already transforming their organization, compared to only 8%

of non-C-suite respondents. C-suite executives surveyed are comparatively less worried about barriers such

as trust, risk management, governance and regulatory compliance. They also have a rosier view of how quickly

their organization is moving, and how quickly the barriers to scaling and value creation will be addressed.

Sixty percent of non-C-suite respondents believe it will take 12 months or more to overcome scaling barriers,

compared to only 47% of C-suite respondents.

This doesn’t necessarily mean CxOs are out of touch with the challenges of adopting and deploying GenAI.

It could be they are still playing the primary role of catalyst or cheerleader and are in the process of learning

what it really takes to implement and scale GenAI. What will be important going forward is for CxOs to direct

that enthusiasm to removing barriers and enabling scaling.

Now that GenAI in the enterprise is moving past its infancy, CxOs should take on new roles, including those

of guide, counselor and challenger. Chief executive officers should show top-down support for GenAI, be the

champions for governance and risk initiatives, and foster an environment of trust and transparency. Chief

information officers, chief technology officers and chief data officers should sharpen their focus on identifying and

overcoming the barriers to large-scale GenAI deployment within their domains. Chief financial officers should

ensure responsible spending without stifling innovation. And chief human resource officers should promote

training, reskilling and other human capital investments.

View from the C-suite

Now: Looking back at 2024

13

14.

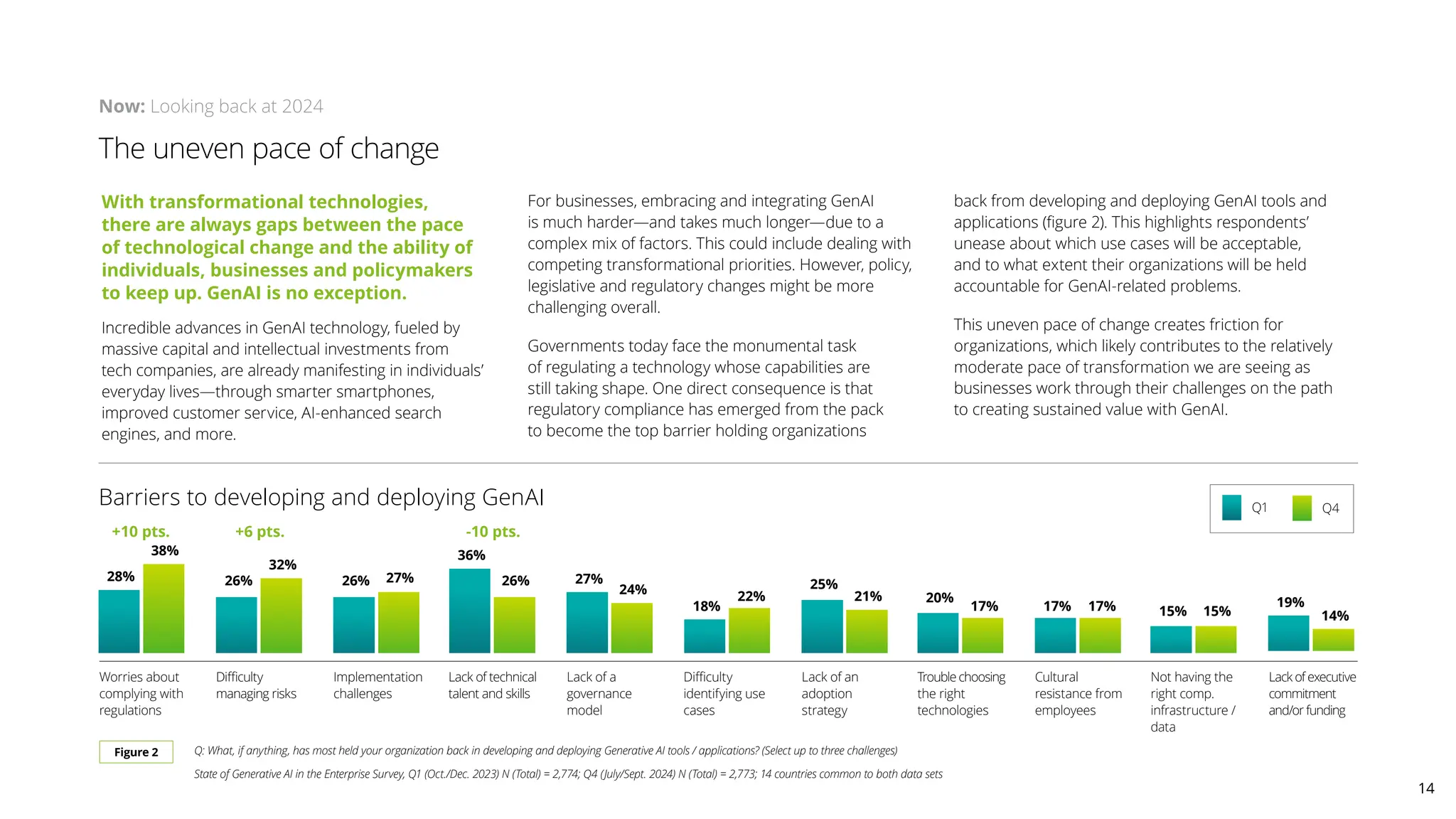

The uneven paceof change

With transformational technologies,

there are always gaps between the pace

of technological change and the ability of

individuals, businesses and policymakers

to keep up. GenAI is no exception.

Incredible advances in GenAI technology, fueled by

massive capital and intellectual investments from

tech companies, are already manifesting in individuals’

everyday lives—through smarter smartphones,

improved customer service, AI-enhanced search

engines, and more.

For businesses, embracing and integrating GenAI

is much harder—and takes much longer—due to a

complex mix of factors. This could include dealing with

competing transformational priorities. However, policy,

legislative and regulatory changes might be more

challenging overall.

Governments today face the monumental task

of regulating a technology whose capabilities are

still taking shape. One direct consequence is that

regulatory compliance has emerged from the pack

to become the top barrier holding organizations

back from developing and deploying GenAI tools and

applications (figure 2). This highlights respondents’

unease about which use cases will be acceptable,

and to what extent their organizations will be held

accountable for GenAI-related problems.

This uneven pace of change creates friction for

organizations, which likely contributes to the relatively

moderate pace of transformation we are seeing as

businesses work through their challenges on the path

to creating sustained value with GenAI.

Now: Looking back at 2024

Barriers to developing and deploying GenAI

Q: What, if anything, has most held your organization back in developing and deploying Generative AI tools / applications? (Select up to three challenges)

State of Generative AI in the Enterprise Survey, Q1 (Oct./Dec. 2023) N (Total) = 2,774; Q4 (July/Sept. 2024) N (Total) = 2,773; 14 countries common to both data sets

Figure 2

Worries about

complying with

regulations

Difficulty

managing risks

Lack of an

adoption

strategy

Difficulty

identifying use

cases

Trouble choosing

the right

technologies

Implementation

challenges

Lack of technical

talent and skills

Lack of a

governance

model

Cultural

resistance from

employees

28%

Not having the

right comp.

infrastructure /

data

Lack of executive

commitment

and/or funding

38%

26%

32%

26% 27%

36%

26% 27%

24%

18%

22%

25%

21% 20%

17% 17% 17% 15% 15%

19%

14%

Q1 Q4

+10 pts. +6 pts. -10 pts.

14

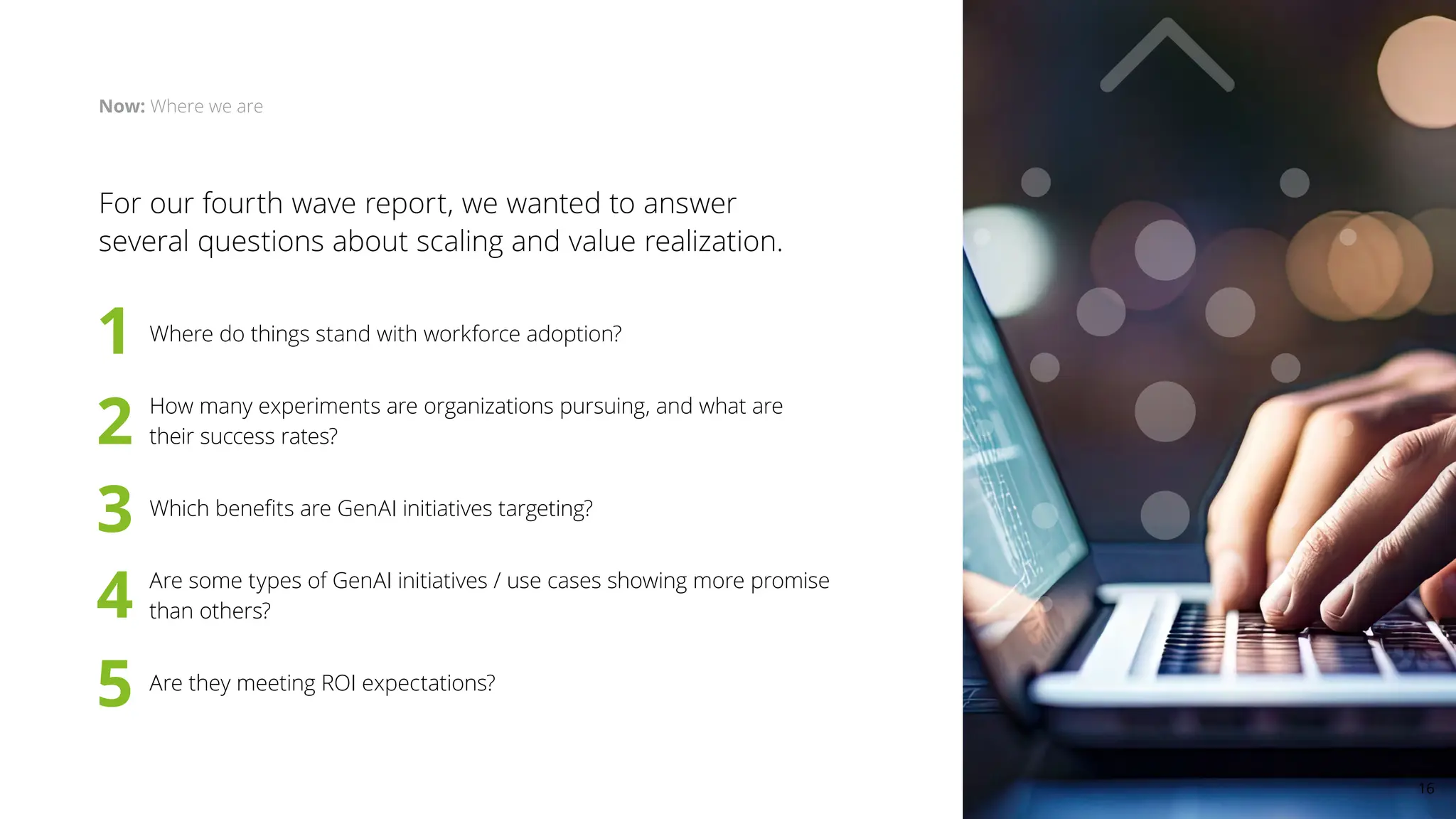

For our fourthwave report, we wanted to answer

several questions about scaling and value realization.

Where do things stand with workforce adoption?

How many experiments are organizations pursuing, and what are

their success rates?

Which benefits are GenAI initiatives targeting?

Are some types of GenAI initiatives / use cases showing more promise

than others?

Are they meeting ROI expectations?

Now: Where we are

1

2

3

4

5

16

17.

Where do thingsstand with workforce adoption?

Now: Where we are

1 Our latest survey results show that access to GenAI is still largely limited to less than

40% of the workforce. Also, for most organizations, fewer than 60% of workers who

have access to GenAI actually use it on a daily basis. This suggests many companies

have yet to integrate GenAI into their standard business workflows. It also raises the

chicken-and-egg question of whether limited access to GenAI is inhibiting comfort and

uptake with the technology (and stifling innovation), or whether the lack of high-value,

innovative use cases is limiting interest and adoption.

For GenAI to become truly transformational, it will likely require greater numbers of

workers experimenting and leveraging the technology to identify new, high-impact use

cases within the business. “Within our organization, the demand for GenAI use cases

and innovation primarily comes from middle management and employees, rather than

being driven by the C-suite,” said the director of product management for GenAI, cloud

and data centers at a leading semiconductor company. “While the C-suite has been

slower to engage in AI implementation, teams across the company are developing

proofs-of-concept and driving AI adoption through internal boards and governance

structures. This bottom-up approach emphasizes improving workflows and test cases,

with leadership providing support as needed for broader integration.”

Of course, access alone does not equate success. Providing access to GenAI does

not mean workers will use it. Conversely, workers with a burning desire to use GenAI

will likely find a way to do so, with or without approval. However, in order to foster

transformation and maintain some level of control over how GenAI is used within the

enterprise, it generally makes sense to offer broad workforce access to sanctioned

GenAI tools, supported by clear guidelines for proper use.

“Currently, GenAI adoption is driven by internal demand, with early adopters seeking

to use the tools to meet their specific needs,” said the head of GenAI in product

management at a major technology company. “However, we expect a shift towards

push-driven adoption in the next year, where all business units will be required to

integrate the platform as it becomes an approved and proven tool. This shift will create

pressure for teams to leverage the technology or risk missing out on the benefits it offers.”

“

Currently, GenAI adoption is driven

by internal demand, with early

adopters seeking to use the tools to

meet their specific needs …”

—

Head of Generative AI, project management at major technology company

17

18.

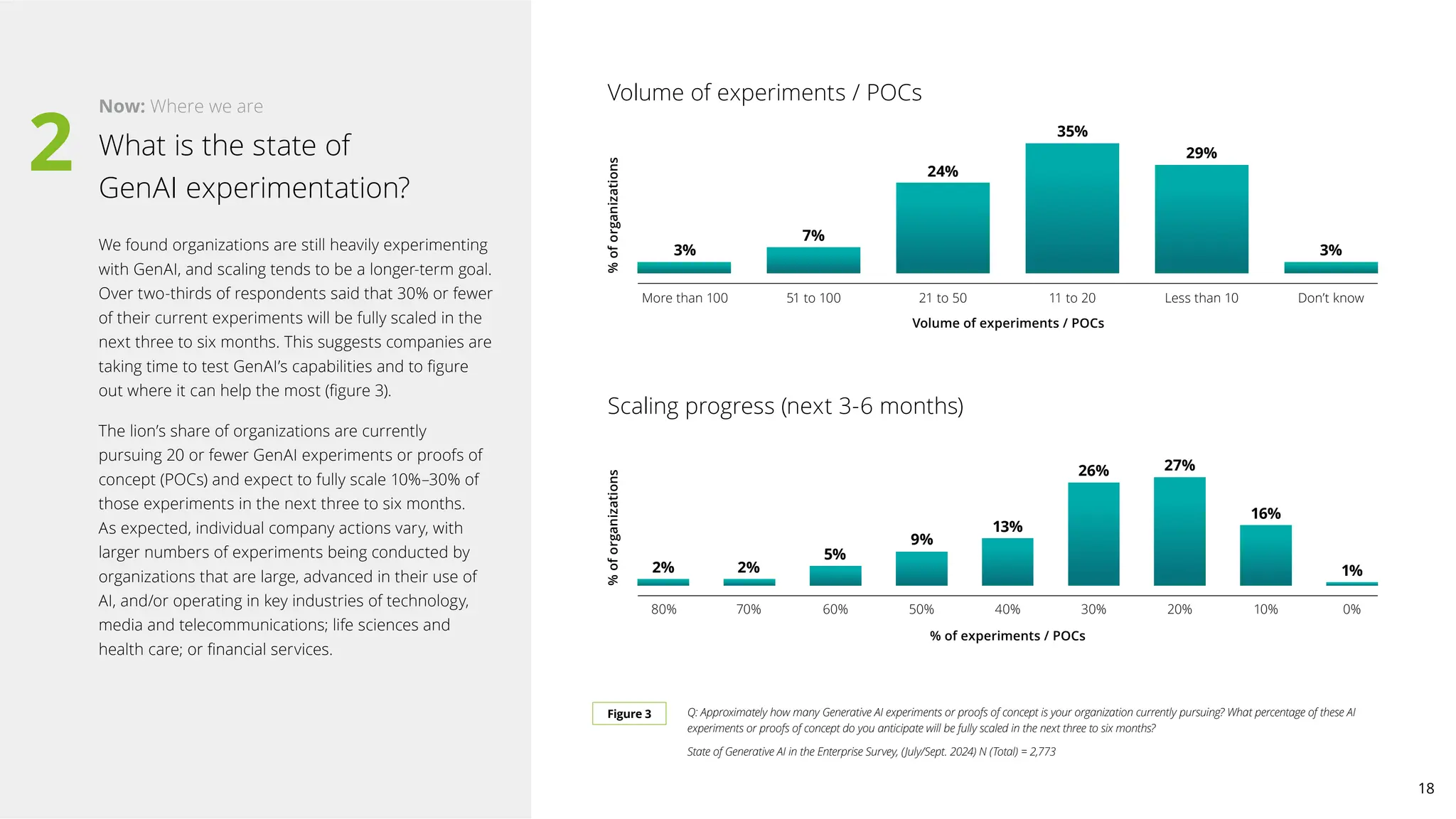

We found organizationsare still heavily experimenting

with GenAI, and scaling tends to be a longer-term goal.

Over two-thirds of respondents said that 30% or fewer

of their current experiments will be fully scaled in the

next three to six months. This suggests companies are

taking time to test GenAI’s capabilities and to figure

out where it can help the most (figure 3).

The lion’s share of organizations are currently

pursuing 20 or fewer GenAI experiments or proofs of

concept (POCs) and expect to fully scale 10%–30% of

those experiments in the next three to six months.

As expected, individual company actions vary, with

larger numbers of experiments being conducted by

organizations that are large, advanced in their use of

AI, and/or operating in key industries of technology,

media and telecommunications; life sciences and

health care; or financial services.

What is the state of

GenAI experimentation?

Q: Approximately how many Generative AI experiments or proofs of concept is your organization currently pursuing? What percentage of these AI

experiments or proofs of concept do you anticipate will be fully scaled in the next three to six months?

State of Generative AI in the Enterprise Survey, (July/Sept. 2024) N (Total) = 2,773

Figure 3

Now: Where we are

2

Volume of experiments / POCs

3%

More than 100 51 to 100 21 to 50 11 to 20 Less than 10 Don’t know

7%

35%

24%

29%

3%

Volume of experiments / POCs

%

of

organizations

Scaling progress (next 3-6 months)

2%

80%

2%

9%

5%

13%

26%

% of experiments / POCs

27%

16%

1%

%

of

organizations 70% 60% 50% 40% 30% 20% 10% 0%

18

19.

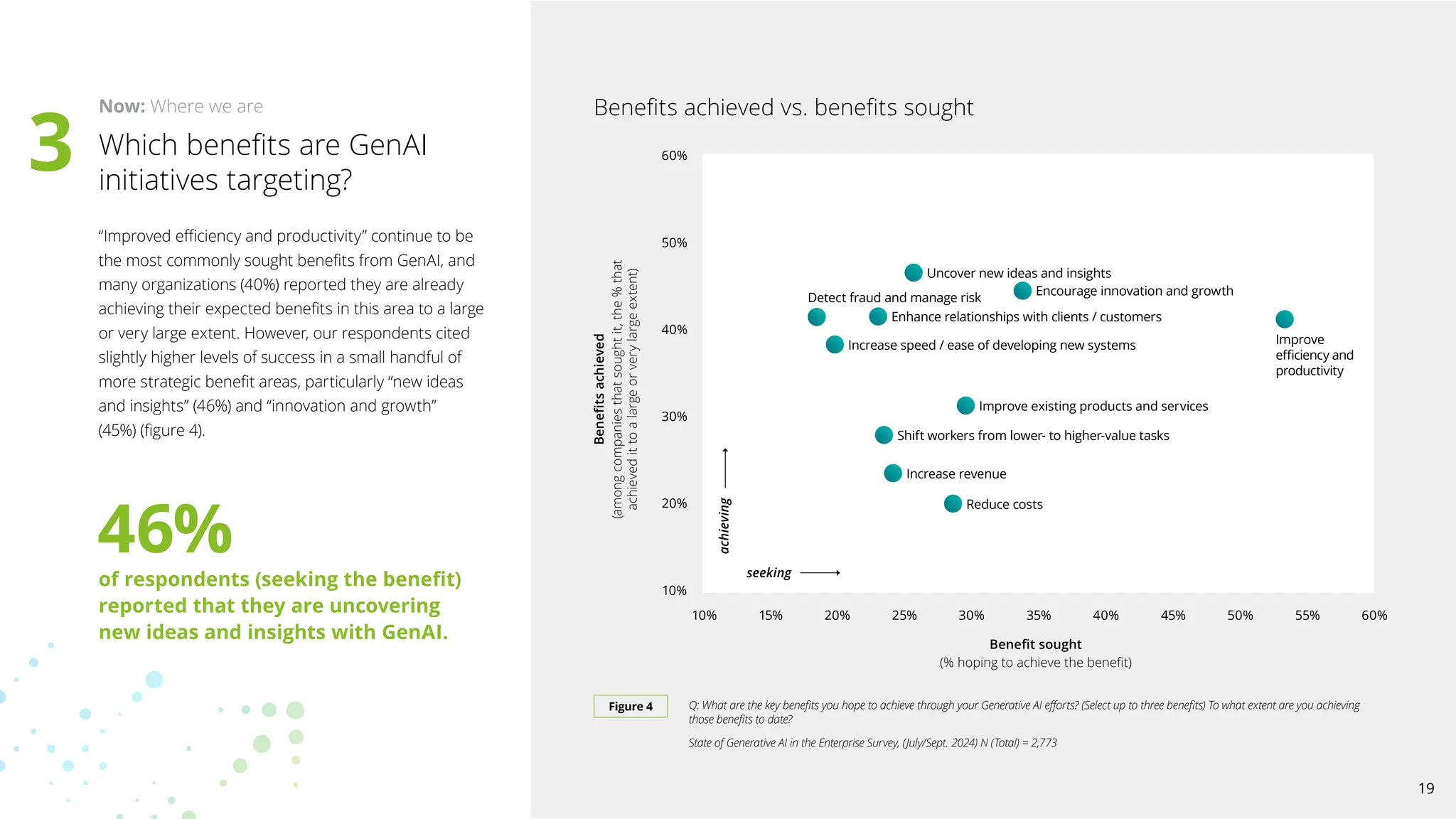

“Improved efficiency andproductivity” continue to be

the most commonly sought benefits from GenAI, and

many organizations (40%) reported they are already

achieving their expected benefits in this area to a large

or very large extent. However, our respondents cited

slightly higher levels of success in a small handful of

more strategic benefit areas, particularly “new ideas

and insights” (46%) and “innovation and growth”

(45%) (figure 4).

Which benefits are GenAI

initiatives targeting?

Now: Where we are

60%

50%

40%

30%

20%

10%

10% 15% 20% 25% 30% 35% 40% 45% 50% 55% 60%

Benefits

achieved

(among

companies

that

sought

it,

the

%

that

achieved

it

to

a

large

or

very

large

extent)

Benefit sought

(% hoping to achieve the benefit)

Q: What are the key benefits you hope to achieve through your Generative AI efforts? (Select up to three benefits) To what extent are you achieving

those benefits to date?

State of Generative AI in the Enterprise Survey, (July/Sept. 2024) N (Total) = 2,773

Figure 4

Benefits achieved vs. benefits sought

Detect fraud and manage risk

achieving

seeking

Increase speed / ease of developing new systems

Enhance relationships with clients / customers

Uncover new ideas and insights

Encourage innovation and growth

Improve

efficiency and

productivity

Improve existing products and services

Shift workers from lower- to higher-value tasks

Increase revenue

Reduce costs

3

46%

of respondents (seeking the benefit)

reported that they are uncovering

new ideas and insights with GenAI.

19

20.

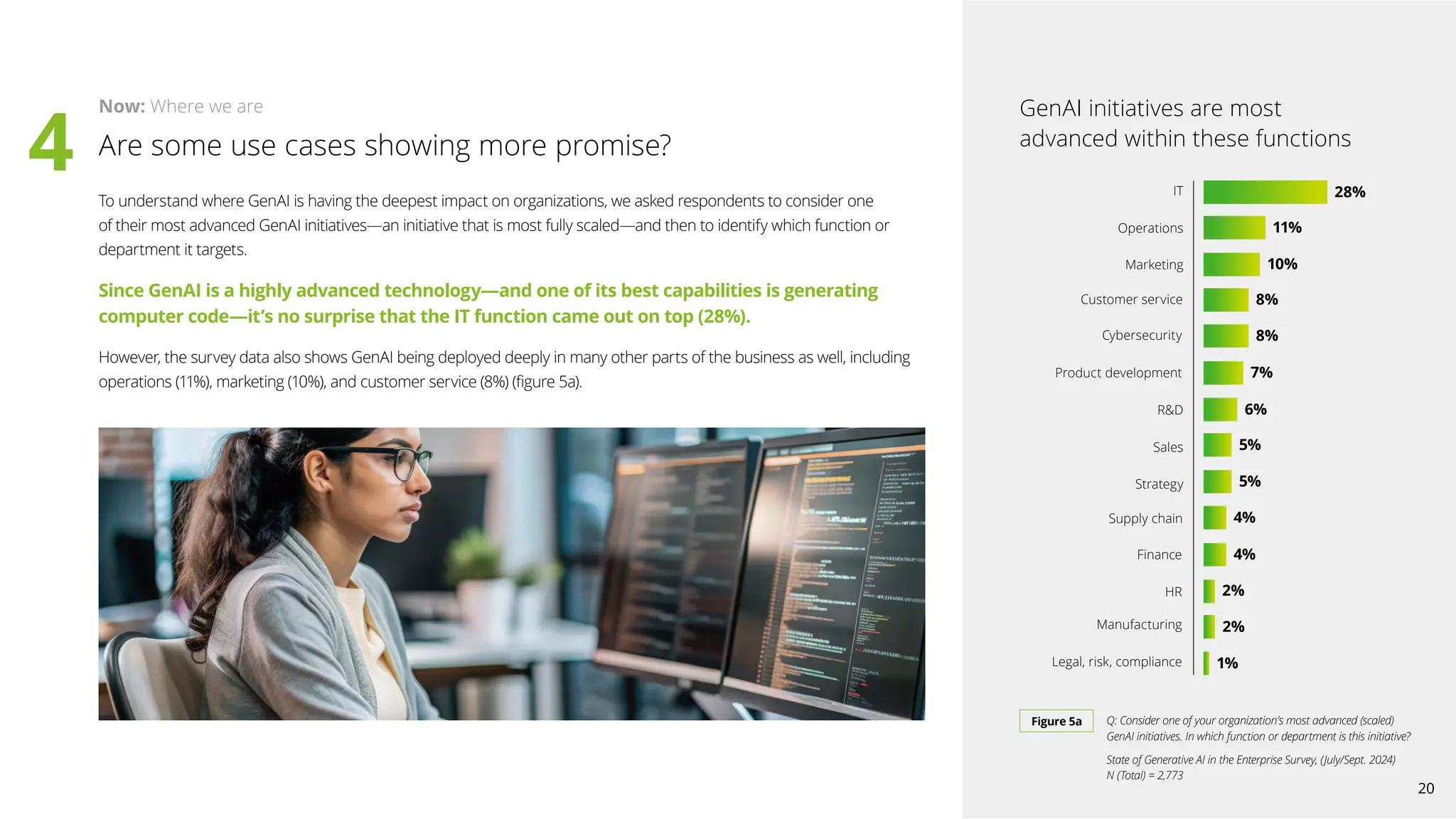

To understand whereGenAI is having the deepest impact on organizations, we asked respondents to consider one

of their most advanced GenAI initiatives—an initiative that is most fully scaled—and then to identify which function or

department it targets.

Since GenAI is a highly advanced technology—and one of its best capabilities is generating

computer code—it’s no surprise that the IT function came out on top (28%).

However, the survey data also shows GenAI being deployed deeply in many other parts of the business as well, including

operations (11%), marketing (10%), and customer service (8%) (figure 5a).

Figure 5a Q: Consider one of your organization’s most advanced (scaled)

GenAI initiatives. In which function or department is this initiative?

State of Generative AI in the Enterprise Survey, (July/Sept. 2024)

N (Total) = 2,773

GenAI initiatives are most

advanced within these functions

28%

IT

Operations

Marketing

Customer service

Cybersecurity

Product development

Are some use cases showing more promise?

Now: Where we are

RD

Sales

Strategy

Supply chain

Finance

HR

Manufacturing

Legal, risk, compliance

11%

8%

10%

8%

6%

7%

5%

4%

5%

4%

2%

2%

1%

4

20

21.

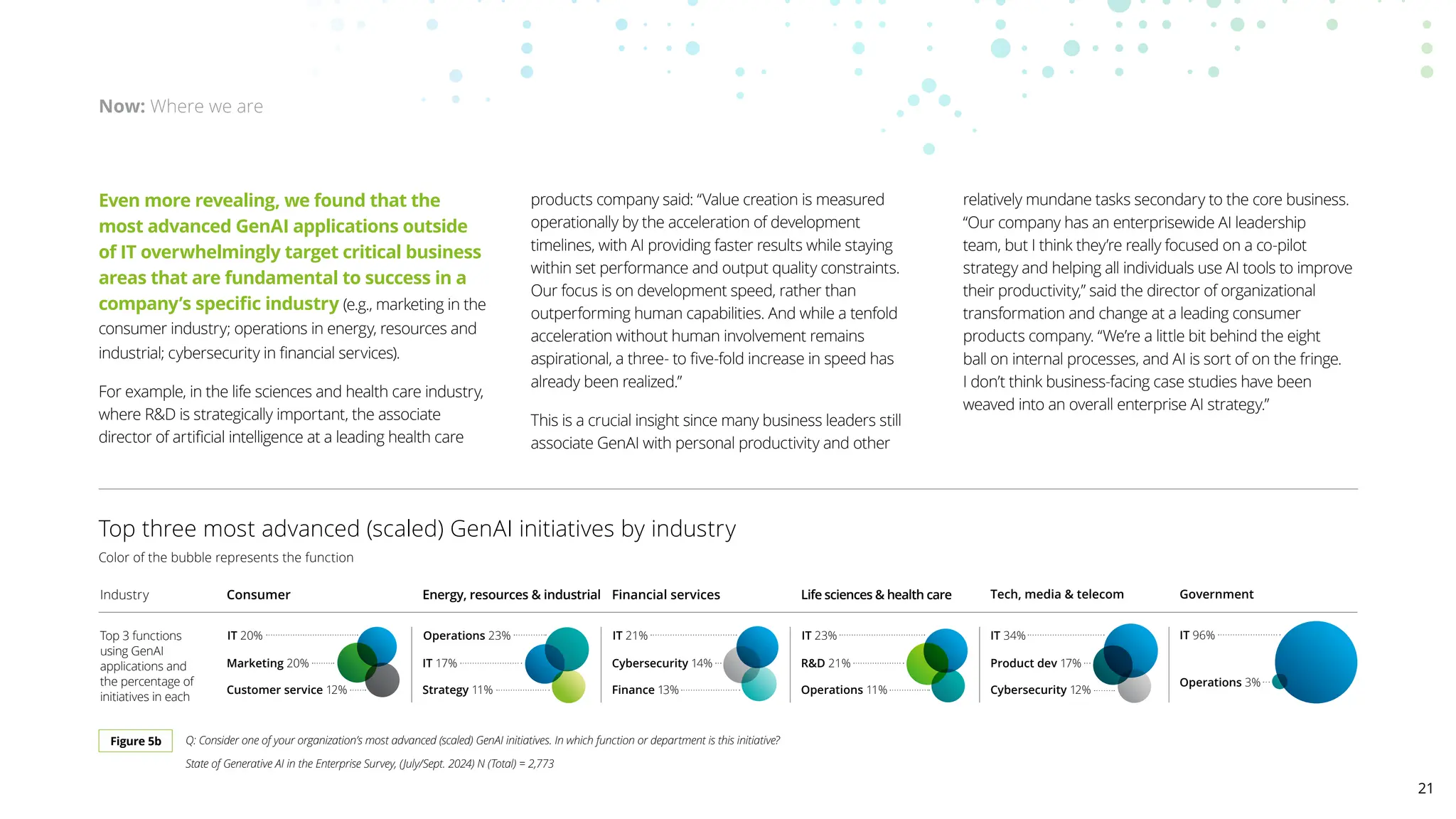

Even more revealing,we found that the

most advanced GenAI applications outside

of IT overwhelmingly target critical business

areas that are fundamental to success in a

company’s specific industry (e.g., marketing in the

consumer industry; operations in energy, resources and

industrial; cybersecurity in financial services).

For example, in the life sciences and health care industry,

where RD is strategically important, the associate

director of artificial intelligence at a leading health care

products company said: “Value creation is measured

operationally by the acceleration of development

timelines, with AI providing faster results while staying

within set performance and output quality constraints.

Our focus is on development speed, rather than

outperforming human capabilities. And while a tenfold

acceleration without human involvement remains

aspirational, a three- to five-fold increase in speed has

already been realized.”

This is a crucial insight since many business leaders still

associate GenAI with personal productivity and other

relatively mundane tasks secondary to the core business.

“Our company has an enterprisewide AI leadership

team, but I think they’re really focused on a co-pilot

strategy and helping all individuals use AI tools to improve

their productivity,” said the director of organizational

transformation and change at a leading consumer

products company. “We’re a little bit behind the eight

ball on internal processes, and AI is sort of on the fringe.

I don’t think business-facing case studies have been

weaved into an overall enterprise AI strategy.”

Now: Where we are

Top three most advanced (scaled) GenAI initiatives by industry

Color of the bubble represents the function

Tech, media telecom Government

IT 96%

Operations 3%

IT 34%

Product dev 17%

Cybersecurity 12%

IT 23%

RD 21%

Operations 11%

IT 21%

Cybersecurity 14%

Finance 13%

Operations 23%

IT 17%

Strategy 11%

IT 20%

Marketing 20%

Customer service 12%

Figure 5b Q: Consider one of your organization’s most advanced (scaled) GenAI initiatives. In which function or department is this initiative?

State of Generative AI in the Enterprise Survey, (July/Sept. 2024) N (Total) = 2,773

Industry

Top 3 functions

using GenAI

applications and

the percentage of

initiatives in each

Consumer Energy, resources industrial Financial services Life sciences health care

21

22.

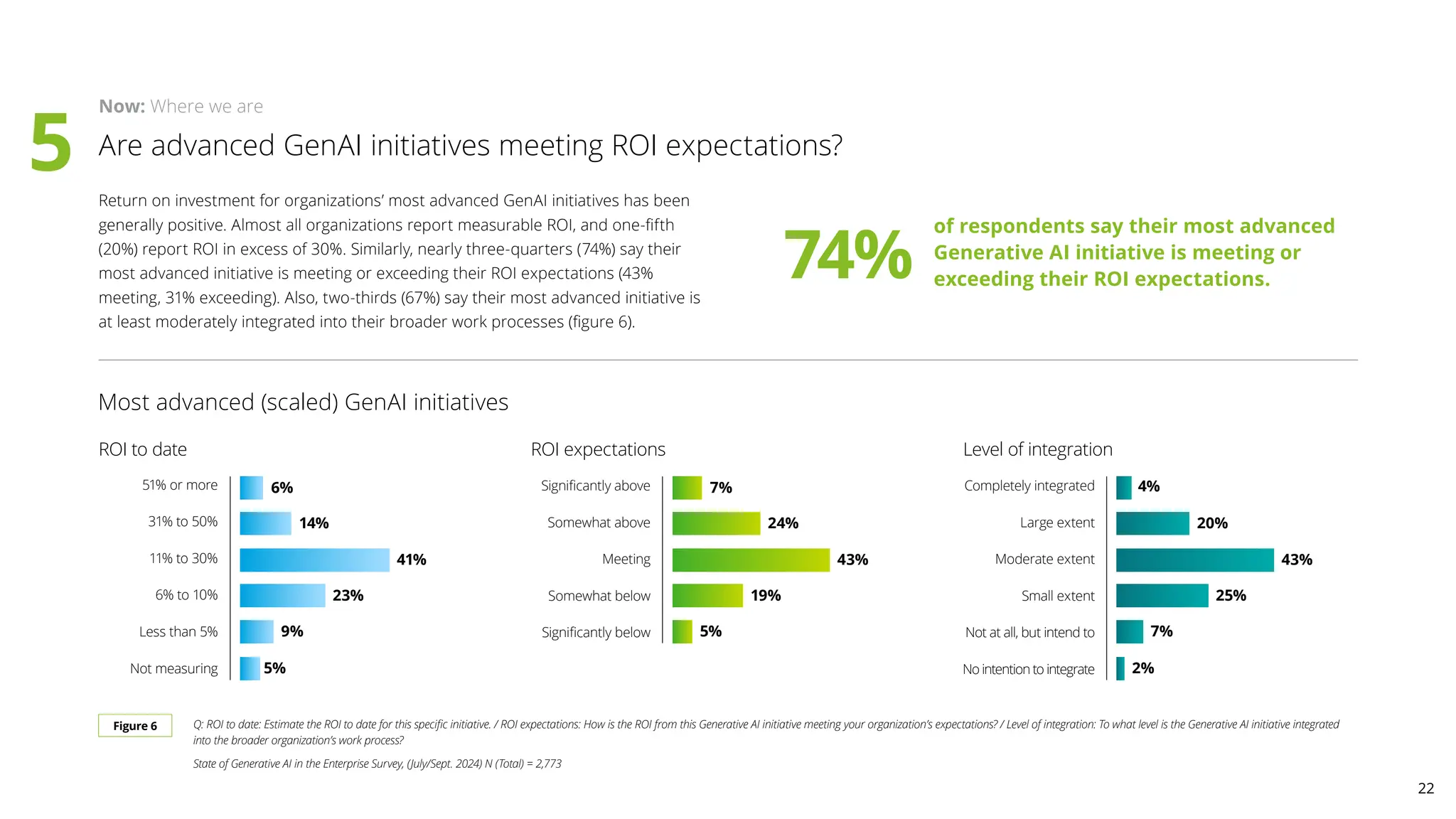

Are advanced GenAIinitiatives meeting ROI expectations?

Return on investment for organizations’ most advanced GenAI initiatives has been

generally positive. Almost all organizations report measurable ROI, and one-fifth

(20%) report ROI in excess of 30%. Similarly, nearly three-quarters (74%) say their

most advanced initiative is meeting or exceeding their ROI expectations (43%

meeting, 31% exceeding). Also, two-thirds (67%) say their most advanced initiative is

at least moderately integrated into their broader work processes (figure 6).

Figure 6

Most advanced (scaled) GenAI initiatives

Now: Where we are

51% or more

31% to 50%

11% to 30%

6% to 10%

Less than 5%

Not measuring

ROI to date

6%

14%

23%

41%

9%

5%

Significantly above

Somewhat above

Meeting

Somewhat below

Significantly below

ROI expectations

7%

24%

19%

43%

5%

Completely integrated

Large extent

Moderate extent

Small extent

Not at all, but intend to

No intention to integrate

Level of integration

4%

20%

25%

43%

7%

2%

Q: ROI to date: Estimate the ROI to date for this specific initiative. / ROI expectations: How is the ROI from this Generative AI initiative meeting your organization’s expectations? / Level of integration: To what level is the Generative AI initiative integrated

into the broader organization’s work process?

State of Generative AI in the Enterprise Survey, (July/Sept. 2024) N (Total) = 2,773

74%

of respondents say their most advanced

Generative AI initiative is meeting or

exceeding their ROI expectations.

5

22

23.

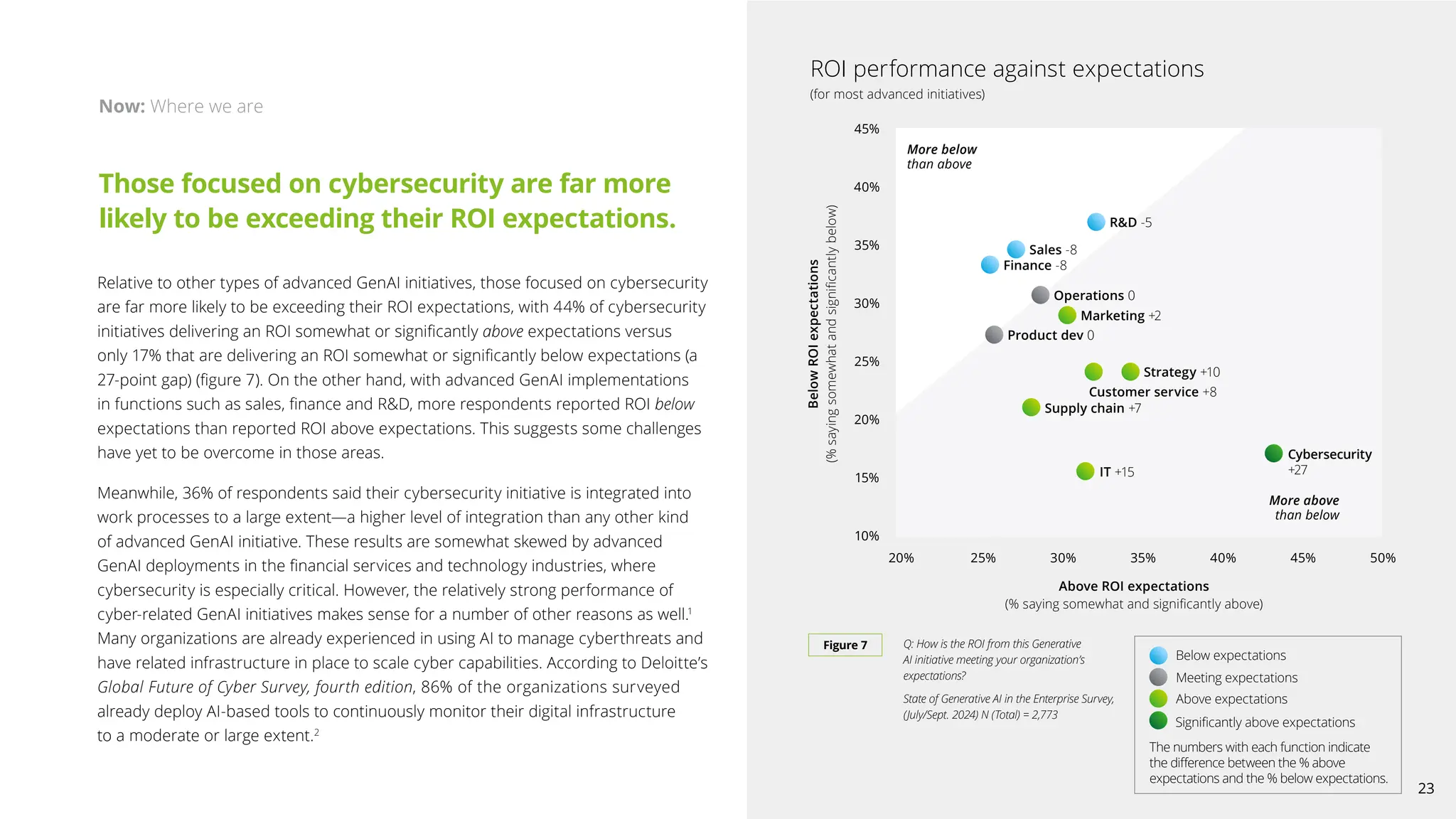

Relative to othertypes of advanced GenAI initiatives, those focused on cybersecurity

are far more likely to be exceeding their ROI expectations, with 44% of cybersecurity

initiatives delivering an ROI somewhat or significantly above expectations versus

only 17% that are delivering an ROI somewhat or significantly below expectations (a

27-point gap) (figure 7). On the other hand, with advanced GenAI implementations

in functions such as sales, finance and RD, more respondents reported ROI below

expectations than reported ROI above expectations. This suggests some challenges

have yet to be overcome in those areas.

Meanwhile, 36% of respondents said their cybersecurity initiative is integrated into

work processes to a large extent—a higher level of integration than any other kind

of advanced GenAI initiative. These results are somewhat skewed by advanced

GenAI deployments in the financial services and technology industries, where

cybersecurity is especially critical. However, the relatively strong performance of

cyber-related GenAI initiatives makes sense for a number of other reasons as well.1

Many organizations are already experienced in using AI to manage cyberthreats and

have related infrastructure in place to scale cyber capabilities. According to Deloitte’s

Global Future of Cyber Survey, fourth edition, 86% of the organizations surveyed

already deploy AI-based tools to continuously monitor their digital infrastructure

to a moderate or large extent.2

Now: Where we are

45%

40%

35%

30%

25%

20%

15%

10%

20% 25% 30% 35% 40% 45% 50%

Below

ROI

expectations

(%

saying

somewhat

and

significantly

below)

Above ROI expectations

(% saying somewhat and significantly above)

Q: How is the ROI from this Generative

AI initiative meeting your organization’s

expectations?

State of Generative AI in the Enterprise Survey,

(July/Sept. 2024) N (Total) = 2,773

Figure 7

ROI performance against expectations

(for most advanced initiatives)

RD -5

Operations 0

Sales -8

Finance -8

More below

than above

More above

than below

Product dev 0

Marketing +2

Strategy +10

Customer service +8

Supply chain +7

IT +15

Cybersecurity

+27

Those focused on cybersecurity are far more

likely to be exceeding their ROI expectations.

Meeting expectations

Significantly above expectations

Below expectations

Above expectations

The numbers with each function indicate

the difference between the % above

expectations and the % below expectations.

23

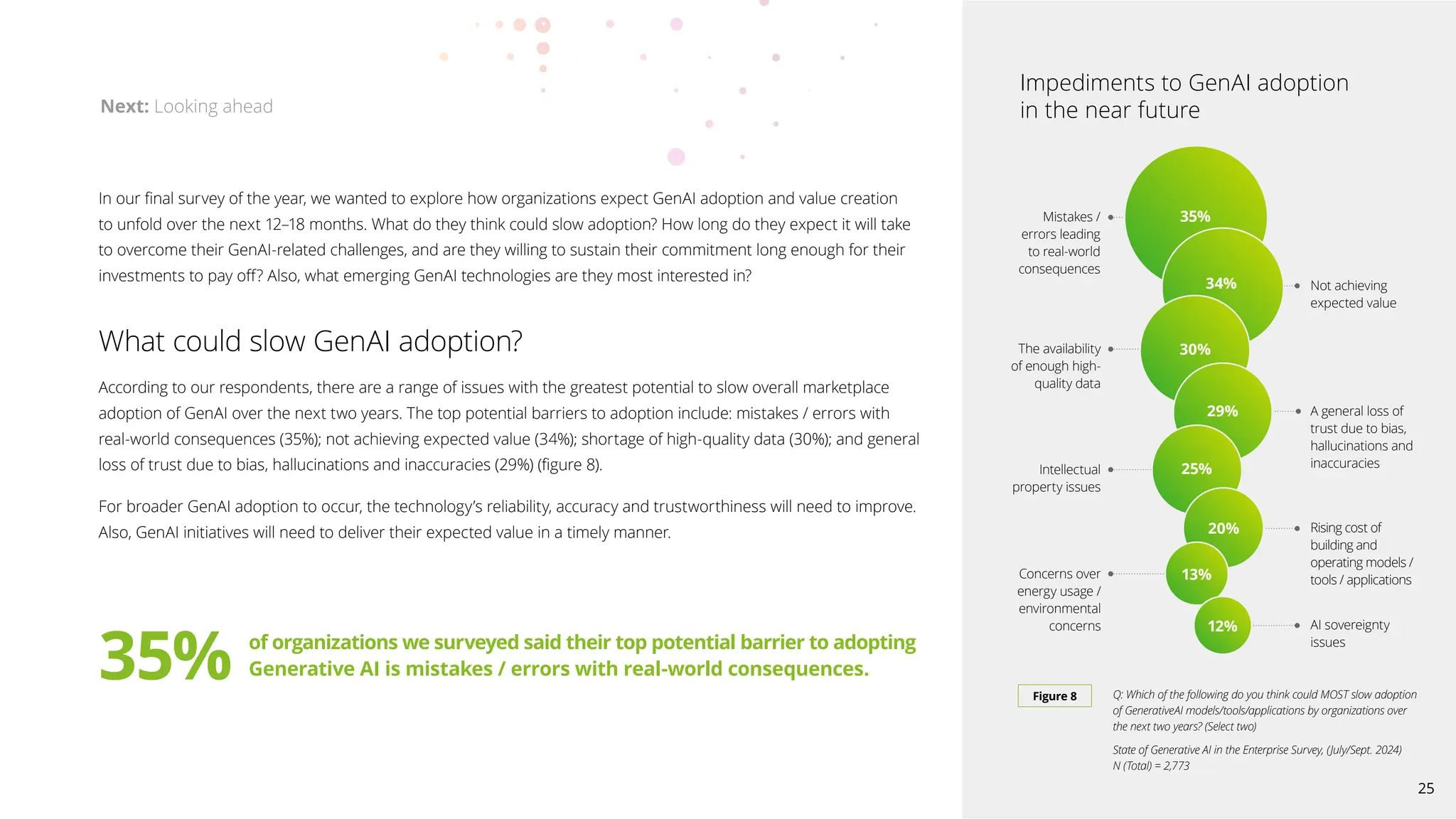

In our finalsurvey of the year, we wanted to explore how organizations expect GenAI adoption and value creation

to unfold over the next 12–18 months. What do they think could slow adoption? How long do they expect it will take

to overcome their GenAI-related challenges, and are they willing to sustain their commitment long enough for their

investments to pay off? Also, what emerging GenAI technologies are they most interested in?

What could slow GenAI adoption?

According to our respondents, there are a range of issues with the greatest potential to slow overall marketplace

adoption of GenAI over the next two years. The top potential barriers to adoption include: mistakes / errors with

real-world consequences (35%); not achieving expected value (34%); shortage of high-quality data (30%); and general

loss of trust due to bias, hallucinations and inaccuracies (29%) (figure 8).

For broader GenAI adoption to occur, the technology’s reliability, accuracy and trustworthiness will need to improve.

Also, GenAI initiatives will need to deliver their expected value in a timely manner.

Next: Looking ahead

Q: Which of the following do you think could MOST slow adoption

of GenerativeAI models/tools/applications by organizations over

the next two years? (Select two)

State of Generative AI in the Enterprise Survey, (July/Sept. 2024)

N (Total) = 2,773

Figure 8

Impediments to GenAI adoption

in the near future

35%

Mistakes /

errors leading

to real-world

consequences

Not achieving

expected value

The availability

of enough high-

quality data

A general loss of

trust due to bias,

hallucinations and

inaccuracies

Intellectual

property issues

34%

30%

29%

25%

Concerns over

energy usage /

environmental

concerns

Rising cost of

building and

operating models /

tools / applications

20%

13%

AI sovereignty

issues

12%

35% of organizations we surveyed said their top potential barrier to adopting

Generative AI is mistakes / errors with real-world consequences.

25

26.

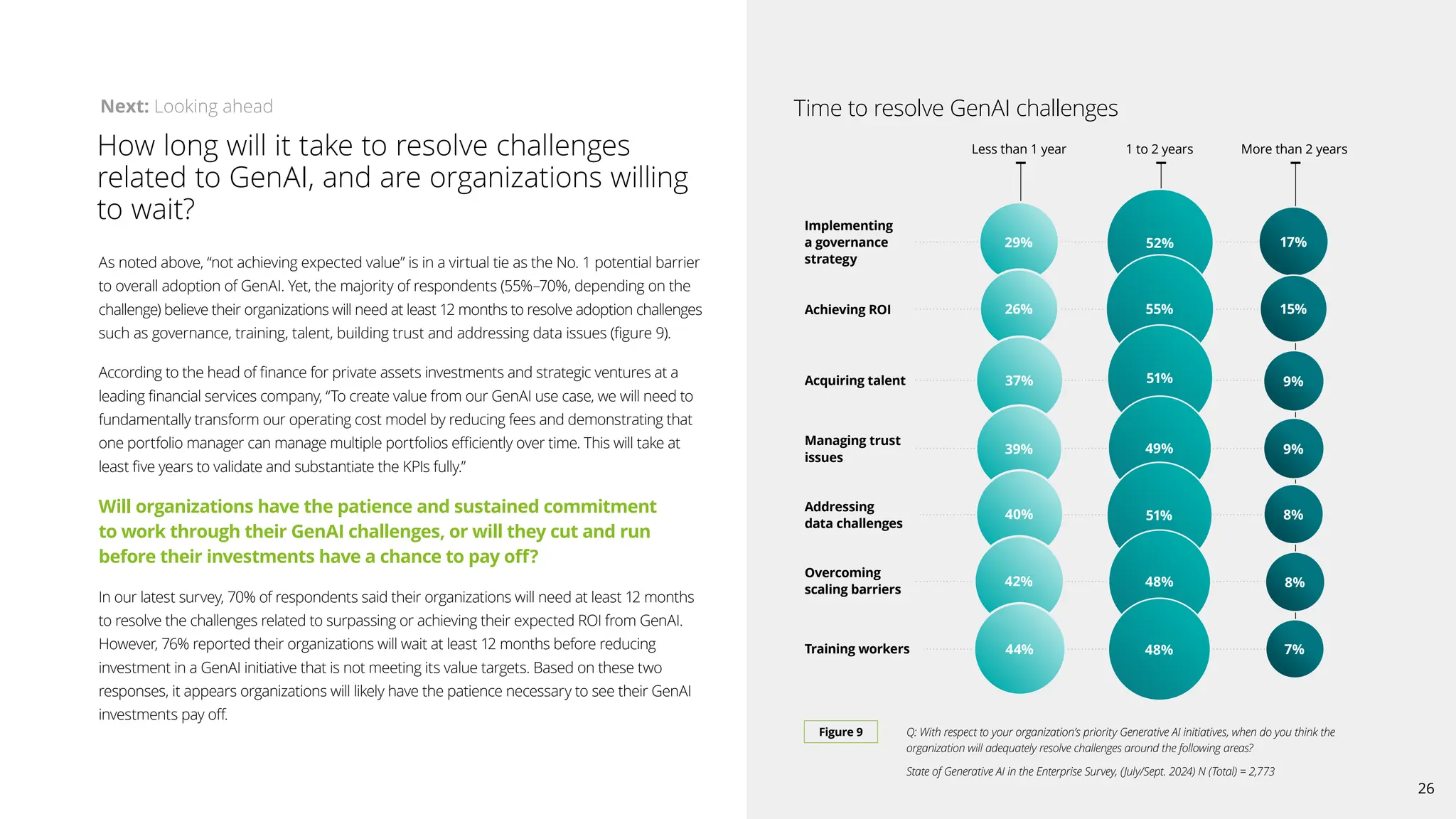

As noted above,“not achieving expected value” is in a virtual tie as the No. 1 potential barrier

to overall adoption of GenAI. Yet, the majority of respondents (55%–70%, depending on the

challenge) believe their organizations will need at least 12 months to resolve adoption challenges

such as governance, training, talent, building trust and addressing data issues (figure 9).

According to the head of finance for private assets investments and strategic ventures at a

leading financial services company, “To create value from our GenAI use case, we will need to

fundamentally transform our operating cost model by reducing fees and demonstrating that

one portfolio manager can manage multiple portfolios efficiently over time. This will take at

least five years to validate and substantiate the KPIs fully.”

Will organizations have the patience and sustained commitment

to work through their GenAI challenges, or will they cut and run

before their investments have a chance to pay off?

In our latest survey, 70% of respondents said their organizations will need at least 12 months

to resolve the challenges related to surpassing or achieving their expected ROI from GenAI.

However, 76% reported their organizations will wait at least 12 months before reducing

investment in a GenAI initiative that is not meeting its value targets. Based on these two

responses, it appears organizations will likely have the patience necessary to see their GenAI

investments pay off.

How long will it take to resolve challenges

related to GenAI, and are organizations willing

to wait?

Time to resolve GenAI challenges

Less than 1 year 1 to 2 years

Figure 9 Q: With respect to your organization’s priority Generative AI initiatives, when do you think the

organization will adequately resolve challenges around the following areas?

State of Generative AI in the Enterprise Survey, (July/Sept. 2024) N (Total) = 2,773

More than 2 years

Implementing

a governance

strategy

29% 52% 17%

Achieving ROI 26% 55% 15%

Acquiring talent 37% 51% 9%

39% 49% 9%

Addressing

data challenges

40% 51%

Overcoming

scaling barriers

42% 48%

Training workers 44% 48%

Next: Looking ahead

8%

8%

7%

Managing trust

issues

26

27.

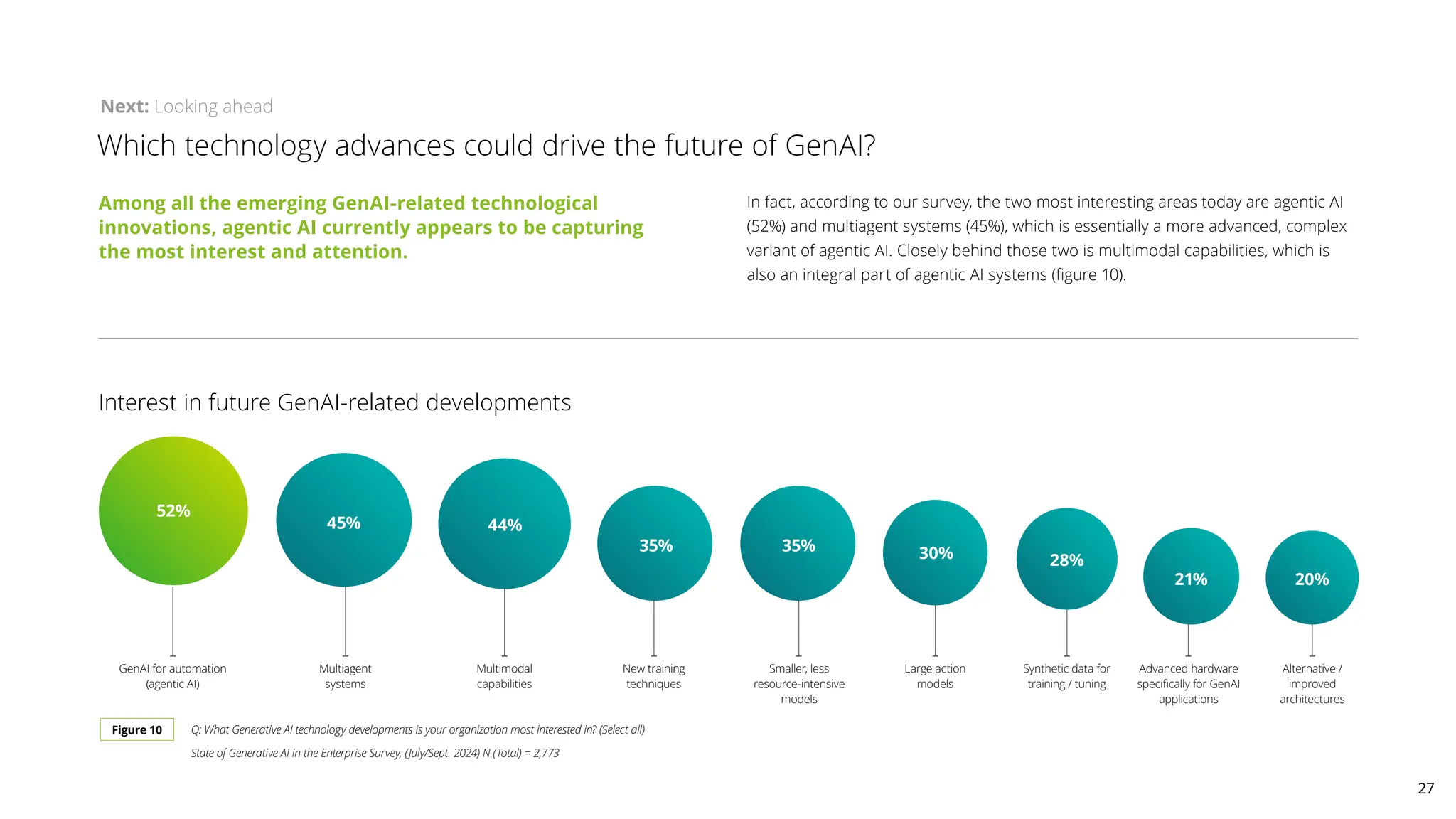

Among all theemerging GenAI-related technological

innovations, agentic AI currently appears to be capturing

the most interest and attention.

In fact, according to our survey, the two most interesting areas today are agentic AI

(52%) and multiagent systems (45%), which is essentially a more advanced, complex

variant of agentic AI. Closely behind those two is multimodal capabilities, which is

also an integral part of agentic AI systems (figure 10).

Interest in future GenAI-related developments

Figure 10 Q: What Generative AI technology developments is your organization most interested in? (Select all)

State of Generative AI in the Enterprise Survey, (July/Sept. 2024) N (Total) = 2,773

52%

GenAI for automation

(agentic AI)

45%

Multiagent

systems

Synthetic data for

training / tuning

Large action

models

Advanced hardware

specifically for GenAI

applications

44%

Multimodal

capabilities

New training

techniques

35%

Smaller, less

resource-intensive

models

35% 30%

Alternative /

improved

architectures

28%

21%

Next: Looking ahead

Which technology advances could drive the future of GenAI?

20%

27

28.

AI agents aresoftware systems that can complete complex tasks and meet objectives

with little or no human intervention. They are called “agents” because they have the

agency to act independently, planning and executing actions to achieve a specified goal.3

The vision for agentic AI is that autonomous AI agents will be able to execute assigned

tasks consistently and reliably by acquiring and processing multimodal data, using various

tools to complete tasks, and coordinating with other AI agents—all while remembering

what they’ve done in the past and learning from their experience.

“In the next phase of GenAI, we envision the development of specialized AI agents

tailored to specific functions, like sales research, to manage the overwhelming volume

of data,” said the director of product management for GenAI, cloud and data centers at

a leading high-tech manufacturing company. “These agents will streamline processes,

helping sales teams gather critical information quickly—without the need for extensive

manual research. Multiagent workflows are a future possibility; however, we anticipate

starting with single-agent solutions that can mature and scale efficiently, focusing on ROI

as they evolve into production.”

Agentic AI is the next logical step for GenAI, giving GenAI-based

systems access to more types of information and increasing AI’s

level of responsibility and autonomy.

In fact, 26% of our survey respondents said their organizations were already exploring

autonomous agent development to a large or very large extent. However, as with

current GenAI systems, agentic AI is not a silver bullet for everything a company needs

to get done. The key barriers currently facing GenAI—such as regulatory uncertainty,

inadequate risk management, data deficiencies, and workforce / talent issues—still apply

and are arguably even more important and challenging due to the increased complexity

of agentic AI systems.

Next: Looking ahead

“

In the next phase of GenAI, we envision the development of specialized AI agents tailored to

specific functions, like sales research, to manage the overwhelming volume of data.”

—

Director of product management for GenAI, cloud and data centers at a leading high-tech manufacturing company

28

Initially, senior executivesacted as catalysts and drivers for GenAI adoption

in their organizations. However, with strategies set, funding approved and

guidance given, many are now expecting GenAI to deliver significant and timely

improvements in efficiency, productivity, innovation and competitive advantage.

As such, C-suite leaders (CxOs) today should think about how to redefine their

roles around GenAI—and how to best lead their organizations forward.

There are three main ways CxOs can aid in this preparation. First, they must

ensure the organization stays aligned. Technical and business executives

should be involved in each other’s conversations and decisions, making

sure GenAI is appropriately represented. Second, CxOs must manage

organizational expectations. Leaders at the most senior level tend to be

more optimistic than those below them when it comes to the organization’s

rate of progress with GenAI (and ability to overcome obstacles). The GenAI

journey is long, and C-suite leaders need to be realistic about time horizons

for project success and organizational transformation. Third, CxOs must

show patience in the face of uncertainty—providing a steady hand and

sustained commitment to achieving long-term transformation across

multiple business areas.

Task the C-suite with creating alignment

and managing expectations

Next: Considerations

30

31.

GenAI initiatives arealready delivering significant enterprise value, including improved

efficiency, relationships and innovation. However, our survey results show that measurable

ROI varies widely for different use cases and functions. Some initiatives are already

exceeding expectations, but others are currently falling short. The bridge to sustained ROI

can only be built by establishing the right holistic strategies, building platform capabilities,

being realistic about targets and timelines, and taking some risks.

In our case studies, we found that focusing on a small number of high-impact use cases in

proven areas can accelerate ROI, as can layering GenAI on top of existing processes. Additionally,

centralized governance can pave the way for smoother adoption and employee buy-in, which

tends to yield better results and improves scalability. Finally, continuous iteration based on user

feedback and real-world performance can help ensure sustained value creation.

Ultimately, organizations need to move beyond isolated initiatives and integrate GenAI

into increasingly sophisticated and interconnected processes, evolving toward cognitive

systems with advanced reasoning capabilities. The goal should be to fundamentally

reinvent business processes.

Build bridges to sustained ROI Prioritize your workforce and prepare it for disruption

According to our survey results, the number of organizations that feel prepared for GenAI

from a talent perspective is still quite low and hasn’t changed much since the beginning of

2024. Also, workforce access to GenAI tools is still somewhat limited and daily use remains

low. These results all shine a spotlight on the need for organizations to do more to prepare

their workers for potential disruption from GenAI.

Although organizations have many priorities and barriers to focus on, they can’t overlook

talent issues if they want to achieve sustained growth and maximize ROI. Workers need

more GenAI access and experience—and they need it sooner rather than later.

Several of our case studies revealed organizational resistance to adopting GenAI solutions,

which slowed project timelines. Usually, the resistance stemmed from unfamiliarity with

the technologies and/or skill and technical gaps. Effective change management, including

education and training, was pivotal in overcoming the challenge. Without adequate

workforce buy-in and training, even the most powerful GenAI solutions can fail to deliver the

expected outcomes. Also, developing systems for continuous improvement is critical—with

users providing ongoing feedback on the quality and accuracy of GenAI solution outputs.

Next: Considerations

31

32.

With agentic AI,the question is not if, but when. Although the technology is still in its early

stages, it is evolving rapidly and will likely become increasingly capable over the next few

years. And while there are still many challenges to overcome—and technical complexities

to sort out—now is the time to start preparing.4

Organizational knowledge and experience

gained from GenAI implementations will help with the development and deployment of AI

agents. Also, the 13 elements of scaling mentioned in our prior GenAI reports will be just as

applicable to agentic AI.5

Organizations can begin by developing a strategic road map and assessing which tasks and

workflows are well-suited for agentic AI. Identify specific goals and desired value. Map out

the risks associated with autonomous agents and create mitigation plans. Start with low-risk

use cases that use noncritical data—with human oversight as a backup. These early steps

can help test and build the data management, cybersecurity and governance capabilities

necessary for safe agentic AI applications. Once your organization is comfortable, it can then

progress to applications that use more proprietary data, have access to more tools, and

operate more autonomously.

Start planning for GenAI agents Manage an uncertain future

GenAI’s present is filled with great promise, but its future holds many uncertainties. Will

investments pay off in the long term? Will bias, hallucinations, misinformation and “AI-

generated pollution” be controlled? Will GenAI use cases lead to new business models and

breakthrough innovations or just optimize existing operations? How fast will GenAI achieve

broad, human-level performance—if ever?

Although no one can answer these questions, one thing we know for sure is that all the

uncertainty surrounding GenAI is hindering its progress.

To act confidently and decisively in the face of this uncertainty, organizations should consider

boosting their efforts and capabilities in the areas of foresight, market sensing and scenario

planning.6

This will help leaders model plausible futures, identify potential blind spots in their

strategies, and make more informed decisions today.

The widespread transformation being driven by GenAI is truly an odyssey that will take place

over many years and have many phases. Building the right capabilities today will help your

organization make more informed strategic choices and position itself to capitalize on future

developments and opportunities.

Next: Considerations

32

GenAI is boostingsoftware security

in banking

In banking, robust cybersecurity and data governance are essential

to protect sensitive customer data, comply with complex regulatory

frameworks, and maintain public trust.

Case study 1:

Return to page 8

34

35.

We met withthe global head of GenAI, cloud and data privacy at a leading bank to explore

how GenAI is transforming secure software development in financial services. By analyzing

application vulnerability alerts and reducing false positives, GenAI enables engineers to focus

on critical issues, limit the number of actionable alerts and enhance operational efficiency.

Problem

On a typical day, the bank’s security team faces millions of alerts related to code-level

security issues, such as endpoint vulnerabilities and misconfigurations. Managing this

volume of alerts is both time intensive and yields false positives, leading to tension with

the application developers whose performance incentives are aligned with new feature

development rather than vulnerability remediation. “Previously, developers got frustrated

because 80% of their time was spent remediating vulnerabilities. Their performance is

measured by how many new features they deliver, not how many vulnerabilities they fix in

their code,” said the leader we interviewed.

Solution

The bank’s solution aimed to improve the way software is securely developed with GenAI.

The leader explained that the solution was built on a mature AI foundation within the

bank. The team deployed “an AI-powered platform, which translates regulations, policies

and standards … into security controls (including preventative controls, detective controls,

responsive controls and corrective controls), and then codifies those controls across the

software development life cycle.”

From there, facing a daily deluge of potential application security alerts, the bank needed an

efficient yet accurate way to identify critical vulnerabilities. To address this need, the bank’s

security operations center implemented a GenAI solution to streamline its vulnerability

management processes and systems.

Case study 1: GenAI is boosting software security in banking

35

36.

Approach

The solution triagesmillions of incoming cyberthreat alerts, paring them down to thousands

of “real threats” that then go to different cyber teams—for example, distributed denial-

of-service, malware and others. To enable that prioritization, different security control

requirements are assessed to score and reduce those alerts down to the most critical

threats based on breachability (the size of the risk) and exploitability (the likelihood of

exploitation by a threat actor).

Additionally, as GenAI is increasingly used to translate regulatory requirements, controls

can become more automated. For example, GenAI can summarize requirements such as

the need to rotate encryption keys at set intervals and identify opportunities to automate

the bank’s security protocols, or it can be used as an intelligence-gathering tool to identify

common security risks that should be automated.

For example, “Say an employee’s login credentials aren’t used for more than 30 days; AI can

detect that and disable the account,” said the leader. “This reduces cybersecurity risk by

reducing the attack surface.”

Results

When asked how to think about ROI for this type of solution, the bank leader explained, “We

calculate the cost for the potential risk against the cost of remediating this risk.” For security,

the risk economic model covers domains positively impacted / measured by the bank’s

data-driven, risk-based, decision-making process. These domains include data protection,

encryption, address in transit, in use, network segmentation, authentication, authorization,

logging and monitoring.

The solution has dramatically reduced the number of common application security

vulnerability alerts the cyber team must triage and development teams must address—

down to fewer than 10 critical vulnerabilities a day.

Overall, the GenAI solution has significantly reduced the bank’s cyber risk by enabling

its security and development teams to focus their time and effort on problems that are

real, impactful and actionable. It has also boosted morale and productivity across the

engineering team by reducing the time spent on DevSecOps so they can focus more time

on what they’re economically incentivized to do—develop new software and push critical

updates into production.

Case study 1: GenAI is boosting software security in banking

36

37.

GenAI is acceleratingsales success

in tech

Tech companies are players on both sides of the Generative AI market,

developing GenAI-based products and services they can sell to external

customers while also harnessing the power of GenAI to help their own

workers and enhance their own business processes.

Case study 2:

Return to page 8

37

38.

We spoke withthe head of Generative AI product management at a large tech company

to learn how his group is using GenAI. He described how the company uses a centralized

process to collect all internal GenAI use cases from various business units, and then

prioritizes them based on importance and feasibility. Use cases are categorized into

three types: (1) external-facing tools such as chatbots and “agentic solutions” aimed at

improving customer service; (2) internal developer tools or “co-pilots” designed to enhance

productivity; and (3) playgrounds driven by application programming interfaces (APIs) that

allow developers—including technical and business users—to build custom applications

for specific needs not covered by the other two categories. By employing a structured,

centralized approach, the company aligns GenAI projects with core business goals,

ensuring high relevance and strategic impact across multiple functions.

One compelling example from the API playground category is the firm’s accelerated sales

application, enabled by GenAI. The solution aims to make the company’s sales teams more

efficient and effective—and help them close deals faster—with an eye toward eventually

selling those same capabilities as an external product.

Problem

When it comes to selling big tech, time is money. Sales reps need to use their time wisely so

they can pursue more deals and build stronger relationships with clients. Although they have

access to detailed playbooks and other materials designed to help them sell more effectively,

sales reps struggle with inconsistent processes and dispersed resources, making it

challenging to efficiently access the available information. What’s more, sales and marketing

leaders have different intake points across different business units, which makes for a highly

variable process.

Sales reps also must be very timely when responding to a new opportunity, especially a “tight

deadline” request for proposal (RFP). “External customers often need to spend their budgets

quickly, otherwise the budget will be gone,” said the executive we interviewed. “In many

cases, the window to respond to an RFP is just three or four business days.”

Solution

The company’s new GenAI-powered sales tools have two major components. One is an RFP

response tool that allows sales reps to summarize customer requirements and expedite

the creation of responses to RFPs, allowing business leaders to more quickly generate a

complete and customized proposal with just a few mouse clicks.

The other is an interactive chatbot with access to the company’s internal knowledge base of

playbooks and other sales materials. The solution helps business leaders quickly summarize

information to better prepare for pitches. “Using the tool is very similar to other chatbot

experiences, but it’s more within our internal domain,” the executive said. “Imagine I’m a

sales rep and tell the chatbot, ‘I want to sell X, Y, Z. What is the playbook?’ And the system

responds by giving me some customized bullet points I can rehearse with myself before I

have to pitch to the client.”

Case study 2: GenAI is accelerating sales success in tech

38

39.

Approach

The overall strategyoriginated from the CEO’s dual GenAI agenda of improving internal

productivity and identifying external commercialization opportunities. This approach

included guidance to develop an internal platform that, if proven, could potentially be offered

in the marketplace to external clients facing similar challenges.

The company used a “sandbox” approach when developing the new sales tools. This gave

interested sales reps access to GenAI tools and APIs in a safe, low-cost environment so

they could experiment freely and develop new applications without writing computer code.

The solution aims to detect common customer pain points and then use those insights to

generate sales activity by identifying opportunities for commercialization or optimization.

Results

The GenAI tools seek to enhance deal closure speed and size and improve the accuracy of

proposal generation—with the ultimate goal of increasing sales performance by leveraging

internal knowledge resources more effectively.

Currently, the company is more focused on feasibility than monetary returns, using key

performance indicators (KPIs) related to efficiency and time savings. How many sales reps

are using the tool, and how long is the period between their first access and generating their

first output? If the period is short, it’s a sign the tool is both appealing and easy to use. The

earliest measure of success is onboarding.

Of course, the most important measure of success for a sales tool is its impact on sales.

In conducting direct A/B comparisons between sales processes that used the new GenAI-

powered tools and those that didn’t, the company found a marked improvement in how

quickly deals got closed when the tools were used.

Although the tools are not yet ready to be offered as external products, doing so remains a

top priority. According to the executive we interviewed, “[Our company’s] CEO would really

like us to first adopt this Generative AI platform internally and then try to think about any

way we can sell it to external customers.”

What does long-term success look like for its GenAI sales tool? The hope is for increased deal

sizes, faster deal closings, and effective deployment of a commercialized external solution.

Case study 2: GenAI is accelerating sales success in tech

39

40.

GenAI is poweringan always-on,

multimodal social media presence in

the consumer industry

Social media is an increasingly important marketing channel for all

consumer companies, allowing them to convey the voice of their brand

and reach customers in a highly compelling way.

Case study 3:

Return to page 8

40

41.

We spoke withthe senior director, head of data and analytics for a leading global consumer

company to learn how his team is activating a GenAI strategy to help the company’s brands fully

automate and expand the scope of their real-time social media trend analysis and content creation.

Problem

Social media marketing is a critical business activity that is costly, time-consuming and subject

to human bias. In a recent year, social media strategy and content generation cost the company

US$500M, with much of that spent on third-party contracts with media and creative agencies.

Solution

The company is now using GenAI to produce and manage much of its brand-focused social

media content, including copywriting and creative design previously performed by humans.

The GenAI-powered solution goes beyond replicating tasks typically handled by third-

party agencies and marketing personnel—expanding creative, targeted and personalized

marketing in ways that are faster, cheaper and more thorough.

“A recent example is the Emmys. Our brands were posting content about the event and

related viral moments,” the consumer executive said. “This content was created entirely by

GenAI models, picking up some of the trending hashtags, viral clips and news moments,

then generating a post when it fit with the brand.”

He continued, “Of course, we have strong moderation because we’re putting content out

to the public web. We have a human in the loop who monitors content, as well as systems

that use reinforcement learning from human feedback.” This highlights that—despite GenAI’s

impressive capabilities and performance—human engagement is still considered essential

to ensure content aligns with brand standards.

Case study 3: GenAI is powering an always-on, multimodal social media presence in the consumer industry

41

42.

Approach

The company builton its already strong data and AI foundation, which included years of

experience working with GenAI-related technologies such as natural language processing,

cognitive intelligence and multistep reasoning. Over the past 18 months, it has deeply

integrated LLMs and foundation models into its business, focusing on architecture,

governance and use case development—balancing build versus buy strategies to maximize

impact and value.

The company’s GenAI strategy has been to rapidly expand and prototype. “In 2023, we were

throwing a lot at the wall and seeing what stuck: lots of different providers, architectures,

models and experimentation types,” the executive said. “But in 2024, a lot of that coalesced

into a strategy we’ve now codified and defined.”

“In this case, our [proof of concept] took the shape of a pre-GenAI solution we already

had that specifically looked at a social media platform [analyzing trending influencers and

brand affinity]. Building on that existing dataset, we focused our initial effort on collecting,

cleansing, organizing and structuring the data in real time. We then took the data and threw

an LLM on top of it to see what kinds of text content it could generate. Later, we expanded

our scope to include hashtags, then a multimodal model that includes images, and now

short-form video.”

Results

In the United States, around 60% of the company’s brands are using the GenAI-powered

solution to achieve an always-on social media presence and produce relevant content with

minimal human involvement. The solution is delivering tangible benefits in three key areas.

First and foremost is increased productivity, which directly translates into substantial cost

savings. “Whether it’s a first party, second or third party, there were individuals who were

conducting these tasks, and there is a dollar value directly associated with each hour of their

time,” the executive said.

Second is increased sales, with the GenAI solution helping to boost both the incremental

number of impressions for each social media post and the monetary value created by those

impressions (due to heightened awareness, increased purchase conviction, and an easier

path to purchase).

The third is reduced media costs, particularly the cost savings that accrue when an effective

unpromoted social media post eliminates the need to pay for a promoted post—freeing up

budget that can be invested more strategically elsewhere.

Although many of these benefits have had an immediate impact on the company’s bottom

line, some of the productivity gains will take longer to fully realize because they require

formal process changes or revisions to existing annual or multiyear contracts.

Case study 3: GenAI is powering an always-on, multimodal social media presence in the consumer industry

42

43.

Authorship and Acknowledgments

Acknowledgments

Theauthors would like to thank our project sponsors and leaders Nitin Mittal, Kevin Westcott and Jeff Loucks, as well as the additional Deloitte subject matter specialists who contributed to the

development of the survey and report: Bjoern Bringmann, Lou DiLorenzo, Rohan Gupta, Kellie Nuttal, Baris Sarer, Ajay Tripathi and Ashish Verma.

We would also like to thank our team of professionals who brought this report and campaign to life, including: Ahmed Alibage, Siri Anderson, Hali Austin, Saurabh Bansode, Natasha Buckley,

Vanessa Carney, Dystnct Media, Tracy Fulham, Jordan Garrick, Gerson Lehrman Group (GLG), Karen Hogger, Susie Husted, Lisa Iliff, Wendy Jenkins, Justin Joyner, Diana Kearns-Manolatos, Lena La,

Amy Lando, Michael Lim, Cullen Marriott, Rajesh Medisetti, Adriana Mendez, Judy Freeman Mills, Melissa Neumann, Inal Olmez, Jamie Palmeroni, Jonathan Pryce, Negina Rood, Emily Rosenberg,

Kate Schmidt, Meredith Schoen, Michael Steinhart, Kelcey Strong, 10 EQS, Sandeep Vellanki, Ivana Vucenovic, Talia Wertico, Micah Whitson, Marianne Wilkinson and Sourabh Yaduvanshi.

Brenna Sniderman

Executive Director

Deloitte Center for Integrated Research

Deloitte Services LP

bsniderman@deloitte.com

Jim Rowan

Applied AI SGO Leader

Deloitte Consulting LLP

jimrowan@deloitte.com

Costi Perricos

Deloitte Global GenAI Business Leader

Deloitte LLP

cperricos@deloitte.co.uk

Beena Ammanath

Executive Director

Global Deloitte AI Institute

Deloitte LLP

bammanath@deloitte.com

Business leadership

Research leadership

David Jarvis

Senior Research Leader

Deloitte Center for Technology,

Media Telecommunications

Deloitte Services LP

davjarvis@deloitte.com

43

44.

About the DeloitteAI Institute

The Deloitte AI Institute™ helps organizations connect all the different dimensions of the robust, highly dynamic and rapidly evolving AI ecosystem. The AI

Institute leads conversations on applied AI innovation across industries, using cutting-edge insights to promote human-machine collaboration in the Age

of With™.

The Deloitte AI Institute aims to promote dialogue about and development of artificial intelligence, stimulate innovation, and examine challenges to AI

implementation and ways to address them. The AI Institute collaborates with an ecosystem composed of academic research groups, startups, entrepreneurs,

innovators, mature AI product leaders and AI visionaries to explore key areas of artificial intelligence including risks, policies, ethics, future of work and talent,

and applied AI use cases. Combined with Deloitte’s deep knowledge and experience in artificial intelligence applications, the institute helps make sense of this

complex ecosystem and, as a result, delivers impactful perspectives to help organizations succeed by making informed AI decisions.

About the Deloitte Center for Integrated Research

The Deloitte Center for Integrated Research (CIR) offers rigorously researched and data-driven perspectives on critical issues affecting businesses today. We sit

at the center of Deloitte’s industry and functional expertise, combining the leading insights from across our firm to help leaders confidently compete in today’s

ever-changing marketplace.

About the Deloitte Center for Technology, Media Telecommunications

The Deloitte Center for Technology, Media Telecommunications (TMT Center) is a world-class research organization that serves Deloitte’s TMT practice and

our clients. Our team of professional researchers produce practical foresight, fresh insights, and trustworthy data to help clients see clearly, act decisively and

compete with confidence. We create original research using a combination of rigorous methodologies and deep TMT industry knowledge.

Learn more

Learn more

Learn more

44

45.

To obtain aglobal view of how Generative AI is being adopted by organizations on the

leading edge of AI, Deloitte surveyed 2,773 leaders between July and September 2024.

Respondents were senior leaders in their organizations and included board and

C-suite members, and those at the president, vice president and director levels. The

survey sample was split equally between IT and line of business leaders. Fourteen

countries were represented: Australia (100 respondents), Brazil (115 respondents),

Canada (175 respondents), France (130 respondents), Germany (150 respondents),

India (200 respondents), Italy (75 respondents), Japan (100 respondents), Mexico (100

respondents), the Netherlands (50 respondents), Singapore (75 respondents), Spain

(100 respondents), the United Kingdom (200 respondents), and the United States

(1,203 respondents).

All participating organizations have one or more working implementations of AI

being used daily. Plus, they have pilots in place to explore Generative AI or have one

or more working implementations of Generative AI being used daily. Respondents

were required to meet one of the following criteria with respect to their organization’s

AI and data science strategy, investments, implementation approach and value

measurement: influence decision-making, are part of a team that makes decisions, are

the final decision-maker, or manage or oversee AI technology implementations.

All statistics noted in this report and its graphics are derived from Deloitte’s fourth

quarterly survey, conducted July – September 2024; The State of Generative AI in the

Enterprise: Now decides next, a report series. N (Total leader survey responses) = 2,773

The survey data was supplemented with case studies and qualitative findings

derived from 15 interviews with executives and AI and data science leaders at large

organizations across a range of industries.

Methodology

1.

Duncan Stewart, Karthik Ramachandran and Prashant Raman, “Generative AI and cyber: Big risks, but big

opportunities too,” Deloitte, November 19, 2024, https://www2.deloitte.com/us/en/insights/industry/technology/